EUROPEAN COMMISSION

EUROPEAN COMMISSION

Brussels, 29.6.2017

SWD(2017) 243 final

COMMISSION STAFF WORKING DOCUMENT

IMPACT ASSESSMENT

Accompanying the document

Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL

on a pan-European Personal Pension Product (PEPP)

and

COMMISSION RECOMMENDATION

on the tax treatment of personal pension products, including the pan-European Personal Pension Product

{COM(2017) 343 final}

{SWD(2017) 244 final}

Table of contents

1.INTRODUCTION AND POLICY CONTEXT

2.PROBLEM DEFINITION

2.1.Underdeveloped capital markets in the Capital Markets Union context

2.2.Insufficient features in the area of personal pension products

2.2.1.Personal pension product features

2.2.2.Insufficiently diverse supply of PPPs

2.3.Incomplete internal market for personal pension products

2.3.1.Insufficient degree of cross-border provision and portability

2.3.2.Diverging legal requirements

2.4.Other factors out of scope of this impact assessment

3.Objectives

3.1.General and specific objectives

3.2.Consistency of the objectives with other EU policies

3.3.Consistency of the objectives with fundamental rights

3.4.Subsidiarity

3.4.1.The objectives of the proposed action cannot be sufficiently achieved by the Member States

3.4.2.The objectives of the proposed action, by reason of its scale and effects, can be better achieved at EU level

4.POLICY OPTIONS AND ANALYSIS OF IMPACTS

4.1.General policy options

4.1.1.Baseline scenario

4.1.2.Pan-European personal pension product

4.1.3.Harmonisation of national regimes

4.2.Key features of a regulatory statute establishing a PEPP

4.2.1.Distribution rules

4.2.2.Investment policy

4.2.3.Rules on switching providers

4.2.4.Cross-border provision and portability

4.2.5.Decumulation

4.2.6.Summary of the recommended PEPP key features – how would a PEPP function in practice ?

4.2.7.Tax treatment based on the recommended PEPP key features

5.OVERALL IMPACTS

5.1.Overall impact of the preferred option

5.2.Macro-economic impacts

5.3.Small and medium-sized enterprises

5.4.Administrative burden

5.5.EU budget

5.6.Social impacts

5.7.Impact on third countries

5.8.Environmental impacts

6.MONITORING AND EVALUATION

Annex 1 – Procedural Steps concerning the process to prepare the impact assessment report and the related initiative

Annex 2 – Stakeholder Consultations

1. Synopsis of consultative work

2. Description of the Public consultation on personal pensions (july-October 2016)

Annex 3 – Who is affected by the initiative and how

Annex 4 – Analytical models used in preparing the impact assessment

Annex 5: Glossary and list of abbreviations used

Annex 6 - Market description of personal pensions

Annex 7 – Synthesis of policy options for the PEPP features (key and other features)

Annex 8 – Distribution: Description of Possible Add-on Provisions

Annex 9 - Cost of switching and advice

Annex 10 - List of other Features that could be part of a regulatory statute establishing a PEPP

1.INTRODUCTION AND POLICY CONTEXT

The case for an EU personal pension initiative must be assessed in the broader context of efforts to build a Capital Markets Union (CMU). The CMU is part of the third pillar of the Commission’s Investment Plan for Europe and is key to delivering the Juncker Commission's priority to boost jobs and growth. The CMU seeks to facilitate the flow of savings to investment and removing obstacles to the free flow of capital across borders. This would strengthen the European financial system by enhancing private risk-sharing, providing alternative sources of financing and increasing options for retail and institutional investors. A stronger capital market as a result of the CMU is in turn expected to provide individuals with better options to meet their retirement goals, delivering better outcomes for savers and providers alike.

In its Action Plan on Building a Capital Markets Union, the Commission observed that no effective single market for 'third pillar' personal pensions exists. A patchwork of rules at EU and national levels stands in the way of the full development of a large and competitive market for personal pensionsMarket fragmentation prevents personal pension providers from maximising economies of scale, risk diversification and innovation, thereby reducing choice and increasing cost for pension savers. In addition, existing personal pension products display in some cases insufficient product features. Finally, cross-border selling and portability of existing personal pensions are very limited.

For the purpose of this impact assessment, personal pension products (PPPs) are defined as retirement financial products which:

·are based on a contract between an individual saver and a non-state entity on a voluntary basis, with an explicit retirement objective;

·provide for capital accumulation until retirement, and where the possibilities for early withdrawal are limited,

·provide an income on retirement.

PPPs should complement state-based pensions and, where they exist, occupational pensions stemming from employment relationships. Public and occupational pensions are not covered by the scope of this initiative (see the Box below).

Box 1 – State-based, occupational and personal pensions and some examples of personal pensions

As explained in the 2014 "Pension Scheme" study for the EMPL Committee commissioned by the European Parliament, a detailed comparison of pension systems across Member States is a difficult task. All Member States have set up pension systems whereby workers are assured of a certain level of income upon their retirement, and the design of the pension system remains a national prerogative. The elements of the pension system are:

- a first pillar consisting of "state-based pensions", which are part of a public statutory social security system (mostly financed through taxes or social contributions, therefore classified as pay-as-you-go systems)

- a second pillar consisting of "occupational pensions" or "second pillar pensions" i.e. financial institutions which manage collective retirement schemes for employers, in order to provide retirement benefits to their employees (the scheme members and beneficiaries)

;

- a third pillar consisting of "personal pensions", "PPPs" as in the impact assessment or "third pillar pensions" i.e. non-compulsory private pension savings by individuals;

There is no agreed unique taxonomy of pension systems, and organisations such as the World Bank, EIOPA, or the OECD isolate more specific features beyond the broad definitions provided above. Moreover, as the terms second and third pillars have different meanings in Member States depending on the design of their national pension systems (e.g. in some Member States, "second pillar" denotes statutory funded pensions, while occupational pension schemes are considered part of the "third pillar") throughout the report we will use the terms "occupational" and "personal" pensions instead of pillars.

EIOPA advice provides an indication of the specific features of PPPs and differences with other types of investment products:

•

The specific aim of PPPs is to provide an income to PPP savers after retirement;

•

PPPs provide capital accumulation from the mid to long term until the (expected) retirement age and may also cover biometric risks;

•

During the accumulation phase premiums and contributions are deferred to a private entity, the PPP provider;

•

During the accumulation phase the possibility for early withdrawal of the accumulated capital is limited and often sanctioned;

•

National legislation could sometimes restrict the ways in which the accumulated PPP capital can be used upon retirement (e.g. (lifelong) annuitisation, programmed withdrawal, (partial) lump sums).

From an economic point of view, investments in (long duration and safe) government bonds and real estate could be considered as substitute products. However, notwithstanding the risks stemming from potential property market crisis, PPPs provide the advantages of divisibility , i.e. the possibility to invest small amounts on a regular basis and portfolio diversification.

Examples of current PPPs include:

- the Pension savings plan in Belgium ("Pensioensparen"), mainly sold by banks and insurers, which offers an investment option between savings funds (aggressive, defensive or balanced strategy) and a guaranteed interest product. Decumulation must normally start after 60 years. This plan is subject to a tax relief of 30% of the contribution, up to a limit of contribution of EUR 940 per year (in 2016).

- the Riester Rente in Germany, mainly sold by banks, brokers and insurers, including online. Investment options include more aggressive strategies (e.g. fund-linked pension insurance), or more defensive ones (e.g. bank saving plans). Decumulation must start after age 62. This plan is subject to a tax relief on contributions with a maximum amount of 2100 EUR per year.

