EUROPEAN COMMISSION

EUROPEAN COMMISSION

Brussels, 19.12.2017

SWD(2017) 469 final

COMMISSION STAFF WORKING DOCUMENT

REFIT EVALUATION

Accompanying the document

Proposal for a Regulation of the European Parliament and of the Council

laying down rules and procedures for compliance with and enforcement of Union harmonisation laying down rules and procedures for compliance with and enforcement of Union harmonisation legislation on products and amending Regulations (EU) No 305/2011, (EU) No 528/2012, (EU) 2016/424, (EU) 2016/425, (EU) 2016/426 and (EU) 2017/1369 of the European Parliament and of the Council, and Directives 2004/42/EC, 2009/48/EC, 2010/35/EU, 2013/29/EU, 2013/53/EU, 2014/28/EU, 2014/29/EU, 2014/30/EU, 2014/31/EU, 2014/32/EU, 2014/33/EU, 2014/34/EU, 2014/35/EU, 2014/53/EU, 2014/68/EU and 2014/90/EU of the European Parliament and of the Council

{COM(2017) 795 final}

{SWD(2017) 466 final}

{SWD(2017) 467 final}

{SWD(2017) 468 final}

{SWD(2017) 470 final}

Annex 1: Procedural information

1.

Identification

·Lead DG: DG Internal Market, Industry, Entrepreneurship and SMEs (GROWTH)

·Agenda planning/Work programme references: 2017/GROW/007

2.

Organisation and timing

Work started in January 2016. An Inter-Service Steering Group (ISSG) chaired by DG Internal Market, Industry, Entrepreneurship and SMEs (GROWTH) was established to this purpose. Its members included representatives of:

·Secretariat-General

·DG Climate Action (CLIMA)

·DG Economic and Financial Affairs (ECFIN)

·DG Employment, Social Affairs and Inclusion (EMPL)

·DG Energy (ENER)

·DG Environment (ENV)

·DG Justice and Consumers (JUST)

·DG For Mobility and Transport (MOVE)

·DG Health and Food Safety (SANTE)

·DG Taxation and Customs Union (TAXUD)

·DG Trade (TRADE)

The ISSG met in total nine times (29/01/2016, 07/03/2016, 21/04/2016, 29/09/2016, 28/11/2016, 27/01/2017, 10/02/2017, 27/02/2017 and 06/03/2017).

3.

Consultation of the Regulatory Scrutiny Board

The Regulatory Scrutiny Board (RSB) of the European Commission assessed a draft version of the present evaluation and issued its opinion on 07/04/2017. The Board made several recommendations. Those were addressed in the revised report as follows:

|

RSB recommendations

|

Modification of the report

|

|

(B) Main considerations

The Board acknowledges a significant effort to collect evidence on non-compliant products as part of the evaluation work.

However, the Board considers that the report contains important shortcomings that need to be addressed, particularly with respect to the following issues:

(1) The evaluation report is not a self-standing document.

(2) The evaluation fails to deliver evidence-based findings and conclusions.

Against this background, the Board gives a negative opinion and considers that in its present form this report does not provide sufficient input for the associated Impact Assessment.

|

See below

|

|

(C) Further considerations and adjustment requirements

(1) Self-standing evaluation report

|

|

|

The evaluation report should be a self-standing document.

|

The SWD and the annexes were fundamentally redrafted so that the evaluation became a self-standing document.

|

|

It should include the main findings of the underlying external evaluation study and other available evidence, which are now in the annexes.

|

Done in section 4, 5.1, 6 and 7 of the SWD.

|

|

The report should present evidence in a structured way, following a clear intervention logic and addressing all the evaluation criteria.

|

New intervention logic in section 2.1.1. All evaluation criteria are examined separately in section 6 of the SWD (except EQ2/EQ3 and EQ8/EQ9 which are examined jointly for the sake of clarity)

|

|

The report should be clear about limitations of what the available evidence can reasonably demonstrate.

|

Done in section 4 of the SWD as a summary of the limitations set out in Annex 4.

|

|

As a REFIT exercise, the evaluation should also assess the scope for simplification and reduction of regulatory burden.

|

Done in section 7.6 of the SWD.

|

|

(2) Scope

|

|

|

The report should more clearly present the scope and limitations of the evaluation.

|

Scope and limitations explained in section 2.1.2 of the SWD

|

|

It should provide an explanation of the existing legislative framework and how the provisions are implemented in Member States.

|

Explained in 2.1.2, 2.1.3 and 2.3.1, and in detail in Annex 5.

|

|

The report should draw conclusions from the diversity of national practices.

|

Done mainly in section 6.1 but it is a recurrent feature throughout the text.

|

|

It should substantiate the fact that penalties are not high enough. It should explain the links with sectoral legislation and how mutual recognition and customs policy work together.

|

The penalties are examined in sections 6.1.2.2, 6.1.2.1, 6.1.3 and under EQ3, and in several other places of the text, and in greater detail on pp. 105-108 of Annex 4. Links with sector legislation explained in section 2.1.3 and table 1 of the SWD, and in Annex 5. Border controls explained in more detail essentially in section 6.1.3 of the SWD, under EQ3, and section 2 of Annex 8.

|

|

Against this background, it should clarify the scope and benchmarks used for the evaluation.

|

Done in section 2.1 of the SWD

|

|

It should add relevant information from previous impact assessments and evaluations

|

Full list in section 8.14 of Annex 4.

|

|

(3) Conclusion

|

|

|

The report should align its conclusions with the revisions required for the other sections. They should clearly set out main lessons learned and how far evidence supports them. As such, the conclusions should provide a solid basis for the scope and problem definition of the parallel impact assessment for future policy developments in the area.

|

Done in section 7 of the SWD.

|

The Regulatory Scrutiny Board (RSB) of the European Commission assessed the revised version of the present evaluation and issued a positive opinion on 31/05/2017. The Board made few final recommendations that were addressed in the revised evaluation as follows:

|

RSB recommendations

|

Modification of the report

|

|

(B) Main considerations / (C) Further considerations

|

|

|

(1) Further elaboration if the REFIT dimension throughout the evaluation.

|

The relevant aspects were consistently referred to in the sections on effectiveness and efficiency. The reasons why regulatory burden reduction concerns mainly authorities are explained.

|

|

(2) Additional explanations on how market surveillance works in practice in a Member States.

|

A detailed overview on the organisation of market surveillance in two Member States was added.

|

|

(3) Reader friendliness.

|

The introduction in particular is now a bit less technical and includes a summary of main findings.

|

Annex 2: Stakeholder consultation

1.

Objectives Of The Consultation

The Commission wanted to make an evidence-based assessment of the extent to which the provisions on market surveillance of Regulation (EC) No 765/2008 have been effective, efficient, relevant, coherent and achieved EU added-value. The results of the evaluation will support taking actions to enhance efforts to fight non-compliant products made available in the Single Market.

1.1

Consultation methods and tools

The market surveillance authorities have been consulted during the meetings of the Expert Group on the Internal Market for Products in 2016 .

A stakeholder conference - open to all interested participants - was organised by the Commission on 17 June 2016.

A public consultation in all EU official languages, published on a website hosted on Europa, run from 1 July to 31 October 2016. Participation of SMEs in the consultation was promoted and supported through the European Enterprise Network.

2.

Results Of The Consultation Activities

2.1

Meetings of the Expert Group on the Internal Market for Products – Market Surveillance Group

The Expert Group on the Internal Market for Products – Market Surveillance Group held its last meetings on 1st February 2016, 21st October 2016 and 31st March 2017.

During the first meeting, the Commission recalled the challenges reported by market surveillance authorities in the national reviews and assessment of activities carried out between 2010 and 2013. The detailed IMP document is annexed to the Impact Assessment (Annex 2).

