This document is an excerpt from the EUR-Lex website

Document 52021XC1028(01)

Communication from the Commission to the European Parliament, the Council and the Court of Auditors – Annual Accounts of the European Union 2020

Communication from the Commission to the European Parliament, the Council and the Court of Auditors – Annual Accounts of the European Union 2020

Communication from the Commission to the European Parliament, the Council and the Court of Auditors – Annual Accounts of the European Union 2020

OJ C 436, 28.10.2021, pp. 1–206

(BG, ES, CS, DA, DE, ET, EL, EN, FR, HR, IT, LV, LT, HU, MT, NL, PL, PT, RO, SK, SL, FI, SV)

|

28.10.2021 |

EN |

Official Journal of the European Union |

C 436/1 |

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL AND THE COURT OF AUDITORS

Annual Accounts of the European Union 2020

(2021/C 436/01)

CONTENTS

| FOREWORD | 2 |

| FINANCIAL HIGHLIGHTS OF THE YEAR | 3 |

| NOTE ACCOMPANYING THE CONSOLIDATED ACCOUNTS | 33 |

| CONSOLIDATED FINANCIAL STATEMENTS AND EXPLANATORY NOTES | 34 |

| BALANCE SHEET | 35 |

| STATEMENT OF FINANCIAL PERFORMANCE | 36 |

| CASHFLOW STATEMENT | 37 |

| STATEMENT OF CHANGES IN NET ASSETS | 38 |

| NOTES TO THE FINANCIAL STATEMENTS | 39 |

| BUDGETARY IMPLEMENTATION REPORTS AND EXPLANATORY NOTES | 130 |

| GLOSSARY | 200 |

| LIST OF ABBREVIATIONS | 204 |

FOREWORD

2020 has been an extraordinary year by any measure: Facing economic and political challenges caused by the coronavirus pandemic, the European Union had to react with unprecedented solutions and speed. The European Commission has been working on all fronts to save lives and livelihoods, to support national health systems and companies, to foster recovery and resilience. We have mobilised all means at our disposal to help Member States coordinate their national responses and to help those most affected by the crises, using instruments such as the Coronavirus Response Investment Initiative or SURE (Support to mitigate Unemployment Risks in an Emergency). Under SURE an amount of EUR 39,5 billion out of a total of EUR 100 billion has already been disbursed in 2020 to affected Member States to address sudden increases in public expenditure for the preservation of employment. Further substantial disbursements followed in 2021.

While fighting the pandemic, the European Union nevertheless delivered on its policy objectives, with a focus on young people, jobs and growth, as well as climate change. Measures to support economic growth and reduce the economic gaps between regions amounted to nearly half of the funds committed. EU funding contributed EUR 29,7 billion to less developed regions and EUR 16,4 billion to research and innovation under Horizon 2020. Furthermore, the 2020 EU budget helped agriculture and rural areas under the European Agricultural Guarantee Fund and Agricultural Fund for Rural Development with total commitments of EUR 59 billion. The 2020 budget was the final budget of the current multiannual financial framework, with budget implementation totalling EUR 181,7 billion in commitments made — adding value for all Europeans.

Finally, 2020 was also the year of the agreement on the EU’s long-term budget for 2021-2027 of EUR 1,074 trillion (in 2018 prices), boosted by EUR 750 billion through NextGenerationEU, a temporary instrument to kickstart the recovery and steer the transition towards a more sustainable and digital Europe.

It is my pleasure to present the 2020 annual accounts of the European Union. They provide a complete overview of EU finances and the implementation of the EU budget for the last year, including information on contingent liabilities, financial commitments and other obligations of the Union. The consolidated annual accounts of the European Union are part of the Commission’s integrated financial and accountability reporting package and form an essential part of our highly developed system of financial accountability.

Johannes HAHN

Commissioner for Budget and Human Resources

FINANCIAL HIGHLIGHTS OF THE YEAR

|

The objective of the Financial Statements Analysis, which has been prepared on the basis of the principles outlined in the IPSASB Recommended Practice Guideline (RPG) 2 ‘Financial Statement Discussion and Analysis’ is to assist readers to understand how the operational, financial and investment activities of the EU are reflected in the different elements of the consolidated financial statements of the EU. The information presented in this section has not been audited It should be noted that due to the rounding of figures into millions of euros, some financial data in the tables below may appear not to add up. |

CONTENTS

|

1. |

KEY FIGURES 2020 | 4 |

|

2. |

CORONAVIRUS RESPONSE | 5 |

|

2.1. |

Highlights of the EU’s coronavirus response | 5 |

|

2.2. |

Response initiatives under 2014-2020 multiannual financial framework (MFF) and SURE programme | 7 |

|

3. |

THE LONG-TERM EU BUDGET 2021-2027 AND NEXT GENERATION EU | 11 |

|

4. |

DEPARTURE OF THE UNITED KINGDOM FROM THE EUROPEAN UNION | 13 |

|

4.1. |

Background | 13 |

|

4.2. |

UK Share | 14 |

|

4.3. |

EU annual accounts: Amounts owed by and to the UK under the Withdrawal Agreement | 14 |

|

5. |

SUMMARY OF BUDGET IMPLEMENTATION | 17 |

|

6. |

FINANCIAL INSTRUMENTS AND BUDGETARY GUARANTEES | 18 |

|

6.1. |

Financial instruments financed by the EU budget | 18 |

|

6.2. |

Financial assets held in guarantee funds for budgetary guarantees | 18 |

|

6.3. |

Loans and related borrowings for financial assistance programmes | 19 |

|

6.4. |

Budgetary contingent liabilities for financial assistance programmes | 23 |

|

7. |

FINANCIAL STATEMENTS ANALYSIS | 24 |

|

7.1. |

REVENUE | 24 |

|

7.2. |

EXPENSES | 25 |

|

7.3. |

ASSETS | 26 |

|

7.4. |

LIABILITIES | 27 |

|

8. |

EU POLITICAL AND FINANCIAL FRAMEWORK, GOVERNANCE AND ACCOUNTABILITY | 28 |

|

8.1. |

POLITICAL AND FINANCIAL FRAMEWORK | 29 |

|

8.2. |

GOVERNANCE AND ACCOUNTABILITY | 30 |

1. KEY FIGURES 2020

The EU budget in 2020 — Implementation of commitment appropriations

|

EUR 181,7 bn implemented to deliver on the EU’s policy objectives: |

||

|

|

||

|

|

The EU coronavirus response |

|

SURE — Amounts granted in 2020 |

|||||

|

Instrument |

agreed EUR bn |

Member State |

granted EUR bn |

||||

|

Next Generation EU |

750 |

|

Italy |

27,4 |

|||

|

SURE (*) |

100 |

Spain |

21,3 |

||||

|

Macro-financial assistance |

3,0 |

Poland |

11,2 |

||||

|

ESI |

2,7 |

Belgium |

7,8 |

||||

|

UCPM |

0,3 |

Portugal |

5,9 |

||||

|

Total |

856,0 |

Romania |

4,1 |

||||

|

|

Greece |

2,7 |

|||||

|

Other |

9,9 |

||||||

|

(*) of which EUR 39,5 bn disbursed in 2020 |

Total granted in 2020 |

90,3 |

|||||

|

|

||||||

Consolidated financial statements

The consolidated financial statements of the EU comprise more than 50 entities (including the European Parliament, the Council, the Commission and EU agencies). The European Commission is the most significant entity, accounting for 98 % of the total assets of the consolidated financial statements.

The EU accounts are prepared according to the highest available standards, the International Public Sector Accounting Standards (IPSAS). Adhering to these standards ensures that the accounts provide relevant, reliable, comparable and understandable financial information for citizens. They provide information on the financial position (balance sheet) of the EU as well as detailed explanations of its assets, liabilities, financial commitments and obligations. They also show how the EU budget was implemented during the year.

|

EUR billion |

||||

|

|

2020 |

2019 |

||

|

ASSETS |

|

|

||

|

Financial assets |

113,1 |

71,2 |

||

|

Pre-financing |

62,7 |

51,4 |

||

|

Receivables |

74,5 |

24,0 |

||

|

Cash and cash equivalents |

16,7 |

19,7 |

||

|

Property, plant and equipment and other assets |

13,0 |

12,6 |

||

|

Total |

280,0 |

178,9 |

||

|

LIABILITIES |

|

|

||

|

Post-employment benefits |

116,0 |

97,7 |

||

|

Financial liabilities |

95,0 |

54,5 |

||

|

Payables |

32,4 |

27,2 |

||

|

Accruals |

64,6 |

67,2 |

||

|

Other liabilities |

5,4 |

4,8 |

||

|

Total |

313,5 |

251,5 |

||

|

NET ASSETS |

|

|

||

|

Reserves |

5,1 |

5,0 |

||

|

Amounts to be called from Member States |

(38,5 ) |

(77,6 ) |

||

|

Total |

(33,4 ) |

(72,5 ) |

||

|

||||

2. CORONAVIRUS RESPONSE

2.1. HIGHLIGHTS OF THE EU’S CORONAVIRUS RESPONSE

Since the outbreak of the COVID-19 pandemic, the European Commission has taken resolute action to reinforce the public health sectors and mitigate the socio-economic impact in the European Union. Based on the 2014-2020 multiannual financial framework (MFF), the European Commission has mobilised all means at its disposal to help Member States coordinate their national responses and provided objective information about the spread of the virus and effective efforts to contain it.

