EUROPEAN COMMISSION

EUROPEAN COMMISSION

Brussels, 25.9.2017

SWD(2017) 312 final

COMMISSION STAFF WORKING DOCUMENT

Activities relating to financial instruments

Accompanying the document

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

on financial instruments supported by the general budget according to Art. 140.8 of the Financial Regulation as at 31 December 2016

{COM(2017) 535 final}

3.Risk Sharing Instruments

3.1.Risk-Sharing Finance Facility under the FP7 (RSFF)

|

Policy DG in charge:

|

DG RTD

|

|

Implementing DG in charge:

|

DG RTD

|

|

Operating Body in charge:

|

EIB

|

|

Initial Overall Budget Envelope:

|

EUR 960,73 million

|

|

Current Overall Budget:

|

EUR 960,73 million

|

A -Summary

The RSFF, officially launched in July 2007, was one of the new, innovative funding mechanisms of FP7. It is a debt finance instrument, jointly developed by the Commission and the European Investment Bank (EIB). The RSFF facilitated access to finance by providing loans and guarantees to a wide range of beneficiaries — including SMEs, mid-sized enterprises, larger companies, research institutions, universities and research infrastructures — investing in RDI.

The RSFF has reached and easily exceeded almost all its operational and intermediate objectives. Three evaluative assessments clearly demonstrate that RSFF is well on its way to realising longer-term objectives and wider achievements.

Loan agreements have been signed with 114 R&I promoters, with a total loan volume (active loans) of EUR 11,31 billion and the instrument had been implemented in 25 countries.

B -Description

(a)Identification of the financial instrument and the basic act;

Decision No 1982/2006/EC of the European Parliament and of the Council of 18 December 2006 concerning the Seventh Framework Programme of the European Community for research, technological development and demonstration activities (2007-2013) (OJ L 412, 30.12.2006, p. 1).

Council Decision 2006/971/EC of 19 December 2006 concerning the specific programme ‘Cooperation’ implementing the Seventh Framework Programme of the European Community for research, technological development and demonstration activities (2007 to 2013) (OJ L 400, 30.12.2006, p. 86).

Council Decision 2006/974/EC of 19 December 2006 on the Specific Programme: ‘Capacities’ implementing the Seventh Framework Programme of the European Community for research, technological development and demonstration activities (2007 to 2013) (OJ L 400, 30.12.2006, p. 299).

(b)Description of the financial instrument, implementation arrangements and the added value of the Union contribution;

Policy objectives and scope

The RSFF, co-developed by the European Commission and the EIB, was established in June 2007. The RSFF facilitates access to finance by providing loans and guarantees to a wide range of beneficiaries — including SMEs, mid-sized enterprises, larger companies, research institutions, universities and research infrastructures —investing in RDI.

Implementation arrangements

The EU and the EIB are risk-sharing partners for loans provided by the EIB directly or indirectly to beneficiaries. The European Union, through FP7 budget resources, and the EIB have set aside a total amount of up to EUR 2 billion (up to EUR 1 billion each) for the period 2007-2013 to cover losses if RSFF loans are not repaid.

Added value

Through those EU/EIB contributions for risk-sharing and loss coverage, the EIB is able to extend a loan volume of EUR 10 billion to companies and the research community for their investments in R&D and Innovation.

(c)The financial institutions involved in implementation;

European Investment Bank (EIB)

C -Implementation

(d)The aggregate budgetary commitments and payments from the budget;

Aggregate budgetary commitments as at 31/12/2016 EUR 960,73 million

Aggregate budgetary payments as at 31/12/2016 EUR 960,73 million

(e)The performance of the financial instrument, including investments realised;

The results of the RSFF under FP7 covering from 2007 until 2013 showed a total number of 114 RDI operations, which were signed, and loan volume of EUR 11 313 million, and 112 disbursed operations (EUR 10 220 million).

The origination period of the instrument has closed as from 31/12/2013.

|

Amount of financing expected to be provided by the instrument (including EU contribution committed) to eligible final recipients,

and corresponding number of eligible final recipients;

|

EUR 11 313 million

114 eligible FRs

|

|

Amount of investments expected to be made by eligible final recipients due to the financing, if applicable

|

EUR 22 000 million

|

|

Amount of financing already provided by the instrument to eligible final recipients,

and the corresponding number of recipients;

|

EUR 10 220 million

112 eligible FRs

|

|

Amount of investments already made by eligible final recipients due to the financing provided through the instrument, if applicable.

|

EUR 20 400 million

|

(f)An evaluation of the use of any amounts returned to the instrument as internal assigned revenue under paragraph 6;

EUR 476 million have been assigned to InnovFin Horizon 2020 Loan Services for R&I Facility which is the successor financial instrument of the Risk-Sharing Finance Facility under the FP7 (RSFF).

(g)The balance of the fiduciary account

EUR 839 290 000

|

In EUR

|

|

Balance on the fiduciary account (current account)

|

7 978 000

|

|

Term deposits/Bonds (if applicable)

|

|

|

Term deposits < 3 months (cash equivalent)

|

100 927 000

|

|

Term deposits > 3 months< 1 year (current assets)

|

0

|

|

Term deposits > 1 year (non-current assets)

|

|

|

Bonds current

|

44 159 000

|

|

Bonds non-current

|

675 149 000

|

|

Other assets (if applicable)

|

11 077 000

|

|

= Total assets

|

839 290 000

|

Please note that the figures provided include RSI figures.

Impact of negative interest on RSFF: no impact as at 31/12/2016.

(h)Revenues and repayments;

For the period 2007-2016, the following revenues and repayments were received by the EU on the EU RSFF Account:

Total operating revenues: EUR 279.43 million

Total repayments: EUR 196,57 million

(i)The value of equity investments, with respect to previous years;

N/A.

(j)The accumulated figures on impairments of assets of equity;

Impairment of assets as at 31/12/16 EUR 10,69 million

(k)The target leverage effect, and the achieved leverage effect;

The target leverage of the Debt facility - defined as the total funding (i.e. Union funding plus contribution from other financial institutions) divided by the Union financial contribution - was expected to range from an average of 5 to 6,5, depending on the type of operations involved (level of risk, target recipients, and the particular debt financial instrument facility concerned).

Together with the EIB window of the Facility, the achieved leverage effect is 10,6 (amount of financing achieved / EU contribution), whereas the expected leverage effect is close to 12 with an amount of financing expected to be provided to final beneficiaries of EUR 11 313 million (the reached loan volume) and an EU contribution of EUR 960,73 million.

D -Strategic importance/relevance

(l)The contribution of the financial instrument to the achievement of the objectives of the programme concerned as measured by the established indicators, including, where applicable, the geographical diversification;

Demand for RSFF loan finance has been high since the launch of the facility in mid-2007: in its first phase (2007-2010), its take-up exceeded initial expectations by more than 50 % in terms of active loan approvals (EUR 11,3 billion versus an initial forecast of EUR 5 billion).

The RSFF has reached and easily exceeded almost all its operational and intermediate objectives. Three evaluative assessments clearly demonstrate that RSFF is well on its way to realising longer-term objectives and wider achievements.

The first interim evaluation concluded that the RSFF had been successfully introduced into the EU’s research funding scheme within FP7, was a model example of an EU financial instrument, and should be further developed and strengthened. Recommendations included the need to better target SMEs and research infrastructures. The second interim evaluation concluded that the RSFF had proved to be attractive to RDI companies and had met or exceeded its loan volume targets and enabled EIB to increase the bank's capacity to make riskier loans.

By the end of 2013, 127 RSFF operations had been approved by the EIB, with a total loan volume of EUR 16,2 billion, and the Bank had signed loan agreements with 114 R&I promoters, with a total loan volume (active loans) of EUR 11,31 billion. The sector diversification was broad, and the instrument had been implemented in 25 countries. The origination period of the instrument ended as from 31/12/2013.