During the meeting held on 21 October 2016, the Commission informed the participants of the state of play of the enforcement and compliance initiative and explained that the purpose was to receive feedback on the suitability of the ideas under examination. The detailed minutes can be found at:

http://ec.europa.eu/transparency/regexpert/index.cfm?do= groupDetail.groupDetailDoc&id=28611

.

The meeting held on 31 March 2017 focused on the legislative proposal and especially on how to enhance cooperation between the member states, create a uniform and sufficient level of market surveillance and have stronger border controls of imported products to the European market.

2.2

Meetings of the Customs Expert Group

The Customs Expert Group that met on 22 April was informed about the launch of the Enforcement and Compliance initiative. Customs authorities were invited to participate in the consultations and provide their views on possible challenges and actions needed.

The Expert Group PARCS met to discuss product safety and compliance controls on 1 December 2016. At the meeting the Commission presented the state of play on the revision of Regulation (EC) No 765/2008.

2.3

Stakeholder conference of 17 June 2016

A stakeholders' event was organised on 17 June 2016, to identify the main issues related to the compliance and better enforcement in the Single Market and to identify possible ways forward. 144 participants attended the event, representing businesses (62), national authorities (60) and others (22). The detailed minutes of this conference can be found at:

http://ec.europa.eu/DocsRoom/documents/17963

.

2.4

Public Consultation

239 replies were received via the online form foreseen during the public consultation. The numbers and percentages used to describe the distribution of the responses to the public consultation derive from the answers under the EU-Survey tool. Other submissions of stakeholders to the public consultation have been taken into account, but without being considered for the statistical representation.

The consultation was divided into five parts. Since only part B1 was obligatory, the other sections were partly answered. Therefore, the average ratio of replies was 80% for section B2, 66% for section B3, 80% for section B4 and 84% for section B5.

All statistics included in this summary are based on the data gathered from the replies for each section. Detailed statistics for each category can be found in Annex 2 of the Impact Assessment.

Businesses were strongly represented (127), followed by public authorities (80), and citizens (32). More specifically for businesses, 49% of them represent product manufacturers, 21% product importer / distributors, 8% product users, 5% conformity assessment bodies, 1% online intermediaries and 16% other.

Concerning the geographical distribution of responses, all countries were represented except for Latvia, Luxembourg, Malta, and Liechtenstein. The majority of respondents (116) exert their activities only in their country of establishment.

2.4.1

Product compliance in the Single Market and deterrence of existing enforcement mechanisms

The majority of respondents (89%) consider that their products are affected by non-compliance with product requirements laid down in EU harmonisation legislation.

However, 45% of the respondents are unable to estimate the approximate proportion of non-compliant products for their sector. This percentage is approximately equal for all type of respondents.

80% of businesses participating in the consultation confirm non-compliance has a negative effect on sales and/or market shares of businesses complying with legal obligations. Many businesses (42%), however, are unable to estimate their approximate loss in sales due to non-compliance.

As to the most important reason for product compliance in the Single Market, 33.47% of the respondents consider that it is about a deliberate choice to exploit market opportunities at the lowest cost, followed by a lack of knowledge (26.78%), a technical or other type of inability to comply with the rules (10.88%), ambiguity in the rules (10.46%) and carelessness (9.62%).

All types of respondents have experience / knowledge of instances where market surveillance authorities lacked sufficient financial and human resources as well as the technical means to carry out specific tasks. Nevertheless, 67.36% of the respondents could not estimate the approximate financial resource gap of the national authority.

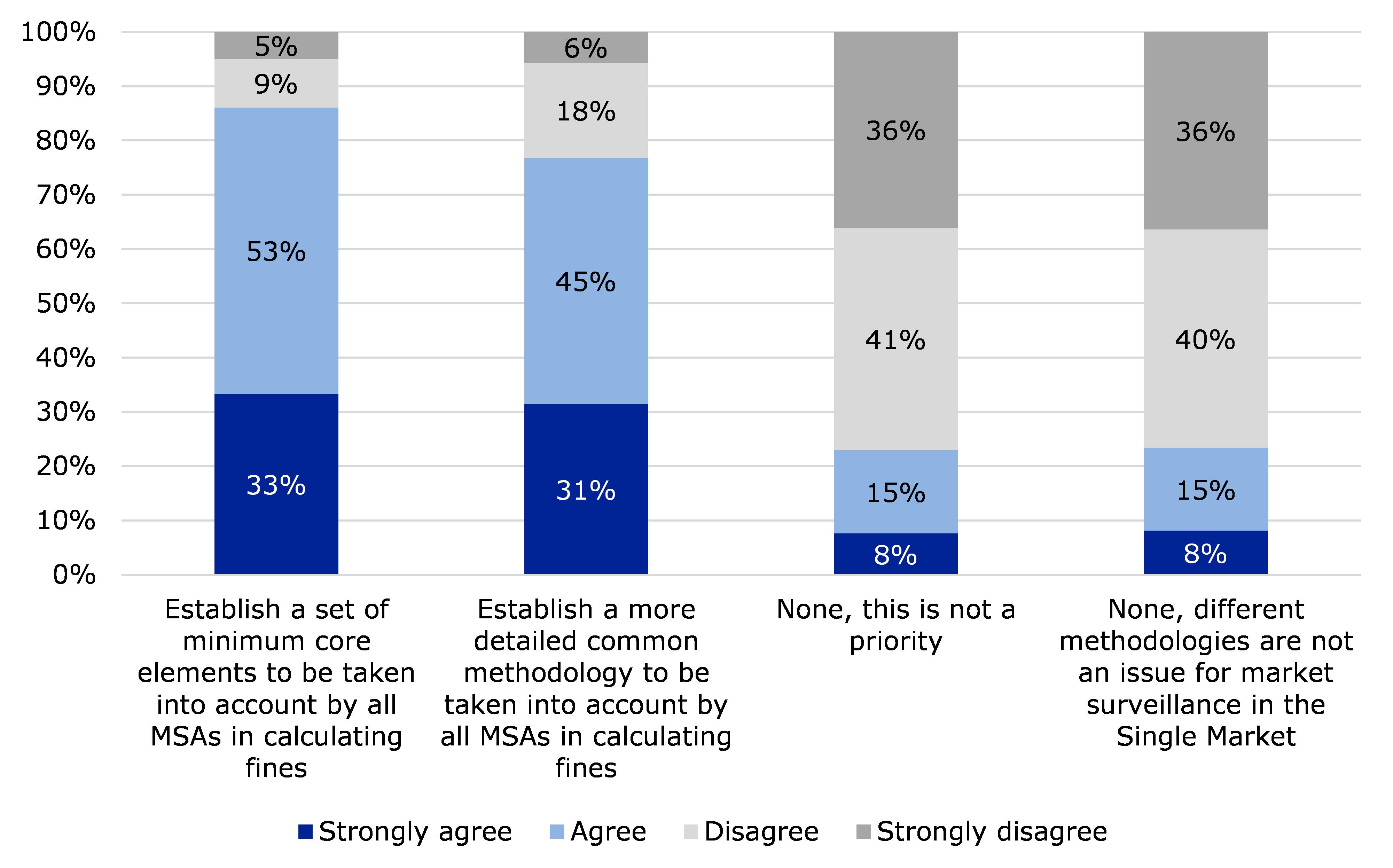

Regarding the increase of resources for market surveillance activities, although two of the three solutions receive a unanimous acceptance by the respondents, for the third one, namely that market surveillance authorities should levy administrative fees on operators in their sector to finance controls, the results are contradictory. 55.91% of the businesses and 40.63% of the consumers and others strongly disagree with this option, while 50.00% of the public authorities agree with it (15% strongly agree and 35% agree).

Stakeholders have similar views as regards the effective use of resources for market surveillance activities.

Many respondents (46%) agree that market surveillance does not provide sufficient deterrence in their sector or that it provides deterrence to a moderate extent (34%) and that the options proposed by the Commission would improve the deterrence of market surveillance action.