Timeline of actions taken (1)

|

— |

2 April Coronavirus response: European Commission mobilises every euro to protect lives and livelihoods |

|

— |

14 April €2,7 billion from the EU budget to support the healthcare sector |

|

— |

16 April President von der Leyen: ‘The European budget will be the mothership of Europe’s recovery’ |

|

— |

22 April €3 billion financial assistance package for ten enlargement and neighbourhood countries |

|

— |

27 May Europe’s moment: major €2,4 trillion Recovery Plan for Europe unveiled to repair and prepare for the next generation |

|

— |

4 June European Commission pledges €300 million to the Vaccine Alliance |

|

— |

21 July European leaders reach a deal on the recovery plan and European long-term budget 2021-2027 |

|

— |

25 August European Commission proposes to provide €87,3 billion in financial support for 16 Member States under SURE |

|

— |

17 September European Commission presents next steps for €672,5 billion Recovery and Resilience Facility |

|

— |

22 September European Commission welcomes finalisation of guarantee system for €100 billion SURE instrument |

|

— |

7 October European Commission to issue EU SURE bonds of up to €100 billion as social bonds |

|

— |

27 October European Commission disburses first €17 billion SURE instalments to Italy, Spain and Poland |

|

— |

10 November European Commission welcomes agreement on €1,8 trillion EU long-term budget and NextGenerationEU to help build greener, more digital and more resilient Europe |

|

— |

17 November European Commission disburses €14 billion to nine Member States under the SURE instrument |

|

— |

1 December European Commission disburses €8,5 billion under SURE to five Member States to help sustain jobs |

|

— |

17 December European Commission welcomes the adoption of the EU's long-term budget for 2021-2027 |

2.2. RESPONSE INITIATIVES UNDER 2014-2020 MULTIANNUAL FINANCIAL FRAMEWORK (MFF) AND SURE PROGRAMME

The European Union’s interventions under the 2014-2020 MFF to fight the COVID-19 pandemic ranged from immediate actions such as funding urgent medical supplies and increasing medical stockpiles, to introducing more flexibility as regards utilising the financial support from the European Structural and Investment Funds, and to providing loans on favorable terms to both Member States and enlargement and neighbourhood partners. The total direct support from the EU budget amounted to about EUR 70 billion in 2020. This covers commitments that could be redirected to COVID-19 related actions, of which EUR 66 billion came from redeployment and reprioritisation within existing programmes and EUR 4 billion from budgetary reinforcement. The key initiatives are explained in more detail below.

2.2.1. Activation of the Emergency Support Instrument (ESI)

Given the depth of the crisis following the COVID-19 pandemic, as well as the extent and nature of the needs requiring support from the EU budget, the EU reactivated the ESI instrument for a period of 2 years to finance expenditure necessary to address the COVID-19 pandemic for the period 1 February 2020 to 31 January 2022 (see Council Regulation (EU) 2016/369 (2)). To further this objective, the 2020 budget was amended (3). Considering in addition DEC 13/2020 adopted on 24 July 2020, EUR 2,7 billion in commitment appropriations and EUR 2,6 billion in payment appropriations were allocated to the ESI instrument for 2020. The reactivation allows the Union to deploy measures preventing and mitigating severe consequences in one or more Member States and to address, in a coordinated manner, the needs related to the COVID-19 pandemic, by complementing any assistance provided under other EU instruments. The instrument is centrally managed by the Commission and focuses on direct procurement and grants, complemented in certain cases by actions implemented through partners such as international organisations.

In 2020, the Commission signed advance purchase agreements with a number of pharmaceutical companies. Advance purchase agreements help reduce the risk linked to investments made by manufacturers in the development of potential vaccines or aim at ensuring deliveries, and thus maximise the chances of quickly developing, manufacturing and deploying safe and effective vaccines, and ensuring that EU citizens will have access to them. The Commission negotiated with pharmaceutical companies on behalf of EU Member States, leading to the initial signature of six agreements, with further exploratory talks with additional vaccine manufacturers that started in 2020 and are still ongoing in 2021. The first vaccine to be granted conditional marketing authorisation, on 21 December 2020, was produced by BioNTech/Pfizer. Its distribution started within days, in time for the launch of the EU Vaccination Days on 27, 28 and 29 December 2020. This authorisation followed a positive scientific recommendation based on a thorough assessment of the safety, effectiveness and quality of the vaccine by the European Medicines Agency, and was endorsed by the Member States.

As of 31 December 2020, the Commission has contracted 1 965 million doses (of which 1 305 million fixed and 660 million optional).

In 2021, the Commission has contracted a further 2 400 million doses (fixed or optional). However, these doses will be fully paid by the Member States concerned, with no effect on the EU budget.

2.2.2. Support for research

On 4 May 2020, the EU and its partners hosted an international pledging conference which has raised EUR 9,8 billion in pledges from donors worldwide to kick-start global cooperation on coronavirus research. This includes a pledge of EUR 1,4 billion from the Commission, of which EUR 1 billion comes from Horizon 2020.

The EU plays a central role in supporting and coordinating research on infectious diseases, with EUR 4,1 billion invested from 2007 to 2019 through the 7th Framework Programme and Horizon 2020, with further commitments in 2020, in addition to the EUR 1 billion pledge for coronavirus research. Up to date figures of all funding pledged and already mobilised under Horizon 2020 to contribute to the Coronavirus Global Response pledging marathon are available online (4).

Moreover, on 3 March 2020, the Innovative Medicines Initiative (IMI) supported through the European Commission’s Horizon 2020 Framework Programme for Research and Innovation, launched a special fast-track call for the ‘Development of therapeutics and diagnostics combatting coronavirus infections’ with an EU contribution of EUR 45 million, which was subsequently increased to EUR 72 million.

Finally, on 8 June 2020 the Commission awarded nearly EUR 166 million, via the European Innovation Council (EIC) Accelerator Pilot, to 36 companies set up to combat the coronavirus pandemic.

2.2.3. Further reinforcement of the Union Civil Protection Mechanism (UCPM/rescEU)

As a complementary measure to the ESI, the UCPM/rescEU was reinforced to allow wider stockpiling and coordination of essential resource distribution across Europe (see Commission Implementing Decision (EU) 2019/570 (5), as amended by Commission Implementing Decision 2020/414 (6) and Commission Implementing Decision (EU) 2020/452 (7)). To this purpose, the 2020 budget was amended to include a further EUR 0,4 billion in commitment appropriations and EUR 0,2 billion in payment appropriations.

The reinforcement of the UCPM/rescEU supports Member States in purchasing some of the required equipment (including therapeutics, medical equipment, personal protective equipment, laboratory supplies), thus increasing the volume as well as complementing and widening the scope of priority items purchased under the Joint Procurement Agreement, a coordinated approach giving Member States a strong position when negotiating with the industry on availability and price of medical products.

The rescEU direct grants provide 100 % financing from the EU budget, which includes full financing for development of these capacities and full financing for deployment of equipment. The equipment purchased will be hosted by one or more Member States, while decision making is organised at EU level, providing emergency supplies over and beyond national stocks. It will be available to all Member States and will be used in case of insufficient national availability.

2.2.4. Coronavirus Response Investment Initiative (CRII and CRIIplus)

One of the first measures launched by the EU, to support Member States financially in their response to the crisis was the CRII, implemented by Regulation (EU) 2020/460 of the European Parliament and the Council (8) of 30 March 2020. By mobilising unspent money already allocated to EU Member States, the initiative provided an immediate liquidity boost to Member States’ and regions’ budgets and helped them to use cohesion policy funding to finance healthcare expenditure and short-term work schemes, and to offer working capital support for small and medium-sized enterprises. The scope of the European Union Solidarity Fund was also extended to cover major public health emergencies, thereby allowing Member States to receive support under this fund to help them tackle the COVID-19 pandemic.

From April, the CRIIplus, implemented by Regulation (EU) 2020/558 of the European Parliament and the Council (9), made it simpler to quickly make use of existing European Structural and Investment Funds for crisis-related measures, and made it possible to raise the EU’s contribution to cohesion policy programmes to up to 100 % for payment applications submitted between 1 July 2020 and 30 June 2021.

In December, the Commission announced the 2020 results of the two initiatives. Since the beginning of the crisis, the EU has mobilised significant funding to fight the effects of the pandemic. Small and medium-sized enterprises benefited from most of the funding available, over EUR 10 billion, which helped businesses to stay afloat. EUR 3 billion was directed to citizens, including providing social services for vulnerable groups and temporary employment schemes for workers. Lastly, EUR 7 billion was provided to support the health sector, in addition to the EUR 10,2 billion from the EU budget that was already allocated to this area for the years 2014–2020 (note that there is some overlap between the groups of beneficiaries).

2.2.5. Assistance to enlargement, neighbourhood partners and beyond

The EU has so far mobilised over EUR 38,5 billion to fight the coronavirus on a global scale. The Team Europe approach combines resources from the EU, its Member States and financial institutions, including the European Investment Bank and the European Bank for Reconstruction and Development, to support partner countries. Half of the EUR 38,5 billion global response to the coronavirus pandemic has been disbursed.

