Eagrán speisialta sa Bhulgáiris: Caibidil 11 Imleabhar 070 P. 133 - 315

Eagrán speisialta sa Rómáinis: Caibidil 11 Imleabhar 070 P. 133 - 315

Eagrán speisialta i gCróitis: Caibidil 11 Imleabhar 012 P. 16 - 196

English

Select your language

Official EU languages:

Access to European Union law

EUR-Lex

Access to European Union law

This document is an excerpt from the EUR-Lex website

Use quotation marks to search for an "exact phrase". Append an asterisk (*) to a search term to find variations of it (transp*, 32019R*). Use a question mark (?) instead of a single character in your search term to find variations of it (ca?e finds case, cane, care).

Need more search options? Use the

Advanced search

Document 21998A0330(01)

Euro-Mediterranean Agreement establishing an association between the European Communities and their Member States, of the one part, and the Republic of Tunisia, of the other part - Protocol No 1 on the arrangements applying to imports into the Community of agricultural products originating in Tunisia - Protocol No 2 on the arrangement applying to imports into the Community of fishery products originating in Tunisia - Protocol No 3 on the arrangements applying to imports into Tunisia of agricultural products originating in the Community - Protocol No 4 concerning the definition of originating products and methods of administrative cooperation - Protocol No 5 on mutual assistance in customs matters between the administrative authorities - Joint Declarations - Declarations

Euro-Mediterranean Agreement establishing an association between the European Communities and their Member States, of the one part, and the Republic of Tunisia, of the other part - Protocol No 1 on the arrangements applying to imports into the Community of agricultural products originating in Tunisia - Protocol No 2 on the arrangement applying to imports into the Community of fishery products originating in Tunisia - Protocol No 3 on the arrangements applying to imports into Tunisia of agricultural products originating in the Community - Protocol No 4 concerning the definition of originating products and methods of administrative cooperation - Protocol No 5 on mutual assistance in customs matters between the administrative authorities - Joint Declarations - Declarations

Euro-Mediterranean Agreement establishing an association between the European Communities and their Member States, of the one part, and the Republic of Tunisia, of the other part - Protocol No 1 on the arrangements applying to imports into the Community of agricultural products originating in Tunisia - Protocol No 2 on the arrangement applying to imports into the Community of fishery products originating in Tunisia - Protocol No 3 on the arrangements applying to imports into Tunisia of agricultural products originating in the Community - Protocol No 4 concerning the definition of originating products and methods of administrative cooperation - Protocol No 5 on mutual assistance in customs matters between the administrative authorities - Joint Declarations - Declarations

IO L 97, 30/03/1998, p. 2–183

(ES, DA, DE, EL, EN, FR, IT, NL, PT, FI, SV) Foilsíodh an doiciméad seo in eagrán speisialta

(BG, RO, HR)

IO L 278, 21/10/2005, p. 9–169

(CS, ET, LV, LT, HU, PL, SK, SL)

In force

In force

ELI: http://data.europa.eu/eli/agree_internation/1998/238/oj

Language

HTML

PDF

Official Journal

|

30.3.1998 |

EN |

Official Journal of the European Communities |

L 97/2 |

EURO-MEDITERRANEAN AGREEMENT

establishing an association between the European Communities and their Member States, of the one part, and the Republic of Tunisia, of the other part

THE KINGDOM OF BELGIUM,

THE KINGDOM OF DENMARK,

THE FEDERAL REPUBLIC OF GERMANY,

THE HELLENIC REPUBLIC,

THE KINGDOM OF SPAIN,

THE FRENCH REPUBLIC,

IRELAND,

THE ITALIAN REPUBLIC,

THE GRAND DUCHY OF LUXEMBOURG,

THE KINGDOM OF THE NETHERLANDS,

THE REPUBLIC OF AUSTRIA,

THE PORTUGUESE REPUBLIC,

THE REPUBLIC OF FINLAND,

THE KINGDOM OF SWEDEN,

THE UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND,

Contracting Parties to the Treaty establishing the European Community and the Treaty establishing the European Coal and Steel Community, hereinafter referred to as the ‘Member States’, and

THE EUROPEAN COMMUNITY,

THE EUROPEAN COAL AND STEEL COMMUNITY,

hereinafter referred to as ‘the Community’, of the one part, and

THE REPUBLIC OF TUNISIA,

hereinafter referred to as ‘Tunisia’, of the other part,

CONSIDERING the importance of the existing traditional links between the Community, its Member States and Tunisia and the common values that the Contracting Parties share;

CONSIDERING that the Community, its Member States and Tunisia wish to strengthen those links and to establish lasting relations, based on reciprocity, partnership and co-development;

CONSIDERING the importance which the Parties attach to the principles of the United Nations Charter, particularly the observance of human rights and political and economic freedom, which form the very basis of the Association;

CONSIDERING recent political and economic developments both on the European continent and in Tunisia;

CONSIDERING the considerable progress made by Tunisia and its people towards achieving their objectives of full integration of the Tunisian economy in the world economy and participation in the community of democratic nations;

CONSCIOUS of the importance of this Agreement, based on cooperation and dialogue, for lasting stability and security in the Euro-Mediterranean region;

CONSCIOUS, on the one hand, of the importance of relations in an overall Euro-Mediterranean context and, on the other, of the objective of integration between the countries of the Maghreb;

BEARING IN MIND the economic and social disparities between the Community and Tunisia and desirous of achieving the objectives of this association through the appropriate provisions of this Agreement;

DESIROUS of establishing and developing regular political dialogue on bilateral and international issues of mutual interest;

TAKING ACCOUNT of the Community's willingness to provide Tunisia with decisive support in its endeavours to bring about economic reform, structural adjustment and social development;

CONSIDERING the commitment of both the Community and Tunisia to free trade, in compliance with the rights and obligations arising out of the General Agreement on Tariffs and Trade (GATT);

DESIROUS of establishing cooperation sustained by regular dialogue on economic, social and cultural issues in order to achieve better mutual understanding;

CONVINCED that this Agreement will create a climate conducive to the development of their economic relations, in particular in the fields of trade and investment, the key sectors for economic restructuring and technological modernisation,

HAVE AGREED AS FOLLOWS:

Article 1

1. An association is hereby established between the Community and its Member States, of the one part, and Tunisia, of the other part.

2. The aims of this Agreement are to:

|

— |

provide an appropriate framework for political dialogue between the Parties, allowing the development of close relations in all areas they consider relevant to such dialogue, |

|

— |

establish the conditions for the gradual liberalisation of trade in goods, services and capital, |

|

— |

promote trade and the expansion of harmonious economic and social relations between the Parties, notably through dialogue and cooperation, so as to foster the development and prosperity of Tunisia and its people, |

|

— |

encourage integration of the Maghreb countries by promoting trade and cooperation between Tunisia and other countries of the region, |

|

— |

promote economic, social, cultural and financial cooperation. |

Article 2

Relations between the Parties, as well as all the provisions of the Agreement itself, shall be based on respect for human rights and democratic principles which guide their domestic and international policies and constitute an essential element of the Agreement.

TITLE I

POLITICAL DIALOGUE

Article 3

1. A regular political dialogue shall be established between the Parties. It shall help build lasting links of solidarity between the partners which will contribute to the prosperity, stability and security of the Mediterranean region and bring about a climate of understanding and tolerance between cultures.

2. Political dialogue and cooperation are intended in particular to:

|

(a) |

facilitate rapprochement between the Parties through the development of better mutual understanding and regular coordination on international issues of common interest; |

|

(b) |

enable each Party to consider the position and interests of the other; |

|

(c) |

contribute to consolidating security and stability in the Mediterranean region and in the Maghreb in particular; |

|

(d) |

help develop joint initiatives. |

Article 4

Political dialogue shall cover all issues of common interest to the Parties, in particular the conditions required to ensure peace, security and regional development through support for cooperation, notably within the Maghreb group of countries.