2.4.2

Compliance assistance in Member States and at EU level

This section of the questionnaire was optional, so the average ratio of replies came up to 80% (approximately 190 replies per question).

There is a consensus on the fact that sometimes it is difficult to find but also understand the correct information on the technical rules that products need to meet before they can be placed on the domestic and on other EU markets.

The approach taken by respondents to look for support and information on technical rules that products need to meet slightly differs according to the type of respondent. The majority of respondents prefer to refer to the information available on Commission websites. Regarding the approaches that should be followed by national authorities to reduce the level of non-compliant products on the market, the respondents consider that the best approach is the combination of information, support and enforcement by the public authorities.

2.4.3

Business' demonstration of product compliance

This section of the questionnaire was optional, so the average ratio of replies came up to 66% (approximately 158 replies per question).

Businesses were asked to provide answers on how they supply information about product compliance. Approximately 30% of the respondents consider that the proposed options are not applicable to them.

A large majority of respondents strongly agrees or agrees that a broader use of electronic means to demonstrate compliance would help to reduce the administrative burden for businesses (70.62%), reduce administrative costs of enforcement for authorities (65.14%), provide/allow information to be obtained faster (82.29%), and provide more and up-to-date information to consumers/end users (68.00%).

2.4.4

Cross-border market surveillance within the EU

This section of the questionnaire was optional, so the average ratio of replies came up to 80% (approximately 190 replies per question).

Most of the respondents (91) were unable to estimate the approximate proportion of products placed on the market by manufacturers or EU importers located in another EU Member State.

Public authorities believe that businesses contacted do not reply to requests for information/documentation or for corrective actions, while for businesses the main difficulty is that authorities find it more costly to contact businesses located in another EU Member State.

Concerning, the exchange of communication between national authorities in the EU Member States, the majority of respondents stated lack of opinion / experience (33%) while 25% of the respondents consider that national authorities rarely restrict the marketing of a product following exchange of information about measures adopted by another authority in the EU against the same product.

Additionally, as to the adequate mechanisms to increase the effectiveness of the market surveillance in the Single Market, the results showed an extremely large support for more exchange of information and discussion among authorities, but also for close coordination between Member States and simultaneous applicability of decisions against non-compliant products.

2.4.5

Market surveillance of products imported from non-EU countries

This section of the questionnaire was optional, so the average ratio of replies came up to 84% (approximately 201 replies per question).

Many respondents (39%) were unable to estimate the approximate proportion of products imported from non-EU countries in their sector. However, 21% of them indicated that the proportion of products imported from non-EU countries is more than 50%. At the same time, 88% of the respondents believe that the products in their sector imported from non-EU countries are affected by non-compliance.

As to the country of origin of often non-compliant imported products, China lead with 137 replies, followed by India (30), Turkey and United States (18) and Hong Kong (17). Finally, the most preferred options in taking actions against non-compliant products traded by businesses located in a non-EU country were the need for more coordination of controls of products entering the EU between customs and market surveillance authorities (88.27%).

2.5

Targeted Consultation conducted by the Contractor

In general, all stakeholders consulted through the targeted surveys and interviews uniformly recognise the effectiveness of the Regulation needs to be improved.

Around half respondents declare that the dimension of product non-compliance has not changed after the entry into force of the Regulation. While this is true for public authorities, respondents from the private sector perceive that product non-compliance has increased. Most economic operators, industry associations and civil society representatives state to experience discrepancies across Member States in terms of market surveillance. Such discrepancies have more negative impacts in terms of hindering the free circulation of goods, influencing market behaviour, reducing the safety of products and raising costs for public authorities and economic operators to comply with the Regulation. Among all respondents, only customs have a positive opinion on the adequacy of current border controls. In general, industry representatives want to be more involved in market surveillance activities. According to respondents, the efficiency of the Regulation could be improved by solving the existing discrepancies in its implementation.

The majority of respondents confirm the Regulation’s relevance, this being confirmed by all economic operators and a large part of customs and coordinating authorities. However, the Regulation’s relevance can be challenged by its low capacity to address emerging issues. All stakeholders agree that the Regulation is not able to tackle issues deriving from online sales. No stakeholder category reported major issues in term of coherence of the Regulation, both within its provisions and with other legislations relevant for market surveillance.

All stakeholders recognise the EU added value of the Regulation, which enhanced the free movement of goods and legislative transparency. The harmonisation of rules and cooperation between Member States are also reported as benefits by all. Different categories also argued that the Regulation can establish a level playing field across businesses in the EU.

2.6

Informal consultation of SMEs at the Small Business Act follow-up meeting with stakeholders in December 2016

The Commission presented the reflections on the possible options to address the problem of non-compliance and asked for feedback. Businesses representatives confirmed that SMEs are also hit by non-compliance like bigger companies.

3.

FEEDBACK TO STAKEHOLDERS

The consultation processes provided a wide range of views regarding the functioning of market surveillance in terms of what has worked well and what has not worked so well, seen through the eyes of these stakeholders. The meetings with the stakeholders provided an early opportunity to promote the engagement of the national authorities, thus enhancing the chances of a good response rate.

The general objective of this initiative is to reduce the number of non-compliant products in the Single Market by improving at the same time incentives to comply and effectiveness of market surveillance..

The considered options covered in order of increasing ambition and EU coordination and action: (1) Baseline, (2) Improvement of existing tools and cooperation mechanisms; (3) in addition increased deterrence effect to enforcement tools and stepped up EU coordination and (4) further added-on centralised EU level enforcement in certain cases.

The preferred option (3) includes:

•the extension of Product Contact Points advice role to businesses and ad-hoc public-private partnerships;

•digital systems through which manufacturers or importers would make compliance information available to both consumers and market surveillance authorities and common European portal for voluntary measures;

•regime of publicity for decisions to restrict the marketing of products, fine-tuning authorities powers notably in relation to on-line sales imports from third countries, recovery of costs of controls for products found to be non-compliant;

•stricter obligations for mutual assistance and legal presumption that products found to be noncompliant in Member State A are also non-compliant in Member State B;

•Member States' enforcement strategies setting out national control activities and capacity building needs and an EU Product Compliance Network providing an administrative support structure to peer review Member States' performance coordinate and help implementing joint enforcement activities of Member States.

The measures underlying the preferred option were rated highly favourable across the different categories of respondents in the public consultation. Stakeholders concur on the need for much stronger coordination, more resources and efficient use of resources for market surveillance and more effective tools to improve the enforcement framework for controls within the Single Market and on imports into the EU. A more pro-active approach to prevent non-compliance by providing information and assistance to economic operators is also supported by stakeholders. On a more detailed level some variations occur between the views of authorities and businesses on the most appropriate form of the digital compliance system or the specific powers and sanctions; these concerns have been integrated in the assessment.

More information on the different options, on those retained and on the views of the stakeholders can be found in Sections 6 and 7 of the Impact Assessment.

4.

Feedback From the Expert Group on the Internal Market for Products – Market Surveillance and Conformity Assessment Policy (IMP-MSG)

4.1

Difficulties and challenges for market surveillance for non-food products in the Single Market

4.1.1

Contributions sent to the Commission in accordance with Article 18(6) of Regulation (EC) No 765/2008

Article 18(6) of Regulation (EC) No 765/2008 requires Member States to periodically review and assess the functioning of their market surveillance activities. Such reviews are to be carried out at least every four years and the results are to be communicated to the other Member States and the Commission and made available to the public.

Many of the national reports reviewing market surveillance activities carried out between 2010 and 2013 comment on major difficulties identified. Common challenges mentioned appear to be the following:

1.Lack of sufficient resources for market surveillance.

2.Current control procedures are not suitable for handling products sold online. Moreover, for effective market surveillance of products sold on the internet and that are offered from outside the EU, collaboration with customs authorities is of crucial importance.