As announced in the Action Plan on Capital Markets Union in September 2015, "an 'opt in' European Personal Pension could provide a regulatory template, based on an appropriate level of consumer protection, that pension providers could elect to use when offering products across the EU. A larger, 'third pillar' European pension market would also support the supply of funds for institutional investors and investment into the real economy". Consequently, the Commission announced that it will "assess the case for a policy framework to establish a successful European market for simple, efficient and competitive personal pensions, and determine whether EU legislation is required to underpin this market".

In its Resolution of 19 January 2016, the European Parliament expressed concern about the lack of available and attractive risk-appropriate (long-term) investments and cost-efficient and suitable savings products for consumers. Whilst reiterating the need for diversity in investor and consumer choices, the European Parliament stressed that "an environment must be fostered that stimulates financial product innovation, creating more diversity and benefits for the real economy and providing enhanced incentives for investments, and that may also contribute to the delivery of adequate, safe and sustainable pensions, such as, for example, the development of a Pan-European Pension Product (PEPP),with a simple transparent design".

In June 2016, the European Council adopted an agenda calling for "swift and determined progress to ensure easier access to finance for business and to support investment in the real economy by moving forward with the Capital Markets Union agenda".

In September 2016, in its Communication on Capital Markets Union – Accelerating Reform, in light of the strong support expressed by the European Parliament, Council and stakeholders to the CMU Action Plan, the Commission announced as a next step developing further priorities, that it will "consider proposals for a simple, efficient and competitive EU personal pension product".

Consequently, in its Communication on the Mid-Term Review of the Capital Markets Union Action Plan, the Commission announced "a legislative proposal on a Pan-European Personal Pension Product (PEPP) by end June 2017. This will lay the foundations for a successful market in affordable and voluntary retirement-related investments that can be managed on a pan-European scale. It will meet the needs of people wishing to provision for retirement, address the demographical challenge, complement the existing pension products and schemes, and provide a powerful new source of private capital for long-term investment".

Accordingly, this impact assessment aims to support the process of taking a well-informed decision on the legislative initiative on a PEPP.

In this regard, a PEPP framework would entail a complementary voluntary regime beside national regimes, allowing providers to create personal pension products on a pan-European scale.

A PEPP framework would contribute to progress towards a single market for personal pensions, by harmonising a set of core product features and facilitating cross-border activity.

The PEPP framework would bring value added as compared to existing PPPs, building on existing best practices complemented by specific features conferring it a pan-european dimension. First, the PEPP could be offered by a wider range of providers then existing PPPs, including not only insurance companies (currently the major players in personal pensions) but also investment firms and asset managers, as well as specialised pension funds (currently more focussed on occupational pensions). It would be authorised by the European Insurance and Occupational Pensions Authority (EIOPA), on the basis of a single set of rules and once authorised could be marketed across the European Union.

PEPP providers would follow specific rules on distribution ensuring adequate information and checks.

The PEPP would be a simple product, with a limited set of investment options. It would include the right to switch provider and the possibility to continue contributing to the same product when exercising mobility across the European Union. The PEPP framework would provide a safe default investment option. It would be innovative – distributed on an electronic basis – and transparent, with appropriate disclosure of all costs and fees. Prospective PEPP savers would receive appropriate information via a PEPP Key Information Document before the conclusion of the contract, as well as information on their pension benefits during the term of the contract.

Subject to the effective development of PEPPs, the PEPP framework could mobilise over time some additional households' savings e.g. from deposits towards investments on capital markets. Even if the development of a PEPP would be progressive and additional investments on capital markets limited, as a long-term savings product, matched by long-term investments, the PEPP framework could contribute to the objectives of CMU.

Against this background, the Commission has organised a public consultation (including a public hearing) on EU personal pensions and received 585 contributions from a broad range of stakeholders (see a synopsis of the consultative work and a detailed analysis of the public consultation, in Annex 2). The responses showed a strong interest from private individuals in simple, transparent and cost-effective PPPs. The public consultation also requested feedback from professionals on the feasibility of an EU personal pension framework including a PEPP. As national tax incentives are an important driver for the take-up of personal pension products, the Commission has commissioned a study on a European Personal Pension Framework (the "EPPF Study" hereafter) in order to map the national tax and other legal requirements applicable to personal pensions on the basis of a set of personal pension products, evaluate the market potential for personal pensions across the EU and assess the feasibility for stakeholders to implement an EU personal pension framework.

This impact assessment builds inter alia on substantial technical advice from the European Insurance and Occupational Pensions Authority (EIOPA) on the development of an EU single market for personal pension products ("EIOPA technical advice" hereafter). This advice itself builds on an earlier preliminary report of EIOPA, entitled "Towards a single market for personal pensions". The selected policy options in this impact assessment are in line with the EIOPA technical advice on the key issues, particularly the choice of a PEPP against other general policy options (section 4.1), and the determination of key features (section 4.2).

This impact assessment also builds on the work carried out by the OECD in the area of private pensions. First, the work on tax treatment of personal pensions products, namely the OECD study on "Stocktaking of the Tax Treatment of Funded Private Pension Plans in OECD and EU countries"and the Commission-OECD project on Taxation, Financial Incentives and Retirement Savings. Second, the impact assessment takes guidance from the OECD Study "Core Principles of Private Pension Regulation" on the design and operation of private pension systems. Finally, the impact assessment also takes into consideration the Oxera Study on the position of savers in private pension products across fourteen Member States.

Based on these various inputs, the next section presents the main problems and shortcomings of the personal pensions market.

2.PROBLEM DEFINITION

The main problems identified in this impact assessment concern the following issues: (1) the fact that the further development of the Capital Markets Union (and long-term investments) is, together with other elements out of scope of this impact assessment, affected by the low level of personal savings in retirement products by households (2) insufficient features of personal pension products; (3) cross-border problems, including the lack of a genuine internal market for personal pensions products within the EU.

2.1.Underdeveloped capital markets in the Capital Markets Union context

The personal pension market in the EU is currently under-developed, highly fragmented and with low cross-border sales (see below and in the following sections). Together with many other elements outside the scope of this impact assessment, this affects the completion of the Capital Market Union which aim is, inter alia, to increase the depth and liquidity of capital markets and their efficiency, ultimately benefitting investment and growth in the EU. More details about the economic benefits of developed capital markets can be found at the end of this section.

The EU actions in order to complete the CMU cover, many other areas beyond personal pensions. The CMU Action Plan sets a broad policy agenda which aims to put in place a structural reform to strengthen European capital markets and reduce the dependency of the European economy on bank lending.

Within all the projects covered under the CMU Action Plan, personal pensions (and more broadly pension funds) play a role as major institutional investors on capital markets. In this context, the EU is lagging behind compared to other advanced economies: as shown in the table below the total investment assets by pension funds (as per OECD definition) in the EU is at around 30% of GDP compared to 79% in the US for example.

