EUROPEAN COMMISSION

EUROPEAN COMMISSION

Strasbourg, 12.4.2016

SWD(2016) 117 final

COMMISSION STAFF WORKING DOCUMENT

IMPACT ASSESSMENT

assessing the potential for further transparency on income tax information

Accompanying the document

Proposal for a Directive of the European Parliament and of the Council

amending Directive 2013/34/EU as regards disclosure of income tax information by certain undertakings and branches

{COM(2016) 198 final}

{SWD(2016) 118 final}

Table of Contents

1Introduction

2Policy context, Problem definition and Subsidiarity

2.1The OECD BEPS: A multilateral approach endorsed by the G20

2.2The US model

2.3State of play in the EU

2.4Problem definition

2.4.1Drivers

2.4.2The problem identified

2.4.3Direct consequences

2.4.4Indirect consequences

2.4.5Affected stakeholders

2.5Baseline Scenario

2.6The EU's right to act, subsidiarity check

2.6.1Subsidiarity

2.6.2International dimension

2.6.3Legal base

3Objectives

4Policy Options

4.1Preliminary approach on the definition of options

4.1.1Content of the information that should be disclosed

4.1.2Transparency: provided by whom?

4.1.3Which companies should be in the scope of a potential initiative

4.1.4Labelling system

4.1.5Publication

4.1.6Enforcement and Audit

4.1.7Link with the existing CBCR requirements for banks and extractive industries

4.2Option 1 - Baseline Scenario

4.3Option 2 – Public CBCR on EU controlled operations

4.3.1Option 2A: Public CBCR on EU controlled operations broken down by EU Member State and aggregated for non-EU operations

4.3.2Option 2B: Public CBCR on EU controlled operations broken down by Member State and third country

4.4Option 3 – Public CBCR on worldwide operations

4.4.1Option 3A: Public CBCR on worldwide operations broken down by EU Member State and aggregated for non-EU operations.

4.4.2Option 3B: Public CBCR on worldwide operations broken down by Member State and third country

4.5Summary of the Options

5Analysis of Impacts

5.1Economic impacts

5.1.1Impact on Growth and Jobs

5.1.2Impact on Market efficiency

5.1.3Impact in terms of level playing field

5.1.4Impact on the competitiveness of EU companies

5.1.5Impact in terms of misinterpretation risk.

5.1.6Tax adjustments and disputes resulting in double taxation

5.1.7Impact on tax revenues

5.2Social and societal impacts

5.3Fundamental rights

5.4Compliance costs and other costs

5.4.1Compliance costs

5.4.2Other costs for companies

5.4.3Costs for authorities

5.5Impacts on third countries

5.6Summary of the impacts

5.6.1Comparison between Options by categories of impact

5.6.2Comparison between Options by affected stakeholder groups

6Comparing the Options

6.1Effectiveness of the options in the context of existing international and European initiatives on tax avoidance

6.1.1Potential impacts of further corporate tax transparency on the multilateral approach of the G20 and the OECD

6.1.2Effectiveness in the context of the G20/OECD approach and the ATAP

6.2Comparison of policy options against effectiveness and efficiency criteria

6.2.1Assessing the effectiveness and efficiency of Option 2A

6.2.2Assessing the effectiveness and efficiency of Option 2B

6.2.3Assessing the effectiveness and efficiency of Option 3A

6.2.4Assessing the effectiveness and efficiency of Option 3B

6.3Preferred option

6.4Overall impacts of the package

7Monitoring and Evaluation

8Glossary

9References

Annex A: Procedural Issues and Consultation of Interested Parties

Annex B: Synopsis report on the consultation activities undertaken by the European Commission to assess the potential for further transparency on corporate income taxes

Annex C: Features of a Country-By-Country Reporting according to OECD BEPS Action 13

Annex D: Background and context: overview of legislative and non-legislative framework

Annex E: Tax adjustments, tax disputes and resolution mechanisms

Annex F: IFRS notes: Geographical information and corporate income tax – illustrative example (abstract, source: Deloitte)

Annex G: FORM 10-K: Illustrative examples of geographic information

Annex H: Parliament's inquiries

Annex I: Compatibility with the Charter of Fundamental Rights - detailed analysis

Annex J: Comparison of extant country-by-country models

Annex K: Analysis of information to be disclosed in a CBCR

Annex L: Analysis of the corporate income tax gap

Annex M: Breakdown of MNEs by country/region

Annex N: U.S. SEC definition of a significant subsidiary

Annex O: Worldwide publication regime of individual accounts

Annex P: Interaction with CBCR requirements for banks and extractive industries

Annex Q: Additional background analysis supplementing the economic analysis section of the impact assessment of increased corporate income transparency

Annex R: Description of a possible labelling system.

Annex S: Compliance costs

Annex T: Who is affected by the initiative and how

ANNEX U: Profit Shifting

1Introduction

This impact assessment explores the case for further transparency vis-à-vis the public with respect to the way companies manage taxable profits per jurisdiction and the related amounts of corporate income tax paid. Corporate income tax revenue for each of the 28 Member States of the Union amounted to an average of 2.6% of GDP in 2012. According to a study by the European Parliament the EU loses EUR 50-70 billion in revenues each year due to corporate tax avoidance.

The fact that certain multinational enterprises (MNEs) appear to pay little tax in relation to their income and profits, while many citizens have been heavily impacted by fiscal adjustments has been met with public criticism. Some of the criticism concerns also tax rulings, as well as the extent of competition among States which translate into specific features of tax laws.