Moreover, the Commission has concluded ten financial guarantee agreements worth EUR 990 million with partner financial institutions that complete the European Fund for Sustainable Development, the financing arm of the External Investment Plan. The agreements should generate up to EUR 10 billion in investment, to stimulate the economic recovery and strengthen the resilience of EU neighbourhood and African countries.

A further EUR 500 million was allocated to support the COVAX global vaccine initiative, aiming to provide one billion coronavirus vaccine doses for low and middle-income countries in Africa, Asia, the Caribbean and Pacific, as well as in Europe’s Southern and Eastern Neighbourhood. EUR 100 million were allocated by the Commission and EUR 400 million by the European Investment Bank, guaranteed by the European Fund for Sustainable Development, for the participation of low and middle-income countries in the COVAX Advance Market Commitment. On 19 February 2021, the European Union announced an additional EUR 500 million for the COVAX Facility, and the European Commission announced EUR 100 million in humanitarian assistance to support the rollout of vaccination campaigns in Africa.

On 25 May 2020 the European Parliament and the Council adopted Decision (EU) 2020/701 of the European Parliament and of the Council (10) on providing macro-financial assistance to ten enlargement and neighbourhood partners to allow short-term policy space to implement measures to counter the economic fallout from the COVID-19 pandemic with a maximum total of EUR 3 billion in the form of loans. In 2020 a total of EUR 1,0 billion was disbursed as a first instalment to seven countries (Ukraine, Jordan, North Macedonia, Georgia, Kosovo (*1), Moldova and Montenegro). Up until June 2021 a total of EUR 0,6 billion was disbursed to five countries as a first instalment (Albania, Tunisia) or second instalment (North Macedonia, Kosovo, Montenegro). Furthermore, a Memorandum of Understanding with Bosnia and Herzegovina has been signed.

2.2.6. Temporary Support to mitigate Unemployment Risks in an Emergency (SURE) following the COVID-19 pandemic

As part of its emergency support package to tackle the economic impact of the COVID-19 pandemic, the EU adopted on 19 May 2020 Council Regulation (EU) 2020/672 (11) establishing the SURE instrument, to help workers keep their jobs during the crisis. SURE is a temporary scheme which can provide up to EUR 100 billion of financial assistance (loans under favourable terms) to Member States. The instrument enables Member States to request EU financial assistance to help finance sudden and severe increases of national public expenditure, as from 1 February 2020, related to national short-time work schemes and similar measures, including for self-employed persons, or to some health-related measures, in particular in the work place in response to the crisis. To enable the EU to provide financial assistance under SURE, the Commission is empowered to borrow on the capital markets or with financial institutions on behalf of the EU up to a maximum amount of EUR 100 billion. SURE loans are backed by the EU budget and guarantees provided by Member States, according to their share in the EU's GNI. The total amount of guarantees amounts to EUR 25 billion. The instrument is time limited until 31 December 2022.

As of 31 December 2020 the Commission has proposed a total of EUR 90,3 billion in financial support to 18 Member States, all of which has already been approved by the Council. The majority of this amount, EUR 87,3 billion, targeting 16 Member States, has already been proposed by August 2020, with the remaining amount of EUR 3 billion, targeting Hungary and Ireland, proposed in October and November 2020, respectively:

Following the first three SURE bond issuances in October and November 2020, the Commission has disbursed a total of EUR 39,5 billion to 15 EU Member States (Belgium, Croatia, Cyprus, Greece, Hungary, Italy, Latvia, Lithuania, Malta, Poland, Portugal, Romania, Slovakia, Slovenia and Spain, see point 6.3).

The implementation of SURE continued in 2021. In February and March 2021 the Commission has proposed EUR 230 million to Estonia and a further EUR 3,7 billion to Belgium, Cyprus, Greece, Latvia, Lithuania and Malta, increasing the total volume under SURE to EUR 94,3 billion. These additional amounts have been approved by the Council in March and April 2021. Following four further bond issuances in January, March and May 2021, the Commission disbursed a further EUR 50,1 billion, resulting in a total level of disbursements of EUR 89,6 billion.

All the bonds issued under SURE were largely oversubscribed, most of them by double-digit numbers, and attracted a diverse base of EU and international investors. This resulted in very favourable pricing terms. The bonds issued by the EU under SURE benefit from a social bond label. This provides investors with confidence that the funds mobilised will serve a truly social objective. The funds raised are being transferred to the beneficiary Member States in the form of loans to help them cover the costs directly related to the financing of national short-time work schemes and similar measures as a response to the pandemic.

3. THE LONG-TERM EU BUDGET 2021-2027 AND NEXT GENERATION EU

In 2020, the EU provided an unprecedented response to the coronavirus crisis that hit Europe and the world. At the heart of it is a stimulus package worth EUR 2,018 trillion in current prices (EUR 1,8 trillion in 2018 prices). It consists of the EU’s long-term budget for 2021-2027 of EUR 1,211 trillion (EUR 1,074 trillion in 2018 prices), topped up by EUR 807 billion (EUR 750 billion in 2018 prices) through NextGenerationEU, a temporary instrument to power the recovery (12). Taken together, the funds will help repair the economic and social damage caused by the coronavirus pandemic and steer the transition towards a modern and more sustainable Europe.

More than 50 % of the long-term budget and NextGenerationEU will go to new priorities. The money will go to research and innovation, via Horizon Europe; to fair climate and digital transitions, via the Just Transition Fund and the Digital Europe programme; to preparedness, recovery and resilience, via the Recovery and Resilience Facility, the EU’s civil protection mechanism, rescEU, and to the health programme, EU4Health.

30 % of the long-term budget and NextGenerationEU will be spent to fight climate change, the highest share ever of the largest European budget ever.

20 % of NextGenerationEU funds will be invested in the EU’s digital transformation. The funds will help the EU invest more in supercomputing, artificial intelligence, cybersecurity, advanced digital skills and the wider use of digital technologies across the economy and society.

In 2026 and 2027, 10 % of the annual spending under the long-term budget will contribute to halting and reversing the decline of biodiversity.

NEXT GENERATION EU

Amounts raised and spent under NextGenerationEU (NGEU) will be included in the 2021 annual accounts. The first bond issuance, raising EUR 20 billion via a ten-year bond due in 2031, took place on 15 June 2021.

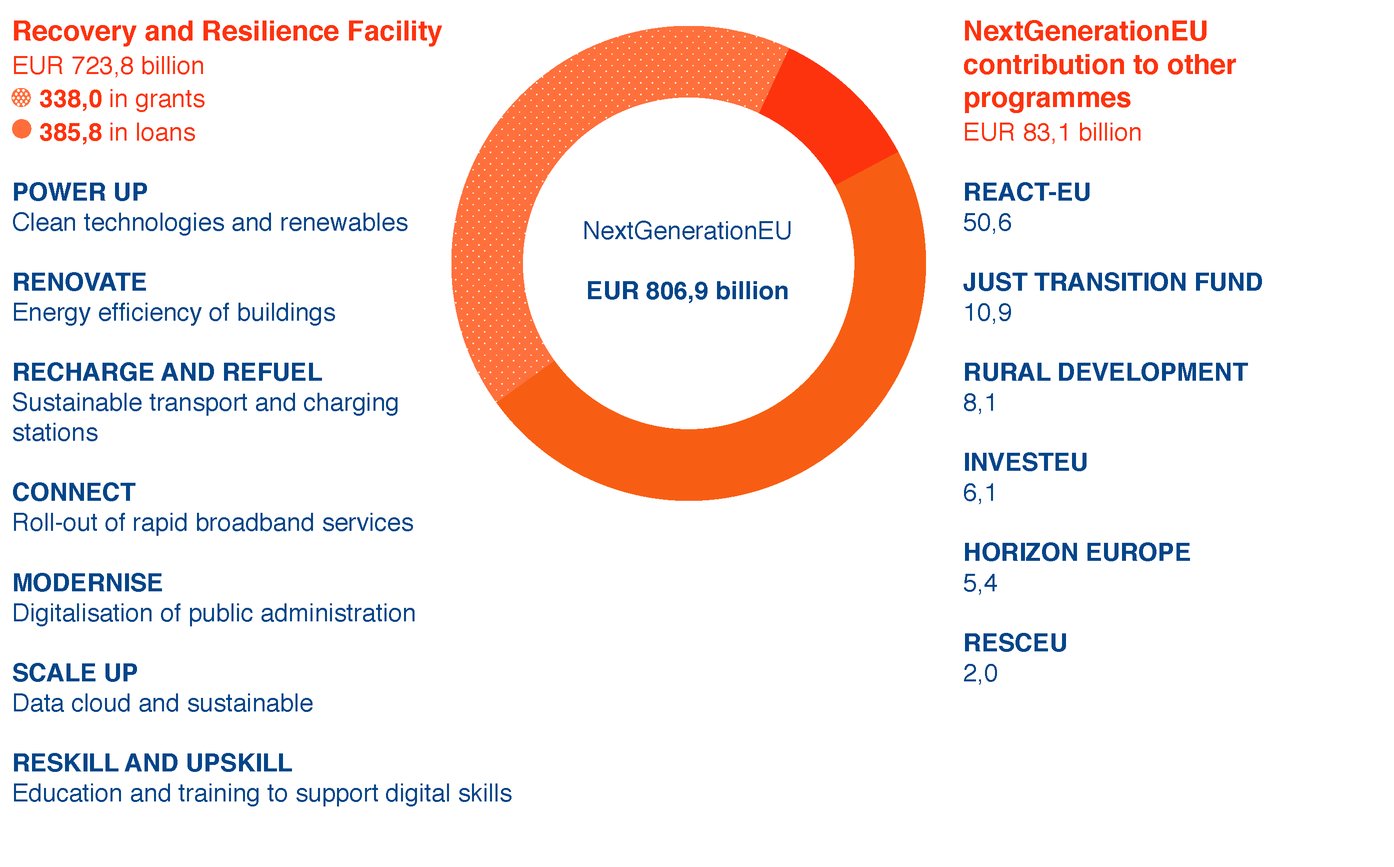

With a budget of EUR 806,9 billion, NextGenerationEU will help repair the immediate economic and social damage brought about by the coronavirus pandemic. The instrument will help build a post-COVID-19 Europe that is greener, more digital, more resilient and better fit for the current and forthcoming challenges.