Table 1: Total investment assets as per OECD definition of pension funds - Billions USD

Source: OECD, IMF, own calculations

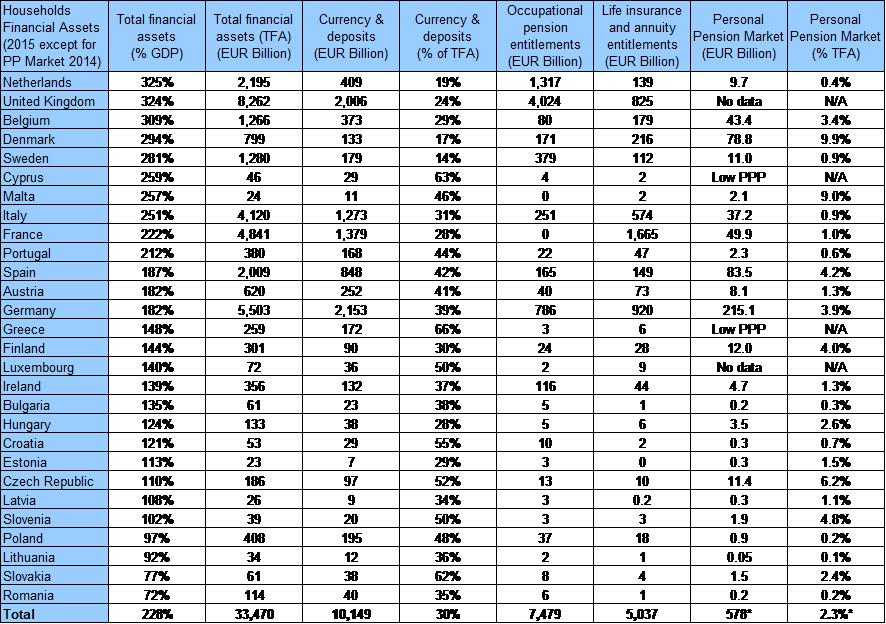

The currently sub-optimal level of savings in personal pensions and the relatively high level of savings in the form of deposits reduce the potential investment flows by households into capital markets. As a matter of fact, households are the main providers of net funding in the economy with, as of December 2015, almost EUR 34 trillion of total financial assets and a saving rate of more than 10% of gross household disposable income in the EU, equivalent to EUR 1 trillion in 2015. The table below shows the amounts for the main financial asset categories held by households at December 2015 in all Member States, ranked from the State with the highest level of total financial assets over GDP to the lowest level (data taken from Eurostat). The last column instead gives an estimation of personal pension assets under management in the countries where data was available.

Table 2: Overview of Households Financial Assets and Personal Pension Market by Member State, EU 28

Source: Eurostat and EPPF Study and own calculations. *The totals for the last two columns are for 24 Member States

In terms of financial instruments, cash and deposits represent around 30% of the total with an amount of more than EUR10 trillion which is equivalent to almost 70% of the EU GDP. The amount held in deposits is quite lower (below 20% of total assets) than the EU average for three Member States (Netherlands, Denmark and Sweden) as the life insurance and occupational pensions markets are quite developed. However, for twelve Member States the currency and deposits account for more than 40% of total financial assets; for seven of them the level is higher or equal than 50% showing a low level of diversification of households' financial portfolio.

The higher propensity to prefer deposits over other financial products is more pronounced for households with lower financial assets. Table 2 shows that the total assets under management (AuM) of PPPs for which data was available are estimated at 578 billion EUR for 2014. This represented less than 3% of European households’ financial assets. This can be considered as low, especially as compared to cash and deposits.

According to the EIOPA technical advice, only 67 million people, out of a total EU population of 243 million between 25-59 years old (27% of the total) are currently voluntarily subscribed to financial products with a long-term pension objective. These areconcentrated primarily in a few markets (Netherlands, United Kingdom, Czech Republic, Belgium and Spain).

A recent survey carried out by the ECB in the euro-area Member States points out that the smallest financial asset portfolios consist almost exclusively of deposits (for example, for the first four deciles of total financial assets, deposits account for more than 80% with the remainder consisting mainly of life insurance policies/voluntary pensions). Savings in the form of other financial instruments are concentrated among wealthier households: the wealthier the household, the more diversified its asset portfolio, and the more educated the household, the higher the share of other assets (e.g. for the top 10% of portfolios, voluntary pensions/life insurance products account for 25%, and risky assets for 26%). Moreover, the current low level of investments and participation by households in pension products has a negative impact on the size and the diversity of participants in capital markets.

The long-term nature of pension products liabilities incentivises providers to invest more in illiquid and long-term assets that yield higher returns. To the extent they invest in equity and corporate bond markets, they provide a long-term supply of funds to capital markets, and thus may contribute to their development.

Taking the pensions funds' assets as proxy, empirical evidence shows that their size has an impact on the development of capital markets especially on the stock market capitalization. Pension funds are indeed an important source of funding, and affect the amount of market financing available and the efficiency of financial intermediation. They provide an alternative savings vehicle for households and add to competition on the loan and securities markets. In so doing, they spread the gains of investments in capital markets to the broader population, facilitate asset diversification, and make the access to capital markets cheaper. Countries with an important pension funds sector tend to have larger capital markets. For example, after World War II many European countries rebuilt their pension system by establishing a pay-as-you-go system, whereas pension funds became an important provider of funds on the US capital market. This led to significant differences in the amount of savings made available for investment in financial securities. A regression analysis performed by the Commission services found that by increasing pension assets in the euro area and the EU by respectively 73% and 60% of GDP (i.e. to the levels observed in the US around 90% of GDP), this would generate an additional stock market capitalisation of 31% and 26% in the euro area and EU respectively.

Moreover, as described in some research papers "even in the case that pension savings crowd out other household savings such that the total savings in the economy do not increase, the accumulation of pension fund assets is expected to potentially promote depth and liquidity in the capital markets because of the different investment behaviour between households and pension funds. Other potential impacts from the growth of pension funds include an inducement toward financial innovation, improvement in financial regulations and corporate governance, modernization in the infrastructure of securities markets, and an overall improvement in financial market efficiency and transparency".

In conclusion, the insufficient provision of simple, cost-effective, transparent and trustworthy personal pension products affects the development of non-bank funding alternatives for companies and longer-term investment, as well as additional risk diversification opportunities for households. The economic benefits of capital markets are multiple and can be summarized as follows:

·Deep, liquid and efficient capital markets bring advantages to borrowers and investors. They have three main advantages for companies seeking finance: (i) improve their access to funds; (ii) reduce their capital costs by creating competition among investors; and (iii) reduce the risk of disruption in financing by diversifying their funding sources. On the investors' side, by increasing the investment opportunities, efficient capital markets offer investors a broader set of financial products to (i) meet their investment objectives, (ii) diversify and manage their risks, and (iii) optimise their risk-return profile, while respecting their investment constraints – whether in terms of risk, duration, or other assets' characteristics. Overall, capital markets (especially equity markets) facilitate entrepreneurial and other risk-taking activities, which have a positive effect on economic growth.

·Large and well-integrated capital markets can contribute to jobs and growth through a number of channels. They can contribute to allocative efficiency by opening up investment and diversification opportunities for investors across Europe, improving access to risk capital for borrowers, and allowing greater competition (unleashing corresponding benefits such as productivity gains, lower costs, greater choice, financial innovation, etc.). Portfolio diversification possibilities should also be enhanced because the larger financial markets are and the better they are integrated across borders, the more opportunities they allow to share risks among actors and economies.

·Moreover the optimal financial structure shifts towards capital markets along with higher levels of economic development. Banks are particularly well-placed to serve economies at an early stage of development. They also have an uncontested role in certain market segments, for example to provide funding to firms that are too small to tap market sources. Capital markets take longer to develop because they require extensive technical and legal infrastructures (e.g. clearing, settlement, information provision). Services provided by financial markets become comparatively more important for higher-income Member States because, when economic and institutional systems mature, demand for a broader set of risk management and capital raising tools increases beyond what banks can typically supply.