Article 5

Political dialogue shall be established at regular intervals and whenever necessary notably:

|

(a) |

at ministerial level, principally within the Association Council; |

|

(b) |

at the level of senior officials representing Tunisia, on the one hand, and the Council Presidency and the Commission on the other; |

|

(c) |

taking full advantage of all diplomatic channels including regular briefings, consultations on the occasion of international meetings and contacts between diplomatic representatives in third countries; |

|

(d) |

where appropriate, by any other means which would make a useful contribution to consolidating dialogue and increasing its effectiveness. |

TITLE II

FREE MOVEMENT OF GOODS

Article 6

The Community and Tunisia shall gradually establish a free trade area over a transitional period lasting a maximum of 12 years starting from the date of the entry into force of this Agreement in accordance with the provisions of this Agreement and in conformity with those of the General Agreement on Tariffs and Trade 1994 and the other multilateral Agreements on trade in goods annexed to the Agreement establishing the WTO, hereinafter referred to as the GATT.

CHAPTER I

INDUSTRIAL PRODUCTS

Article 7

The provisions of this Chapter shall apply to products originating in the Community and Tunisia with the exception of the products referred to in Annex II to the Treaty establishing the European Community.

Article 8

No new customs duties on imports nor charges having equivalent effect shall be introduced in trade between the Community and Tunisia.

Article 9

Products originating in Tunisia shall be imported into the Community free of customs duties and charges having equivalent effect and without quantitative restrictions or measures having equivalent effect.

Article 10

1. The provisions of this Chapter shall not preclude the retention by the Community of an agricultural component on imports of the goods originating in Tunisia listed in Annex 1.

The agricultural component shall reflect differences between the price on the Community market of the agricultural products considered as being used in the production of such goods and the price of imports from third countries where the total cost of the said basic products is higher in the Community. The agricultural component may take the form of a fixed amount or an ad valorem duty. Such differences shall be replaced, where appropriate, by specific duties based on tariffication of the agricultural component or by ad valorem duties.

The provisions of Chapter 2 applicable to agricultural products shall apply mutatis mutandis to the agricultural component.

2. The provisions of this Chapter shall not preclude the separate specification by Tunisia of an agricultural component in the import duties in force on the products listed in Annex 2 originating in the Community. The agricultural component may take the form of a fixed amount or an ad valorem duty.

The provisions of Chapter 2 applicable to agricultural products shall apply mutatis mutandis to the agricultural component.

3. In the case of the products shown in Annex 2, list 1, originating in the Community, Tunisia shall apply upon the entry into force of this Agreement import duties and charges having equivalent effect no greater than those in force on 1 January 1995, within the limits of the tariff quotas shown in that list.

During elimination of the industrial component of the duties pursuant to paragraph 4, the level of the duties to be applied in respect of the products for which the tariff quotas are to be abolished may not be higher than the level of the duties in force on 1 January 1995.

4. In the case of the products in Annex 2, list 2, originating in the Community, Tunisia shall eliminate the industrial component of the duties in accordance with the provisions laid down in Article 11 (3) of the Agreement in respect of products in Annex 4.

In the case of the products in Annex 2, lists 1 and 3, originating in the Community, Tunisia shall eliminate the industrial component of the duties in accordance with the provisions laid down in Article 11 (3) of the Agreement in respect of products in Annex 5.

5. The agricultural components applied pursuant to paragraphs 1 and 2 may be reduced where, in trade between the Community and Tunisia, the charge applicable to a basic agricultural product is reduced or where such reductions are the result of mutual concessions relating to processed agricultural products.

6. The reduction referred to in paragraph 5, the list of products concerned and, where appropriate, the tariff quotas within which the reduction applies shall be established by the Association Council.

Article 11

1. Customs duties and charges having equivalent effect applicable on import into Tunisia of products originating in the Community other than those listed in Annexes 3 to 6 shall be abolished upon the entry into force of this Agreement.

2. Customs duties and charges having equivalent effect applicable on import into Tunisia of the products originating in the Community listed in Annex 3 shall be progressively abolished in accordance with the following timetable:

On the date of entry into force of this Agreement each duty and charge shall be reduced to 85 % of the basic duty;

One year after the date of entry into force of this Agreement each duty and charge shall be reduced to 70 % of the basic duty;

Two years after the date of entry into force of this Agreement each duty and charge shall be reduced to 55 % of the basic duty;

Three years after the date of entry into force of this Agreement each duty and charge shall be reduced to 40 % of the basic duty;

Four years after the date of entry into force of this Agreement each duty and charge shall be reduced to 25 % of the basic duty;

Five years after the date of entry into force of this Agreement the remaining duties shall be abolished.

3. Customs duties and charges having equivalent effect applicable on import into Tunisia of the products originating in the Community listed in Annexes 4 and 5 shall be progressively abolished in accordance with the following timetables:

In the case of the list appearing in Annex 4:

On the date of entry into force of this Agreement each duty and charge shall be reduced to 92 % of the basic duty;

One year after the date of entry into force of this Agreement each duty and charge shall be reduced to 84 % of the basic duty;

Two years after the date of entry into force of this Agreement each duty and charge shall be reduced to 76 % of the basic duty;

Three years after the date of entry into force of this Agreement each duty and charge shall be reduced to 68 % of the basic duty;

Four years after the date of entry into force of this Agreement each duty and charge shall be reduced to 60 % of the basic duty;

Five years after the date of entry into force of this Agreement each duty and charge shall be reduced to 52 % of the basic duty;

Six years after the date of entry into force of this Agreement each duty and charge shall be reduced to 44 % of the basic duty;

Seven years after the date of entry into force of this Agreement each duty and charge shall be reduced to 36 % of the basic duty;

Eight years after the date of entry into force of this Agreement each duty and charge shall be reduced to 28 % of the basic duty;

Nine years after the date of entry into force of this Agreement each duty and charge shall be reduced to 20 % of the basic duty;

Ten years after the date of entry into force of this Agreement each duty and charge shall be reduced to 12 % of the basic duty;

Eleven years after the date of entry into force of this Agreement each duty and charge shall be reduced to 4 % of the basic duty;

Twelve years after the date of entry into force of this Agreement the remaining duties shall be abolished.

In the case of the list appearing in Annex 5:

Four years after the date of entry into force of this Agreement each duty and charge shall be reduced to 88 % of the basic duty;

Five years after the date of entry into force of this Agreement each duty and charge shall be reduced to 77 % of the basic duty;

Six years after the date of entry into force of this Agreement each duty and charge shall be reduced to 66 % of the basic duty;

Seven years after the date of entry into force of this Agreement each duty and charge shall be reduced to 55 % of the basic duty;

Eight years after the date of entry into force of this Agreement each duty and charge shall be reduced to 44 % of the basic duty;

Nine years after the date of entry into force of this Agreement each duty and charge shall be reduced to 33 % of the basic duty;

Ten years after the date of entry into force of this Agreement each duty and charge shall be reduced to 22 % of the basic duty;

Eleven years after the date of entry into force of this Agreement each duty and charge shall be reduced to 11 % of the basic duty;

Twelve years after the date of entry into force of this Agreement the remaining duties shall be abolished.

4. In the event of serious difficulties for a given product, the relevant timetables in accordance with paragraph 3 may be reviewed by the Association Committee by common accord on the understanding that the schedule for which the review has been requested may not be extended in respect of the product concerned beyond the maximum transitional period of 12 years. If the Association Committee has not taken a decision within thirty days of its application to review the timetable, Tunisia may suspend the timetable provisionally for a period which may not exceed one year.

5. For each product the basic duty to which the successive reductions laid down in paragraphs 2 and 3 are to be applied shall be that actually applied vis-à-vis the Community on 1 January 1995.

6. If, after 1 January 1995, any tariff reduction is applied on an erga omnes basis, the reduced duties shall replace the basic duties referred to in paragraph 5 as from the date when such reductions are applied.

7. Tunisia shall communicate its basic duties to the Community.

Article 12

The provisions of Articles 10, 11 and 19(b) shall not apply to products in the list appearing in Annex 6. The arrangements to be applied to such products shall be re-examined by the Association Council four years after the Agreement's entry into force.