3.There is a need to reinforce customs controls. Furthermore, to make it harder for non-European manufacturers, whose non-compliant products have been rejected by a customs authority, to switch to other customs clearance locations, improved cooperation between the customs authorities of the EU Member States also seems necessary. For some Member States there exists a mismatch between the customs product classification and the nomenclature used by market surveillance authorities, which hamper cooperation in some areas (e.g. electrical low voltage equipment, personal protective equipment, pressure equipment, equipment for use in potentially explosive atmospheres, lifts and machinery).

4.There is insufficient cross-border cooperation in some sectors (i.e. equipment for use in potentially explosive atmospheres, pyrotechnic articles, civil explosives and gas appliances), which is difficult to tackle when relevant economic operators are located abroad. Complications due to the lack of ADCOs for marine equipment and motor vehicles are also mentioned.

5.There is a lack of traceability of information especially when products are imported into the EU by intermediaries located in other Member States

6.There is the difficulty of dealing with products from third countries sold via informal channels (marketplaces), and the ineffectiveness of market surveillance techniques in this case.

7.Penalties laid down in national law might not be a sufficient deterrent, in particular in the case of larger companies trying to market non-compliant products;

8.The non-existence of test laboratories makes conformity assessment difficult and costly.

9.There is a lack of knowledge amongst economic operators about applicable product rules. In some sectors formal requirements such as technical documentation and CE marking are disregarded by businesses, possibly due to lack of knowledge or misunderstanding of those requirements.

10.There is a lack of cooperation by certain economic operators and some abuses by businesses of the legal principles concerning the notification of restrictive measures contained in Article 21 (1) and (2) of Regulation (EC) 765/2008.

11.There is the need to reduce the administrative burden for market surveillance authorities (i.e. simplify current safeguard clause procedures for serious risk products by using the Rapex system). Furthermore, there is a demand for a single integrated system since reporting in different information exchange systems is deemed cumbersome and not always suitable.

4.1.2

Future new actions to improve market surveillance – initial suggestions by Member States

At the latest joint IMP-MSG and CSN meeting on 30 January 2015 the Commission asked Member States representatives to come up with informal suggestions about possible future new actions to improve market surveillance. A Member State suggested that a possible way to increase the availability of resources for market surveillance would be to ensure EU-wide agreements (financed by EU funds), with laboratories having recognised competence in a given domain to which national authorities could send on a pro-rata basis products to be tested.

The question about possible new actions to improve market surveillance was also asked at the last meeting of ADCO Chairs that took place on 12 March 2015. Some of the suggested new actions informally proposed during that meeting were the following:

1.Workshops with other ADCO Groups

2.Cooperation between inspectors checking products during use and market surveillance

3.Cooperation with producer countries, especially China

4.Supervision of notified bodies and collaboration with market surveillance authorities

5.More documents to be shared through CIRCA BC

6.Joint actions between directives

7.Feedback on safeguard notifications from the Commission

8.Shorter dates between publication of legislation and guidance

9.Exchange between inspectors across Member States

10.Easier contacts with economic operators abroad

11.Team building, networking, exchange of experience

12.More information on what is happening in other fields

13.Review of notified bodies' certificates

14.Exchange of ADCO members

15.Convergence of ICSMS and RAPEX platforms

16.E-commerce: administrative requirements for information to be displayed on websites, legal powers for authorities to carry out test purchases, campaign aimed at consumers

17.More responsibilities for importers

18.More resources

19.Applicability across the EU of sale bans issued by national authorities.

4.2

Questions to the Members of the IMP-MSG Group and overview of replies

On 2 December the members of the IMP-MSG group were invited to provide input on the following questions:

(1)Do you share the analysis of the problem of non-compliant products in the internal market made by the Commission in the Single Market Strategy? Is there any other relevant problem to take into account?

(2)What action do you consider necessary to tackle those problems?

(3)What action is necessary to address the difficulties faced by national authorities that have emerged in the context of the national reviews according to Article 18(6) of Regulation (EC) 765/2008?

(4)What should be the main priorities when it comes to improving market surveillance and to generally reducing non-compliance in the internal market?

Thirteen Member States provided answers to the above questions.

As to question (1) most of these Member States share the analysis carried by the Commission. The following additional qualifications are noted:

A Member State also stresses the problems of (i) several pieces of legislation applicable to the same product which makes it more complex and difficult for both economic operators and authorities to maintain the overall picture, (ii) uneven quality and quantity of market surveillance activities in different Member States, which could be addressed by establishing common standards, (iii) limited availability of resources.

Another one notes that the problem of non-compliance is to be addressed to ensure a level playing field among economic operators, although accidents due to non-compliance are limited in number overall.

Furthermore, there is no solid proof that the number of non-compliant products is increasing, as statistics on market surveillance differ from statistics on non-compliance that could result from market research.

Similarly, two other Member States note that since market surveillance inspectors focus on areas where non-compliance is expected to be high, results of inspections are not representative of the level of non-compliance in general. Denmark stresses that it is not possible to measure the percentage of non-compliant products in the market.

Some questions exclusive focus on the non-compliance of products stating that market surveillance should also play a role to ensure that legitimate products do not face unfair barriers to trade.

Finally, another Member State would have appreciated a deeper analysis of if, when and in what ways the impact of varying degrees of market surveillance (or the lack of it) harm consumers, compliant competitors, and Member States as a whole (loss of manufacturing, reduced competitiveness, etc.). Such an analysis could indeed give valuable input regarding when and where a lack of enforcement has the least impact on the different interests that a product rule is designed to protect, which in turn could be used in subsequent Refit procedures with a view to reducing the administrative burden.

The suggestions made by the Member States who responded to questions (2) to (4) have been grouped as far as possible by topics as follows:

4.2.1

Information to economic operators

The lack of knowledge of product rules on the part of economic operators is one of the main problems that should be addressed.

Informing the national economic operators – who are sometimes not aware of their responsibilities - about specific legislation and their obligations, is a main priority.

Economic operators probably disregard the rules mainly because of a lack of knowledge, or because they lack the resources to follow up the complicated rules on their own (SMEs).

There is a need to intensify efforts to provide early information to economic operators, especially small and medium-sized enterprises, on existing and future product legal requirements but also to raise awareness amongst economic operators via better channels of communication.

It is also suggested developing rules and best practices concerning products to be disseminated via internet and improving information on European regulations on the websites of the Commission to make it more educational and useful for economic operators (input by product type, not directive).

If the problem which has been identified is referring to economic operators “in general” the solution has to be Commission-led. This might be done, for example, by revisiting the guidance and how it is made available to them, making changes where appropriate. However, if this refers to specific economic operators the approach also has to be specific, and it is more likely to fall to individual Market Surveillance Authorities and Member States to determine the action which should be taken.

In addition, the Commission does not have sufficient manpower to handle a 'first port of call' to address businesses' questions on all areas of product legislation, which would require a huge amount of work. An eLearning system is proposed for raising awareness and educating economic operators through graphic interfaces, and access to applicable standards and conformity assessment procedures, and a "10-20 questions card" for importers to ask when they buy goods overseas.

4.2.2

Simplification of product legislation; alignment between legal requirements and verification procedures by MSAs

Legislation should set out economic operators' obligations more clearly and it should be possible to make a clear distinction between basic non-compliance and more serious safety issues. Legislation needs to be simplified and updated.

As regards future legislation, there is a suggestion reflecting on how to include the necessary new rules in existing legal acts rather than developing new (unknown) specifications but also to better take into account the concerns of market surveillance authorities during the legislative process: the feasibility of checking specific requirements and the foreseeable costs of those requirements should be assessed in the development stages of legislation.