Part of the funds — EUR 385,8 billion — will be used to provide loans from the Union to individual Member States. These loans will be repaid by those Member States. The other part — EUR 338,0 billion — will be provided in the form of grants or to enable budgetary guarantees for investment support.

The centrepiece of NextGenerationEU is the Recovery and Resilience Facility — an instrument to offer grants and loans to support reforms and investments in the EU Member States to a total value of EUR 723,8 billion. The funds under the Recovery and Resilience Facility will be distributed according to national Recovery and Resilience plans prepared by each Member State, in cooperation with the Commission, and in line with an agreed allocation key.

In addition, NextGenerationEU will reinforce several existing EU programmes:

|

— |

Cohesion, under the Recovery Assistance for Cohesion and the Territories of Europe (REACT-EU), to help address the economic consequences of COVID-19 in the first years of the recovery, |

|

— |

Just Transition Fund, to guarantee that the transition to climate neutrality works for all, |

|

— |

Rural development, to further support farmers, |

|

— |

InvestEU, to support investment efforts of our businesses, |

|

— |

rescEU, so that the EU civil protection mechanism has the capacity to respond to large-scale emergencies, |

|

— |

Horizon Europe, to make sure the EU has the capacity to fund more excellence in research. |

To finance NextGenerationEU, the EU will borrow on the markets with the EU budget as a guarantee. Repayment will take place over a long time horizon, until 2058. This will avoid immediate pressure on Member States’ national finances and enable EU countries to focus their efforts on the recovery.

4. DEPARTURE OF THE UNITED KINGDOM FROM THE EUROPEAN UNION

4.1. BACKGROUND

On 31 January 2020, the United Kingdom (UK) withdrew from the European Union. The terms of its departure are defined in an Agreement on the withdrawal of the UK from the EU and the European Atomic Energy Community (13), also known as the ‘Withdrawal Agreement’ or ‘WA’. As part of this deal, the UK agreed to honour all financial obligations undertaken while it was a member of the EU. The agreement entered into force on 31 January 2020.

|

— |

31 January 2020 The UK officially leaves the Union and the Withdrawal Agrement enters into force |

|

— |

1 February-31 December 2020 Transition period |

|

— |

31 March 2021 Reporting on financial information made by the EU to the UK |

|

— |

16 April 2021 Amounts to be paid are communicated by the EU to the UK |

|

— |

30 June 2021 First payments by the UK under Withdrawal Agreement due to begin |

|

— |

16 September 2021 Amounts to be paid communicated by the EU to the UK |

|

— |

31 October 2021 Second round of payments by the UK to begin |

During the transition period, the UK continued to contribute to and benefit from the EU budget, as if it were a Member State. After the end of the transition period and in line with the WA, the UK will continue to contribute to the EU budget. Equally, the UK will continue to benefit from pre-2021 EU programmes and expenditure as if it was a Member State. The UK will also receive back certain defined monies it paid into the EU budget or monies received by the EU budget linked to its period of membership.

These obligations create liabilities and receivables for the EU which have to be calculated and reflected in the EU’s annual accounts: the 2020 annual accounts show these amounts for the first time, as this is the year the UK left the EU.

These annual accounts therefore contain detailed explanations of the future UK contributions to the EU budget required by the WA, as well as amounts due to the UK. The amounts concerned will be paid by the UK over a long period of time.

The net amount fully respects the three principles underpinning the financial settlement in the WA:

|

— |

no Member State should pay more or receive less because of the UK’s withdrawal from the Union, |

|

— |

the UK should pay its share of the commitments undertaken during its membership, and |

|

— |

the UK should neither pay more nor earlier than if it had remained a Member State. This implies in particular that the amounts that the UK should pay are based on the actual outcome of the budget, i.e. adjusted to implementation. |

The WA also details the methodologies to calculate the various amounts, as explained below.

4.2. UK SHARE

In accordance with Article 139 of the WA, the UK's share of the financial obligations arising from the WA is calculated as a ratio between the own resources made available by the United Kingdom in the years 2014 to 2020 and the own resources made available during that period by all Member States and the United Kingdom. The adjustments resulting from the netting of the VAT and GNI balances for the years 2014 to 2019 are also included. The calculated UK share will be subject to the final adjustments foreseen in Article 139 WA in 2022. The UK share for 2021 is used for the calculations in points (a) and (c) of Article 136(3), and in Articles 140 to 147.

The UK share calculated in accordance with Article 139 WA is 12,358072326018200 %.

4.3. EU ANNUAL ACCOUNTS: AMOUNTS OWED BY AND TO THE UK UNDER THE WITHDRAWAL AGREEMENT

The WA identifies provides for payments obligations between the two parties in particular in the following areas:

|

— |

Own resources (Article 136) |

|

— |

Outstanding commitments (Article 140) |

|

— |

Competition fines (Article 141) |

|

— |

Union liabilities (Article 142) |

|

— |

Contingent financial liabilities and financial instruments (Articles 143 & 144) |

|

— |

Net assets of the European Coal & Steel Community (Article 145) |

|

— |

EU investment in the European Investment Fund, EIF (Article 146) |

|

— |

Contingent liabilities concerning legal cases (Article 147). |

The WA also lays down the methodology as to how these obligations will be dealt with each year — in summary the EU will report twice a year to the UK on the amounts due and the UK will pay these on a monthly basis. The reporting will be updated each year based on actual figures.

The table below summarises the amounts due by the UK to the EU, as well as any amounts due by the EU to the UK, resulting in a net overall receivable for the EU. All calculations have been made in full respect of the WA. These obligations relate to past commitments made when the UK was a Member State of the EU and during the transition period until 31 December 2020, and will expire as soon as they have been paid or if the obligation does not materialise. Payments will be made in line with the procedure set out in Article 148 WA.

|

EUR billion |

||||

|

|

Article 140 |

Article 142 |

Other |

31.12.2020 |

|

Due from the UK |

35,0 |

14,3 |

0,3 |

49,6 |

|

Due to the UK |

— |

— |

(2,1 ) |

(2,1 ) |

|

Net receivable from the UK |

35,0 |

14,3 |

(1,8 ) |

47,5 |

|

Estimated to be paid by the UK after 2021 |

28,2 |

14,3 |

(1,9 ) |

40,6 |

|

Estimated to be paid by the UK in 2021 |

6,8 |

0,0 |

0,0 |

6,8 |

The overall amount comprises the following elements:

Article 136: Own resources

Article 136 establishes the provisions applicable after 31 December 2020 in relation to own resources. The UK is entitled to receive its share of adjustments related to the surplus of the year 2020. It is also subject to any adjustments of VAT and GNI own resources that relate to the financial years until 2020 — these adjustments will be calculated yearly until 31 December 2028. Updates of the UK correction are also made.

The UK is required to pay the traditional own resources collected by them after 28 February 2021, but related to the year 2020 and earlier. Their share of the total made available traditional own resources by the EU 27 and by them is then deducted from this amount. The separate account for traditional own resources shall be fully liquidated at 31 December 2025.

An amount of EUR 230 million is to be paid by the UK during 2021.

Article 140: Outstanding commitments (‘RAL’)

The ‘Reste à liquider’, or ‘RAL’ represents the total volume of legal commitments the EU has made to recipients, for which payments will follow in the coming years. The RAL is a normal feature of all multi-annual budgets, such as the EU budget.

The commitments therefore refer to projects, programmes, agreements or contracts which have already been committed to, before 31 December 2020, but which are not yet fully implemented, with payments still to follow. Some of these payments are for UK recipients.

According to the WA, the UK must pay its share of the EU’s outstanding commitments as of 31 December 2020, the end of the transition period. Any commitments, or parts of it, expected to be cancelled (decommitments) and amounts relating to commitments funded by assigned revenue, or to programmes where UK does not participate (opt outs), are deducted from the total amount.

Other adjustments to the amount owed by the UK under this article are related to the net financial corrections from 2014-2020 or previous programming periods and the Traditional Own Resources relating to 2020 and made available in January-February 2021.

To calculate the UK share of the RAL, the official budgetary RAL as of 31 December 2020 has been used as the starting point (EUR 303,2 billion see table 4.4 in the budgetary implementation tables). As of end-2020, the UK share of the adjusted RAL stood at EUR 36 billion — once adjusted for the forecast of decommitments, the receivable to the EU at end-2020 amounted to EUR 35 billion, of which EUR 6,8 billion will be paid between 30 June 2021 and 31 December 2021.