Article 13

The provisions concerning the abolition of customs duties on imports shall also apply to customs duties of a fiscal nature.

Article 14

1. Exceptional measures of limited duration which derogate from the provisions of Article 11 may be taken by Tunisia in the form of an increase or reintroduction of customs duties.

These measures may only concern infant industries, or certain sectors undergoing restructuring or facing serious difficulties, particularly where these difficulties produce major social problems.

Customs duties on imports applicable in Tunisia to products originating in the Community introduced by these measures may not exceed 25 % ad valorem and shall maintain an element of preference for products originating in the Community. The total value of imports of the products which are subject to these measures may not exceed 15% of total imports of industrial products from the Community during the last year for which statistics are available.

These measures shall be applied for a period not exceeding five years unless a longer duration is authorised by the Association Committee. They shall cease to apply at the latest on the expiry of the maximum transitional period of twelve years.

No such measures can be introduced in respect of a product if more than three years have elapsed since the elimination of all duties and quantitative restrictions or charges or measures having equivalent effect concerning that product.

Tunisia shall inform the Association Committee of any exceptional measures it intends to take and, at the request of the Community, consultations shall be held on such measures and the sectors to which they apply before they are implemented. When taking such measures Tunisia shall provide the Committee with a timetable for the elimination of the customs duties introduced under this Article. This timetable shall provide for a phasing-out of these duties in equal annual instalments starting at the latest two years after their introduction. The Association Committee may decide on a different timetable.

2. By way of derogation from the fourth subparagraph of paragraph 1, the Association Committee may exceptionally, in order to take account of the difficulties involved in setting up a new industry, authorise Tunisia to maintain the measures already taken pursuant to paragraph 1 for a maximum period of three years beyond the twelve-year transitional period.

CHAPTER II

AGRICULTURAL AND FISHERY PRODUCTS

Article 15

The provisions of this Chapter shall apply to the products originating in the Community and Tunisia listed in Annex II to the Treaty establishing the European Community.

Article 16

The Community and Tunisia shall gradually implement greater liberalisation of their reciprocal trade in agricultural and fishery products.

Article 17

1. Agricultural and fishery products originating in Tunisia shall benefit on import into the Community from the provisions set out in Protocols Nos 1 and 2 respectively.

2. Agricultural products originating in the Community shall benefit on import into Tunisia from the provisions set out in Protocol No 3.

Article 18

1. From 1 January 2000 the Community and Tunisia shall assess the situation with a view to determining the liberalisation measures to be applied by the Community and Tunisia with effect from 1 January 2001 in accordance with the objective set out in Article 16.

2. Without prejudice to the provisions of the preceding paragraph and taking account of the patterns of trade in agricultural products between the Parties and the particular sensitivity of such products, the Community and Tunisia will examine on a regular basis in the Association Council, product by product and on a reciprocal basis, the possibilities of granting each other further concessions.

CHAPTER III

COMMON PROVISIONS

Article 19

Without prejudice to the provisions of the GATT:

|

(a) |

no new quantitative restriction on imports or measure having equivalent effect shall be introduced in trade between the Community and Tunisia; |

|

(b) |

quantitative restrictions on imports and measures having equivalent effect in trade between Tunisia and the Community shall be abolished upon the entry into force of this Agreement; |

|

(c) |

the Community and Tunisia shall apply to the other's exports customs neither duties or charges having equivalent effect nor quantitative restrictions or measures of equivalent effect. |

Article 20

1. Should specific rules be introduced as a result of implementation of their agricultural policies or modification of their existing rules, or should the provisions on the implementation of their agricultural policies be modified or developed, the Community and Tunisia may modify the arrangements laid down in the Agreement in respect of the products concerned.

The Party carrying out such modification shall inform the Association Committee thereof. At the request of the other Party, the Association Committee shall meet to take appropriate account of that Party's interests.

2. If the Community or Tunisia, in applying paragraph 1, modifies the arrangements made by this Agreement for agricultural products, they shall accord imports originating in the other Party an advantage comparable to that provided for in this Agreement.

3. Any modification of the arrangements made by this Agreement shall be the subject, at the request of the other Contracting Party, of consultations within the Association Council.

Article 21

Products originating in Tunisia shall not enjoy more favourable treatment when imported into the Community than that applied by Member States among themselves.

The provisions of this Agreement shall apply without prejudice to the provisions of Council Regulation (EEC) No 1911/91 of 26 June 1991 on the application of the provisions of Community law to the Canary Islands.

Article 22

1. The two Parties shall refrain from any measures or practice of an internal fiscal nature establishing, whether directly or indirectly, discrimination between the products of one Party and like products originating in the territory of the other Party.

2. Products exported to the territory of one of the Parties may not benefit from repayment of indirect internal taxation in excess of the amount of indirect taxation imposed on them directly or indirectly.

Article 23

1. This Agreement shall not preclude the maintenance or establishment of customs unions, free trade areas or arrangements for frontier trade insofar as they do not have the effect of altering the trade arrangements provided for in this Agreement.

2. Consultations between the Parties shall take place within the Association Committee concerning agreements establishing customs unions or free trade areas and, where appropriate, on other major issues related to their respective trade policies with third countries. In particular in the event of a third country acceding to the Community, such consultations shall take place so as to ensure that account is taken of the mutual interests of the Community and Tunisia stated in this Agreement.

Article 24

If one of the Parties finds that dumping is taking place in trade with the other Party within the meaning of Article VI of the General Agreement on Tariffs and Trade, it may take appropriate measures against this practice in accordance with the Agreement relating to the application of Article VI of the General Agreement on Tariffs and Trade, related internal legislation and the conditions and procedures laid down in Article 27.

Article 25

Where any product is being imported in such increased quantities and under such conditions as to cause or threaten to cause:

|

— |

serious injury to domestic producers of like or directly competitive products in the territory of one of the Contracting Parties, or |

|

— |

serious disturbances in any sector of the economy or difficulties which could bring about serious deterioration in the economic situation of a region, |

the Community or Tunisia may take appropriate measures under the conditions and in accordance with the procedures laid down in Article 27.

Article 26

Where compliance with the provisions of Article 19(c) leads to:

|

(i) |

re-export to a third country of a product against which the exporting Party maintains quantitative export restrictions, export duties or measures or charges having equivalent effect; or |

|

(ii) |

a serious shortage, or threat thereof, of a product essential to the exporting Party, |

and where the situations referred to above give rise, or are likely to give rise, to major difficulties for the exporting Party, that Party may take appropriate measures under the conditions and in accordance with the procedures laid down in Article 27. The measures shall be non-discriminatory and shall be eliminated when conditions no longer justify their maintenance.

Article 27

1. In the event of the Community or Tunisia subjecting imports of products liable to give rise to the difficulties referred to in Article 25 to an administrative procedure having as its purpose the rapid supply of information on trade flow trends, it shall inform the other Party.

2. In the cases specified in Articles 24, 25 and 26, before taking the measures provided for therein or, in cases to which paragraph 3(d) applies, as soon as possible, the Community or Tunisia, as the case may be, shall supply the Association Committee with all relevant information with a view to seeking a solution acceptable to the two Parties.

In the selection of measures, priority shall be given to those which least disturb the functioning of this Agreement.

The safeguard measures shall be immediately notified to the Association Committee by the Party concerned and shall be the subject of periodic consultations, particularly with a view to their abolition as soon as circumstances permit.