2.2.Insufficient features in the area of personal pension products

Currently, personal pension products are regulated at national level as further described in Section 2.3. This results in a diverse set of product features and a lack of portability. Many respondents to the public consultation view the supply of personal pension products currently available and sold in the EU as insufficient. These views are supported by the 2015 European Commission scoreboard on retail investor markets, which shows that personal pension products are indeed among the three products with the lowest satisfaction rating from retail investors. This low ranking reflects the potential for improvement of performance of personal pensions in terms of comparability and choice of product features and choice of providers.

In addition, there is insufficient diversity in the provision of PPPs. This further affects the supply of certain product features.

2.2.1.Personal pension product features

Some of the concerns on the quality of existing personal pension products, as highlighted in the public consultation and the EIOPA technical advice, are presented in more detail below. These concerns limit the attractiveness of some existing PPPs for savers.

(a)Disclosure of information

In its technical advice EIOPA considers that information asymmetries between providers and customers reduce trust in personal pension products. As savers are less well informed than PPP providers, they have difficulty judging or comparing the performance and quality of the pension product and providers. This information asymmetry has the potential to result in sub-optimal decision making by savers on PPPs and could lead to less cost-effective and unintended outcomes for PPP holders.

Consumer organisations indicated in the public consultation that in some cases information on fees and costs is opaque and disclosed in a non-aggregated manner, especially in the case of multi-layer products. For consumer organisations, the information provided on returns is often incomplete and does not indicate the net return (taking into account all taxes and fees) that the pension saver will effectively receive. Some consumer organisations indicated that PPP customers of life insurers are not sufficiently informed about the total amount of the benefits they are likely to receive on retirement, even if an annual information sheet is provided by the insurer. The information provided is often not comprehensive and does not include the expected future benefits or how an annuity product would evolve over time.

(b)Distribution of PPPs

One way of overcoming information asymmetries of PPPs for savers is to make use of independent advisors or compare products features through online distribution. However, EIOPA concludes that the current distribution model of PPPs takes place through existing distribution channels, either directly by the provider or through non-independent intermediaries.

Figure 1 below shows limited use, in the Member States surveyed, of independent advisors (except for Czech Republic and Netherlands) or online sales (captured under "other", mainly in Hungary). Absence of advice or inability to compare products online can increase risks of miss-selling.

Figure 1. Distribution of PPPs per Member State, for ten Member States

Source: EIOPA technical advice

(c)Diverse levels of net performance after costs and charges

The Better Finance Study on Pensions Savings – The Real Return shows very diverse levels of net performance after costs and charges for PPPs in a series of Member States. The low returns of PPPs in some Member States undermine attractiveness of saving for retirement through PPPs. As shown in Figure 2 below, Spanish, some French, Italian and Bulgarian PPPs provided on average negative real returns in the period 2000-2015. In most Member States, the average net return of some PPPs is just above the inflation rate. The study identified net returns clearly above inflation only in some Member States (the Polish and Danish pension products providing yearly net real returns above 4%).

Figure 2. Net real performance of pension funds (occupational and personal), in different Member States, from 2000 onwards

Evidence suggests that charges and costs of PPPs are one of the causes of negative or low real net returns. As an example, COVIP, the Italian supervisor of pension funds publishes every year an aggregate cost index of personal pensions sold in Italy. For 2016, the average yearly costs (calculated over a 10 year period and assuming investments of annual EUR 2500 and annual return of 4%) are quite high: from 1.1% to 2.7% depending on the type of investment strategy. As shown in Figure 3 below, the charges can take away a considerable amount of a pension pot. Furthermore, as outlined in section 2.1.2 a) above, fees are often relatively opaque, making it more difficult for savers to compare costs and charges of distinct products and providers.

Figure 3 - Reduction in yield through charges in some Member States – Oxera Report 2013

(d)Locked-in nature of some PPPs

For certain PPPs, which are by nature very long-term products, the insufficient flexibility for savers to switch between products and providers is a major disincentive to take-up. Currently, the majority of existing products do not allow for switching provider, or else switching is costly and subject to penalising exit fees (See an analysis of the costs of switching and advice in Annex 9). The Irish Competition and Consumer Protection Commission indicated that for unit-linked funds in Ireland, the costs of early withdrawals (which may be triggered by the wish to switch providers) typically amount to 1% up to 5% of assets under management. Complexity often arises with regard to insurance-based products, whereby individual schemes may impose additional restrictions on switching, such as termination fees. The risk of being locked in a product or with a provider for a long time, especially until retirement age, regardless of the performance of the product, is a reason for consumers to be cautious with regard to acquiring some PPPs. A thematic review of the treatment of long-standing customers in a similarly long-term business like the life insurance sector by the UK Financial Conduct Authority found that the impact these charges can have on returns can be significant and may present barriers to shopping around.

(e)Decumulation options

The decumulation or payout phase of a PPP is the period during which assets (accrued in the accumulation phase) are paid out to the saver. Decumulation options of PPPs, i.e. the way that benefits are paid at retirement, display significant variations across Member States. Based on the EIOPA database of pensions plans and products in the EEA, the possible forms of retirement payments are annuities (a stream of payments for as long as the retiree lives), lump sums (a single payment), and programmed withdrawals (a series of fixed or variable payments whereby the annuitant draws down a part of the accumulated capital).

The EIOPA advice and the EPPF Study show that currently available PPPs sometimes have restrictions as regard the choice of out-payments. Such restrictions are either imposed by providers or due to national legislation. The use of a certain form of out-payments might also be linked to tax incentives. As shown in Figure 4 below, only the annuity-based form of retirement payment is possible for a majority of PPPs with 44% of PPPs covered by the EPPF Study only allowing for annuities. According to the EPPF Study (Interim Report), annuity is legally mandatory for nine PPP schemes in six Member States (Denmark, Finland, France, Germany, the Netherlands and Sweden). However, they do not lead to tax incentives, save from the Dutch PPPs. In Finland, the Netherlands and Sweden there are no PPP schemes allowing lump sums as a decumulation option. According to the EPPF Study, twenty-five Member States in principle allow lump sums as a decumulation option (but sometimes only if combined with annuities).

Figure 4 – Decumulation options for 49 existing PPPs

Source: EPPF Study, Interim Report, p. 39

Contributions made by consumer associations to the public consultation also touch upon this problem suggesting that savers desire flexibility as regards decumulation options at the age of retirement. Indeed, major consumer associations responding considered that decumulation options should be flexible and should be based on the choice of the individual.

(f)Protection of the savings invested in the PPPs

As personal pension products have a long-term nature, some savers are concerned with the eventual product of their savings on retirement. Contributions for retirement provisions constitute often one of the most important investments during a person's life-time. That is why some consumer associations underlined the need for enhanced protection of savings in PPPs. On the other hand, consumer associations also indicate that adequate protection should not hamper investment strategies aiming at better returns.

The EIOPA technical advice shows that only 20 % of PPPs currently on the market provide some type of a guarantee. The vast majority of PPPs are pure defined contribution (DC) products, representing a market share of 80 percent. Defined benefit (DB) pension schemes represent only a very small portion of the total PPPs.

On the other hand, consumer associations also indicated that guarantees are often a costly product feature adding to the complexity of PPPs. Furthermore, some consumer organisations consider that guarantees are sometimes misleading, especially if only the nominal capital is guaranteed, without taking into account inflation; in their view, a guarantee on capital is only useful if the real value of the capital saved (taking into account inflation) is protected. Some other consumer organisations considered that a guarantee might be beneficial for consumers close to retirement, if at least they compensate for inflation. During the public consultation, providers such as asset managers and investment funds indicated that other risk mitigation techniques, such as life-cycling could have a similar effect to providing a guarantee on capital.