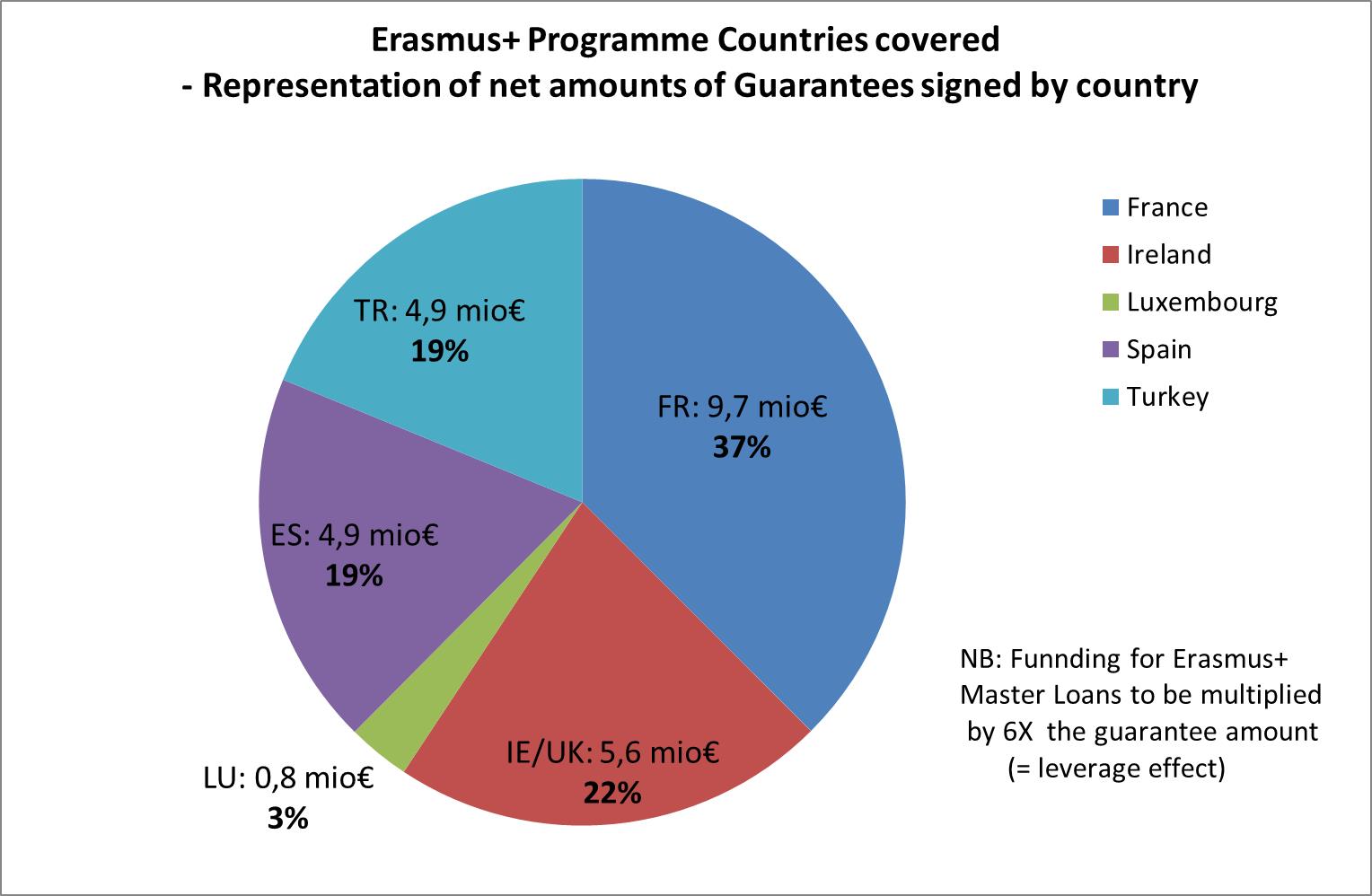

Graph: Allocation of the portfolio by country

E -Other key points and issues

At the end of 2016, reflows of EUR 476 million had been reallocated to the 'Loans Service for R&I' successor debt instrument in Horizon 2020.

3.2.Horizon 2020 Loan Services for R&I Facility

|

Policy DG in charge:

|

DG RTD

|

|

Implementing DG in charge:

|

DG RTD

|

|

Operating Body in charge:

|

EIB

|

|

Initial Overall Budget Envelope:

|

EUR 1 060 million

|

|

Current Overall Budget:

|

EUR 1 060 million

|

A -Summary

The InnovFin Large Projects, InnovFin MidCap Growth Finance and InnovFin MidCap Guarantee aim is to improve access to risk finance for R&I projects carried out by a variety of promoters notably including medium and large midcaps, larger companies, universities and research institutes, R&I infrastructures and special-purpose vehicles located in Member States or in Associated Countries.

This instrument helps addressing riskier projects or sub-investment grade promoters carrying out RDI investments across all Horizon 2020's Societal Challenges. A particular approach is foreseen to address the financing needs of midcap companies (with employees between 500 and 3 000 employees).

The InnovFin Large Projects, InnovFin MidCap Growth Finance and InnovFin MidCap Guarantee instruments offers better access to risk finance in an open, demand-driven way through direct loans or hybrid/mezzanine investments made available by the EIB as well as through risk-sharing (guarantees) involving other banks and financial intermediaries.

The InnovFin Large Projects, InnovFin MidCap Growth Finance and InnovFin MidCap Guarantee cover a broad spectrum of final recipients with a flexible loan financing approach, and are complemented by a dedicated guarantee facility for loans and leases for innovative SMEs and Small Midcaps. For 2014-2020, the EU contribution of EUR 1 060 million is targeted to mobilise an amount of financing of EUR 13 250 million for the target final recipients.

B -Description

(a) Identification of the financial instrument and the basic act;

Regulation (EU) No 1291/2013 of the European Parliament and of the Council of 11 December 2013 establishing Horizon 2020 - the Framework Programme for Research and Innovation (2014-2020) (OJ L 347/104, 20.12.2013)

Regulation (EU) No 1290/2013 of the European Parliament and of the Council of 11 December 2013 laying down the rules for participation and dissemination in "Horizon 2020 - the Framework Programme for Research and Innovation (2014-2020)" (OJ L 347/81, 20.12.2013)

Council Decision 2013/743/EU of 3 December 2013 establishing the specific programme implementing Horizon 2020 - the Framework Programme for Research and Innovation (2014-2020) (OJ L 347/965, 20.12.2013).

(b)Description of the financial instrument, implementation arrangements and the added value of the Union contribution;

Policy objectives and scope

The goal is to improve access to debt financing — loans, guarantees, counter-guarantees and other forms of debt and risk finance — for public and private entities and public-private partnerships engaged in research and innovation activities requiring risky investments in order to come to fruition. The focus is on supporting research and innovation with a high potential for excellence.

The target final recipients are potentially legal entities of all sizes that can borrow and repay money and, in particular, SMEs with the potential to carry out innovation and grow rapidly; mid-caps and large firms; universities and research institutes; research infrastructures and innovation infrastructures; public-private partnerships; and special-purpose vehicles or projects.

Implementation arrangements

The Loan and Guarantee Service for Research and Innovation is implemented by the EIB and by financial intermediaries (banks). Financial intermediaries will be guaranteed against a proportion of potential losses by EIB, which will also offer counter-guarantees to guarantee institutions. This is a demand-driven instrument, with no prior allocations between sectors, countries or regions, or types or sizes of firm or other entities.

The Delegation Agreement signed with the entrusted entity ensures that the InnovFin Large Projects, InnovFin MidCap Growth Finance and InnovFin MidCap Guarantee are accessible for large firms and medium and large midcaps, universities and research institutes, R&I infrastructures, public-private partnerships, and special-purpose vehicles or projects.

Regarding the indirect delivery, financial intermediaries selected by entrusted entities for the implementation of financial instruments pursuant to Article 139(4) of Regulation (EU, Euratom) No 966/2012 on the basis of open, transparent, proportionate and non- discriminatory procedures may include private financial institutions as well as governmental and semi-governmental financial institutions, national and regional public banks as well as national and regional investment banks.

The funding of the Loan and Guarantee Service for Research and Innovation has two main components:

·demand-driven, providing loans and guarantees on a first-come, first-served basis, with specific support for beneficiaries such as SMEs and mid-caps. This component shall respond to the steady and continuing growth seen in the volume of RSFF lending, which is demand-led. This demand-driven component will be supported by the budget of the Horizon 2020 Access to Risk Finance programme.

·Targeted, focusing on policies and key sectors crucial for tackling societal challenges, enhancing competitiveness, supporting sustainable, low-carbon, inclusive growth, and providing environmental and other public goods. That component helps the Union address research and innovation aspects of sectorial policy objectives and will be supported by other parts of Horizon 2020, other frameworks, programmes and budget lines in the Union budget, particular regions and Member States that wish to contribute with their own resources (including through Structural Funds) and/or specific entities (such as Joint Technology Initiatives) or initiatives.