3. For the implementation of paragraph 2, the following provisions shall apply:

|

(a) |

as regards Article 24, the exporting Party shall be informed of the dumping case as soon as the authorities of the importing Party have initiated an investigation. When no end has been put to the dumping within the meaning of Article VI of the GATT or no other satisfactory solution has been reached within 30 days of the matter being referred, the importing Party may adopt the appropriate measures; |

|

(b) |

as regards Article 25, the difficulties arising from the situation referred to in that Article shall be referred for examination to the Association Committee, which may take any decision needed to put an end to such difficulties. If the Association Committee or the exporting Party has not taken a decision putting an end to the difficulties or no other satisfactory solution has been reached within 30 days of the matter being referred, the importing Party may adopt the appropriate measures to remedy the problem. These measures shall not exceed the scope of what is necessary to remedy the difficulties which have arisen; |

|

(c) |

as regards Article 26, the difficulties arising from the situations referred to in that Article shall be referred for examination to the Association Committee. The Association Committee may take any decision needed to put an end to the difficulties. If it has not taken such a decision within 30 days of the matter being referred to it, the exporting Party may apply appropriate measures to exports of the product concerned; |

|

(d) |

where exceptional circumstances requiring immediate action make prior information or examination, as the case may be, impossible, the Community or Tunisia, whichever is concerned, may, in the situations specified in Articles 24, 25 and 26, apply forthwith the precautionary measures strictly necessary to deal with the situation and shall inform the other Party immediately thereof. |

Article 28

The Agreement shall not preclude prohibitions or restrictions on imports, exports or goods in transit justified on grounds of public morality, public policy or public security; the protection of health and life of humans, animals or plants; the protection of national treasures of artistic, historic or archaeological value or the protection of intellectual, industrial and commercial property of rules relating to gold and silver. Such prohibitions or restrictions shall not, however, constitute a means of arbitrary discrimination or a disguised restriction on trade between the Parties.

Article 29

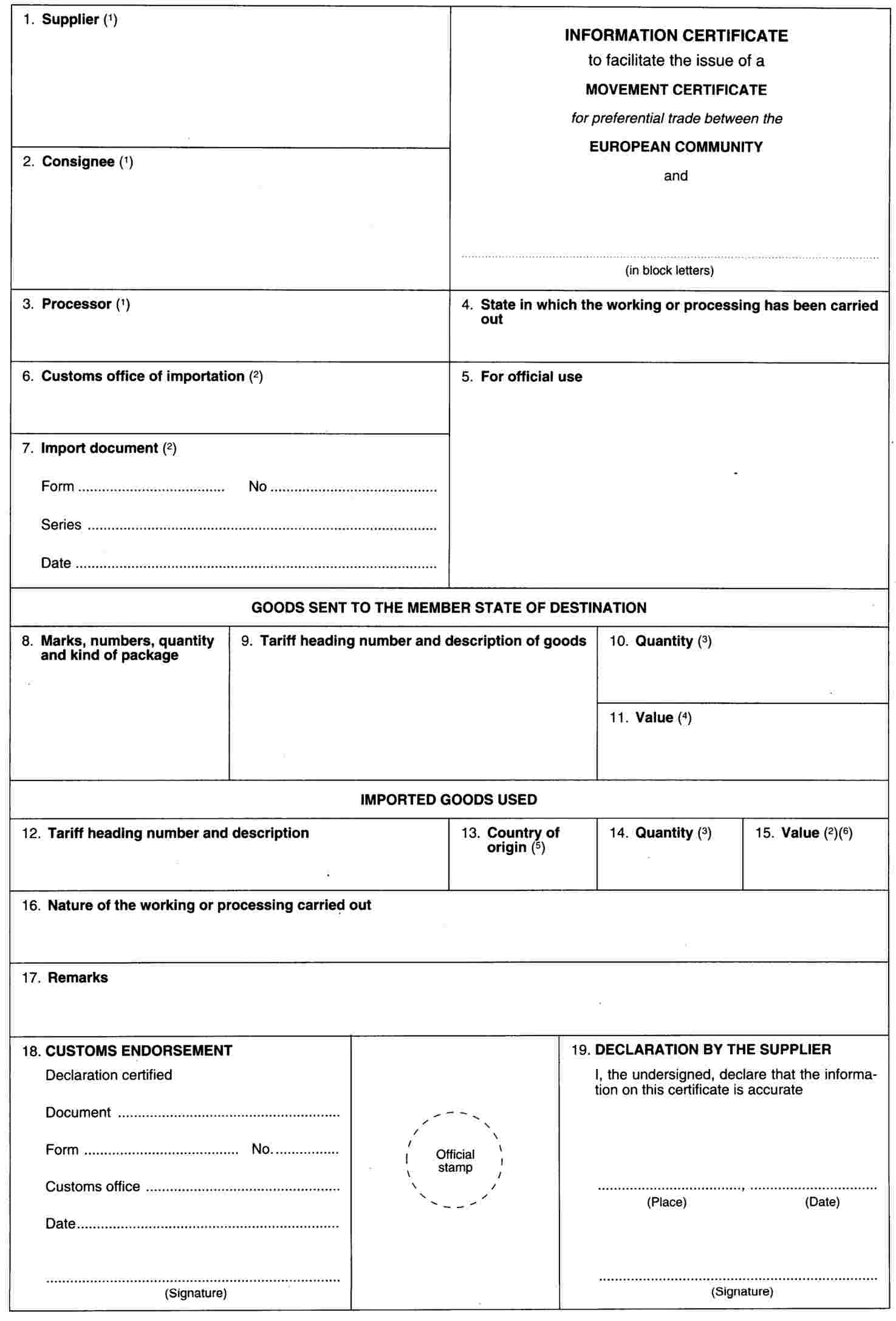

The concept of ‘originating products’ for the purposes of implementing this Title and the methods of administrative cooperation relating thereto are laid down in Protocol No 4.

Article 30

The Combined Nomenclature of goods shall be applied to the classification of goods in trade between the two Parties.

TITLE III

RIGHT OF ESTABLISHMENT AND SERVICES

Article 31

1. The Parties agree to widen the scope of the Agreement to cover the right of establishment of one Party's firms on the territory of the other and liberalisation of the provision of services by one Party's firms to consumers of services in the other.

2. The Association Council will make recommendations for achieving the objective described in paragraph 1.

In making such recommendations, the Association Council will take account of past experience of implementation of reciprocal most-favoured-nation treatment and of the respective obligations of each Party under the General Agreement on Trade in Services annexed to the Agreement establishing the WTO, hereinafter referred to as the ‘GATS’, particularly those in Article V of the latter.

3. The Association Council will make a first assessment of the achievement of this objective no later than five years after the Agreement enters into force.

Article 32

1. At the outset, each of the Parties shall reaffirm its obligations under the GATS, particularly the obligation to grant reciprocal most-favoured-nation treatment in the service sectors covered by that obligation.

2. In accordance with the GATS, such treatment shall not apply to:

|

(a) |

advantages granted by either Party under the terms of an agreement of the type defined in Article V of the GATS or to measures taken on the basis of such an agreement; |

|

(b) |

other advantages granted in accordance with the list of exemptions from most-favoured-nation treatment annexed by either Party to the GATS. |

TITLE IV

PAYMENTS, CAPITAL, COMPETITION AND OTHER ECONOMIC PROVISIONS

CHAPTER I

CURRENT PAYMENTS AND MOVEMENT OF CAPITAL

Article 33

Subject to the provisions of Article 35, the Parties undertake to allow all current payments for current transactions to be made in a freely convertible currency.

Article 34

1. With regard to transactions on the capital account of balance of payments, the Community and Tunisia shall ensure, from the entry into force of this Agreement, that capital relating to direct investments in Tunisia in companies formed in accordance with current laws can move freely and that the yield from such investments and any profit stemming therefrom can be liquidated and repatriated.

2. The Parties shall consult each other with a view to facilitating, and fully liberalising when the time is right, the movement of capital between the Community and Tunisia.

Article 35

Where one or more Member States of the Community, or Tunisia, is in serious balance of payments difficulties, or under threat thereof, the Community or Tunisia, as the case may be, may, in accordance with the conditions established under the General Agreement on Tariffs and Trade and Articles VIII and XIV of the Articles of Agreement of the International Monetary Fund, adopt restrictions on current transactions which shall be of limited duration and may not go beyond what is strictly necessary to remedy the balance of payments situation. The Community or Tunisia, as the case may be, shall inform the other Party forthwith and shall submit to it as soon as possible a timetable for the elimination of the measures concerned.