2.2.2.Insufficiently diverse supply of PPPs

At present, the supply of PPPs is mostly dominated by insurers and limited to a set of national providers. The EIOPA technical advice demonstrates that PPPs are currently overwhelmingly sold by insurers (more than 80% of assets under management of PPPs, as shown in Figure 5 below). Occupational pension funds and asset managers represent respectively only 9% and 4% of assets under management. The limited number of providers supplying PPPs reduces choice for savers, as more providers could provide products with a bigger range of product features. For example, insurers typically provide guarantees for in-payments and annuities for out-payments. Alternative providers could favour distinct risk mitigating strategies for in-payments and distinct options for out-payments. EIOPA considers that as a consequence, savers cannot reap the benefits of wider choice of provider, better quality and lower prices due to the insufficient EU-wide competition between market players. Figure 5 bis below shows the limited take-up of personal pensions in certain Member States.

Figure 5. PPP Assets under Management by type of provider

Source: EIOPA technical advice

Figure 5 bis- Assets under Management in Personal Pensions by Member State

Source: EPPF Study

Source: EPPF Study

In addition, the public consultation indicates limited satisfaction of savers with the supply of PPPs. On the other hand, it is instructive that most of the professional stakeholders responding to the public consultation do not actually supply PPPs, and almost half of those which do so are active in only one Member State. The low supply of personal pension products seems to be significantly due to certain national regulatory requirements that are in place for justified reasons (e.g. prudential requirements and consumer protection), but may however have the effect of limiting competition and market access. In addition, stakeholders repeatedly pointed in their contributions to the public consultation to the hurdles represented by tax requirements, which are presented later in this impact assessment.

2.3.Incomplete internal market for personal pension products

Two main obstacles result in an incomplete internal market for personal pension products: an insufficient degree of portability across borders and diverging legal requirements.

2.3.1.Insufficient degree of cross-border provision and portability

Existing personal pension products are not adapted to the needs of mobile workers, which may vary during the lifetime of a PPP, notably when exercising mobility in the EU. Even when portability of PPPs is not legally or contractually prohibited, cross-border portability is de facto difficult in practice, harming intra-EU mobile workers. In particular, the recognition and transfer of pension contributions across providers and across Member States is hindered. As a consequence, mobile workers, in practice, need to sign up for a new personal pension product when moving across borders. On retirement, mobile workers could end up with multiple pension products from distinct providers, subject to distinct national requirements. Therefore, mobile workers are incentivised to save for retirement through other means, limiting the take-up of personal pension products. The insufficient provision of suitable products for mobile workers may thus negatively affect labour mobility in the EU.

According to a 2010 Eurobarometer survey, 10% of people polled in the EU replied that they had lived and worked in another Member State at some point in the past, while 17% intended to take advantage of the right to free movement in the future. The recent trend of intra-EU mobility is positive (e.g. 2004:1.7%, 2008: 2.4%, 2012: 2.8%) with the pace picking up again after the economic recession. Indeed, according to the 2016 Annual Report on intra-EU Labour Mobility, almost 11.3 million EU citizens of working age (20-64 years) were residing in a Member State other than their country of citizenship, making up 3.7% of the total working-age population across the EU-28. In addition, there were in 2015, 1.4 million retired EU citizens living in a Member State other than their country of citizenship.

Moreover, according to a 2016 Eurobarometer survey, 71% of the respondents agree that free movement of people within the EU brings overall benefits to the economy.

As an example of mobile workers, researchers often spend a part of their career in different EU Member States working on distinct projects, often with multiple employers. The MORE 2 study shows that, out of a population of 1.2 million researchers, on average 15% percent are currently mobile. 30% of researchers have been mobile during the last ten years. Due to insufficient portability they have difficulties to save for retirement by means of personal pension products. As a targeted response to such needs, the Resaver pension fund enables employees to remain with the same pension arrangement when moving between Member States and when changing jobs.

According to the feedback from professional stakeholders taking part in the public consultation, there are a number of hurdles that prevent providers from supplying PPPs on a cross-border basis. These include an unfamiliar customer base combined with language and cultural differences, distinct expectations of the local policyholders, the risks and prevalence of fraud; the supervisory environment and national prudential rules, the current generosity of public pension systems in some Member States, local dominant distribution channels and branding difficulties. The differences in national tax treatment are the most important. These barriers are presented in more detail below.

As part of its technical advice, EIOPA conducted a quantitative study to identify cross-border requirements for third pillar products. EIOPA collected data from thirteen Member States (Belgium, Bulgaria, Czech Republic, Estonia, France, Croatia, Italy, Lithuania, Luxemburg, Hungary, Malta, Portugal, Slovakia) with regards to cross-border contracts. Other Member States could not provide detailed information with respect to cross-border services of PPPs.

This study shows that only 4% of the assets under management of these thirteen Member States result from cross-border business. However, there are large differences between Member States. In the vast majority of Member States (Belgium, Czech Republic, Estonia, France, Croatia, Luxemburg, Hungary, Slovakia) cross-border business represents less than 2% of assets under management. According to the same study, in Italy, Portugal and Lithuania cross-border business represents respectively 10%, 20% and 30% of all assets under management. In two Member States, Bulgaria and Malta, more than 75% of the assets under management result from products provided by cross-border entities. In Bulgaria, PPPs are provided by companies from other Member States or from outside the EU establishing a branch, whereas in Malta all PPPs are contracted with providers from other Member States or from outside the EU.

2.3.2.Diverging legal requirements

Today, due to diverging legal requirements at national level, there is no genuine single market for existing personal pension products – and design, distribution, contract law, as well as consumer protections are widely different. And for instance, EU legislation on distribution requirements for investment products such as IDD, MiFID II and the PRIIPs Regulation do not apply to most personal pension products. Indeed, products which under national law are "recognised as having the primary purpose of providing the investor with an income in retirement, and which entitle the investor to certain benefits" are exempted.

Other national legal requirements are also diverse. Table 3 below shows the diversity of tax regimes applied in various Member States, based on 49 existing personal pension products across the EU. In some cases, the tax regimes vary for existing personal pension products within the same Member State (e.g. Poland).

Most Member States apply either the so-called EET system (Exempt contributions, Exempt investment income and capital gains of the pension institution, Taxed benefits) or the ETT principle (Exempt contributions, Taxed investment income and capital gains of the pension institution, Taxed benefits). Other systems (such as TET, TEE, EEE) are less common, but can also be found across the EU. Even within the EET system, the requirements for tax deductibility of contributions vary widely from one Member State to another and may be often limited to a certain level of income replacement or a fixed amount. Therefore, in order to offer qualifying PPPs in different Member States, PPP suppliers manufacture and distribute (through subsidiaries or branches where appropriate) products which are tailored to the tax law of each Member State and thus do not achieve economies of scale, due to a lack of standardisation.

Table 3: overview of direct income tax regimes applicable to personal pension products

Source: EPPF Study Interim Report

Within the 49 products identified in the Study there are no two products with 100% identical requirements from a tax perspective, in some cases even within a Member State. As a consequence, a product cannot qualify for tax incentives in more than one Member State.