The weakness of verification procedures in some sectoral legislation is also pointed out. Even when a Member State performs verification tests, the results of these tests may turn out to be inconclusive, because of the unreliability of the results when the tests are replicated, and/or because of ambiguities in dealing with those results. A comprehensive “fitness check” on verification procedures based on established best practice would be useful. For example: a wet-grip-in-tyre labelling regulation where the test method seems to be unsuitable to providing sufficient accuracy (actually the 2sigma-interval of reproducibility uncertainty covers 3 grading classes). Technical requirements for verification of big products at the manufacturers site, for instance by means of witness-testing during factory acceptance tests, should also be definitively introduced.

4.2.3

Coordination of market surveillance at EU level

The need for closer cooperation and exchange of information is generally acknowledged. Specific proposals are made with respect to the use of current tools or to the need for additional forms of cooperation.

4.2.3.1

ICSMS and RAPEX

The importance of the development of the ICSMS and RAPEX systems for communication between all authorities involved in market surveillance (market surveillance authorities of all Member States, COM and, where appropriate, customs authorities) is stressed. ICSMS should be used consistently by Member States in all areas of legislation while interfaces with national systems should be provided. The creation of single system for exchange of information has also been requested but also the idea of fusion between ICSMS and RAPEX platforms to avoid the double encoding of data; however, this should take into account the fact that the RAPEX system has been used for a long time by all stakeholders.

The focus of the Commission’s wording on the Single Market Strategy is on working better together, with better sharing of information. In this regard Member States could make better and more consistent use of ICSMS; they recognise that this is a medium- to long-term issue, and one which might require funding/support from the Commission in order to make it work – in particular for those Member States who do not use the system.

There is a need for closer cooperation between surveillance authorities in Member States and between surveillance and custom authorities, and between surveillance authorities and notified bodies, and suggests it would be good to have a stronger convergence between the the ICSMS and RAPEX platforms.

4.2.3.2

ADCOS and IMP-MSG groups

The role of ADCOs should be revisited and clarified (many discuss policy issues rather than focussing on issues related to technical cooperation, for example), and absences from meetings/participation should be marked. The Commission desk officers for the relevant directives should also take a stronger role in encouraging attendance/participation. Furthermore, the European Market Surveillance Forum, which was proposed in the “Regulation on Market Surveillance”, would be a positive way of addressing this issue.

Member States welcome the proposal mentioned in section 3.2 above relating to workshops with other ADCOs. Similarly, a Member State suggests a better use of ADCOs to improve coordination, exploit synergies and avoid duplication. Furthermore, it suggests that the IMP-group should develop a shared understanding of the horizontal rules and promote more interaction between the market surveillance authorities of the Member States in the different fields of law by means of visits, joint actions, etc.

There is also a proposal devoting an extra IMP-MSG meeting to the exchange of best practice. ADCOs should contribute to the meeting by reporting on experience accumulated during their earlier joint action projects.

4.2.3.3

Cross-border cooperation

The need for consistent implementation of the guidelines on cross-border–cooperation is stressed, complemented if necessary by the set-up of additional legal arrangements. Furthermore, under the safeguard clause procedure all European market surveillance authorities must take, where necessary, measures to enforce requirements under European law. Furthermore, a Member State suggests that where a public authority prohibits the making available on the national market, this should automatically apply in all MS, with the ECJ possibly acting as appeal. Member States should reflect on the possibility of specialising in specific fields. In order to achieve an effective market surveillance system, the adaptation of national legislation to the EU legislation will be necessary in a number of areas (cross-border cooperation, mutual recognition of activities of the market surveillance authorities of other Member States - for example, recognition of test reports, etc.). The organisation of market surveillance at national level should be reconsidered in order to reduce the fragmentation of responsibilities.

There is also a need for guidance on cross-border cooperation to improve and optimize the results of authorities’ actions. To achieve better results in trans-border cooperation between the Member States, in cases of non–compliant products a contact points list for each product group should be prepared which could provide fast and easily accessible communication.

A mandatory harmonized procedure for MSA cooperation will facilitate cases of cross-border cooperation and will further harmonize existing market surveillance approaches. The administrative burden for MSAs of this procedure should nevertheless be as minimal as possible.

Prior to setting additional requirements for mutual change of information, the Commission should ensure that all Member States actively use the present procedures and notes that for example EMC and LVD notifications are made by only a few States.

It would be useful for Member States to receive more feedback on safeguard notifications. In general, more cooperation and exchange of information is needed at EU and national level.

'Language borders' are considered as the main obstacle to day-to-day cooperation among authorities.

4.2.4

Harmonisation of market surveillance practice across Member States

There is a suggestion developing common European standards on the quality and quantity of their market surveillance activities.

The development and publication of guidelines and best practices on market surveillance in general is welcomed as a means to achieve the consolidation of the procedures of the EU market surveillance authorities in many problematic areas.

Publication of guidance documents would considerably help the harmonization of market surveillance in Europe as they would help inspectors and economic operators to interpret and correctly apply the directives and regulations. Shorter dates for the publication of guidance documents are required.

In addition, it is proposed to encourage via EU funding the participation of more Member States in common projects in which different products can be tested in order to achieve more representative results, and the dissemination of all information, analysis, results and decisions taken for this specific product group after a project is completed.

According to feedback from domestic surveillance authorities having taken part in international cooperation projects, they have provided a good overview of the practices of other countries and have contributed to carrying out uniform surveillance in different Member States.

The problem of limited human resources and training opportunities has been pointed out and a suggestion was made to promote the exchange of inspectors across Member States and closer cooperation among surveillance authorities to improve knowledge and exchange experiences.

Training programmes and exchange of experience between Member States' inspectors are also proposed.

The exchange of experience and best practices between inspectors across the Members States is very important to improve the harmonization of market surveillance in Europe. Regular exchanges of officials could be a solution.

Similarly, exchange of inspectors, teambuilding and networking are endorsed by other Member States.

Moreover, the Product Safety & Market Surveillance Package has to be finalized, since it will enable better coherence of the rules regulating consumer products and will improve coordination of the way authorities check products and enforce product safety rules across the European Union.

The current delay with revision of the Market Surveillance Regulation is considered to be problematical, and stresses the importance of a horizontal legislative framework on market surveillance.

The Commission should provide more information on what instruments are available to the authorities and how they are used in practice (frequency, criteria for deciding what tools to use in different cases), so that the barriers for putting non-compliant products on the market might be the same for all Member States.

4.2.5

Better control of products imported from third countries

There is a need to strengthen border controls, where the goods are centralised before being dispatched throughout the EU. This could be achieved either by reinforcing the role of customs or by ensuring detailed cooperation with market surveillance authorities.

More effective cooperation between market surveillance and customs authorities should also be achieved via a clearer definition/better alignment of the tasks performed by the customs authorities in order to ensure compliance with the European product rules. The need for improved communication between the customs and market surveillance authorities is also stressed.

Controls would improve if there was better communication between authorities. This might potentially be done through an electronic forum which authorities could use to discuss and agree issues which arise on products, and better guidance on the application of the directives concerned and the procedures which need to be followed.

Both the importance of cooperation between customs and market surveillance authorities and the importance of cooperation among customs on market surveillance matters are mentioned.

Customs should be enabled to request manufacturer and type designation as part of the customs declaration. Furthermore, combined nomenclature (CN) codes must be amended to be also useful for market surveillance purposes.

There is a need to improve border control of non–compliant products and to ensure regular exchange of information on results of controls and lists of products not released for free circulation.

Another problem is that, while many products come from outside the EU, authorities can do little against those manufacturers. Products are often placed on the EU market through “once only importers” that disappear after one or two years, so even there we can do little. Strong measures against these products are needed to target the non EU economic operator. For example, a strong message could be sent when all products need to be recalled if there is no technical file present.

A Member State supports the strengthening of responsibilities of importers, especially when the manufacturer is outside the EU. For the supervisory authorities it is especially helpful to have a partner in the EU, which has full responsibility and all the technical documentation. According to France this could possibly be done by creating a concept of "first placer on the market", which would need to be an economic operator on the EU territory (manufacturer, agent or importer if the manufacturer outside the EU).