CHAPTER II

COMPETITION AND OTHER ECONOMIC PROVISIONS

Article 36

1. The following are incompatible with the proper functioning of the Agreement, insofar as they may affect trade between the Community and Tunisia:

|

(a) |

all agreements between undertakings, decisions by associations of undertakings and concerted practices between undertakings which have as their object or effect the prevention, restriction or distortion of competition; |

|

(b) |

abuse by one or more undertakings of a dominant position in the territories of the Community or of Tunisia as a whole or in a substantial part thereof; |

|

(c) |

any official aid which distorts or threatens to distort competition by favouring certain undertakings or the production of certain goods, with the exception of cases in which a derogation is allowed under the Treaty establishing the European Coal and Steel Community. |

2. Any practices contrary to this Article shall be assessed on the basis of criteria arising from the application of the rules of Articles 85, 86 and 92 of the Treaty establishing the European. Community and, in the case of products falling within the scope of the European Coal and Steel Community, the rules of Articles 65 and 66 of the Treaty establishing that Community, and the rules relating to state aid, including secondary legislation.

3. The Association Council shall, within five years of the entry into force of this Agreement, adopt the necessary rules for the implementation of paragraphs 1 and 2.

Until these rules are adopted, the provisions of the Agreement on interpretation and application of Articles VI, XVI and XXIII of the General Agreement on Tariffs and Trade shall be applied as the rules for the implementation of paragraph l(c) and related parts of paragraph 2.

|

4. |

|

5. With regard to products referred to in Chapter II of Title II:

|

— |

the provisions of paragraph l(c) do not apply, |

|

— |

any practices contrary to paragraph 1(a) shall be assessed according to the criteria established by the Community on the basis of Articles 42 and 43 of the Treaty establishing the European Community, and in particular those established in Council Regulation No 26/62. |

6. If the Community or Tunisia considers that a particular practice is incompatible with the terms of paragraph 1, and:

|

— |

is not adequately dealt with under the implementing rules referred to in paragraph 3, or |

|

— |

in the absence of such rules, and if such practice causes or threatens to cause serious prejudice to the interest of the other Party or material injury to its domestic industry, including its services industry, |

it may take appropriate measures after consultation within the Association Committee or after 30 working days following referral to that Committee.

In the case of practices incompatible with paragraph l(c) of this Article, such appropriate measures may, where the General Agreement on Tariffs and Trade applies thereto, only be adopted in accordance with the procedures and under the conditions laid down by the General Agreement on Tariffs and Trade and any other relevant instrument negotiated under its auspices which is applicable between the Parties.

7. Notwithstanding any provisions to the contrary adopted in accordance with paragraph 3, the Parties shall exchange information taking into account the limitations imposed by the requirements of professional and business secrecy.

Article 37

The Member States and Tunisia shall progressively adjust, without affecting commitments made unter the GATT, any state monopolies of a commercial character so as to ensure that, by the end of the fifth year following the entry into force of this Agreement, no discrimination regarding the conditions under which goods are procured and marketed exists between nationals of the Member States and of Tunisia. The Association Committee will be informed about the measures adopted to implement this objective.

Article 38

With regard to public enterprises and enterprises which have been granted special or exclusive rights, the Association Council shall ensure, from the fifth year following the entry into force of the Agreement, that no measures which disturbs trade between the Community and Tunisia in a manner which runs counter to the interests of the Parties is adopted or maintained. This provision shall not impede the performance in fact or in law of the specific functions assigned to those enterprises.

Article 39

1. The Parties shall provide suitable and effective protection of intellectual, industrial and commercial property rights, in line with the highest international standards. This shall encompass effective means of enforcing such rights.

2. Implementation of this Article and of Annex 7 shall be regularly assessed by the Parties. If difficulties which affect trade arise in connection with intellectual, industrial and commercial property rights, either Party may request urgent consultations to find mutually satisfactory solutions.

Article 40

1. The Parties shall take appropriate steps to promote the use by Tunisia of Community technical rules and European standards for industrial and agri-food products and certification procedures.

2. Using the principles set out in paragraph 1 as a basis, the Parties shall, when the circumstances are right, conclude agreements for the mutual recognition of certifications.

Article 41

1. The Parties shall set as their objective a reciprocal and gradual liberalisation of public procurement contracts.

2. The Association Council shall take the steps necessary to implement paragraph 1.

TITLE V

ECONOMIC COOPERATION

Article 42

Objectives

1. The Parties undertake to step up economic cooperation in their mutual interest and in the spirit of partnership which is at the root of this Agreement.

2. The objective of economic cooperation shall be to support Tunisia's own efforts to achieve sustainable economic and social development.

Article 43

Scope

1. Cooperation will be targeted first and foremost at areas of activity suffering the effects of internal constraints and difficulties or affected by the process of liberalising Tunisia's economy as a whole, and more particularly by the liberalisation of trade between Tunisia and the Community.

2. Similarly, cooperation shall focus on areas likely to bring the economies of the Community and Tunisia closer together, particularly those which will generate growth and employment.

3. Cooperation shall foster economic integration within the Maghreb using any measures likely to further such relations within the region.

4. Preservation of the environment and ecological balances shall constitute a central component of the various fields of economic cooperation.

5. Where appropriate, the Parties shall determine by agreement other fields of economic cooperation.

Article 44

Methods

Economic cooperation shall involve methods including:

|

(a) |

regular economic dialogue between the two Parties covering all aspects of macroeconomic policy; |

|

(b) |

communication and exchanges of information; |

|

(c) |

advice, use of the services of experts and training; |

|

(d) |

joint ventures; |

|

(e) |

assistance with technical, administrative and regulatory matters. |

Article 45

Regional cooperation

In order to make the most of this Agreement, the Parties shall foster all activities which have a regional impact or involve third countries, notably:

|

(a) |

intra-regional trade within the Maghreb; |

|

(b) |

environmental matters; |

|

(c) |

the development of economic infrastructure; |

|

(d) |

research in science and technology; |

|

(e) |

cultural matters; |

|

(f) |

customs matters; |

|

(g) |

regional institutions and the establishment of common or harmonised programmes and policies. |

Article 46

Education and training

The aim of cooperation shall be to:

|

(a) |

find ways to bring about a significant improvement in education and training, including vocational training; |

|

(b) |

place special emphasis on giving the female population access to education, including technical training, higher education and vocational training; |

|

(c) |

encourage the establishment of lasting links between specialist bodies on the Parties' territories in order to pool and exchange experience and methods. |

Article 47

Scientific, technical and technological cooperation

The aim of cooperation shall be to:

|

(a) |

encourage the establishment of permanent links between the Parties' scientific communities, notably by means of:

|

|

(b) |

improve Tunisia's research capabilities; |

|

(c) |

stimulate technological innovation and the transfer of new technology and know-how; |

|

(d) |

encourage all activities aimed at establishing synergy at regional level. |

Article 48

Environment

The aim of cooperation shall be to prevent deterioration of the environment, to improve the quality of the environment, to protect human health and to achieve rational use of natural resources for sustainable development.

The Parties undertake to cooperate in areas including:

|

(a) |

soil and water quality; |

|

(b) |

the consequences of development, particularly industrial development (especially safety of installations and waste); |

|

(c) |

monitoring and preventing pollution of the sea. |

Article 49

Industrial cooperation

The aim of cooperation shall be to:

|

(a) |

encourage cooperation between the Parties' economic operators, including cooperation in the context of access for Tunisia to Community business networks and decentralised cooperation networks; |

|

(b) |

back the effort to modernise and restructure Tunisia's public and private sector industry (including the agri-food industry); |

|

(c) |

foster an environment which favours private initiative, with the aim of stimulating and diversifying output for the domestic and export markets; |

|

(d) |

make the most of Tunisia's human resources and industrial potential through better use of policy in the fields of innovation and research and technological development; |

|

(e) |

facilitate access to credit to finance investment. |

Article 50

Promotion and protection of investment

The aim of cooperation shall be to create a favourable climate for flows of investment, and to use the following in particular:

|

(a) |

the establishment of harmonised and simplified procedures, co-investment machinery (especially to link small and medium-sized enterprises) and methods of identifying and providing information on investment opportunities; |

|

(b) |

the establishment, where appropriate, of a legal framework to promote investment, chiefly through the conclusion by Tunisia and the Member States of investment protection agreements and agreements preventing double taxation. |

Article 51

Cooperation in standardisation and conformity assessment

The Parties shall cooperate in developing:

|

(a) |

the use of Community rules in standardisation, metrology, quality control and conformity assessment; |

|

(b) |

the updating of Tunisian laboratories, leading eventually to the conclusion of mutual recognition agreements for conformity assessment; |

|

(c) |

the bodies responsible for intellectual, industrial and commercial property and for standardisation and quality in Tunisia. |

Article 52

Approximation of legislation

Cooperation shall be aimed at helping Tunisia to bring its legislation closer to that of the Community in the areas covered by this Agreement.