The expiry date of the instrument is expected to be in 2027-2030.

Added value

This financial instrument aims to improve access to risk finance for R&I projects emanating from large firms and medium and large midcaps, universities and research institutes, R&I infrastructures (including innovation-enabling infrastructures), public-private partnerships, and special-purpose vehicles or projects (including those promoting first-of-a-kind, commercial-scale industrial demonstration projects). Firms and other entities located in Member States or in Associated Countries are eligible as final recipients.

This instrument will help address sub-optimal investment situations stemming from poor prospects within firms or other entities for the creation or commercialisation of products or services of societal importance (in the sense of Horizon 2020's Societal Challenges) or that constitute a public good. Overall, it will improve access to risk finance.

(c)The financial institutions involved in implementation;

European Investment Bank (EIB)

C -Implementation

(d)The aggregate budgetary commitments and payments from the budget;

Aggregate budgetary commitments as at 31/12/2016 EUR 796 million

Aggregate budgetary payments as at 31/12/2016 EUR 786 million

(e)The performance of the financial instrument, including investments realised;

|

Amount of financing expected to be provided by the instrument (including EU contribution committed) to eligible final recipients,

and corresponding number of eligible final recipients;

|

EUR 5 918,2 million

97 eligible FRs

|

|

Amount of investments expected to be made by eligible final recipients due to the financing, if applicable

|

EUR 17 063 million

|

|

Amount of financing already provided by the instrument to eligible final recipients,

and the corresponding number of recipients;

|

EUR 3 544,5 million

72 eligible FRs

|

|

Amount of investments already made by eligible final recipients due to the financing provided through the instrument, if applicable.

|

EUR 10 220 million

|

(f)An evaluation of the use of any amounts returned to the instrument as internal assigned revenue under paragraph 6;

EUR 6 million of 2016 revenues have been assigned to Horizon 2020 Loan Services for R&I Facility

(g)The balance of the fiduciary account;

EUR 697 996 000

|

In EUR

|

|

Balance on the fiduciary account (current account)

|

1 000

|

|

Term deposits/Bonds (if applicable)

|

693 815 000

|

|

Term deposits < 3 months (cash equivalent)

|

10 352 000

|

|

Term deposits > 3 months < 1 year (current assets)

|

|

|

Term deposits > 1 year (non-current assets)

|

|

|

Bonds current

|

71 598 000

|

|

Bonds non-current

|

611 865 000

|

|

Other assets (if applicable)

|

4 180 000

|

|

= Total assets

|

697 996 000

|

Impact of negative interest on the Facility: no impact as at 31/12/2016

(h)Revenues and repayments;

Aggregate additional resources as at 31/12/2016 EUR 31 494 000

Additional information

It should be noted that EUR 476 million have been paid back by the EIB further to the signature of the 8th amendment to the RSFF cooperation agreement and to reflows stemming from RSFF activities. In accordance with Article 52.3 of the Horizon 2020 Rules for Participation, this amount has been transferred to its successor debt instrument under Horizon 2020 (Horizon 2020 Loan Services for R&I Facility)

(i)The value of equity investments, with respect to previous years;

N/A.

(j)The accumulated figures on impairments of assets of equity or risk-sharing instruments, and on called guarantees for guarantee instruments;

Impairment of assets as at 31/12/16 90,53 million

(k)The target leverage effect, and the achieved leverage effect;

The target leverage effect equals 12,5 with an amount of financing expected to be provided by financial intermediaries of EUR 13 250 million and an EU contribution of EUR 1 060 million.

The achieved leverage effect as at 31/12/2016 is close to 4,5 with an amount of financing provided of EUR 3 544,5 million and an EU contribution of EUR 796 million.

The expected leverage effect as at 31/12/2016 is close to 7,5 with an amount of financing signed provided of EUR 5 918,2 million and an EU contribution of EUR 796 million.

D -Strategic importance/relevance

(l)The contribution of the financial instrument to the achievement of the objectives of the programme concerned as measured by the established indicators, including, where applicable, the geographical diversification;

InnovFin Large Projects, InnovFin MidCap Growth Finance and InnovFin MidCap Guarantee, like their predecessor scheme (RSFF), are demand-driven instruments, with no prior allocations between sectors, countries or regions, or types or sizes of firm or other entities.

For direct loans or hybrid/mezzanine investments, the indicators are the number and volume of loans or investments made. For intermediated loans, the indicators are the number of agreements signed with financial intermediaries and the number and volume of loans made. Targets and milestones (performance indicators) are set for EIB to incentivize implementation and to reach envisaged volumes of lending, target groups as well as satisfactory geographical coverage.

For 2014-2020, the EU contribution of EUR 1 060 million is targeted to mobilise an amount of financing of EUR 13 250 million for the target final recipients.

Graph: Signed loans EU+EIB windows as at 31/12/2016 (in EUR million)

Graph: Number of operations by country as at 31/12/2016

E -Other key point and issues

·Main issues for implementation:

ocritical for the implementation of the InnovFin Large Projects, InnovFin MidCap Growth Finance and InnovFin MidCap Guarantee will be attractiveness of the instrument, its stronger focus on midcap companies (with up to 3 000 employees) and the possibility to develop new financing approaches, if necessary, to respond to financing needs coming from the various Societal Challenges of Horizon 2020.

oHowever, the contractual arrangements between the EU and the EIB foresee sufficient flexibility to develop such new financing approaches and also to create policy-driven sub-facilities which could address specific needs (provided that additional budget resources become available).

·Main risks:

ono risks identified.

·General outlook:

obased on the very satisfactory implementation of the preceding loan instrument supported by FP7, (the RSFF), on-going demand for loans to finance riskier RDI investments, first indications for a robust project pipeline for the next 12 months, and a stronger focus on the midcap target group, the outlook for the InnovFin Large Projects, InnovFin MidCap Growth Finance and InnovFin MidCap Guarantee is generally positive.

oIt can be reasonably expected that across Horizon 2020 Societal Challenges (i.e. Energy, Bio-economy, Transport, Health), companies will seek EIB loan finance or risk sharing (via guarantees) to support medium and longer-term RDI investments. Target volumes for the Loan Service for R&I instrument with Horizon 2020 budget envisage lending of at least EUR 5 to 6,5 billion for the entire period 2014-2020.

oIn addition, under EIB's own complementary window for RDI investments, which will be part of the overall loan finance approach for RDI investments, a similar lending volume, i.e. a further EUR 5 to 6,5 billion (EUR 13 billion in total) can be expected.

3.3.Risk sharing debt instrument under the Connecting Europe Facility (CEF Debt Instrument)

Including the legacy instruments: LGTT and Pilot phase of the Project Bonds (PBI) established in the period 2007-2013 and merged into the CEF Debt

|

Policy DG in charge:

|

DG Mobility and Transport

DG Energy

DG CNECT

|

|

Implementing DG in charge:

|

DGs MOVE, ENER and CNECT

|

|

Operating Body in charge:

|

European Investment Bank

Other possible entrusted entities

|

|

Initial Overall Budget Envelope:

|

Up to 8,4% of the funds from the CEF Regulation (EU) 1316/2013

EUR 2 557 149 756

|

|

Current Overall Budget:

|

Up to 8,4% of the funds from the CEF Regulation (EU) 1316/2013

EUR 2 557 149 756

|

A -Summary

The Debt Financial instrument under the CEF will tackle one of the key failures identified in the market, i.e. the insufficient involvement of private investors in infrastructure financing throughout the Union, particularly on cross-border and riskier projects.

The objective of the Debt Instrument under the CEF is to facilitate infrastructure projects' access to project and corporate financing by using Union funding as leverage. The financial instrument shall help finance projects of common interest with a clear European added value, and facilitate greater private sector involvement in the long-term financing of such projects in the transport, energy and broadband sectors.

B -Description

(a)Identification of the financial instrument and the basic act;

Regulation (EU) No 1316/2013 of the European Parliament and of the Council of 11 December 2013 establishing the Connecting Europe Facility, amending Regulation (EU) No 913/2010 and repealing Regulations (EC) No 680/2007 and (EC) No 67/210.

(b)Description of the financial instrument, implementation arrangements and the added value of the Union contribution;

Policy objectives and scope

The goal of the CEF Debt Instrument is to contribute to overcoming deficiencies of the European debt capital markets by offering risk-sharing for debt financing. Debt financing shall be provided by entrusted entities or dedicated investment vehicles in the form of senior and subordinated debt or guarantees.