Article 141 Competition fines

The European Commission directly enforces EU competition rules, by ensuring that all companies compete equally and fairly on their merits. This can lead to the imposition of fines. Once imposed by the EU, fines can be contested (via legal proceedings) by the recipient of the fine — the fine is not definitive until all such proceedings are terminated.

The EU will pay the UK, each year, its share of any competition fines that had been decided upon by the Union before 31 December 2020, once these fines become definitive, i.e. the fined entity either does not introduce an appeal in front the European Court of Justice or the appeal fails and it must pay the fine.

In the annual accounts, the amounts owed to the UK as a result of fines are deducted from the overall amount due by the UK. As of 31 December 2020, the estimated UK share of outstanding fines is EUR 1,8 billion. This amount will be returned to the UK over a long period of time. The figure is based on the outstanding cases at 31 December 2020 and it may change, to reflect the actual amounts entered into the budget after the fines have become definitive.

Article 142 Union liabilities

The UK has committed to pay its share of Union liabilities as of end-2020 except for specified liabilities as laid down in the WA. The UK will therefore be paying its share of obligations linked to the EU as an employer (i.e. pensions and sickness insurance of retired staff), as of 31 December 2020:

|

1. |

Pensions of EU officials: The payments of the pensions of EU staff are covered by the EU annual budget. In addition, EU officials pay pension contributions throughout their working career. These contributions are entered into the budget as revenue, decreasing the contributions needed from Member States to finance the global annual budget. The EU Member States commit to cover the pension costs of EU staff when they retire. In line with this commitment, the UK will be paying, starting in June 2022, its share of the annual pensions paid to EU officials until all the pension rights acquired by staff up to 31 December 2020 are exhausted, over several decades. The UK may decide to settle its obligation at any point, by paying the actuarial liability at that year-end over a period of 5 years. |

|

2. |

Pensions of Members of the European Parliament, European Commissioners, Judges in the European Court of Justice, etc.: The UK will pay its share of the actuarial liability as at 31 December 2020 over a period of 10 years, starting in October 2021. |

|

3. |

Joint Sickness Insurance Scheme (JSIS): this is the system that covers the healthcare costs of EU staff, including pensioners. EU officials and pensioners make contributions to the scheme throughout their career and when retired, as does the EU as an employer. In line with the principle also applied to the pension system of EU officials, the UK will pay its share of the EU’s budget contribution to the healthcare coverage for retired staff. These payments, beginning in June 2022, will continue over several decades, or until all those obligations have been exhausted. As with the pensions of officials, the UK can choose to settle the outstanding obligations at any point in time by paying the actuarial liability at that year-end over a period of 5 years. |

The EU’s liabilities relating to the above post-employment benefit obligations are calculated using audited actuarial valuations based on international standards. The amount attributable to the UK at 31 December 2020 stands at EUR 14,3 billion.

EUR 11 million is due to be paid by the UK during 2021 and relates only to the separate specific pension schemes (e.g. MEPs). The remaining amounts for all schemes will be paid in line with the arrangements outlined above, from 2022 onwards.

Articles 143/144 Financial instruments and Budgetary guarantees

Under these articles, the UK shall be liable to fund the contingent liabilities of the EU stemming from pre-withdrawal date operations in relation to its borrowing, lending and guarantee activities should these crystallise and should they not be covered by the UK share in the existing guarantee funds. The EU will refund to the UK amounts which the UK has already contributed to guarantee funds and which ultimately end up not being needed.

These amounts are primarily:

|

— |

Amounts owed to the UK for its share of the European Fund for Sustainable Development (EFSD) Guarantee Fund where the UK has already contributed through its budget payments but where there have been no approved operations pre-withdrawal, thus no obligations for the UK to cover — EUR 93 million due to be returned to the UK in 2021, |

|

— |

Amounts to be paid to the UK in relation to financial instruments — EUR 46 million, |

|

— |

The UK remains liable to contribute its share of the EU’s contingent liabilities (budgetary guarantees — EFSI, ELM, EFSM and other borrowings, etc.) if these fall due. The maximum obligation of the UK totals EUR 12,9 billion at year-end — see note 4.1 of the EU consolidated annual accounts for more details. The amounts are not due from the UK unless the obligation crystallises in the future and is not covered by a guarantee fund. This is considered unlikely. |

Article 145 European Coal and Steel Community in Liquidation (ECSC i.L.)

The UK is entitled to its share of the net assets of the European Coal and Steel Community (ECSC) in Liquidation at 31 December 2020 — this will be paid to the UK over 5 years. The total amount payable to the UK is EUR 183 million (EUR 37 million to be repaid, i.e., offset against other amounts due in 2021). This means that every year between 2021 and 2025, the amount of EUR 37 million will be deducted from the amounts due by the UK.

Article 146 Investment in the EIF

The UK is entitled to its share of the investment that the EU has made in the paid-in share capital of the European Investment Fund (EIF), payable in equal instalments over 5 years. The total amount payable to the UK is EUR 33 million. This means that every year between 2021 and 2025, the amount of EUR 7 million will be deducted from the amounts due by the UK.

Article 147 Contingent liabilities related to legal cases

The UK must pay, each year, its share of amounts paid out by the EU budget in relation to legal cases concerning events that occurred before 31 December 2020. The estimate of the UK’s share of legal cases that will likely require future payments at year-end is EUR 46 million, but it is not payable by the UK until and unless the cases are settled and a payment is first made by the EU.

5. SUMMARY OF BUDGET IMPLEMENTATION

The 2020 final adopted budget amounted to EUR 173,9 billion of commitment appropriations and EUR 164,1 billion of payment appropriations. Its implementation was heavily impacted by the COVID-19 pandemic and subsequent cross-sectoral crisis. The crisis created a need to take resolute actions to reinforce EU public health sectors and mitigate the socio-economic impact in the EU, as well as provide assistance to third countries. The 2020 budget was the last budget implemented under the Multiannual Financial Framework 2014-2020. Its implementation was carefully monitored and actively managed, which resulted in virtually full implementation of almost all programmes.

The implementation of the total commitment appropriations in 2020 totalled EUR 181,7 billion:

|

— |

EUR 172,9 billion from the final adopted budget, |

|

— |

EUR 1,1 billion from appropriations carried-over from 2019, |

|

— |

EUR 7,7 billion from appropriations stemming from assigned revenue. |

Total payments made in 2020 totalled EUR 173,3 billion:

|

— |

EUR 161,8 billion from the final adopted budget, |

|

— |

EUR 1,6 billion from appropriations carried-over from 2019, |

|

— |

EUR 9,9 billion from appropriations stemming from assigned revenue. |

All headings reached high levels of implementation in 2020. The 2020 implementation for all types of appropriations (budget, carry-overs from previous year and assigned revenue) was 97 % for commitments and 94 % for payments. Implementation rates excluding assigned revenue showed full implementation in 2020 (99,5 % for commitment appropriations and 98,5 % for payment appropriations).

The highest part of income was represented by Own resources, which amounted to 91,9 % of the total revenue of EUR 174,3 billion, followed 4,7 % from Contributions and refunds in connection with EU agreements and programmes, which mainly concern revenue from financial corrections (ESIF, EAGF and EAFRD).

Outstanding commitments (sometimes referred to as RAL — reste à liquider), which are committed amounts not yet paid for, stood at EUR 303,2 billion at the end of 2020. An increase from the 2019 level had been expected, given the difference between budgeted commitment and payment appropriations (EUR 9,8 billion) in the final adopted budget and taking into account the fact that an increase in outstanding commitments constitutes a normal evolution, as commitment appropriations increase every year as foreseen in the MFF. The increase in outstanding commitments compared to 2019 was EUR 5,5 billion.

The budget result (surplus) decreased from EUR 3,2 billion in 2019 to EUR 1,8 billion in 2020:

|

EUR million |

||||

|

|

2020 |

2019 |

||

|

Revenue for the financial year |

174 306 |

163 918 |

||

|

Payments against current year appropriations |

(171 721 ) |

(157 428 ) |

||

|

Payment appropriations carried over to year N+1 |

(2 086 ) |

(1 615 ) |

||

|

Cancellation of unused appropriations carried over from year N-1 |

78 |

75 |

||

|

Evolution of assigned revenue (B)-(A) |

1 398 |

(1 736 ) |

||

|

7 694 |

9 092 |

||

|

9 092 |

7 356 |

||

|

Exchange rate differences for the year |

(207) |

4 |

||

|

Budget result |

1 768 |

3 217 |

||

6. FINANCIAL INSTRUMENTS AND BUDGETARY GUARANTEES

6.1. FINANCIAL INSTRUMENTS FINANCED BY THE EU BUDGET

Under this type of budget implementation, funds are either already disbursed to the fiduciary accounts managed by the entrusted entities and stay available (as cash and cash equivalents, debt securities or investments in money market funds or pooled portfolios of assets) to cover future guarantee calls or have been invested in equity. The significance and volume of financial instruments financed by the EU budget under direct and indirect management has been increasing in recent years. The basic concept behind this approach, in contrast to the traditional method of budget implementation of giving grants and subsidies, is that for each euro spent from the budget via financial instruments, the final beneficiary receives more than EUR 1 as financial support due to the leverage effect. Financial instruments financed by the EU budget exist in the form of guarantee instruments, equity instruments and loan instruments. Under the 2021-2027 MFF the use of budgetary guarantees is expected to increase in comparison to the use of financial instruments fully financed or provisioned from the EU budget. In particular, under the InvestEU Programme EUR 26,2 billion of EU guarantee will be provided to the EIB group and other financial institutions to support various policy objectives of the Union by means of financing and investment operations.