Article 53

Financial services

The aim of cooperation shall be to achieve closer common rules and standards in areas including the following:

|

(a) |

bolstering and restructuring Tunisia's financial sectors; |

|

(b) |

improving accounting, auditing, supervision and regulation of financial services and financial monitoring in Tunisia. |

Article 54

Agriculture and fisheries

The aim of cooperation shall be to:

|

(a) |

modernise and restructure agriculture and fisheries through methods including the modernisation of infrastructure and equipment, the development of packaging and storage techniques and the improvement of private distribution and marketing chains; |

|

(b) |

diversify output and external markets; |

|

(c) |

achieve cooperation in health, plant health and growing techniques. |

Article 55

Transport

The aim of cooperation shall be to:

|

(a) |

achieve the restructuring and modernisation of road, rail, port and airport infrastructure of common interest, in correlation with major trans-European communication routes; |

|

(b) |

define and apply operating standards comparable to those found in the Community; |

|

(c) |

bring equipment up to Community standards, particularly where multimodal transport, containerisation and transhipment are concerned; |

|

(d) |

gradually improve road transit and the management of airports, air traffic and railways. |

Article 56

Telecommunications and information technology

Cooperation shall focus on:

|

(a) |

telecommunications in general; |

|

(b) |

standardisation, conformity testing and certification for information technology and telecommunications; |

|

(c) |

dissemination of new information technologies, particularly in relation to networks and the interconnection of networks (ISDN — integrated services digital networks — and EDI — electronic data interchange); |

|

(d) |

stimulating research on and development of new communication and information technology facilities to develop the market in equipment, services and applications related to information technology and to communications, services and installations. |

Article 57

Energy

Cooperation shall focus on:

|

(a) |

renewable energy; |

|

(b) |

promoting the saving of energy; |

|

(c) |

applied research relating to networks of databases linking the two Parties' economic and social operators; |

|

(d) |

backing efforts to modernise and develop energy networks and the interconnection of such networks with Community networks. |

Article 58

Tourism

The aim of cooperation shall be to develop tourism, particularly with regard to:

|

(a) |

catering management and quality of service in the various fields connected with catering; |

|

(b) |

development of marketing; |

|

(c) |

promotion of tourism for young people. |

Article 59

Cooperation in customs matters

1. The aim of cooperation shall be to ensure fair trade and compliance with trade rules. It shall focus on:

|

(a) |

simplifying customs checks and procedures; |

|

(b) |

the use of the Single Administrative Document and creating a link between the Community and Tunisian transit systems. |

2. Without prejudice to other forms of cooperation provided for in this Agreement, and particularly those provided for in Articles 61 and 62, the Contracting Parties' administrative authorities shall provide mutual assistance in accordance with the terms of Protocol No 5.

Article 60

Cooperation in statistics

The aim of cooperation shall be to bring the methods used by the Parties closer together and to put to use data on all areas covered by this Agreement for which statistics can be collected.

Article 61

Money laundering

1. The Parties agree on the need to work towards and cooperate on preventing the use of their financial systems to launder the proceeds of criminal activities in general and drug trafficking in particular.

2. Cooperation in this area shall include administrative and technical assistance with the purpose of establishing suitable standards against money laundering equivalent to those adopted by the Community and international fora in this field, including the Financial Action Task Force (FATF).

Article 62

Combating drug use and trafficking

1. The aim of cooperation shall be to:

|

(a) |

improve the effectiveness of policies and measures to prevent and combat the production and supply of and trafficking in narcotics and psychotropic substances; |

|

(b) |

eliminate illicit consumption of such products. |

2. The Parties shall together set out appropriate strategies and methods of cooperation, in accordance with their own legislation, to attain those objectives. For any action which is not conducted jointly, there shall be consultations and close coordination.

Such action may involve the appropriate public and private sector institutions and international organisations, in collaboration with the government of the Republic of Tunisia and the relevant authorities in the Community and the Member States.

3. Cooperation shall take the following forms in particular:

|

(a) |

the establishment or expansion of clinics/hostels and information centres for the treatment and rehabilitation of drug addicts; |

|

(b) |

the implementation of prevention, information, training and epidemiological research projects; |

|

(c) |

the establishment of standards for preventing diversion of precursors and other essential ingredients for the illicit manufacture of narcotics and psychotropic substances, which are equivalent to those adopted by the Community and the appropriate international authorities, particularly the Chemicals Action Task Force (CATF). |

Article 63

The two Parties shall together establish the procedures needed to achieve cooperation in the fields covered by this Title.

TITLE VI

COOPERATION IN SOCIAL AND CULTURAL MATTERS

CHAPTER I

WORKERS

Article 64

1. The treatment accorded by each Member State to workers of Tunisian nationality employed in its territory shall be free from any discrimination based on nationality, as regards working conditions, remuneration and dismissal, relative to its own nationals.

2. All Tunisian workers allowed to undertake paid employment in the territory of a Member State on a temporary basis shall be covered by the provisions of paragraph 1 with regard to working conditions and remuneration.

3. Tunisia shall accord the same treatment to workers who are nationals of a Member State and employed in its territory.

Article 65

1. Subject to the provisions of the following paragraphs, workers of Tunisian nationality and any members of their families living with them shall enjoy, in the field of social security, treatment free from any discrimination based on nationality relative to nationals of the Member States in which they are employed.

The concept of social security shall cover the branches of social security dealing with sickness and maternity benefits, invalidity, old-age and survivors' benefits, industrial accident and occupational disease benefits and death, unemployment and family benefits.

These provisions shall not, however, cause the other coordination rules provided for in Community legislation based on Article 51 of the EC Treaty to apply, except under the conditions set out in Article 67 of this Agreement.

2. All periods of insurance, employment or residence completed by such workers in the various Member States shall be added together for the purpose of pensions and annuities in respect of old age, invalidity and survivors' benefits and family, sickness and maternity benefits and also for that of medical care for the workers and for members of their families resident in the Community.

3. The workers in question shall receive family allowances for members of their families who are resident in the Community.

4. The workers in question shall be able to transfer freely to Tunisia, at the rates applied by virtue of the legislation of the debtor Member State or States, any pensions or annuities in respect of old age, survivor status, industrial accident or occupational disease, or of invalidity resulting from industrial accident or occupational disease, except in the case of special non-contributory benefits.

5. Tunisia shall accord to workers who are nationals of a Member State and employed in its territory, and to the members of their families, treatment similar to that specified in paragraphs 1, 3 and 4.

Article 66

The provisions of this Chapter shall not apply to nationals of the Parties residing or working illegally in the territory of their host countries.

Article 67

1. Before the end of the first year following the entry into force of this Agreement, the Association Council shall adopt provisions to implement the principles set out in Article 65.

2. The Association Council shall adopt detailed rules for administrative cooperation providing the necessary management and monitoring guarantees for the application of the provisions referred to in paragraph 1.

Article 68

The provisions adopted by the Association Council in accordance with Article 67 shall not affect any rights or obligations arising from bilateral agreements linking Tunisia and the Member States where those agreements provide for more favourable treatment of nationals of Tunisia or of the Member States.