The Debt Instrument will consist of a risk-sharing instrument for loans and guarantees as well as for Project Bonds. The project promoters may, in addition, seek equity financing under the Equity Instrument (currently under development).

The instrument builds on the existing Project Bond Initiative and the Loan Guarantee for TEN-Transport. However, given that not all CEF eligible projects where market failures have been identified can be financed by capital markets or on a project financing basis and to face efficiently a changing market environment, the instrument deploys a wide toolbox available of debt products, including senior and subordinated funded and unfunded products.

All operations under the Debt Instrument are supported by a risk sharing mechanism with the EIB where the EU budget takes the first loss piece of the portfolio of such operations. The first loss provisioning provided by the EU budget is shared among all projects in the three sectors covered by the CEF DI. This allows for higher diversification and hence maximises the number of projects that can be supported by the CEF Debt Instrument. Also, the portfolios and first-loss pieces of the existing Project Bond Initiative and of the Loan Guarantee for TEN-T transport have been merged together with the CEF Debt Instrument.

With the introduction of EFSI, the CEF Debt Instrument Steering Committee has approved a complementary approach of the interplay between EFSI and the CEF debt instrument and possible future instruments, where CEF concentrates on innovative, demonstrator (for example using the CEF DI for the first time in a sector, or mode, in a Member State) and pilot products and initiatives (equity/hybrid/new products), taking into account the overall portfolio risk of such an approach - while recognising also the need to strike a balance between commitments under both funding sources, especially in the early stages.

Implementation arrangements

Risk-sharing instrument for loans and guarantees

The risk-sharing instrument for loans and guarantees is designed to create additional risk capacity in the entrusted entities. This shall allow the entrusted entities to provide funded and unfunded subordinated and senior debt to projects and corporates in order to facilitate promoters' access to bank financing. If the debt financing is subordinated, it shall rank behind the senior debt but ahead of equity and related financing related to equity.

The subordinated debt financing cannot exceed 30 % of the total amount of the senior debt issued.

The senior debt financing provided under the Debt Instrument does not exceed 50 % of the total amount of the overall senior debt financing provided by the entrusted entity or the dedicated investment vehicle (as according to part III, point I of Annex I to the CEF Regulation).

Project Bonds

The risk-sharing instrument for project bonds is designed as a subordinated debt financing in order to facilitate financing for project companies raising senior debt in the form of bonds. This credit enhancement instrument aims at helping the senior debt to achieve an investment grade credit rating. It ranks behind the senior debt but ahead of equity and financing related to equity.

The subordinated debt financing does not exceed 30 % of the total amount of the senior debt issued (as according to part III, point I of Annex I to the CEF Regulation).

Combination with other sources of funding

Funding from the Debt Instrument may be combined with other budgetary contributions listed below, subject to the rules laid down in Regulation (EU, Euratom) No 966/2012 and the relevant legal base:

·other parts of the CEF;

·other instruments, programmes and budget lines in the Union budget;

·Member States, including regional and local authorities, that wish to contribute own resources or resources available from the funds under the cohesion policy without changing the nature of the instrument.

Duration of the Debt Instrument

The last tranche of the Union contribution to the Debt Instrument shall be committed by the Commission by 31 December 2020. The actual approval of debt financing by the entrusted entities or the dedicated investment vehicles shall be finalized by 31 December 2022.

Expiry

The Union contribution allocated to the Debt Instrument shall be reimbursed to the relevant fiduciary account as debt financing expires or is repaid. The fiduciary account shall maintain sufficient funding to cover fees or risks related to the Debt Instrument until its expiry.

EU added value

This CEF Debt Instrument merged portfolio is supported by a portfolio first loss piece of which the EU holds 95% of the risk. This merged portfolio and portfolio first loss piece will allow for an improved risk diversification allowing for a better use of the EU funds committed to the merged instrument. This will in return increase the leverage and allow for a more wide deployment of the instrument bringing affordable financial support to projects targeted under CEF.

(c)The financial institutions involved in implementation;

The European Investment Bank (EIB)

Other Entrusted Entities may also be selected (not yet designated at this stage; entities to be selected in accordance with Regulation (EU, Euratom) No 966/2012).

C -Implementation

(d)The aggregate budgetary commitments and payments from the budget;

Aggregate budgetary commitments as at 31/12/2016: EUR 688 669 980

MOVE EUR 551 881 251

ENER EUR 99 289 000

CNECT EUR 37 499 729

Aggregate budgetary payments as at 31/12/2016: EUR 479 381 251

MOVE EUR 449 381 251

ENER EUR 10 000 000

CNECT EUR 20 000 000

(e)The performance of the financial instrument, including investments realised;

As at end 2016, following the merger of PBI and LGTT portfolios as of 1 January 2016, the CEF DI portfolio comprised 11 signed projects, as follows:

·Three projects in the transport sector (which benefitted from financing under the LGTT instrument;

·One energy project, i.e. Greater Gabbard project, signed in November 2013 under the Project Bond Initiative;

·One broadband project, i.e. Axione Telecom Infrastructure, signed in 2014 under the Project Bond Initiative;

·Three TEN-T projects were signed under the PBI, i.e. A11 Motorway (2014), A7 Motorway (2014), Port of Calais (2015), while two transport projects were signed after the portfolio merger in 2016, i.e. Passante di Mestre and N25 New Ross Bypass PPP;

·In June 2016, fianncial close for the refinancing of Autobahn A8 Augsburg-Ulm project in Germany (initially supported under the LGTT instrument) was achieved. The Senior Debt Credit Enhancement amounting to EUR 67.7 million played an important role in the optimisation process. No additional EU budget contribution was required for this refinancing.

An overview of the projects forming part of the CEF DI portfolio as of 31 December 2016 is provided here below:

|

CEF DI Project

|

Sector

|

Country

|

CEF DI product

|

Project Costs 31-Dec-2016 (EUR m)

|

|

AUTOBAHN A-5 PPP TEN

|

Transport

|

Germany

|

LGTT

|

628,4

|

|

EIX TRANSVERSAL C-25 PPP

|

Transport

|

Spain

|

LGTT

|

815,3

|

|

LGV SUD EUROPE ATLANTIQUE

|

Transport

|

France

|

LGTT

|

7 851

|

|

OFFSHORE TRANSMISSION NETWORK- ROUND 1 (Greater Gabbard)

|

Energy

|

UK

|

PBCE

|

424,9

|

|

A11 BRUGGE PPP

|

Transport

|

Belgium

|

PBCE

|

657,5

|

|

N25 NEW ROSS BYPASS PPP

|

Transport

|

Ireland

|

PBCE

|

169

|

|

AXIONE TELECOM INFRASTRUCTURE

|

Broadband

|

France

|

PBCE

|

189,1

|

|

AUTOBAHN A-7 PPP TEN

|

Transport

|

Germany

|

PBCE

|

772,6

|

|

CALAIS PORT 2015

|

Transport

|

France

|

PBCE

|

862,5

|

|

PASSANTE AUTOSTRADALE DI MESTRE

|

Transport

|

Italy

|

PBCE

|

990

|

|

AUTOBAHN A8 AUGSBURG ULM PPP TEN

|

Transport

|

Germany

|

SDCE

|

505

|

|

|

|

|

|

13 865,3

|

In November 2016, the first Framework Agreement under the EC-EIB Green Shipping Guarantee Programme has been signed for an amount of EUR 150 million between the EIB and Société Genérale as part of the pilot phase to be delegated under the CEF Debt Instrument. The pilot phase is expected to include Framework Agreements signed by the EIB with other partner financial institutions, and to take place in France, the Netherlands and the Scandinavian countries with an objective of providing financing for clean vessels or retrofitting of vessels.

The Programme can be further rolled out under the EFSI for a total amount of EUR 750 million of approved financing with an estimated overall volume of investments amounting to EUR 3 billion.