The diverging legal requirements across Member States result in the following effects, leading to the absence of a single market for personal pensions:

- Difficulty for providers to operate across borders as they need to adapt their PPPs to cater for national requirements. Based on the 49 PPPs surveyed in the EPPF Study, product legislation varies significantly across Member States, for instance on authorising savers to switch providers. The product legislation does not necessarily have a tax dimension. More specifically, failing compliance with every single tax requirement a PPP cannot qualify for tax relief. The differences between national tax requirements indeed require designing distinct products to access national markets. As an example, in order to benefit from tax relief, PPPs in three Member States (Austria, the Netherlands, Slovenia) must have annuities for out-payments in the decumulation phase, those in two Member States (Cyprus, Malta) require a lump sum, while thirteen Member States allow for both annuities and lump sums to benefit from tax incentives. In other Member States the out-payments are taxed, whatever the decumulation option (annuities, lump sum or a combination of both). An operator willing to operate across borders in those jurisdictions would be required to offer a product with lump sum in certain Member States and a product with annuities in other Member States. Such requirements result in the need to design a national product and hinder providers from entering a market of another Member State, even where the potential for PPPs is not fully tapped. As already mentioned, EIOPA estimated in 2015 that only 4% of personal pension asset volumes are sold across borders in the EEA.

- The transfer of accumulated capital from a TEE/TTE Member State to an EET/ETT Member State can lead to double taxation. The double taxation is, for example, the result of the denial of tax relief for contributions made in Member State A and the taxation of the pension in Member State B. On the other hand, a transfer from an EET/ETT system to a TEE/TTE system may lead to non-taxation. Furthermore, it cannot be ruled out that the tax administration of a Member State would retrospectively deny tax credit granted in case of the transfer of accumulated savings outside its jurisdiction to a Member State that prescribes different condition for tax relief (e.g. enables to take programmed withdrawal, or sets out different minimum retirement age). Since direct taxation is within the competence of individual Member States, the variety in taxation regimes hinders the application of the principle of non-discrimination under EU law.

In some Member States, specific legal requirements result in a limited supply of certain products. For example, the option to exit with a lump sum is not available in six Member States, as this would be dis-incentivised in a prohibitive way by national tax requirements. In other cases, legal or tax restrictions on investment options can have adverse consequences on returns. For example, some national rules limit tax benefits to products that offer a guarantee on return. In the current economic context of low interest rates this requirement could result in high costs for providers and correspondently low returns for savers, making the product un-attractive.

2.4.Other factors out of scope of this impact assessment

Besides the main drivers, problems, and consequences that are assessed above, the problem tree (see below) also shows a number of other factors that are outside of the assessment scope. These other factors are described below.

Demographic changes in the following years will lead to the ageing of the population and an increased number of pensioners. Such demographic tendencies increase the costs of existing pension systems and put pressure on public finances, creating incentives for measures by public authorities.

Such measures in public and occupational pension schemes can affect pension adequacy and hence affect the need for additional personal savings for retirement. The pressure on state-run pensions systems is well documented,and was described in the 2012 White Paper on adequate, safe and sustainable pensions. While state-based pensions provide the majority of retirement income in the EU, demographic and fiscal pressures would limit their capacity to sustain adequate retirement incomes in the long run. Accordingly, supplementary retirement sources such as personal pensions are likely to increase and can bring a positive contribution to solving the pension challenge. The Annual Growth Survey (AGS) 2017 noted that "broad coverage of supplementary (occupational and personal) pensions can play a key role in retirement income provision, in particular where the adequacy of public pensions might be a challenge, and should be promoted by appropriate means, depending on the national context".

A well-functioning internal market for personal pension that provides better options for citizens to save for retirement could, as a potential long term side impact, contribute to addressing the existing pension gap (See Glossary in Annex 5) as well as deteriorating replacement ratios. The main side effect achieved over time could be that retirees across Europe have better options to save for retirement to help address potential shortages in retirement income.

At the same time, the coverage of supplementary pensions, and thus their contribution to pension adequacy, remains very uneven across the EU. Personal pensions have relatively wide take-up in only a few Member States (over 60% coverage in the Czech Republic, over 30% in Sweden and Germany) while in most Member States take-up is moderate and fragmented, and in some, nearly non-existent.

In addition, the ongoing dynamics of the labour market result in a more mobile workforce and an increase of self-employed workers with often inadequate pension savings. Another factor leading to low demand for personal pensions is the limited disposable income available for saving for retirement in some Member States, especially amongst young generations.

These issues are not covered by this impact assessment.

Prob

3.Objectives

3.1.General and specific objectives

For the EU economy in general, an EU personal pension framework could contribute to address some of the personal pension market shortcomings and to increasing savings and investment. The PEPP framework could indeed help to create large pools of pension savings, thus injecting more savings into capital markets and channel additional financing to productive long-term investments which would contribute among other projects to complete the CMU.

Regarding the product features on the personal pension market, the PEPP framework could bring more simplicity, safety, transparency, cross-border enhancements and overall minimum quality standards to the personal pension market, addressing the needs of savers and providers. This could improve the attractiveness of personal pension products, towards creating in the long run a single market for personal pensions.

These general objectives can be broken down in the following, more specific objectives:

|

Problems

|

Specific objectives

|

|

Underdeveloped capital markets in the CMU context

|

Increase investment in the EU and contribute to completing the CMU

|

|

Insufficient features in the area of PPPs

|

Enhance product features on the personal pension market

|

|

Cross-border problems: insufficient cross-border provision of personal pensions and their portability

|

Enhance the cross-border provision and portability of personal pension products

|

3.2.Consistency of the objectives with other EU policies

The initiative would reduce the obstacles to cross-border provision of personal pension products, overcoming existing hurdles in national tax and legal requirements applicable to such products.

The initiative, by enhancing the cross-border portability of personal pension products, would contribute to further facilitating the free movement of workers, one of the key pillars of the internal market. Thus the initiative is in line with the objective of promoting labour mobility, highlighted in President Juncker's Political Guidelines for the European Commission.

Developing a PEPP framework is also in line with the Commission's 2012 White Paper on Pensions, and in particular with the intention of developing complementary private retirement schemes by encouraging Member States to optimise tax and other incentives for such schemes. The White Paper focusses on enhancing the safety of supplementary pension schemes, as well as on making supplementary pensions compatible with mobility; it supports legislation protecting the pension rights of mobile workers and promotes the establishment of pension tracking services across the EU. In accordance with another commitment in the White Paper, the Commission is supporting, through Horizon 2020, a consortium of employers in creating a single European pension arrangement (RESAVER) that will offer a defined contribution plan, tailor-made for research organisations and their employees.

3.3.Consistency of the objectives with fundamental rights

The EU is committed to high standards of protection of fundamental rights and is signatory to a broad set of conventions on human rights. In this context, the proposed objectives as discussed above are not likely to have a direct impact on these rights, as listed in the main United Nations conventions on human rights, the Charter of Fundamental Rights of the European Union which is an integral part of the EU Treaties, and the European Convention on Human Rights ('ECHR').

3.4.Subsidiarity

Regarding subsidiarity, under Article 4 TFEU, EU action for completing the internal market has to be appraised in the light of the subsidiarity principle set out in Article 5(3) TEU. Hence it must be assessed whether the objectives of the proposal could not be achieved by the Member States in the framework of their national legal systems and, by reason of its scale and effects, is better achieved at EU level.

3.4.1.The objectives of the proposed action cannot be sufficiently achieved by the Member States

The uncoordinated efforts of Member States, either at central level or at regional and local level, cannot remedy the legal fragmentation in product regulation, which results in extra compliance cost for providers and discourages them from going cross-border. For instance, EU legislation on distribution requirements for financial products such as IDD, MiFID II and the PRIIPs Regulation do not apply to most personal pension products, leaving national legislation to apply.