Improving the opportunities for the European market surveillance authorities to impose penalties on operators in third countries by means of agreements between the EU and third countries was also pointed out. It was also proposed to have a sustainable education strategy on the existing European rules in third countries that export mainly to Europe but also some guidelines on how to deal with different types of non-conformity (e.g. should a product be rejected at the border if there are shortcomings in labelling?). Measures must be proportionate and consistent across the EU.

4.2.6

Better control of Internet commerce

E-commerce is a great challenge because it’s very difficult to trace products which are imported from non-EU countries, and to get the required information from the economic operators who are responsible for the product. A solution would be to improve market surveillance organisation and strategies with respect to internet commerce, as well as broadening the concept of economic operators.

There is an agreement on the need to incorporate Fulfilment Houses into new legislation (in particular, this might be achieved by including it in a revised Regulation on Market Surveillance), but also the need for clarity on market surveillance tools to be used for products bought online, either through guidance documents or legislative action.

The biggest future challenge in e-commerce is the changeover from imports of big consignments (containers with a number of the same products) sent to a distributer vs. a high number of small consignments consisting of only one product sent directly to the end user. In such a scenario, market surveillance authorities can only learn of a case when they are involved by customs.

Stronger border controls are also an important factor in terms of control procedures of products sold online. It is also necessary to improve the way authorities communicate market surveillance work electronically.

A Member State stresses the need for authorities' powers to purchase goods to be tested and to increase the budget for purchase and test of products found online. It also notes that MSAs face similar problems to those presented by Internet sales in cases of sales via catalogues (for example for construction products).

As to the products purchased through e-commerce platforms, the need to develop a method covering both border control, testing and cross-border communication between market surveillance and customs authorities is noted.

The Commission should capitalise on the opportunity presented by the revision of the E-commerce Directive and submit to the competent service the feedback from ADCOs on the needs of market surveillance over the internet.

4.2.7

More and/or better use of resources; tools to support market surveillance authorities

Lack of resources has prevented some authorities from carrying out sufficient market surveillance in some specific sectors. Often, resources are just enough to cover one part of the total market surveillance activities as initially foreseen, so some specific sectors are neglected.

In the current climate it is unrealistic to expect Member States to attribute more funding to market surveillance and that the emphasis should be on how to use the existing allocation of resource more effectively, and to consider better and more effective ways to improve market surveillance. The Primary Authority system is considered as a good example of a model which the Commission and other Member States might wish to adopt more broadly.

The problem of limited resources can only be tackled by streamlining the whole market surveillance process, from planning to sanction the use of the latest technologies. The following specific suggestions are put forward:

Carry out studies on the inherent risk of the different product categories under the different directives; as an example, see the preliminary study for the next Ecodesign working plan.

Collect information on the number of product categories on the European market: this is one of the crucial factors in determining the “adequate scale of the checks” stipulated in Art. 19 (1) of Reg. 765.

Consider mandatory registration in a product database, as is done partially under the RED, and is envisaged for energy labelling and adaptation of existing registration obligations (WEEE directive) to make them suitable for market surveillance planning.

Facilitate checks at the border by including information on the manufacturer in customs declarations, and amending CN (Combined Nomenclature) to make it useful for market surveillance purposes.

Facilitate documentary checks via a digital compliance system (see below) and by including compulsory photos in the DoC to enable a positive identification of products, EAN (Bar)-Codes and CN-Codes.

Future standardisation mandates, including affordable preliminary testing: only products exceeding the preliminary limits would deserve full testing.

Simplification of reporting duties by providing an integrated IT solution from planning to documentary checks to product identification and reporting.

Market surveillance should be risk-based and should focus on the minority of non-compliant products that pose a high risk to persons, livestock and property, while other non-conformities should be addressed by means of education of businesses (see proposals under section 4.1 above).

The lack of notified bodies and testing laboratories in many technical areas is stressed, which makes testing of products expensive. This lack of laboratories might be a problem in some sectors, however not in all.

For market surveillance authorities without their own laboratories, budget and administration of external testing costs are a major issue limiting the effectiveness of their surveillance. Thus, programs facilitating sufficient laboratory capacity would be necessary. EU-wide agreements with laboratories, to which market surveillance authorities could send products to be tested on a pro-rata basis, would be a perfect solution.

This option of EU-wide agreements with laboratories is also proposed by another Member State, while another one suggests EU financial support from the Commission for laboratory tests (rather than for 'joint actions', which imply prohibitive administrative costs for MSAs).

On the other hand, the availability of laboratories is not considered as an issue by other Member States, since they believe they have excellent access to a number of test laboratories (test houses) which are also available for other Member States to use. It is not necessary or proportionate to introduce this at a supranational level.

A Member State also stresses the need for: (i) an on-line database where the national market surveillance authorities would be able to download the harmonised standards; (ii) the creation of a rapid advice forum at EU level; (iii) legal assistance from the Commission.

The simplification of the work of national authorities by means of an easier administration of joint actions and an integrated reporting system is suggested.

A very serious reshaping by the Commission of the internal approval procedure for joint actions is needed.

Finally, the need for adequate and reliable 'facts and figures' on products, volumes and economic operators is stressed as a necessary basis for developing and improving a risk-based approach. This kind of information is also considered useful in showing the importance of market surveillance.

4.2.8

Stronger measures against economic operators; Penalties

There is a need to take stricter measures against economic operators and to apply sanctions against economic operators located in third countries.

The harmonisation of the levels of penalties has been considered by one Member State, while keeping the possibility to adapt them on a case by case basis.

However, another Member State considers that penalties must remain the responsibility of Member States – it is for the Member State to determine what is effective, proportionate and deterrent. It is therefore also for the Member State to revise its legislation if it does not provide a sufficient deterrent.

For SMEs especially, limited financial leeway implies limited ability to react to more deterrence.

4.2.9

Digital compliance

There should be a greater emphasis on e-commerce and e-compliance as there are many more opportunities to take advantage of new and developing technology and make market surveillance more effective (e.g. using e-labelling whereby relevant information is provided online at the point of purchase).

Studying the impact of a possible e-compliance system, which could be useful for strengthening border controls, is supported: the system could be tried for products manufactured outside the EU, for which the technical documentation is more complicated to obtain.

The need for a database where manufacturers upload their declarations of conformity, technical documentation and instructions for easy reference by market surveillance authorities is stressed. This database would facilitate data collection of checked products but also provide an excellent basis for information on new and revised products on the market.

By contrast, other Member States strongly disagree with the suggestion of developing a digital compliance system. Some of the reasons reported are:

·The main problem for market surveillance authorities is not access to documentation but the fact that the documentation received does not always correspond to the actual product. The problem of falsified certificates etc. will not be solved by a digital system.

·The authorities cannot trust the data in the system, because they are supplied by those they are supposed to check.

·While a voluntary system would provide no added value, a mandatory system would create unjustified administrative burdens for economic operators as well as for market surveillance authorities. Compliant economic operators are already put at a competitive disadvantage vis-à-vis rogue traders, who will either report nothing or report false information to the system. Businesses in third countries would more easily escape the application of a mandatory system.

·It could lead to a practice where authorities allow undue time and resources to checking documentation in the database instead of focusing on the actual compliance of products. There is a fear that the emphasis will shift from checking products to checking the data entered in the system, without consideration of the reality of the market.

·There are many questions regarding the confidentiality of data in such a system.

Annex 3: methods and analytical models used in preparing the Evaluation

The methodology used in preparing the valuation consists of the desk research, the field research and the case studies.

The desk research focused on an in-depth review of the national market surveillance programmes and reports drafted by Member States pursuant to Article 18(6) of Regulation (EC) 765/2008 covering also the sectoral impact assessments drafted by the European Commission for the relevant product categories covered by the Regulation, together with other policy documents relevant for market surveillance such as the Impact Assessment (IA) for the Regulation or the IA for the Product Safety and Market surveillance Package.