Total financing and investment figures in the table below include the merger of previous instruments LGTT and PBI portfolios.

|

Amount of financing expected to be provided by the instrument (including EU contribution committed) to eligible final recipients,

and corresponding number of eligible final recipients;

|

Expected EIB financing supported by the EU contribution: EUR 1 377 million

Total financing expected: 15 583 million

eligible FRs N/A

|

|

Amount of investments expected to be made by eligible final recipients due to the financing, if applicable

|

EUR 15 583 million

|

|

Amount of financing already provided by the instrument to eligible final recipients,

and the corresponding number of recipients;

|

EIB financing supported by the EU contribution: EUR 877 million

Total financing achieved: 13 865,3 million

eligible FRs: 11

|

|

Amount of investments already made by eligible final recipients due to the financing provided through the instrument, if applicable.

|

EUR 13 865,3 million

|

(f)An evaluation of the use of any amounts returned to the instrument as internal assigned revenue under paragraph 6;

No amounts returned to the instrument as internal assigned revenue as at 31/12/2016

(g)The balance of the fiduciary account

EUR 492 897 190

|

In EUR

|

|

Balance on the fiduciary account (current account)

|

7 101

|

|

Term deposits/Bonds (if applicable)

|

482 667 774

|

|

Term deposits < 3 months (cash equivalent)

|

0

|

|

Term deposits > 3 month < 1 year (current assets)

|

0

|

|

Term deposits > 1 year (non-current assets)

|

0

|

|

Bonds current and investments in Unitary Fund

|

61 458 468

|

|

Bonds non-current

|

421 209 306

|

|

Other assets (if applicable)

|

10 222 315

|

|

= Total assets

|

492 897 190

|

Impact of negative interest on CEF DI (in EUR) as at 31/12/2016: EUR 12 357

(h)Revenues and repayments;

According to the audited statements for 2016 the total revenues attributable to the Commission for the year amount to EUR 13 428 237. The revenues cover revenues from operating activities, including first loss piece remuneration, and financial revenues.

Accumulated Surplus as of 31/12/2016: EUR 23 805 002. This figure includes the revenues generated before 2016 by LGTT and PBI prior to the merger into CEF DI (EUR 4 097 607) which were paid to the EC and recorded in the FS only in 2016 in accordance with article 3 (f) of Annex 11 transitional provisions of the CEF agreement.

(i)The value of equity investments, with respect to previous years;

Not applicable

(j)The accumulated figures on impairments

of assets of equity or risk-sharing instruments, and on called guarantees for guarantee instruments;

No impairments registered at 31/12/2016

(k)The target leverage effect, and the achieved leverage effect;

The target (expected) leverage of the Debt Instrument — defined as the total funding (i.e. Union contribution plus contributions from other financial sources) divided by the Union contribution — is expected to range from 6 to 15, depending on the type of operations involved (level of risk, target beneficiaries, and the debt financing concerned).

The achieved leverage is quantified as the aggregate of the amounts raised to finance the projects supported by the CEF DI, divided by the aggregate amount of the EU Contribution committed to the instrument to date, As at 31 December 2016, the achieved leverage effect amounted to approximately 20,1x.

D -Strategic importance/relevance

(l)The contribution of the financial instrument to the achievement of the objectives of the programme concerned as measured by the established indicators, including, where applicable, the geographical diversification;

The financial instruments to be deployed under the CEF Debt Instrument will tackle one of the key failures identified in the market, i.e. the insufficient involvement of private investors in infrastructure financing throughout the Union, particularly on cross-border and riskier projects. The objective of the debt instrument under the CEF is to facilitate infrastructure projects' access to project and corporate financing by using Union funding as leverage. The CEF debt instrument shall support the financing of projects of common interest with a clear European added value, and facilitate greater private sector involvement in the long-term financing of such projects in the transport, energy and broadband sectors. At the same time, CEF debt instrument shall be designed such as to enhance the development of a sustainable financial environment – both capital markets and banks.

E -Other key points and issues

·Main issues

No specific issues.

·Main risks

No specific risks identified.

·General outlook

The CEF Debt Instrument has an important role to play through facilitating access to project and corporate financing of infrastructure projects eligible to the sectorial guidelines of the CEF Regulation in a complementary manner to EFSI, in particular to pilot projects, sectors, or financings in Member States.

The latest pipeline of projects expected to receive support under the CEF Debt Instrument over 2017-2018 is as set out below:

|

Project

|

CEF Sector

|

|

Port Development

|

TEN-T

|

|

Port Development

|

TEN-T comprehensive network

|

|

Pilot phase of the Green Shipping Guarantee (first guarantee signed in November 2016)

|

TEN-T

|

|

Liquefied natural gas project

|

TEN-E

|

|

Gas PCI Programme

|

TEN-E

|

|

Natural gas pipeline project

|

TEN-E

|

3.4.Natural Capital Financing Facility (NCFF)

|

Policy DG in charge:

|

DG ENV and DG CLIMA

|

|

Implementing DG in charge:

|

DG ENV

|

|

Operating Body in charge:

|

EIB

|

|

Initial Overall Budget Envelope:

|

EUR 60 million

|

|

Current Overall Budget:

|

EUR 60 million (2014-2017)

|

A -Summary

NCFF provides direct and indirect financing for natural capital investment projects. The financing may consist in loans or equity. It finances revenue-generating or cost-saving projects which promote the conservation, restoration, management and enhancement of natural capital that contribute to the Union's objectives for biodiversity and climate change adaptation, e.g. through ecosystem-based solutions to challenges related to land, soil, forestry, agriculture, water and waste.

The NCFF is a risk sharing financial instrument which is implemented under indirect management by the European Investment Bank.

The NCFF will finance up to 75% of total project cost for direct investments. When investing in equity funds, the maximum share is 33%.

B -Description

(a)Identification of the financial instrument and the basic act;

Regulation (EU) N° 1293/2013 of the European Parliament and of the Council of 11 December 2013 on the establishment of a Programme for the Environment and Climate Action (LIFE) Article 17.

(b)Description of the financial instrument, implementation arrangements and the added value of the Union contribution;

Policy objectives and scope

NCFF provides direct and indirect financing for natural capital investment projects. The financing may consist in loans or equity. It finances upfront investment and operating costs for revenue-generating or cost-saving projects which promote the conservation, restoration, management and enhancement of natural capital that contribute to the Union's objectives for biodiversity and climate change adaptation, e.g. through ecosystem-based solutions to challenges related to land, soil, forestry, agriculture, water and waste.

Projects will fall into four broad categories:

·Payments for Ecosystem services (PES): projects involving payments for the flows of benefits resulting from natural capital, usually a small scale bilateral transaction with a well identified buyer and seller of an ecosystem service. They are based on the "beneficiary pays" principle, whereby payments take place to secure critical ecosystem services.

·Green Infrastructure (GI): GI is a strategically planned network of natural or semi-natural areas with other environmental features designed and managed to deliver a wide range of ecosystem services. It incorporates green spaces (or blue if aquatic ecosystems are concerned) and other physical features in terrestrial (including coastal) and marine areas. On land, GI is present in rural and urban settings. GI projects have the potential to generate revenues or save costs based on the provision of goods and services, e.g. water management, air quality, forestry, recreation, flood/erosion/fire control, pollination, increased resilience to the consequences of climate change.

·Biodiversity offsets: they are conservation actions intended to compensate for the residual, unavoidable harm to biodiversity caused by development projects. They are based on the "polluter pays" principle, whereby offsets are undertaken for compliance or to mitigate reputational risks. Projects aimed at compensating damages done to Natura 2000 sites according to Article 6(4) of the Habitats Directive are not eligible for financing under the NCFF.

·Innovative pro biodiversity and adaptation investments: they are projects involving the supply of goods and services, mostly by SMEs, which aim to protect biodiversity or increase the resilience of communities and other business sectors.

Implementation arrangements

The NCFF is a risk sharing financial instrument which is implemented under indirect management by the European Investment Bank. The delegation agreement was signed on 18 December 2014.

The NCFF is currently implemented in a pilot phase, which will allow testing different financing options to focus on the most suitable approaches in a potential second phase. The EIB has the possibility to invest the available funds up to the end of 2019. An extension of the implementation period is under preparation. The overall EU budget contribution foreseen for this period is EUR 60 million, including EUR 10 million for the Technical Support Facility.

Added value

The added value of the NCFF is to address current market gaps and barriers to the private financing of projects in the field of biodiversity and climate change adaptation. The aim is to establish a pipeline of replicable, bankable investments that will serve as a "proof of concept" and that demonstrate to private investors the attractiveness of such investments for the longer term. A further aim is to leverage funding from private investors for this pipeline of investments.

The NCFF will support projects that the EIB normally does not invest in, because they are too small, the time to ensure an investment return is too long, or the perceived credit risk of biodiversity and climate change adaptation investments is too high. To this end the EIB and the Commission agreed on a risk sharing mechanism whereby the EU funds will absorb first losses in case of project failure, thereby reducing the credit risk faced by the EIB.