CHAPTER II

DIALOGUE IN SOCIAL MATTERS

Article 69

1. The Parties shall conduct regular dialogue on any social matter which is of interest to them.

2. Such dialogue shall be used to find ways to achieve progress in the field of movement of workers and equal treatment and social integration for Tunisian and Community nationals residing legally in the territories of their host countries.

3. Dialogue shall cover in particular all issues connected with:

|

(a) |

the living and working conditions of the migrant communities; |

|

(b) |

migration; |

|

(c) |

illegal immigration and the conditions governing the return of individuals who are in breach of the legislation dealing with the right to stay and the right of establishment in their host countries; |

|

(d) |

schemes and programmes to encourage equal treatment between Tunisian and Community nationals, mutual knowledge of cultures and civilizations, the furthering of tolerance and the removal of discrimination. |

Article 70

Dialogue on social matters shall be conducted at the same levels and in accordance with the same procedures as provided for in Title I of this Agreement, which can itself provide a framework for that dialogue.

CHAPTER III

COOPERATION IN THE SOCIAL FIELD

Article 71

With a view to consolidating cooperation between the Parties in the social field, projects and programmes shall be carried out in any area of interest to them.

Priority will be afforded to:

|

(a) |

reducing migratory pressure, in particular by creating jobs and developing training in areas from which emigrants come; |

|

(b) |

resettling those repatriated because of their illegal status under the legislation of the state in question; |

|

(c) |

promoting the role of women in the economic and social development process through education and the media in step with Tunisian policy on the matter; |

|

(d) |

bolstering and developing Tunisia's family planning and mother and child protection programmes; |

|

(e) |

improving the social protection system; |

|

(f) |

enhancing the health cover system; |

|

(g) |

improving living conditions in poor, densely populated areas; |

|

(h) |

implementing and financing exchange and leisure programmes for mixed groups of Tunisian and European young people residing in the Member States, with a view to promoting mutual knowledge of their respective cultures and fostering tolerance. |

Article 72

Cooperation schemes may be carried out in coordination with Member States and relevant international organisations.

Article 73

A working party shall be set up by the Association Council by the end of the first year following the entry into force of this Agreement. It shall be responsible for the continuous and regular evaluation of the implementation of Chapters 1 to 3.

CHAPTER IV

COOPERATION ON CULTURAL MATTERS

Article 74

1. In order to boost mutual knowledge and understanding, taking account of activities already carried out, the Parties shall undertake — while respecting each other's culture — to provide a firmer footing for lasting cultural dialogue and to promote continuous cultural cooperation between them, without ruling out a priori any field of activity.

2. In putting together cooperation projects and programmes and carrying out joint activities, the Parties shall place special emphasis on young people, on written and audio-visual means of expression and communication, and on the protection of their heritage and the dissemination of culture.

3. The Parties agree that cultural cooperation programmes already under way in the Community or in one or more of its Member States may be extended to Tunisia.

TITLE VII

FINANCIAL COOPERATION

Article 75

With a view to full attainment of the Agreement's objectives, financial cooperation shall be implemented for Tunisia in line with the appropriate financial procedures and resources.

These procedures shall be adopted by mutual agreement between the Parties by means of the most suitable instruments once the Agreement enters into force.

In addition to the areas covered by the Titles V and VI of this Agreement, cooperation shall entail:

|

— |

facilitating reforms aimed at modernizing the economy, |

|

— |

updating economic infrastructure, |

|

— |

promoting private investment and job creation activities, |

|

— |

taking into account the effects on the Tunisian economy of the progressive introduction of a free trade area, in particular where the updating and restructuring of industry is concerned, |

|

— |

flanking measures for policies implemented in the social sectors. |

Article 76

Within the framework of Community instruments intended to buttress structural adjustment programmes in the Mediterranean countries — and in close coordination with the Tunisian authorities and other contributors, in particular the international financial institutions — the Community will examine suitable ways of supporting structural policies carried out by Tunisia to restore financial equilibrium in all its key aspects and create an economic environment conducive to boosting growth, while at the same time enhancing social welfare.

Article 77

In order to ensure a coordinated approach to dealing with exceptional macroeconomic and financial problems which could stem from the progressive implementation of the Agreement, the Parties shall closely monitor the development of trade and financial relations between the Community and Tunisia as part of the regular economic dialogue established under Title V.

TITLE VIII

INSTITUTIONAL, GENERAL AND FINAL PROVISIONS

Article 78

An Association Council is hereby established which shall meet at ministerial level once a year and when circumstances require, on the initiative of its Chairman and in accordance with the conditions laid down in its rules of procedure.

It shall examine any major issues arising within the framework of this Agreement and any other bilateral or international issues of mutual interest.

Article 79

1. The Association Council shall consist of the members of the Council of the European Union and members of the Commission of the European Communities, on the one hand, and of members of the Government of the Republic of Tunisia, on the other.

2. Members of the Association Council may arrange to be represented, in accordance with the provisions laid down in its rules of procedure.

3. The Association Council shall establish its rules of procedure.

4. The Association Council shall be chaired in turn by a member of the Council of the European Union and a member of the Government of the Republic of Tunisia in accordance with the provisions laid down in its rules of procedure.

Article 80

The Association Council shall, for the purpose of attaining the objectives of the Agreement, have the power to take decisions in the cases provided for therein.

The decisions taken shall be binding on the Parties, which shall take the measures necessary to implement the decisions taken. The Association Council may also make appropriate recommendations.

It shall draw up its decisions and recommendations by agreement between the Parties.

Article 81

1. Subject to the powers of the Council, an Association Committee is hereby established which shall be responsible for the implementation of the Agreement.

2. The Association Council may delegate to the Association Committee, in full or in part, any of its powers.

Article 82

1. The Association Committee, which shall meet at the level of officials, shall consist of representatives of members of the Council of the European Union and of members of the Commission of the European Communities, on the one hand, and of representatives of the Government of the Republic of Tunisia, on the other.

2. The Association Committee shall establish its rules of procedure.

3. The Association Committee shall be chaired in turn by a representative of the Presidency of the Council of the European Union and by a representative of the Government of the Republic of Tunisia.

The Association Committee shall normally meet alternately in the Community and in Tunisia.

Article 83

The Association Committee shall have the power to take decisions for the management of the Agreement as well as in those areas in which the Council has delegated its powers to it.

It shall draw up its decisions by agreement between the Parties. These decisions shall be binding on the Parties, which shall take the measures necessary to implement the decisions taken.

Article 84

The Association Council may decide to set up any working group or body necessary for the implementation of the Agreement.

Article 85

The Association Council shall take all appropriate measures to facilitate cooperation and contacts between the European Parliament and the Chamber of Deputies of the Republic of Tunisia, and between the Economic and Social Committee of the Community and the Economic and Social Council of the Republic of Tunisia.

Article 86

1. Either Party may refer to the Association Council any dispute relating to the application or interpretation of this Agreement.

2. The Association Council may settle the dispute by means of a decision.

3. Each Party shall be bound to take the measures involved in carrying out the decision referred to in paragraph 2.

4. In the event of it not being possible to settle the dispute in accordance with paragraph 2, either Party may notify the other of the appointment of an arbitrator; the other Party must then appoint a second arbitrator within two months. For the application of this procedure, the Community and the Member States shall be deemed to be one Party to the dispute.

The Association Council shall appoint a third arbitrator.

The arbitrators' decisions shall be taken by majority vote.

Each party to the dispute shall take the steps required to implement the decision of the arbitrators.