The market analysis is aimed at providing an understanding of the market for which EU harmonised product rules exist and at assessing the main trends in the intra EU trade of harmonised products. In order to identify the variables to be included in the analysis, we started from the reference list of sectors included in the EC template in its version published on 26 October 2015 and we tried to identify the available statistics that are useful for the scope of the study. A two-stage approach was implemented: an analysis at the sectoral level oriented towards the macro dimension and an analysis at the product level focused on the value of products that are traded within the EU internal market and for which EU harmonised rule exist (hereafter harmonised products).

Results from these analyses have been combined to identify the sectors whose trade value in harmonised products is more relevant.

The field research made use of a combination of field research tools, namely five targeted surveys and 23 interviews, plus the results of a Public Consultation launched by the Commission.

As for the geographical coverage of the stakeholder consultation, all EU Member States, together with Iceland, Norway, Switzerland and Turkey, were involved in the consultation.

Five thematic case studies aimed at gathering a deeper understanding of all the issues covered by the evaluation questions. Each case study required four interviews for in-depth investigation.

Detailed analysis of each method is provided in Annex 4.

Annex 4: Ex-post evaluation of regulation (ec) no 765/2008

ABSTRACT (EN)

Regulation (EC) No 765/2008 aims at strengthening the protection of public interests, through reducing the number of non-compliant products on the EU Internal Market, and at ensuring a level playing field among economic operators, providing a framework for market surveillance and controls of products.

The evaluation aimed at understanding to what extent the Regulation has achieved these objectives. Moreover, it analysed the Regulation’s practical implementation in the EU Member States and assessed the market for products in its scope.

The evaluation concluded that the Regulation is not fully effective in achieving its objectives. Moreover, it has a limited cost effectiveness due to its partial achievement of both expected results and impacts, and to both resources allocated to enforcement and related activities not being correlated to the size of surveyed markets. The needs addressed by the Regulation are still relevant, although there exist a number of issues that could call this into question, particularly with respect to increasing online trade and budgetary constraints at national level. Moreover, the scope of the Regulation is not fully clear and its market surveillance provisions suffer from a lack of specificity. This allowed for different implementations at the national level, which impact on the level of uniformity and rigorousness of market surveillance controls across the EU. Finally, the coherence of the Regulation with respect to the GPSD and sectoral directives is not straightforward and this reduces the clarity of the overall framework for market surveillance.

ABSTRACT (FR)

Le règlement (CE) N° 765/2008 vise à renforcer la protection des intérêts publics en réduisant le nombre de produits non conformes sur le marché intérieur de l'Union Européenne (EU). Il vise également à assurer des conditions équitables entre les opérateurs économiques en fournissant un cadre pour la surveillance du marché et le contrôle des produits.

L’objectif de l’évaluation était de comprendre dans quelle mesure le règlement a atteint ces objectifs. En outre, les analyses de la mise en œuvre du règlement dans les États membres et du marché inclut dans son champ d’application ont été conduites.

En conclusion, il apparait que le règlement n'est pas pleinement efficace dans l’accomplissement de ses objectifs. De plus, il a un rapport coûts-efficacité limité en raison de l’accomplissement partiel soit des résultats soit des impacts attendus, ainsi que des ressources deployées et des activités connexes à l'exécution qui ne sont pas corrélées à la taille des marchés contrôlés. Les besoins abordés par le règlement sont toujours pertinents, bien qu'il existe des problèmes susceptibles de les remettre en question, en particulier en ce qui concerne l'augmentation des pratiques de commerce en ligne et des contraintes budgétaires au niveau national. En outre, le champ d'application du règlement n'est pas entièrement clair et ses dispositions manquent de spécificité. Ceci a conduit à des implémentations différentes au niveau national, qui ont eu un impact sur le niveau d'uniformité et de rigueur des contrôles du marché dans l'UE. Enfin, la cohérence du règlement par rapport à la DSGP et aux directives sectorielles n'est pas toujours évidente, ce qui réduit la clarté du cadre général de la surveillance du marché.

ABSTRACT (DE)

Die Verordnung (EG) Nr. 765/2008 hat das Ziel, die öffentlichen Interessen zu schützen, indem sie die Anzahl der nichtkonformen Produkte im europäischen Binnenmarkt reduziert und durch die Vorgabe eines Rahmens für die Marktüberwachung und die Produktkontrolle allen Wirtschaftsakteuren die selben Wettbewerbsbedingungen garantiert.

Die Evaluation hatte zum Ziel, zu verstehen, in welchem Ausmass die Marktüberwachungsbestimmungen der Verordnung ihre Zielsetzung erreicht haben. Zudem wurde die konkrete Umsetzung dieser Bestimmungen in den EU Mitgliedstaaten analysiert und der Markt für Waren im Geltungsbereich der Verordnung festgestellt.

Die Evaluation kam zu dem Schluss, dass die Verordnung ihr Ziel nicht vollständig erreicht hat. Ausserdem weist diese eine eingeschränkte Kostenwirksamkeit auf, was einerseits darauf zurückzuführen ist, dass die erwarteten Ergebnisse und Auswirkungen nur teilweise realisiert wurden, und andererseits auf eine fehlende Korrelation der Durchsetzungsressourcen und –tätigkeiten mit der Größe der befragten Märkte. Die in der Verordung angegangenen Bedürfnisse sind immer noch relevant, obwohl eine gewisse Anzahl an mit der Marktüberwachung der Online-Verkäufe und den steigenden nationalen Haushaltszwängen verbundenen Angelegenheiten besteht, die dies in Frage stellen könnten. Zudem ist der Rahmen der Verordung nicht eindeutig definiert und die darin enthaltenen Marktüberwachungsbestimmungen leiden unter einem Mangel an Spezifität. Dies hat auf nationaler Ebene zu verschiedenen Implementationen geführt, welche die Einheitlichkeit und Rigorosität der europaweiten Marktüberwachungskontrollen beeinträchtigen. Die Schlüssigkeit der Verordnung, was die Richtlinie über die allgemeine Produktsicherheit und die sektorspezifischen Richtlinien betrifft, ist nicht eindeutig und dadurch reduziert sich die Klarheit der gesamten Rahmenbedingunen der Marktüberwachung.

EXECUTIVE SUMMARY (EN)

Regulation (EC) No 765/2008 (hereinafter also referred to as ‘the Regulation’) setting out the requirements for accreditation and market surveillance relating to the marketing of products and repealing Regulation (EEC) No 339/93 has been applicable since 1 January 2010. The Regulation has the strategic objectives of ‘strengthening the protection of public interests through the reduction of the number of non-compliant products on the EU Internal Market and ensuring a level playing field among economic operators’, providing a framework for market surveillance and product control.

The evaluation

The evaluation performed aimed at understanding to what extent the Regulation has achieved its original objectives in terms of effectiveness, efficiency, relevance, coherence, and EU added value. Moreover, it analysed the practical implementation of the Regulation in EU Member States and assessed the product market within the scope of the Regulation.

This evaluation also aimed to contribute to the identification of the relevant set of actions supporting this Regulation within the framework of the Single Market Strategy.

Effectiveness

The evaluation concluded that the Regulation is not fully effective.

In particular, although a plethora of coordination and communication mechanisms and tools for information exchange exist within and between the individual Member States and with third countries, these do not work efficiently or effectively enough (e.g. Market surveillance authorities (MSAs) rarely restrict the marketing of a product following the exchange of information on measures taken by other MSAs; and in the context of products manufactured outside the national territory, MSAs find it difficult to contact the economic operator even if it is based in another EU Member State). Moreover, Member States have implemented the Regulation in many different iterations, with substantial variations in terms of organisational structures, level of resources deployed (financial, human and technical), market surveillance strategies and approaches, powers of inspection, and sanctions and penalties for product non-compliance. Finally, although Customs’ powers are perceived as adequate and procedures for border controls are clear and appropriate, checks on imported products are still considered inadequate in light of increasing import from third countries – particularly China – and online sales.