When assessing the EU added value of potential projects, the EIB will investigate not only the contribution to the nature, biodiversity and climate change adaptation objectives, but also the potential for demonstration effect, replicability, transferability and the ability of the investment to leverage additional funding. The aim is to invest in some 9 to 12 operations. The broad geographical coverage is to enhance the effectiveness of the pilot phase.

A technical support facility is provided for capacity building measures to help the development of successful projects. This support will be provided to operations expected to be eligible for receiving finance from the NCFF and will develop competences in preparatory, management, monitoring, evaluation, audit and control activities.

(c)Financial institutions involved in implementation;

European Investment Bank (EIB)

C -Implementation

(d)The aggregate budgetary commitments and payments from the budget;

Aggregate budgetary commitments as at 31/12/2016 EUR 50 000 000

Aggregate budgetary payments as at 31/12/2016 EUR 11 750 000

(e)The performance of the financial instrument, including investments realised;

The Delegation Agreement was signed in December 2014, no operation was signed by the end of 2016.

(f)An evaluation of the use of any amounts returned to the instrument as internal assigned revenue under paragraph 6;

N/A

(g)The balance of the fiduciary account;

EUR 10 250 000

.

|

In EUR

|

|

Balance on the fiduciary account (current account)

|

10 250 000

|

|

Term deposits/Bonds (if applicable)

|

|

|

Term deposits < 3 months (cash equivalent)

|

|

|

Term deposits > 3 months < 1 year (current assets)

|

|

|

Term deposits > 1 year (non-current assets)

|

|

|

Bonds current

|

|

|

Bonds non-current

|

|

|

Other assets (if applicable)

|

|

|

= Total assets

|

10 250 000

|

Impact of negative interest on NCFF: no impact as at 31/12/2016.

(h) Revenues and repayments (Art.140. 6);

N/A.

(i)The value of equity investments, with respect to previous years;

N/A.

(j)The accumulated figures on impairments of assets of equity or risk-sharing instruments, and on called guarantees for guarantee instruments;

N/A.

(k)The target leverage effect, and the achieved leverage effect;

·The target leverage effect.

The EU budget allocation foreseen in the LIFE regulation for the programming period 2014-2017 amounts to EUR 60 million. That amount includes EUR 50 million for the Investment Facility and EUR 10 million for the Technical Support Facility.

The total contribution by the EIB is deemed to reach EUR 100-125 million. An amount of EUR 120-240 million is the target aggregate amount of finance available to eligible final recipients supported by the Financial Instrument. For the avoidance of doubt, this amount does not include the financing that eligible final recipients make available from their own resources.

The target leverage effect as indicated in the Delegation Agreement is 2-4 (EUR 120-240 million divided by EUR 60 million of Union contribution) over the lifetime of the financial instrument.

·The achieved leverage effect: NA for 2016

D -Strategic importance/relevance

(l)The contribution of the financial instrument to the achievement of the objectives of the programme concerned as measured by the established indicators, including, where applicable, the geographical diversification;

The Delegation Agreement was signed in December 2014, and no operation was signed by 31/12/2016.

E -Other key points and issues

·Main issues:

The key implementation issues to meet the aims and requirements of the facility are:

oto identify and develop financially viable projects which have a positive impact on biodiversity and climate adaptation;

oto ensure sufficient uptake in a broad range of sectors, in view of future replicability;

oto ensure a good geographical spread among Member States, in particular in smaller Member States or where financing constraints are more acute.

·Main risks identified:

olow uptake is a risk. Publicity and communication, and the support facility will remain important in this context.

owhen implementing the NCFF, it will be taken into account that the EIB, financial intermediaries and final recipients may have limited experience with the nature and biodiversity and climate adaptation aspects of investment projects, including the proper monitoring and reporting. This is inherent to the innovative and pilot character of the instrument. The Support Facility may be used to address such issues.

oprojects will be closely monitored to ensure that biodiversity and climate adaptation objectives are achieved, in line with the LIFE Regulation.

·General outlook:

oThe first operation, 'Rewilding Europe', has been launched in April 2017, and one or two further operations are expected to be signed in 2017. They concern two indirect operations, one in the form of a loan, the other in the form of an investment in an equity fund, and a direct loan operation. Several further potential operations are being investigated covering several project categories. The entities proposing the (potential) operations come from different MS. The investment that has been launched involves a larger number of MS. This is in line with the aim to have a balanced geographical spread.

3.5.EU SME Initiative (focus on indirect Commission management part, i.e. COSME/H2020)

|

Policy DG in charge:

|

DGs ECFIN, RTD, GROW, REGIO, AGRI

|

|

Implementing DG in charge:

|

DGs RTD, GROW, REGIO, AGRI

|

|

Operating Body in charge:

|

EIF

|

|

Initial Overall Budget Envelope:

|

EUR 175 million (ceiling for contributions from each COSME and Horizon 2020)

|

|

Current Overall Budget:

|

EUR 1 137 million (ERDF)

|

A -Summary

SME support is a main focus of the European Structural and Investment Funds (ESIF), and financial instruments play an increasingly important role within ESIF support. The basic act governing ESIF interventions is the so-called Common Provisions Regulation (CPR; see below for more information).

Within the financial instruments "family", the SME Initiative is a real novelty, in that it combines different EU funding resources in one financial instrument – namely resources from ESIF, COSME or Horizon 2020 and EIB Group resources. Thereby, it increases the leverage of (both public and private) additional resources to be mobilised for SME support. Its overall aim is to enhance access to finance for SMEs, to stimulate economic growth and entrepreneurship. Access to finance is a real issue in the economy of at least several Member States in Southern and Eastern Europe: the problem is not so much the lack of liquidity in the market, but the missing transmission of that liquidity into the real economy, so that SMEs have adequate access to finance at reasonable conditions, which enables them to invest, develop their competiveness and grow. Often, a lack of collateral on the SME side is the main reason why banks are not willing to lend.

There are several crucial elements of the SME Initiative which ensure its contribution to the objectives of better SME access to finance and, thereby, enhanced SME competitiveness, innovativeness and growth – e.g. its unique and targeted products, the enhanced leverage, the early deployment and frontloading of payments, but also the streamlined and comparatively light documentation necessary to implement it. The aspect of geographical diversification in the sense of Cohesion Policy, i.e. the fact that the policy focuses explicitly on less developed regions, is also fully taken into account: the single dedicated national programme (SDNP), although being a national Operational Programme, can have regional compartments so that the regional allocations to the SME Initiative remain clearly visible.

Concrete implementation in terms of loans provided to final recipients through financial intermediaries has taken place so far (i.e. as of 31/12/2016) in Spain, Malta and Bulgaria. In Finland and Romania, financial intermediaries were at the stage of being selected by the EIF, so as to subsequently disburse new loans to SMEs, backed by the SME Initiative's uncapped guarantee. In Italy, preparations for implementing the SME Initiative were underway.

The target volume of new loans to be generated for all Spanish regions is EUR 5 723 million, out of which EUR 2 976 million are guaranteed by the ESIF contribution (at a guarantee rate of 50%). Similarly, such target volumes can be calculated for the other participating Member States as well (see summary table in the Annex to the Report).

B -Description

(a) Identification of the financial instrument and the basic act;

The EU SME Initiative may receive funding from the following four programmes.

COSME:

Regulation (EU) No 1287/2013 of the European Parliament and of the Council of 11 December 2013 establishing a Programme for the Competitiveness of Enterprises and small and medium-sized enterprises (COSME) (2014 - 2020) and repealing Decision No 1639/2006/EC (OJ L 347/33 of 20 December 2013). The European Commission has established financial instruments that aim to facilitate and improve access to finance for SMEs in their start-up, growth and transfer phases, complementary to the Member States' use of financial instruments for SMEs at national and regional level.

H2020:

Regulation (EU) No 1291/2013 of the European Parliament and of the Council of 11 December 2013 establishing Horizon 2020 - the Framework Programme for Research and Innovation (2014-2020) and repealing Decision No 1982/2006/EC (OJ L 347/104 of 20 December 2013) and pursuant to the Decision No 2013/743/EU of the Council of 3 December 2013 establishing the Specific Programme implementing Horizon 2020 – the Framework Programme for Research and Innovation (2014-2020), the European Commission has established financial instruments that aim to ease access to the risk financing for final recipients carrying out research and innovation projects.