With PPP markets left exclusively to national regulation, asymmetric information issues can be observed between providers and savers, particularly in a cross-border context. The insufficiently complete information to savers from providers at national level reduces trust in PPP providers and often results in fewer transactions, lower levels of engagement with pension provision, alongside poor decision-making by savers.

The portability of PPPs is a concern for individuals moving cross-border while trying to maintain the same product and provider. At present, upon changing residence to another Member State, individuals in practice have no choice but to search for a new product developed by a new provider in the new Member State, on the basis of substantially different rules, instead of continuing to save in their former Member State. National tax incentives encourage individuals to save for retirement and are key to promoting the take-up of personal pensions; losing such tax benefits on moving to another Member State is currently a barrier to the cross-border portability of personal pension products. Member States alone cannot remedy portability issues.

3.4.2.The objectives of the proposed action, by reason of its scale and effects, can be better achieved at EU level

Action at EU level can substantially add value to remedy the consequences, particularly in terms of costs, of market fragmentation. If no EU action is taken, asset pools are likely to remain small and limited to national borders, without economies of scale, and competition would remain restricted to domestic providers. Individual savers are therefore not likely to benefit from lower prices and better products that would result from efficiency gains and returns of large asset pools. Fragmentation is expensive also for providers: the smallest divergence in national regulation means extra compliance cost. There are limited incentives for providers to offer products cross-border mainly due to high costs. On the other hand, a standardised EU personal pension product is expected to cut providers' costs by creating larger asset pools. For example, a study shows that spreading fixed costs over larger pool of members could save 25% administration costs.

The creation of an EU legislative framework for personal pensions would diminish providers' costs by creating economies of scale, particularly in the areas of investment and administration. The creation of an EU personal pensions statute would help providers operate cross-border as it would allow them to centralise certain functions at an EU-level (rather than running them locally or outsourcing). Standardisation would make it easier for providers to offer a pension solution to corporate clients active in several Member States and looking for an EU-wide personal pension solution for their employees. This could also bring a potential to realise efficiency gains in the area of distribution through using for example digital channels for selling personal pensions, as it is the case already e.g. in the UK. As such, EU legislative framework for personal pensions could be flanked by EU policy work in the area of FinTech.

Greater choice of safe and high quality personal pension products is a benefit to all individuals, whether employed, mobile or self-employed. An EU single market for personal pensions would make the product accessible to a wider range of individuals. Minimum product requirements laid down in EU rules would create transparency and simplicity as well as safety for investors. In addition, it would accommodate the increasing mobility of EU citizens and the increasingly flexible nature of work (see Annex 3 for more details on how stakeholders would be affected by this initiative). For self-employed, who do not contribute in such capacity to a state-based or occupational pension, personal pensions could be an attractive way to save for retirement.

4.POLICY OPTIONS AND ANALYSIS OF IMPACTS

The policy options and analysis of impacts are assessed in three consecutive steps.

In a first step, in section 4.1, the high level policy options under consideration are assessed against achieving the broad policy goals. In a second step, section 4.2 assesses the individual policy options of the preferred set of key product features and its implications in terms of tax treatment.

4.1.General policy options

As a first step, with a view to addressing the gaps described above, a range of high level policy options are described and analysed below. A "voluntary 2nd regime" designates a parallel EU-level regime, which would come in addition to the existing national personal pension regimes.

In the public consultation, several policy options were presented, including the creation of a personal pension product and the harmonisation of national regimes. Based on the replies received, they will be analysed further below.

Other policy options were also initially contemplated, such as the creation of a code of conduct or of a personal pension account. They are nevertheless not further analysed in the remainder of this section as they would not sufficiently address the objectives of completing the CMU and of enhancing product features of the personal pensions, not leading to the creation of a single market for personal pensions. Indeed, a code of conduct would lack legal certainty that there will be a single market for personal pensions. This option would therefore most likely not open up national markets to new types of providers.

As to a potential personal pension account, this option implies the existence of a "federal" tax on personal pension products, as in the USA, which is not considered in this Impact Assessment. In addition, as this regime is very flexible on the key features, a pension account could not bring the standardisation of personal pensions. In particular, this flexibility could lead to increased miss-selling risks, especially regarding savers with limited financial education. Overall, this option would limit the creation of a pension internal market, keeping this market local and not bringing any cross-border benefits.

|

High level policy option

|

Description

|

|

1. Baseline scenario

|

No policy action is taken

|

|

2. Pan-European Personal Pension Product (PEPP)

|

Establish a statute for a Pan-European personal pension product (PEPP), based on a set of common and flexible features through a voluntary 2nd regime.

|

|

3. Harmonisation of national regimes

|

Harmonise national personal pension regimes on the key features of a personal pension product and disclosure requirements, taxation, type of providers and prudential supervision

|

4.1.1.Baseline scenario

Under the baseline scenario, no action is undertaken and the problems described above would continue to exist. This would imply that the asset pools are likely to remain small, limited by national borders and providers would not benefit from economies of scale and investment diversification would be limited. As a consequence, there would be limited opportunities to transfer savings in personal pensions into long-term investments and providers and the development of a deep and liquid Capital Markets Union would be hindered.

Individuals would continue to have access to national pension products where they are currently available. However, they might not benefit from the best outcomes on retirement as national personal pension products would likely continue to provide insufficient transparency, remain costly and provide limited returns and might encounter difficulties to switch products. Importantly, in a number of Member States, there would be no personal pension product available. In addition, mobile workers would continue to have difficulties to manage savings in personal pension products when moving across borders and might not benefit from national tax incentives.

The contribution of PPPs to increase the savings for retirement would continue to follow the current trendline and gradually increase over time. This assumes that existing tax incentives on national products, where available, would continue to exist, driving uptake of existing PPPs. Based on a quantification exercise, under the baseline scenario the uptake of PPPs is estimated to increase (notably due to the continuation of inpayments in existing PPPs) from EUR 0.7 trillion today to EUR 1.4 trillion by 2030. Further explanation on the economic model can be found in Annex 4.

4.1.2.Pan-European personal pension product

Description

Under this option, a legislative instrument (a Regulation) would define a pan-European personal pension product (PEPP) through a set of common rules, thereby establishing a 2nd regime in the European Union. Similar types of 2nd regimes are in place, e.g. in the area of company law or financial services. Indeed, the regime for Undertakings for Collective Investment in Transferable Securities (UCITS) shows an example of a well-functioning EU single market for compliant investment funds. Similarly, a successful development of the PEPP over the coming years would set a benchmark for national personal products to follow in terms of product features.

Box 2 - The UCITS example

Since its origin in 1985, the UCITS Directive, through its successive revisions, has been the basis on which a genuine European retail investment fund 'product' has been built. UCITS has created a comprehensive legal framework that offers increased investment opportunities for businesses and households alike.

At the same time, the directive also introduced a financial services 'passport', whereby a UCITS fund can be marketed across the EU, following authorisation from the competent authorities of its country of domicile (i.e. the home country) and notification to the competent authorities of the host market. Cross border subscriptions to UCITS compliant investment funds have grown considerably since the UCITS rules were first introduced in 1985. The UCITS acronym has developed into a strong EU brand and is nowadays, apart from Europe, also recognised in Asia and South America. The success of UCITS as a cross border vehicle for investments is borne out by the rapid growth of assets that are managed in UCITS compliant funds especially in the last years. As a matter of fact, after a slow start throughout the second half of the eighties, the total assets under management grew from just above EUR1 trillion in 1993 to EUR8.2 trillion by end 2015.