Article 87

Nothing in the Agreement shall prevent a Contracting Party from taking any measures:

|

(a) |

which it considers necessary to prevent the disclosure of information contrary to its essential security interests; |

|

(b) |

which relate to the production of, or trade in, arms, munitions or war materials or to research, development or production indispensable for defence purposes, provided that such measures do not impair the conditions of competition in respect of products not intended for specifically military purposes; |

|

(c) |

which it considers essential to its own security in the event of serious internal disturbances affecting the maintenance of law and order, in time of war or serious international tension constituting threat of war or in order to carry out obligations it has accepted for the purpose of maintaining peace and international security. |

Article 88

1. In the fields covered by this Agreement, and without prejudice to any special provisions contained therein:

|

— |

the arrangements applied by the Republic of Tunisia in respect of the Community shall not give rise to any discrimination between the Member States, their nationals, or their companies or firms, |

|

— |

the arrangements applied by the Community in respect of the Republic of Tunisia shall not give rise to any discrimination between Tunisian nationals or its companies or firms. |

Article 89

Nothing in the Agreement shall have the effect of:

|

— |

extending the fiscal advantages granted by either Party in any international agreement or arrangement by which it is bound, |

|

— |

preventing the adoption or application by either Party of any measure aimed at preventing fraud or the evasion of taxes, |

|

— |

opposing the right of either Party to apply the relevant provisions of its tax legislation to taxpayers who are not in an identical situation as regards their place of residence. |

Article 90

1. The Parties shall take any general or specific measures required to fulfil their obligations under the Agreement. They shall see to it that the objectives set out in the Agreement are attained.

2. If either Party considers that the other Party has failed to fulfil an obligation under the Agreement, it may take appropriate measures. Before so doing, except in cases of special urgency, it shall supply the Association Council with all the relevant information required for a thorough examination of the situation with a view to seeking a solution acceptable to the Parties.

In the selection of measures, priority must be given to those which least disturb the functioning of the Agreement. These measures shall be notified immediately to the Association Council and shall be the subject of consultations within the Association Council if the other Party so requests.

Article 91

Protocols Nos 1 to 5, Annexes 1 to 7 and the declarations shall form an integral part of the Agreement.

Article 92

For the purposes of this Agreement, ‘Parties’ shall mean, on the one hand, the Community or the Member States, or the Community and its Member States, in accordance with their respective powers, and, on the other hand, Tunisia.

Article 93

This Agreement shall be concluded for an unlimited period.

Either Party may denounce this Agreement by notifying the other Party. The Agreement shall cease to apply six months after the date of such notification.

Article 94

This Agreement shall apply, on the one hand, to the territories in which the Treaties establishing the European Community and the European Coal And Steel Community are applied and under the conditions laid down in those Treaties and, on the other hand to the territory of the Republic of Tunisia.

Article 95

This Agreement is drawn up in duplicate in the Danish, Dutch, English, Finnish, French, German, Greek, Italian, Portuguese, Spanish, Swedish and Arabic languages, each of these texts being equally authentic.

Article 96

1. The Agreement shall be approved by the Contracting Parties in accordance with their own procedures.

It shall enter into force on the first day of the second month following the date on which the Contracting Parties notify each other that the procedures referred to in the first paragraph have been completed.

2. Upon its entry into force, the Agreement shall replace the Cooperation Agreement between the European Community and the Republic of Tunisia and the Agreement between the Member States of the European Coal and Steel Community and the Republic of Tunisia, signed in Tunis on 25 April 1976.

Hecho en Bruselas, el diecisiete de julio de mil novecientos noventa y cinco.

Udfærdiget i Bruxelles den syttende juli nitten hundrede og fem og halvfems.

Geschehen zu Brüssel am siebzehnten Juli neunzehnhundertfünfundneunzig.

Έγινε στις Βρυξέλλες, στις δέκα εφτά Ιουλίου χίλια εννιακόσια ενενήντα πέντε.

Done at Brussels on the seventeenth day of July in the year one thousand nine hundred and ninety-five.

Fait à Bruxelles, le dix-sept juillet mil neuf cent quatre-vingt-quinze.

Fatto a Bruxelles, addì diciassette luglio millenovecentonovantacinque.

Gedaan te Brussel, de zeventiende juli negentienhonderd vijfennegentig.

Feito em Bruxelas, em dezassete de Julho de mil novecentos e noventa e cinco.

Tehty Brysselissä seitsemäntenätoista päivänä heinäkuuta vuonna tuhatyhdeksänsataayhdeksänkymmentäviisi.

Som skedde i Bryssel den sjuttonde juli nittonhundranittiofem.

Pour le Royaume de Belgique

Voor het Koninkrijk België

Für das Königreich Belgien

Cette signature engage également la Communauté française, la Communauté flamande, la Communauté germanophone, la Région wallonne, la Région flamande et la Région de Bruxelles-Capitale.

Deze handtekening verbindt eveneens de Vlaamse Gemeenschap, de Franse Gemeenschap, de Duitstalige Gemeenschap, het Vlaamse Gewest, het Waalse Gewest en het Brusselse Hoofdstedelijke Gewest.

Diese Unterschrift verbindet zugleich die Deutschsprachige Gemeinschaft, die Flämische Gemeinschaft, die Französische Gemeinschaft, die Wallonische Region, die Flämische Region und die Region Brüssel-Hauptstadt.

På Kongeriget Danmarks vegne

Für die Bundesrepublik Deutschland

Για την Ελληνική Δημοκρατία

Por el Reino de España

Pour la République française

Thar ceann na hÉireann

For Ireland

Per la Repubblica italiana

Pour le Grand-Duché de Luxembourg

Voor het Koninkrijk der Nederlanden

Für die Republik Österreich

Pela República Portuguesa

Suomen tasavallan puolesta

För Konungariket Sverige

For the United Kingdom of Great Britain and Northern Ireland

Por las Comunidades Europeas

For De Europæiske Fællesskaber

Für die Europäischen Gemeinschaften

Για τις Ευρωπαϊκές Κοινότητες

For the European Communities

Pour les Communautés européennes

Per le Comunità europee

Voor de Europese Gemeenschappen

Pelas Comunidades Europeias

Euroopan yhteisöjen puolesta

På Europeiska gemenskapernas vägnar

ANNEX 1

PRODUCTS REFERRED TO IN ARTICLE 10(1)

|

CN-Code |

Description |

|

0403 |

Buttermilk, curdled milk and cream, yogurt, kephir and other fermented or acidified milk and cream, whether or not concentrated or containing added sugar or other sweetening matter or flavoured or containing added fruit, nuts or cocoa: |

|

0403 10 51 |

— Yogurt, flavoured or containing added fruit, nuts or cocoa: |

|

— — — not exceeding 1,5 % |

|

|

0403 10 53 |

— — — exceeding 1,5 % but not exceeding 27 % |

|

0403 10 59 |

— — — exceeding 27 % |

|

— — — other, of a milk fat content by weight: |

|

|

0403 10 91 |

— — — not exceeding 3 % |

|

0403 10 93 |

— — — exceeding 3 % but not exceeding 6 % |

|

0403 10 99 |

— — — exceeding 6 % |

|

0403 90 71 |

— Other, flavoured or containing added fruit, nuts or cocoa: |

|

— — in powder, granules or other solid forms, of a milk fat content, by weight: |

|

|

— — — not exceeding 1,5 % |

|

|

0403 90 73 |

— — — exceeding 1,5 % but not exceeding 27 % |

|

0403 90 79 |

— — — exceeding 27 % |

|

— — other, of a milk fat content by weight: |

|

|

0403 90 91 |

— — — not exceeding 3 % |

|

0403 90 93 |

— — — exceeding 3 % but not exceeding 6 % |

|

0403 90 99 |

— — — exceeding 6 % |

|

0710 40 00 |

Sweet corn, uncooked or cooked by steaming or boiling in water, frozen: |

|

0711 90 30 |

Sweet corn, provisionally preserved (for example, by sulphur dioxide gas, in brine, in sulphur water or in other preservative solutions), but unsuitable in that state for immediate consumption |

|

1517 |

Margarine; edible mixtures or preparations of animal or vegetable fats or oils or of fractions of different fats or oils of this chapter, other than edible fats or oils or their fractions of heading No 1516: |

|

1517 10 10 |

— Margarine, excluding liquid margarine, containing more than 10 % but not more than 15% by weight of milk fats |

|

1517 90 10 |

— other, containing more than 10% but not more than 15 % by weight of milk fats |

|

1702 50 00 |

Chemically pure fructose |

|

1704 |

Sugar confectionery (including white chocolate), not containing cocoa, except liquorice extract containing more than 10% by weight of sucrose but not containing other added substances, of CN code 1704 90 10 |