ERDF and EAFRD (Article of the 39 CPR):

Regulation (EU) No 1303/2013 of the European Parliament and the Council laying down common provisions on the European Regional Development Fund, the European Social Fund, the Cohesion Fund, the European Agricultural Fund for Rural Development and the European Maritime and Fisheries Fund and laying down general provisions on the European Regional Development Fund, the European Social Fund, the Cohesion Fund and the European Maritime and Fisheries Fund and repealing Council Regulation (EC) No 1083/2006 (OJ L 347/320 of 20 December 2013).

(b)Description of the financial instrument, implementation arrangements and the added value of the Union contribution;

Policy objectives and scope

The SME Initiative has been presented on 27-28 June 2013 in the Commission's and EIB's joint report to the European Council, to complement and utilise synergies between existing SME support programmes at national and EU level. More specifically, the SME Initiative is a joint instrument, combining EU funds available under COSME and Horizon 2020 and ERDF-EAFRD resources in cooperation with EIB/EIF in view of generating additional lending to SMEs.

Implementation arrangements

Three financial instruments could be implemented under the SME Initiative, and they boil down in substance to two alternative ways of operating, namely:

(*) uncapped guarantees providing capital relief to financial intermediaries for new portfolio of debt finance to SMEs and

(**) securitisation instruments (with two possibilities, i.e. option n°2 securitisation instrument with MS contribution used exclusively for the participating MS and option n°3 securitisation instrument with several MS contributions pooled and used to provide protection on the aggregate exposure, particularly to the mezzanine tranches guaranteed by EIF).

The period of time during which the participating Member State may commit some funds to the EIF was to expire on 31 December 2016. As defined in the funding agreement to be signed between the EIB and the participating MS, the selected financial intermediary will originate new debt finance no later than the end of the eligibility period (i.e. 31/12/2023).

In terms of budget, the Common Provisions Regulation foresees a global ceiling (for all Member States) of EUR 8,5 billion of aggregate ERDF-EAFRD to be committed under the SME Initiative, and a ceiling by Member State of 7 % of their allocation from the ERDF and EAFRD. In that scenario, the corresponding maximum COSME and Horizon 2020 contributions would amount to EUR 175 million each over the 2014-2016 period.

As of 31/12/2016, financial intermediaries were selected in Spain, Malta and Bulgaria, and partly in Finland. The selection process of banks by the EIF was still ongoing in Romania and partly in Finland, and in preparation in Italy. The instrument's implementation in all the participating Member States is based on their respective Operational Programmes approved by the European Commission between 2014 and 2016 and their Intercreditor and Funding Agreements signed in 2015 and 2016.

Added value

As indicated in the legal base, the added value of the EU contribution results in a minimum leverage effect (e.g. 4 in Spain and Malta) over the lifetime of the financial instrument for the ERDF contribution. Based on the minimum leverage of the instrument agreed in the Single Dedicated National Programme, it is estimated that the total amount of investments/loan volumes mobilised would be e.g. around EUR 6 billion for Spain and Malta (based on all available funds, i.e. ERDF, H2020, EIB/EIF and private (bank) funds). Apart from this minimum leverage, for the ERDF part of the Initiative, most Member States have negotiated target leverages with the EIF in their Funding Agreements, which go beyond the respective minimum leverages.

A portion of the new Debt Finance portfolio equal to at least 20 times the contribution under the COSME Regulation and/or 9 times the contribution under the H2020 Regulation should fulfil respectively the COSME and/or H2020 eligibility criteria. Therefore, the table under point k) is summarising the overall leverage that should be reached for each option. The new debt finance originated by the selected financial intermediary should also include an amount equal to 20 times the COSME and/or 9 times the H2020 contribution.

(c)The financial institutions involved in implementation;

European Investment Bank

European Investment Fund

C -Implementation

(d)The aggregate budgetary commitments and payments from the budget;

Aggregate budgetary commitments as at 31/12/2016:

23 280 826,31

Aggregate budgetary payments as at 31/12/2016:19 277 097,31

(e)The performance of the financial instrument, including investments realised;

No data yet available.

(f)An evaluation of the use of any amounts returned to the instrument as internal assigned revenue under paragraph 6;

No amounts returned to the instrument as internal assigned revenue as at 31/12/2016.

(g)The balance of the fiduciary account;

N/A (due to aggregation with other funds under H2020).

(h)Revenues and repayments;

No data yet available.

(i)The value of equity investments, with respect to previous years;

N/A.

(j)The accumulated figures on impairments of assets of equity or risk-sharing instruments, and on called guarantees for guarantee instruments;

EUR 782 176 for all risk takers

(k)The leverage effect;

The target leverage effect

The target leverage may vary between the different national instruments depending the risk sharing arrangement in the Intercreditor Agreements. The following table shows for illustrative purpose the calculation of the target leverage for the SME Initiative in Spain, in accordance with the agreed approach for such calculation. The figures represent the different risk covers/risk takers as defined in the Intercreditor Agreement: in absolute and percentage terms, the loan portfolio will have a senior tranche/risk cover accounting for 69% of its size, an upper mezzanine (4,5%), middle mezzanine (0,5%) and lower mezzanine (3,0%) part as well as a junior tranche (23%). Summing those amounts up, the part of the portfolio that is backed by the guarantee is obtained: EUR 2 862 million.

Since for the SME Initiative in Spain a guarantee rate of 50% was agreed, the originating banks will retain 50% of the risk, and the overall portfolio is thus double the amount above, i.e. EUR 5 723 million. These are loans to SMEs. Dividing this aggregate amount of EUR 5 723 million by the aggregate support provided through ERDF and Horizon 2020, EUR 816,8 million, provides the leverage targeted, namely 7,0.

Calculation of target leverage for the SME Initiative in Spain

|

SIUGI Risk Cover

|

Risk taker

|

Maximum Risk Cover Size (EUR)

|

Target Rating (at least)

|

|

Senior Risk Cover

|

EIB

|

1 974 461 538,46

|

Aa3

|

|

Upper Mezzanine Risk Cover

|

EIF

|

128 769 230,77

|

Baa3

|

|

Middle Mezzanine Risk Cover

|

Horizon 2020

|

14 307 692,31

|

Ba1

|

|

Lower Mezzanine Risk Cover

|

ESIF

|

85 846 153,85

|

Ba2

|

|

Junior Risk Cover

|

ESIF

|

658 153 846,15

|

Not Rated

|

|

Guaranteed Portfolio without originator

(corresponds to 50% because of a 50% guarantee rate)

|

|

2 861 538 461,54

|

|

|

Originator's risk (bank own risk)

|

|

50%

|

|

|

Total amount of the guaranteed loan portfolio (100%)

|

|

5 723 076 923,08

|

|

|

Total ERDF/COSME/Horizon2020

|

|

816 800 000,00*

|

|

|

Leverage in relation to ERDF (but based on ERDF, H2020, EIB and EIF funds)

|

|

7,0

|

|

* EU contribution including management costs and fees

The achieved leverage effect

SME Initiative in Spain:

·SIUGI actual total loan volume : EUR 2 616 million,

oOut of which from H2020 : EUR 251,7 million

oNumber of SIUGI Final Recipients Transactions: 33 285

oThe achieved leverage effect for signed operations over ERDF/Horizon2020 reaches 3,2

The Expected Leverage for Signed Operations

The expected leverage effect for signed operations over the ESIF contribution is factor 7.

D -Strategic importance/relevance

(l)The contribution of the financial instrument to the achievement of the objectives of the programme concerned as measured by the established indicators, including, where applicable, the geographical diversification;

SME support is a main focus of the European Structural and Investment Funds (ESIF). This is reflected by the CPR's thematic objective 3 "Enhancing the competitiveness of SMEs", under which in 2014-2020 according to preliminary figures about EUR 59 billion will be devoted to supporting SMEs (EUR 32,4 billion by the ERDF and EUR 26,6 billion by the EAFRD). The investment priorities as laid down in the ERDF Regulation (No 1301/2013) illustrate the objectives of the ESIF programmes: promoting entrepreneurship, developing new business models for SMEs, supporting SMEs' growth and innovation capacities.

While much of this support is still provided through grants, financial instruments play an increasingly important role. Within the financial instruments "family", the SME Initiative is a real novelty, in that it combines different EU funding resources in one financial instrument, thereby increasing the leverage of (both public and private) additional resources to be mobilised for SME support.