This success is essentially based on a robust harmonized framework, regularly updated since its inception and a fund passport.

The fact that fund managers have been competing on their domestic markets with investment funds and asset managers from other Member States led to an increase in the overall quality of the product offering available and also helped to reduce costs and fees.

The chart below shows the progression of the UCITS volumes over time. It shows that Assets under Management reached 2 trillion EUR over ten years after the launch of the framework.

Source: European Fund and Asset Management Association (EFAMA), March 2017

A "European statute" for such a personal pension product would define key features contributing to a single market for providers, helping complete the CMU and aiming to provide simple, transparent and safe products for PEPP savers. Such features could notably include rules on distribution and advice, information requirements, investment policy (see section on key features below). In addition to rules protecting PEPP savers for the sale of the product and during the accumulation or decumulation phases, the possibility to switch PEPP provider and benefit from portability would be key to addressing PEPP savers' concerns, in particular when exercising mobility within the European Union.

The optimal definition of the PEPP key features is further described in the next section, describing the options per key feature. In this respect, the key features should achieve balance between more standardisation for the PEPP and sufficient flexibility so that providers can adapt to the different national requirements for tax incentives. In addition, the tax treatment of the PEPP can be subject to more convergence, as presented in the next section.

In analogy with the UCITs example, it can be reasonably expected that the introduction of the PEPP would be a long term process which could take more than a decade to reach its full potential. In particular the tax treatment by Member States of the PEPP will be an important factor for the provision and the take-up of the PEPP. In addition, the uptake of the PEPP could potentially consist of an important substitution effect whereby funds currently saved in deposits, other investment products or even existing PPPs would be redirected towards the PEPP. Consequently, only a limited part of the PEPP uptake would be incremental savings.

Based on the same quantification assumptions as for the baseline scenario, the volumes of PPPs combined with the PEPP could reach EUR 2.1 trillion by 2030 in the most favourable scenario whereby the PEPP would be granted a favourable tax treatment in all Member States. This implies that the introduction of the PEPP would contribute to 50% of the growth on the whole personal pension market between now and 2030. This estimate is based on the favourable assumption that PEPP would receive the same tax treatment as existing PPPs in all Member States under the baseline scenario. Should the favourable treatment of the PEPP be limited to fewer Member States, or even absent, the development of the PEPP would be sufficiently lower. Should no favourable tax treatment be granted, savers would be disincentivised to contribute to a PEPP and this would result in an outcome close to the baseline scenario of EUR 1.4 trillion. Nevertheless, the fiscal treatment of the PEPP could gradually develop over time, and national products could take on board the features of the PEPP. A detailed description of the economic model can be found in Annex 4.

Consequences

Retail investors will be provided with an additional option to save for retirement, with high quality product features, ensuring the PEPP is a safe, transparent and pan-European pension product which has the potential to provide better returns. The PEPP project is to be conceived in a long-term perspective as the provision and take-up of PEPPs would take time. The overall consequences, extent and timing of benefits of this option would depend on the approach taken as regards the level of definition of product features and the implications for the national tax treatment of PEPPs. In general, all types of providers would benefit from economies of scale as the PEPP would allow creating larger asset pools and through the standardised product features. The provision of a personal pension product cross-border would be facilitated. Individuals, especially in Member States with low product supply, would benefit from more choice. As a voluntary regime, a PEPP framework would not entail any direct consequences for national models or personal pension products which will continue to exist. Nevertheless, a substitution between distinct financial products held by households, from deposits, investment products and PPPs towards the PEPP could occur.

Assessment

The level of standardisation, and hence the possibility for providers to pool assets and achieve economies of scale, would depend on the key features determined in a statute. This would contribute to opening market opportunities to providers whose access is complicated by existing national requirements. In particular the PEPP is expected to increase competition in a market largely dominated by insurers, creating opportunities for asset managers, investment funds, pension funds and banks to enter a new market. Increased competition would bring benefits to savers by optimising product features, lowering costs and potentially improve returns. It would also allow savers to benefit from the wider range of provider choosing the product from those providers that better cater for their needs in terms of product features, offer lower costs or potentially higher returns.

Most professional stakeholders assumed in their responses to the public consultation that this option would largely address the challenges faced by existing PPPs in the EU – increasing investment in the EU and contributing to complete the CMU; enhancing product features on the personal pension market, in particular improving efficiency, asset allocation and returns; contributing to innovation within the PPP market; finally, increasing cross-border provision of PPPs by EU-based providers and widening of their range. As benefits of providing a personal pension product on an EU scale, most professional stakeholders which are insurance companies, SMEs and/or involved in the management of funds esteem as very important the lower operating costs and making the product attractive to mobile customers.

The PEPP would co-exist with national products tailored to specific national requirements and qualifying for national tax incentives. However, even if its take-up would be affected by its tax treatment in the Member States, the establishment of a single market, as well as the standardisation of key components of the product would allow providers to compete and offer a simple, transparent and safe product on a European-wide basis. In their contribution to the public consultation, professional stakeholders, in particular asset managers, showed interest in the possibilities of standardisation provided by the PEPP, even without national tax incentives. As the PEPP framework would establish an additional regime in parallel to existing national regimes, any lack of take-up of the PEPP would not have a negative impact on the existing national regimes or products.

4.1.3.Harmonisation of national regimes

Description

Under this option the EU would harmonise national personal pension regimes, either through partial harmonisation of the key features or through full harmonisation, including of the tax regime.

Consequences

Maximum harmonisation, including harmonisation of tax treatment, would contribute to establishing a real single market, as well as genuine pan-European products. A legislative statute would grant legal certainty to providers and protection to savers.

Harmonisation of the product features only would lead to a similar outcome as the establishment of a regulatory statute for a PEPP but involve major consequences for Member States' personal pensions markets.

Assessment

A maximum harmonisation option could bring the most in terms of creating a truly pan-European single market, with homogeneous asset pools and ease of cross-border access. Without it, national tax laws continue to incentivise most providers (i.e. the supply side) to offer different products and organise all related services (such as investment advice, taxation, accounting, distribution and transparency, reporting to supervisor) locally in each Member State. However, the feasibility of this option is questionable, in light of the differences between Member States' personal pensions regimes, both in terms of tax and labour law, and Member States’ insufficient willingness to change their personal pension taxation rules.

The necessary changes to existing pension products would entail considerable compliance costs (unless they were "grandfathered" and could continue under previous rules).

Professional stakeholders expressed cautiousness on the option of harmonising national personal pension regimes, especially with a view to tax requirements. Most respondents, across all sectors and fields of activity, consider that such a solution would partly address the challenges currently faced by the existing PPPs in EU, or would not address them at all.

Comparison of policy options

|

|

EFFECTIVENESS

|

EFFICIENCY

(cost-effectiveness)

|

Coherence

|

Political feasibility

|

|

Objectives

Policy

option

|

Objective 1

Increase investment in the EU and complete the CMU

|

Objective 2

Enhance product features on the personal pension market

|

Objective 3

Enhance the cross-border provision and portability of personal pension products

|

|

|

|

|

Option 1

No policy change

|

0

|

0

|

0

|

|

0

|

0

|

0

|

|

Option 2

Personal Pension Product

|

+

|

+

|

+

|

|

+

|

+

|

+

|

|

Option 3

Harmonisation of national legislation

|

++

|

++

|

++

|

|

- -

|

+

|

- -

|