All these elements have had an impact on achieving uniform and sufficiently rigorous controls. Thus, they have also had an impact on the effectiveness of the measure in achieving its objectives in terms of protecting public interests and the level playing field for EU businesses.

The Regulation’s effectiveness towards achieving its objectives is also thrown into question by the increasing number of non-compliant products included in its scope, as demonstrated by the rising number of RAPEX notifications and restrictive measures taken by MSAs. An important reason for product non-compliance in the internal market seems to relate in particular to a lack of knowledge among economic operators about the applicable legislative requirements.

Efficiency

The Regulation introduces costs for Member States and, to a more limited extent, for economic operators. The former are related to organisational, information, surveillance, and cooperation obligations; costs for economic operators relate to information obligations, as defined in Article 19 of the Regulation.

The budget allocated to MSAs in nominal terms varies considerably from one Member State to another. These differences might be related to the fact that Member States have different organisational models requiring different levels of financial resources. However, another possible explanation might be sought in the different approaches followed by MSAs in reporting data on the level of financial resources used and on activities performed.

The fact that Member States are free to define their own approaches to market surveillance created a significant variation in the way the different sectors are controlled and managed. Moreover, fragmentation of control activities throughout the internal market may interfere with timely action by the authorities and cause additional costs for businesses.

As regards costs for economic operators, information costs are not perceived as significant although some cross-border inconsistencies still remain and the current enforcement mechanism is unable to create a level playing field for those businesses marketing products in the internal market. This might reduce businesses' willingness to comply with the rules and discriminate against businesses that abide by the rules and those who do not.

The analysis of RAPEX database and of national reports highlighted that product non-compliance increased consistently from 2006-2009 to 2010-2015.

The limited cost effectiveness of the market surveillance provisions is confirmed by the fact that neither the average annual budgets allocated to MSA activities nor their variation during the period 2011-2013 correlate with the size of the market (i.e. number of enterprises active in the harmonised sectors).

Relevance

Overall, the Regulation is relevant, although the study concluded there were issues which could put this into question.

For instance, the scope of the Regulation is not fully clear. This drawback could eventually be exacerbated by technological developments which introduce new types of products. As for the Regulation’s definitions, although they are generally clear and appropriate, they are not complete and up to date, especially when considering the need to address online sales. The concept of lex specialis represents a suitable interface to address market surveillance in specific sectors. However, some issues have emerged regarding a lack of clarity in the scope of market surveillance rules in sector-specific legislation.

Considering the relevance of the Regulation to stakeholders’ needs, the analysis concluded that it is relevant to some extent. Overall, it is relevant when considering current needs associated to its general and specific objectives, but it becomes less relevant when referring to the needs related to new/emerging dynamics, especially with reference to increasing online trade and budgetary constraints at the national level.

Coherence

The evaluation concluded that the Regulation’s market surveillance provisions are coherent within themselves; and the roles and tasks of all the different stakeholders are well defined and there are no traces of duplication of activities. However, they suffer from a lack of specificity, which has allowed for discrepancies in implementation of the Regulation at the national level. As for external coherence, some issues have been identified between the GPSD and the Regulation mainly in terms of definitions provided, which are not always aligned. Moreover, the boundary between the two legislations is not always clear. Similarly, the Regulation’s coherence with sectoral directives is questioned, as there are discrepancies and gaps in the definitions and terminology provided in the different legislative pieces. Although not hindering the implementation of the Regulation, these inconsistencies diminish the overall clarity of the framework for market surveillance, causing some uncertainties in its application.

EU added value

The analysis focused on assessing the EU added value as per the Regulation’s specific provisions. Its EU added value mainly stems from provisions envisaging common information systems for cooperation and coordination, favouring administrative cooperation, and enhancing collaboration between Customs and MSAs. Conversely, the EU added value provided by provisions related to collaboration between Member States, market surveillance organisation at national level and national programmes and reports has not reached its full potential.

RÉSUMÉ (FR)

Le règlement (CE) N° 765/2008 (ci-après dénommé "le règlement") fixant les prescriptions relatives à l'accréditation et à la surveillance du marché pour la commercialisation des produits est devenu applicable depuis le 1er janvier 2010. Le règlement vise à renforcer la protection des intérêts publics à travers la réduction du nombre de produits non conformes sur le marché intérieur de l'UE et à assurer l'égalité des conditions entre les opérateurs économiques, en fournissant un cadre pour la surveillance du marché et le contrôle des produits.

L'évaluation

L'évaluation portait sur les dispositions de surveillance du marché du règlement. L’objectif était de comprendre dans quelle mesure le règlement a atteint ses objectifs en termes d'efficacité, d’efficience, de pertinence, de cohérence et de la valeur ajoutée de l'UE. En outre, les analyses de la mise en œuvre du règlement dans les États membres et du marché inclut dans son champ d’application ont été conduites.

Cette évaluation visait également à identifier les actions qui appuient le présent règlement dans le cadre de la Stratégie du marché unique.

Efficacité

En conclusion, il apparait que le règlement n'est pas pleinement efficace.

Bien qu'il existe une pléthore de mécanismes et d'outils de coordination et de communication pour l'échange d'informations au sein et entre les différents États membres et avec les pays tiers, ceux-ci ne fonctionnent pas efficacement ou efficientement (par exemple, les autorités de surveillance du marché restreignent rarement la commercialisation d'un produit suite à l'échange d'informations sur les mesures prises par d'autres autorités de surveillance et, dans le cadre de produits fabriqués en dehors du territoire national, les autorités de surveillance ont des difficultés à contacter l'opérateur économique même s’il est basé dans un autre État membre de l'UE. En outre, les États membres ont mis en œuvre le règlement de différentes façons, avec des variations substantielles en termes de structures organisationnelles, de niveau de ressources déployées (financières, humaines et techniques), de stratégies et d'approches de surveillance du marché, de pouvoirs d'inspection et de sanction, et de pénalités pour les produits non conformes. Enfin, bien que les pouvoirs des douanes soient perçus comme adéquats et que les procédures de contrôle des frontières soient claires et appropriées, les contrôles des produits importés sont encore considérés comme insuffisants à la lumière des importations croissantes en provenance de pays tiers - en particulier de la Chine - et des ventes en ligne.

Tous ces éléments ont eu un impact sur l’uniformité et la rigueur des contrôles. Par conséquent, ils ont également eu un impact sur l'efficacité de la mesure à atteindre de ses objectifs en termes de protection des intérêts publics et de conditions équitables pour les entreprises de l'UE.

L'efficacité du règlement dans la réalisation de ses objectifs est également mise en question par l'augmentation du nombre de produits non conformes inclus dans son champ d'application, comme en témoigne le nombre croissant des notifications sur RAPEX et des mesures restrictives prises par les autorités de surveillance du marché. Une raison importante pour la non-conformité des produits sur le marché intérieur semble concerner en particulier un manque de connaissance des opérateurs économiques des exigences législatives applicables.

Efficience

Le règlement introduit de nouveaux coûts pour les États membres et, de manière plus limitée, pour les opérateurs économiques. Les coûts pour les États membres sont liés aux obligations d'organisation, d'information, de surveillance et de coopération. Les coûts pour les opérateurs économiques sont liés aux obligations d'information définies à l'article 19 du règlement.

Le budget alloué aux autorités de surveillance du marché en termes nominaux varie considérablement d'un État membre à l'autre. Ces différences pourraient être liées au fait que les États membres ont des modèles organisationnels différents, qui nécessitent différents niveaux de ressources financières. Cependant, une autre explication pourrait être explorée attrayant aux différentes approches suivies par les autorités de surveillance du marché dans la déclaration des données concernant les ressources financières utilisées ainsi que les activités réalisées.