6.2. FINANCIAL ASSETS HELD IN GUARANTEE FUNDS FOR BUDGETARY GUARANTEES

Under this type of budget implementation the EU provides guarantees to counterparts for which the funding is only partially provisioned via guarantee funds set up by the Commission and thus creating contingent liabilities for the EU budget in case the provisioning is not sufficient to cover the calls. The EU has given guarantees on loans granted outside of the EU (so-called External Lending Mandate or ELM) and on debt and equity operations covered by the EFSI guarantee to the EIB Group, as well as guarantees on operations covered by the EFSD guarantee, given to EIB Group and other financial institutions.

In order to mitigate the risk that guarantee calls by the EIB Group or other financial institutions could have on the EU budget, the EU has created dedicated guarantee funds funded by the budget. At 31 December 2020, the Commission holds financial assets in the:

|

— |

Guarantee Fund for external actions of EUR 2,8 billion, |

|

— |

EFSI Guarantee Fund of EUR 8,0 billion, and |

|

— |

EFSD Guarantee Fund of EUR 0,8 billion. |

The Guarantee Fund for external actions is provisioned by the EU budget so as to cover 9 % of the guaranteed loans outstanding at year-end for EIB external lending mandate activities to third countries. At 31 December 2020, the total asset value mentioned above covers an exposure of amounts disbursed of EUR 20,3 billion.

The EFSI Guarantee Fund started its activities in 2016. Pursuant to the amended EFSI Regulation (Regulation (EU) 2017/2396 of the European Parliament and of the Council (14)) the EFSI EU guarantee ceiling was increased to EUR 26 billion (from the initial EUR 16 billion) and the boundary for the guarantee fund decreased to 35 % (from the initial 50 %) of the total EU guarantee obligation. Therefore, the EFSI Guarantee Fund is now expected to reach a total amount of EUR 9,1 billion. The total assets that make up the EFSI Guarantee Fund at 31 December 2020 is EUR 8,0 billion and that covers an exposure of disbursed amounts of EUR 18,9 billion.

Pursuant to EFSD Regulation (Regulation (EU) 2017/1601 of the European Parliament and of the Council (15)), the EFSD Guarantee of up to EUR 1,5 billion (further increased by external contributions) is to be made available to support investments in partner countries in Africa and in the European Neighbourhood. The EU discloses the EFSD Guarantee in the notes to its consolidated annual accounts (see note 4.1.1) as a contingent liability. As at 31 December 2020, fifteen EFSD guarantee agreements were effective, for a total cover limit of EUR 1 370 million. The EFSD Guarantee Fund has been established in order to cover potential future guarantee calls. Total contributions received into the fund as at 31 December 2020 amount to EUR 0,8 billion. Given that most of the guarantee agreements were concluded with the counterparts in 2020, the programme is in the ramp up phase with EUR 438 million guaranteed operations signed by the counterparts by the end of 2020.

Following the entry into force of the 2021-2027 MFF, the net assets of the EFSI Guarantee Fund were transferred as from 1 January 2021 into the Common Provisioning Fund (CPF) (16) which hold the provisions made to cover the financial liabilities arising from budgetary guarantees and financial assistance programmes under the 2021-2027 MFF. The assets of the EFSD Guarantee Fund and the Guarantee Fund for external actions are expected to be transferred to the CPF in the course of 2021.

6.3. LOANS AND RELATED BORROWINGS FOR FINANCIAL ASSISTANCE PROGRAMMES

Financial support for Member States and third countries in the form of bilateral loans financed from the capital markets with the guarantee of the EU budget is provided by the Commission under decisions of the European Parliament and of the Council.

In 2020 the Commission, acting on behalf of the EU, operated four main programmes under which it may grant loans:

|

— |

Balance of Payments (BOP) assistance, |

|

— |

European Financial Stabilisation Mechanism (EFSM) assistance, |

|

— |

Macro-financial assistance (MFA), and |

|

— |

SURE assistance. |

The capital required to fund the EU lending is raised on the capital markets or with financial institutions. The EU borrowing and lending activities for financial assistance programmes are non-budget operations. In general, funds raised are on-lent back-to-back to the beneficiary country, i.e. with the same coupon, maturity and amount. Notwithstanding the back-to-back methodology, the debt service of the funding instruments is a legal obligation of the EU, which will ensure that all payments are made fully and in a timely manner. The Commission has put procedures in place to ensure the repayment of borrowings even in case of a loan default.

At 31 December 2020, the nominal amount of the loans granted for financial assistance were:

|

EUR billion |

||||

|

|

Total granted |

Total disbursed at year-end |

Total repaid at year-end |

Outstanding at year-end |

|

SURE |

|

|

|

|

|

Belgium |

7,8 |

2,0 |

— |

2,0 |

|

Bulgaria |

0,5 |

— |

— |

— |

|

Croatia |

1,0 |

0,5 |

— |

0,5 |

|

Cyprus |

0,5 |

0,3 |

— |

0,3 |

|

Czechia |

2,0 |

— |

— |

— |

|

Greece |

2,7 |

2,0 |

— |

2,0 |

|

Hungary |

0,5 |

0,2 |

— |

0,2 |

|

Ireland |

2,5 |

— |

— |

— |

|

Italy |

27,4 |

16,5 |

— |

16,5 |

|

Latvia |

0,2 |

0,1 |

— |

0,1 |

|

Lithuania |

0,6 |

0,3 |

— |

0,3 |

|

Malta |

0,2 |

0,1 |

— |

0,1 |

|

Poland |

11,2 |

1,0 |

— |

1,0 |

|

Portugal |

5,9 |

3,0 |

— |

3,0 |

|

Romania |

4,1 |

3,0 |

— |

3,0 |

|

Slovakia |

0,6 |

0,3 |

— |

0,3 |

|

Slovenia |

1,1 |

0,2 |

— |

0,2 |

|

Spain |

21,3 |

10,0 |

— |

10,0 |

|

|

90,3 |

39,5 |

— |

39,5 |

|

EFSM |

|

|

|

|

|

Ireland |

22,5 |

22,5 |

— |

22,5 |

|

Portugal |

26,0 |

24,3 |

— |

24,3 |

|

|

48,5 |

46,8 |

— |

46,8 |

|

MFA |

|

|

|

|

|

Ukraine |

5,0 |

4,4 |

(0,6 ) |

3,8 |

|

Tunisia |

1,4 |

0,8 |

— |

0,8 |

|

Jordan |

1,1 |

0,6 |

— |

0,6 |

|

Other |

1,5 |

0,8 |

(0,2 ) |

0,6 |

|

|

9,0 |

6,6 |

(0,8 ) |

5,8 |

|

BOP |

|

|

|

|

|

Latvia |

3,1 |

2,9 |

(2,7 ) |

0,2 |

|

|

3,1 |

2,9 |

(2,7 ) |

0,2 |

|

Total |

150,9 |

95,8 |

(3,5 ) |

92,3 |

The repayment schedule for the amounts outstanding at year-end is as follows:

|

EUR billion |

||||

|

|

SURE |

EFSM |

MFA |

TOTAL |

|

2021 |

— |

9,8 |

— |

9,8 |

|

2022 |

— |

2,7 |

— |

2,7 |

|

2023 |

— |

3,5 |

0,1 |

3,6 |

|

2024 |

— |

2,6 |

0,6 |

3,2 |

|

2025 |

8,0 |

2,4 |

— |

10,4 |

|

2026 |

— |

4,0 |

0,1 |

4,1 |

|

2027 |

— |

3,0 |

0,2 |

3,2 |

|

2028 |

— |

2,3 |

0,2 |

2,5 |

|

2029 |

— |

1,4 |

0,9 |

2,3 |

|

2030 |

10,0 |

— |

0,1 |

10,1 |

|

2031 |

— |

2,2 |

0,9 |

3,1 |

|

2032 |

— |

3,0 |

0,1 |

3,1 |

|

2033 |

— |

2,1 |

0,5 |

2,6 |

|

2034 |

|

— |

0,2 |

0,2 |

|

2035 |

8,5 |

2,0 |

1,9 |

12,4 |

|

2036 |

— |

1,0 |

— |

1,0 |

|

2038 |

— |

1,8 |

— |

1,8 |

|

2040 |

7,0 |

— |

— |

7,0 |

|

2042 |

— |

3,0 |

— |

3,0 |

|

2050 |

6,0 |

— |

— |

6,0 |

|

Total |

39,5 |

46,8 |

5,8 |

92,1 |

SURE

SURE was established in 2020 to provide financial assistance to Member States which are experiencing, or are seriously threatened with, a severe economic disturbance caused by the COVID-19 pandemic on their territory. The instrument complements the national measures taken by affected Member States.

The maximum amount of financial assistance shall not exceed EUR 100 billion for all Member States. In 2020, Member States signed loan facility agreements amounting to EUR 85,9 billion and out of this amount EUR 39,5 billion were disbursed. The maturity of loans varies between 5, 10, 15, 20 and 30 years.