In the Single Dedicated National Programmes (SDNPs) that Member State have to establish to devote ESIF resources to the SME Initiative, the progress in implementing the SME Initiative is measured against output indicators (e.g. the number of SMEs receiving support, the ERDF amount committed to cover the New Debt Finance portfolio (for the uncapped guarantee option) and the ERDF amount used to cover the existing portfolios of debt finance to SMEs (for the securitisation option)) as well as against result indicators (e.g. reduction in the market failure for debt finance, improvement of SMEs' access to finance, or the minimum leverage that the instrument sets out to achieve).

The Single Dedicated National Programmes for Spain (ERDF contribution of EUR 800 million) and Malta (ERDF contribution of EUR 15 million) were signed at the end of 2014. Those for Bulgaria (ERDF contribution EUR 102 million) and Italy (ERDF contribution EUR 100 million) were signed towards the end of 2015, while those for Romania (ERDF contribution EUR 100 million) and Finland (ERDF contribution EUR 20 million) were signed in spring 2016. In all these Member States, following the signature of these Operational Programmes, Intercreditor Agreements (bringing together all the risk-takers/contributors to the structure, i.e. the respective Member State, the Commission, EIB and EIF) and Funding Agreements (between Member State and EIF – for the ERDF part) were negotiated and signed (the last ones in autumn 2016). Subsequently, the EIF launched calls for expression of interest to select the banks that were to benefit from the uncapped guarantee and/or securitisation, in exchange for generating new loan portfolios to SMEs at favourable conditions for these final recipients.

The aspect of geographical diversification in the sense of Cohesion Policy, i.e. the fact that the policy focuses explicitly on less developed regions, is also fully taken into account: the SDNP, although being a national Operational Programme, can have regional compartments so that the regional allocations to the SME Initiative remain clearly visible and traceable.

E -Other key points and issues

· Main issues, for the implementation:

othe firm political will and commitment to implement the SME Initiative with all its novel elements (e.g. the various funds it brings together) is a conditio sine qua non for implementing it successfully. This also means that the different services involved within the Government (even more so if national and regional players come in) have to cooperate very effectively and efficiently.

oMoreover, a continuous reality check and reassessment needs to be carried out regarding the two options/financial products – are they really the ones best placed to improve SME access to finance? Are they adequately designed to meet the needs of SMEs (and financial intermediaries)? Is the financial volume dedicated to them appropriate? The SME Initiative has to ensure it complements – through its particular set-up and its specific products – existing financial instruments (and grants) and provides synergies with them.

oWhile the uncapped guarantee instrument was ready for implementation (e.g. in Spain) at the beginning of 2015, Commission services and the EIF worked together throughout the second half of 2015 to prepare the provisions for the instrument's option 2, securitisation (which is the option Italy has chosen). In 2016, this workstream could be successfully finished, with the common provisions for option 2 being in place and available for implementation. .

·Main risks:

oTo be seen once more Member States embark on implementation on the ground.

·General outlook:

·The central problem of the economy of at least several Member States in Southern and Eastern Europe is not the lack of liquidity in the market, but the missing transmission of that liquidity into the real economy, so that SMEs have adequate access to finance at reasonable conditions, which enables them to invest, develop their competiveness and grow. Often, a lack of collateral on the SME side is the main reason why banks are not willing to lend. In such a context, products offered by the SME Initiative such as the uncapped guarantee instrument are very well-suited to tackle the main obstacles for SMEs to get appropriate access to finance. Hence, in principle, the main rationale for the SME Initiative remains fully valid.

·The implementation and the preparatory steps in all of the Member States concerned progressed according to plan in 2016, and the Commission was satisfied to see an increased takeup of the instruments. It is expected to continue in 2017 with the outstanding steps to be completed timely in 2017 (i.e. finalisation of the selection process of banks by the EIF for Romania and Finland and similarly in Italy, where this was less progressed though at the end of 2016).

4.Dedicated Investment Vehicles

4.1.The European Progress Microfinance FCP-FIS

|

Policy DG in charge:

|

DG EMPL, with participation of DG ECFIN for the design of the instruments

|

|

Implementing DG in charge:

|

DG EMPL

|

|

Implementing Body in charge:

|

EIF

|

|

Initial Overall (2007-2013) Programme Budget:

|

EUR 78 million*

|

|

Current Overall (2007-2013) Programme Budget:

|

EUR 80 million

|

|

Executed Budget since beginning until 31/12/2016:

|

Commitments: EUR 80 million

Payments: EUR 80 million

|

*Initial voted commitments out of which EUR 75 million from DG EMPL and EUR 3 million from EPPA (DG REGIO).

A -Summary

The EPMF FCP-FIS is managed by the Management Company (EIF). The specific investment objective of the Fund is to increase access to, and availability of a range of financial products and services in the area of microfinance for:

·Persons starting their own enterprise, including self-employment;

·Enterprises, especially microenterprises;

·Capacity building, professionalization and quality management of microfinance institutions and of organisations active in the area of microfinance;

·Local and regional employment and economic development initiatives.

The Fund provides mainly debt products priced below market for the final benefit of the eligible final recipients.

As of 30/09/2016, EIF had signed 50 loan agreements in 16 member states including a Commission contribution of EUR 80 million while 32 428 micro-enterprises and vulnerable persons had been supported under the Facility for a total microloans volume of EUR 236,06 million thereby supporing 56 861 jobs.

As at 30/09/2016, the entire programme (EPMF-G + EPMF-FCP FIS) provided 56 221 micro-loans to final recipients, reaching the volume of EUR 471,7 million.

B -Description

(a)Identification of the financial instrument and the basic act;

Decision No 283/2010/EU of the European Parliament and of the Council of 25 March 2010 establishing a European Progress Microfinance Facility for employment and social inclusion.

EU Microfinance Platform MICROFINANCE PLATFORM (the “Fund”) is structured as a Luxembourg “fonds commun de placement – fonds d’investissement spécialisé” (FCP - FIS) governed by the law of 13 February 2007 relating to specialised investment funds (the “2007 Law”) and launched on 22 November 2010.

It is established as an umbrella fund, which may have several sub-funds. The Fund has been launched with an unlimited duration provided that the Fund will however be automatically put into liquidation upon the termination of a sub-fund if no further sub-fund is active at that time. At 31 December 2013, the Fund has had a single sub-fund - the European Progress Microfinance Fund (the “Sub-fund”) - created with a limited duration ending on 30 April 2020.

(b)Description of the financial instrument, implementation arrangements and the added value of the Union contribution;

Policy objectives and scope

The Fund is an unincorporated co-ownership of securities and other eligible assets. The Fund does not have legal personality. The Fund is therefore managed in the exclusive interests of the Unit-holders (the European Union, represented by the Commission, and the EIB) by the Management Company (EIF) in accordance with Luxembourg laws and the Management Regulations.

The specific investment objective of the Fund is to increase access to, and availability of a range of financial products and services in the area of microfinance for the following target groups (see also the objectives under the EPMF-Guarantee Facility above):

·persons starting their own enterprise, including self-employment;

·enterprises, especially microenterprises;

·capacity building, professionalization, and quality management of microfinance institutions and of organisations active in the area of microfinance;

·local and regional employment and economic development initiatives.

Implementation arrangements

The FCP-FIS is managed by the Management Company (EIF) which is vested with the broadest powers to administer and manage the Fund and the sub-fund(s) in accordance with the Management Regulations and Luxembourg laws and regulations and, in the exclusive interest of the Unit-holders, to exercise all of the rights attaching directly or indirectly to the assets of the Fund.

The EIF has the exclusive authority with regard to any decisions in respect of the Fund or any sub-fund(s), and shall act with the diligence of a professional management company and in good faith in the exclusive interests of the Unit-holders.

The Fund issues unit classes, which are redeemable at the option of the Management Company on a pro rata basis among existing investors in accordance with the provisions of the management regulations and the commitment agreements.

Unit classes are issued and redeemed at the option of the Management Company at prices based on the Fund’s net asset value per Unit of the related redeemable Unit classes at the time of issue or redemption.

The following classes of Units are available for subscription under the single sub-fund of the Fund:

·Junior Units

Junior Units are subordinated to the Senior Units and shall bear the first net losses in the Sub-Fund's assets. Junior Units are reserved for the European Commission.

·Senior Units

Senior Units are senior to Junior Units and shall only suffer a net loss in the Sub-fund's assets if the cumulated Net Asset Value of all Junior Units together has been reduced to zero.