EFSM

EFSM was created to provide financial assistance to all Member States experiencing or seriously threatened by a severe economic financial disturbance caused by exceptional occurrences beyond their control. The EFSM was used to provide financial assistance, conditional on the implementation of reforms, to Ireland and Portugal between 2011 and 2014. This programme expired and no additional loans can be drawn, though it remains in place for specific tasks such as the lengthening of maturities for loans to Ireland and Portugal and providing bridging loans. In February 2021, Ireland and Portugal requested the maturity lengthening for the amounts due in June 2021 (EUR 4,8 billion) and September 2021 (EUR 5 billion). In April 2021, the Commission has borrowed EUR 4,8 billion to roll-over the loans due in June 2021, which have been extended by 15 years.

No new operations nor loan repayments occurred in 2020.

MFA

The macro-financial assistance programme (MFA) is a form of financial assistance extended by the EU to partner countries outside the EU experiencing a balance of payments crisis. It takes the form of medium/long-term loans or grants, or a combination of these, and is only available to countries benefiting from a disbursing IMF programme.

In 2020, the Commission adopted a proposal for a EUR 3 billion MFA package to ten enlargement and neighbourhood partners to help them limit the economic fallout of the coronavirus pandemic. The decision was adopted by the European Parliament and the Council on 25 May 2020.

Overall, EUR 1,7 billion was disbursed in 2020 under the MFA programme.

BOP

The BOP is an assistance programme designed for countries outside the euro area that are experiencing or are threatened by difficulties regarding their balance of payments. BOP assistance takes the form of medium-term loans that are conditional on the implementation of policies designed to address underlying economic problems. Typically, balance of payments assistance from the EU is offered in cooperation with the International Monetary Fund (IMF) and other international institutions or countries.

No new operations or loan repayments occurred in 2020.

6.4. BUDGETARY CONTINGENT LIABILITIES FOR FINANCIAL ASSISTANCE PROGRAMMES

Borrowings of the EU constitute direct and unconditional obligations of the EU and are guaranteed by the EU Member States (budgetary contingent liabilities). Borrowings undertaken to fund loans to countries outside the EU are covered by the Guarantee Fund for external actions. Should a beneficiary Member State default, the debt service will be drawn from the available treasury balance of the Commission, if possible. If that is not possible at that time, the Commission would draw the necessary funds from the Member States. EU Member States are legally obliged, according to the EU own resources legislation (Article 14 of Council Regulation (EU, Euratom) 609/2014 (17)), to make available sufficient funds to meet the EU’s obligations. Thus investors are only exposed to the credit risk of the EU, not to that of the beneficiary of loans funded. ‘Back-to-back’ lending ensures that the EU budget does not assume any interest rate or foreign exchange risk.

Loans provided to Member States under the SURE instrument are underpinned by a system of voluntary guarantees from Member States amounting to 25 % of the maximum amount of financial assistance. Each Member State’s contribution to the overall amount of the guarantee corresponds to its relative share in the total gross national income (GNI) of the European Union, based on the 2020 EU budget.

For each country programme, the European Parliament, the Council and the Commission decisions determine the overall granted amount, the number of instalments to be disbursed, and the maximum (average) maturity of the loan package. Subsequently, the Commission and the Member State concerned, agree the loan/funding parameters, in particular the maturity of instalments. In addition, except for the first one, all instalments of the loan depend on compliance with policy conditions, in the context of a joint EU/IMF financial assistance, which is another factor influencing the timing of funding operations. This implies that the timing and maturities of issuances are dependent on the related EU lending activity. Funding is exclusively denominated in euro and the maturity spectrum is from 3 to 30 years.

7. FINANCIAL STATEMENTS ANALYSIS

7.1. REVENUE

The consolidated revenue of the EU incorporates amounts related to exchange transactions and non-exchange transactions, the latter being the most significant. The five-year trend of the main non-exchange revenue categories (comprising GNI resources, Traditional own resources, VAT resources, Fines and Recovery of expenses, and excluding the one-time effect of revenue relating to the UK’s withdrawal from the EU in the year 2020) is as follows:

Five-year trend of revenue from main non-exchange transactions

(in EUR million)

As budget revenue should equal (or exceed) budget expenditure, the main driver in the revenue trend shown above is the payments made each year.

In 2020, the consolidated revenue amounted to EUR 224,0 billion, a considerable increase of EUR 63,7 billion or 39,7 % from the previous year figure of EUR 160,3 billion. The main driver of this development was the financial effect of the UK’s withdrawal from the European Union (EUR 47,5 billion). If adjusted for this one-time effect, the consolidated revenue of 2020 amounted to EUR 176,5 EUR billlion, still an increase of EUR 16,2 billion or 10,1 % compared to the previous year. This adjusted increase is mainly due to the following effects:

|

— |

Revenue from GNI (gross national income), the primary element of the EU’s operating revenue, increased from EUR 108,8 billion in 2019 to EUR 125,4 billion in 2020. The increase of EUR 16,6 billion or 15,3 % was mainly due to the increase in payment appropriation needs for the year 2020, designed to reinforce key EU policies, e.g the COVID-19 vaccines strategy (implemented via the Emergency Support Instrument), and the cohesion area (by adopting the Coronavirus Response Investment Initiative Plus). |

|

— |

Other non-exchange revenue increased from EUR 2,1 billion in 2019 to EUR 7,1 billion in 2020. The increase of EUR 5,0 billion was mainly due to the contribution from Member States to the Innovation Fund which started operating in 2020 (EUR 2,1 billion), an increase of the budget surplus taken in from the previous year (EUR 3,2 billion in 2020 vs. EUR 1,8 billion in 2019) as well as a contribution from Member States of EUR 0,8 billion to top up the Emergency Support Instrument ESI. |

|

— |

Financial revenue increased from EUR 1,8 billion in 2019 to EUR 3,4 billion in 2020. The increase of EUR 1,6 billion or 88,9 % was mainly due to the increase in late payment interest, more specifically for the UK TOR cases (EUR 0,5 billion) and non-UK cases (EUR 0,5 billion), as well as revenues from bond premiums related to the SURE instrument (EUR 0,7 billion). |

|

— |

Fines revenue decreased from EUR 4,3 billion in 2019 to EUR 0,5 billion in 2020. The decrease of EUR 3,8 billion or 88,4 % was due to both the lower number and the lower amounts of fines issued in 2020. Whereas in 2020 the main fines amounted to EUR 0,26 billion in total (Orbia, Clariant and Celanese), the biggest cases in 2019 amounted to EUR 3,1 billion (Google, two Forex cases and MasterCard). |

The above changes were counterbalanced by a decrease in revenue from traditional own resources, which fell from EUR 21,2 billion in 2019 to EUR 19,6 billion in 2020 (a decrease of EUR 1,6 billion or 7,5 %) and the decrease in financial recoveries, which fell from EUR 2,6 billion in 2019 to EUR 1,4 billion in 2020 (a decrease of EUR 1,2 billion or 46,2 %).

7.2. EXPENSES

The main component of expenses recognised in the consolidated financial statements are transfer payments under the shared management mode, which includes the following funds: (i) European Agricultural Guarantee Fund (EAGF); (ii) European Agricultural Fund for Rural Development (EAFRD) and other rural development instruments; (iii) European Regional Development Fund (ERDF) & Cohesion Fund (CF); and (iv) European Social Fund (ESF). These funds made up EUR 109,7 billion or 65,9 % of the total expenses of EUR 166,6 billion incurred in 2020 (2019: EUR 103,9 billion or 66,8 %). The split of expenses can be found in the chart below:

Relative weight of the main expenses implemented by the Member States (shared management) for the financial year of 2020

Expenses incurred under direct management represent the budget implementation by the Commission, by executive agencies and by trust funds. Under indirect management the budget is implemented by EU agencies, EU bodies, third countries, international organisations and other entities.

The EU recognises certain future payment obligations as expenses even if they are not yet shown in the cash-based budgetary accounts. Significant amounts are shown under payables and accrued charges concerning agriculture and rural development, and also under pension and employee benefits liabilities relating to pension and other post-employment rights acquired by Commissioners, Members of the EU institutions and staff.

Overall, expenses increased by 7,1 % or EUR 11,1 billion from EUR 155,5 billion to EUR 166,6 billion when compared with 2019, which was mainly driven by the following effects:

|

— |

ERDF & CF expenses increased from EUR 35,2 billion in 2019 to EUR 41,1 billion in 2020. The increase of EUR 5,9 billion or 16,8 % was due to better implementation of programmes as the MFF advanced. |

|

— |

ESF expenses increased from EUR 11,2 billion in 2019 to EUR 13,7 billion in 2020. The increase of EUR 2,5 billion or 22,3 % was mainly due to increased implementation. |

|

— |

Expenses under direct management by the Commission increased from EUR 18,9 billion in 2019 to EUR 22,1 billion in 2020. The increase of EUR 3,2 billion or 16,9 % was mainly due to the spending on vaccines against COVID-19 (EUR 1,6 billion) as well as spending under the neighbourhood and pre-accession instruments (EUR 0,6 billion). |

|

— |

EAGF expenses decreased from EUR 44,0 billion in 2019 to EUR 40,5 billion in 2020. The decrease of EUR 3,5 billion or 8 % was mainly due to the decrease of EUR 2,6 billion in amounts claimed for direct payments aimed at contributing to farm incomes. |

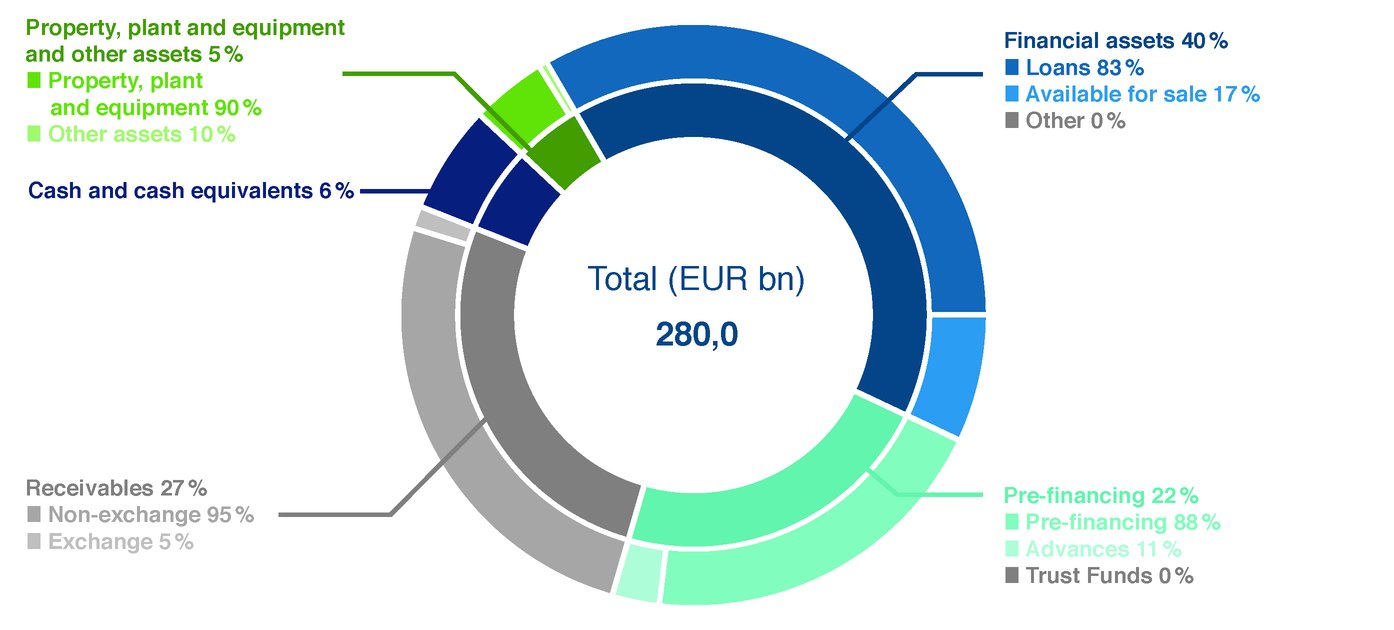

7.3. ASSETS

The most significant items on the asset side of the balance sheet relate to financial assets (other than cash and cash equivalents), which make up 40,4 % of the EU’s total assets, followed by receivables and pre-financing with percentages of 26,6 % and 22,4 % respectively:

Composition of the consolidated assets of the EU

As at 31 December 2020 the total assets were EUR 280,0 billion, reflecting an increase of EUR 101,1 billion or 56,5 % over the previous year (2019: EUR 178,9 billion), mainly due to the following key changes:

|

— |

Receivables increased from EUR 24,0 billion in 2019 to EUR 74,5 billion in 2020. The considerable increase of EUR 50,5 billion is primarily the result of the UK’s withdrawal from the European Union and the receivable generated by this (EUR 47,5 billion). |

|

— |

Loans increased from EUR 52,7 billion in 2019 to EUR 93,3 billion in 2020. The considerable increase of EUR 40,6 billion or 77,0 % mainly reflects the issuance of loans for financial assistance under the SURE instrument (EUR 39,5 billion). |

|

— |

Pre-financing increased from EUR 51,4 billion in 2019 to EUR 62,7 billion in 2020. The increase of EUR 11,3 billion or 22,0 % is mainly due to the non-recovery of the 2019 annual pre-financing in 2020 as part of the Coronavirus Response Investment Initiatives measures (EUR 6,6 billion) and the pre-financing paid for the development of vaccines to address the COVID-19 pandemic (EUR 1 billion). |

The cash balance of EUR 16,7 billion at year end is made up of the following main elements:

|

— |

An amount of EUR 9,4 billion of payments not yet implemented at year end, of which EUR 7,9 billion relates to assigned revenues. The assigned revenues include EUR 1,3 billion of cash raised on the sale of emission allowances and recovered from the EIB after being assigned by Member States to the Innovation Fund. |

|

— |

An amount of EUR 2,4 billion belonging to financial instruments concerning primarily cash equivalents managed by fiduciaries, on behalf of the Commission, for the purpose of implementing particular financial instrument programmes funded by the EU budget and cash and cash equivalents held in the guarantee funds relating to budgetary guarantees. The cash belonging to financial instruments and guarantee funds can only be used by the programmes concerned. |

|

— |

An amount of EUR 1,6 billion belonging to agencies and joint undertakings and managed by the Commission treasury on behalf of these entities. |

|

— |

Cash relating to fines of EUR 1,5 billion mainly relating to cash received in connection with fines issued by the Commission for which the case is still open and, to a lesser extent, to definitively received fines to be transferred to the budget in the following year. |

|

— |

Cash relating to other consolidated institutions, agencies and bodies of EUR 1,4 billion. |

Pre-financing

It should be noted that the level of pre-financing is significantly influenced by the MFF cycle — for example at the beginning of an MFF period large advances are expected to be paid to Member States under cohesion policy and these amounts remain available to the Member States until the closure of the programmes. An annual pre-financing is also paid out, which must be used within the year or be recovered the following year as part of the annual closure of the accounts cycle. The Commission makes every effort to ensure that the levels of pre-financing are maintained at an appropriate level. A balance has to be struck between ensuring sufficient funding for the projects and the timely recognition of expenditure.

The total pre-financing (excluding other advances to Member States and contributions to the trust funds Bêkou and Africa) on the EU balance sheet amounts to EUR 55,5 billion (2019: EUR 44,4 billion), almost all of which relates to Commission activities. Some 58 % of the Commission's pre-financing concerns shared management, which means that the implementation of the budget is delegated to Member States (the Commission retains a supervisory role).

Commission pre-financing by management mode

7.4. LIABILITIES

The most significant items on the liability side of the balance sheet consist primarily of four items: (i) pension obligations and other post-employment benefits’ liabilities; (ii) borrowings; (iii) payables to third parties; and (iv) accrued charges.

Composition of the liabilities on the consolidated balance sheet of the EU

As at 31 December 2020 the total liabilities were EUR 313,5 billion, an increase of EUR 62,0 billion or 24,7 % compared to the previous year (EUR 251,5 billion).

The key changes were related to the following effects:

|

— |

Pensions and other post-employee benefits increased from EUR 97,7 in 2019 to EUR 116,0 in 2020. The increase of EUR 18,3 billion or 18,7 % was mainly due to the actuarial loss from financial assumptions caused by a further significant decrease in the discount rate. |

|

— |

Borrowings increased from EUR 52,6 billion in 2019 to EUR 93,2 billion in 2020. The increase of EUR 40,6 billion or 77,2 % mainly reflects the SURE issuance amounting to EUR 39,5 billion at the end of 2020. |

|

— |

Payables increased from EUR 27,2 billion in 2019 to EUR 32,4 billion in 2020. The increase of EUR 5,2 billion or 19,1 % is mainly due to open cost claims for the MFF period 2014-2020 that were received at the very year-end and not treated or paid because of lack of payment appropriations. |

Total cost claims and invoices received and recognised in the Balance Sheet under the heading ‘Payables’

Net assets

The excess of liabilities over assets does not mean that the EU institutions and bodies are in financial difficulties, rather it means that certain liabilities will be funded by future annual budgets. Many expenses are recognised under accrual accounting rules in the current year although they may be actually paid in the following or later years and funded using future budgets; the related revenues will only be accounted for in future periods. The most significant amounts to be highlighted are the EAGF activities (the bulk of which is usually paid in the first quarter of the following year) and the employee benefits liability (to be paid over several decades). The considerable decrease of the amounts to be called from Member States from EUR 77,6 billion in 2019 to EUR 38,5 billion in 2020 is primarily due to the revenue related to the net amounts owed by the UK under the WA signed following its departure from the Union in 2020 — see note 2.6.1.2 of the EU consolidated annual accounts.

8. EU POLITICAL AND FINANCIAL FRAMEWORK, GOVERNANCE AND ACCOUNTABILITY

The European Union (EU) is a Union on which the Member States confer competences to attain objectives they have in common. The Union is founded on the values of respect for human dignity, freedom, democracy, equality, the rule of law and respect for human rights, including the rights of persons belonging to minorities. These values are common to the Member States in a society in which pluralism, non-discrimination, tolerance, justice, solidarity and equality between women and men prevail.

8.1. POLITICAL AND FINANCIAL FRAMEWORK

EU Treaties