The Commission's analysis shows that pricing of intra-firm transactions and strategic IP location could explain about 70% of profit shifting

. That said, there is no conclusive evidence that this has led to the prevalence of low effective CIT rates. For instance, the overall effective tax rates of the largest 100 MNEs based in the United States has been found to average 30% between 2001-2010, and approximately 34% for the largest MNEs based in the EU. This is in spite of the fact that the United States' statutory rate is more than ten percentage points higher than the EU average. Various sources point to average effective CIT rates in the EU of about 20%, however with significant differences between Member States.

The European Commission, the European Parliament, the Council, the OECD, the G20 and many governmental organisations are committed to the fight against tax evasion and tax avoidance. The work in this document takes as given the fact that while MNEs’ profits are managed globally, their taxation is local. Under this premise, only a number of combined measures could put an end to base erosion and profit shifting (BEPS), many of which lie in the field of taxation rules, international treaties, intra-EU co-operation and transparency, some of which may interplay with this impact assessment. In 2011, for instance, the European Commission proposed a Common Consolidated Corporate Tax Base (CCCTB) as a framework for ensuring effective taxation where profits are generated, which is being relaunched. On 28 January 2016, The Commission also published the Anti-Tax Avoidance Package (ATAP).

The Commission wants to ensure that the country in which a business’ profits are generated is also the country of taxation. This impact assessment examines different options for further corporate tax transparency under the umbrella of the Commission's work program.

2Policy context, Problem definition and Subsidiarity

2.1The OECD BEPS: A multilateral approach endorsed by the G20

MNEs' taxation is a global issue. The G20 calls for a global solution to fight tax evasion and avoidance on corporate income taxes by multinational enterprises. According to the G20 international cooperation and integrity of national tax systems are key. The G20 shaped its tax agenda around three main elements: 1) Base erosion and profit shifting (BEPS), 2) Automatic exchange of tax information (AEOI) and 3) Tax and development.

The G20 leaders and the OECD have put substantial hope into the efficiency of the OECD BEPS Action Plan developed by the OECD. The Plan was endorsed by the G20 leaders at the Antalya summit in November 2015. Leaders said: "To reach a globally fair and modern international tax system, we endorse the package of measures developed under the ambitious G20/OECD Base Erosion and Profit Shifting (BEPS) project. Widespread and consistent implementation will be critical to the effectiveness of the project".

The BEPS initiative includes 15 proposals for action, a number of which are designed to enhance transparency – in the sense of transparency towards and between tax authorities by exchange of information. BEPS Action 13 is particularly relevant from the angle of corporate transparency, as it contains features of country-by-country reporting even if the disclosure will be done on a confidentiality basis to tax administrations. BEPS Action 13 includes

guidance on Transfer Pricing Documentation and CBCR

, a model legislation, and proposes a Multilateral Competent Authority Agreement (MCAA) on the Exchange of CBCR. In addition, BEPS Action 11 seeks to address weaknesses in the existing data, as well establish methodologies to collect and analyse data on BEPS in the future, which could provide indications of the scale and economic impact of BEPS.

2.2The US model

In the US, disclosure by companies is regulated at Federal level mainly for issuers of securities on capital markets. The geographical breakdown of information to be given by these issuers is structured in terms of US versus non-US activities. It is limited to a few key items: revenues, long-lived assets and corporate income tax expense. Per US GAAP, issuers must provide a breakdown of their revenues (and certain long-lived assets) on a geographical basis showing separately the revenues in the country of domicile and, as the case may be, in material countries. A total figure must be given for revenues in the remnant countries. In addition, the Securities and Exchange Commission requires the disclosure by the issuers of their corporate income tax expense (current and deferred) on a geographical basis as follows: domestic (US State level and Federal level), and foreign (total figure for other countries).

2.3State of play in the EU

The Commission has tabled comprehensive and ambitious packages in the course of 2015 and 2016 to tackle tax evasion. The Anti-Tax Avoidance Package (ATAP) proposed on 28 January 2016 is particularly relevant in that it addresses the submission of a CBCR by certain MNEs to their tax authorities, as well as the exchange of that information between tax authorities, as described in the baseline scenario.

Particularly relevant as well in the frame of this impact assessment is the CCCTB. The legislative process on the proposal made by the Commission back in 2011 has stalled largely because of its scale. The CCCTB aims to allow businesses to compute their tax base according to a set of common rules, which would replace the current setting of different rules in each Member State where they operate. An important advantage of the CCCTB is the fact that within the Union, tax consolidation makes transfer pricing largely obsolete and discourages profit shifting for MNEs within the consolidated group. This should render tax competition more transparent in the EU because, the tax base being the same across the group, differences in tax rates become evident. In defending the internal market against aggressive tax planning, the CCCTB will also allow Member States to implement a common approach vis-à-vis third countries. Clearly, with the CCCTB, there will be less room for tax planning. The re-launch of the CCCTB has been announced by the Commission in the fourth quarter of 2016, in two stages. This would reduce the added value of a CBCR to a certain extent, whether submitted to tax authorities or public. However, CBCR would continue to have added value in terms of tax competition within the EU (tax rates) and as regards the EU vis-à-vis third countries.

Under EU law, limited liability companies established in the EU are required to publish their financial statements. Their content is driven by Generally Accepted Accounting Principles (GAAP) and other rules adopted by the EU (Accounting Directive, IFRS, Transparency Directive…). This information is mainly designed to inform and protect shareholders, investors and other stakeholders.

As per the relevant GAAP, the financial statements disclose information on CIT with varying degrees of details. For instance, the IFRS require disclosures and reconciliation on the effective tax rate. In the EU, large companies must in addition disclose the average number of employees, net assets, stated capital, accumulated earnings and a complete list of companies consolidated in the financial statements. However, GAAP applied in the EU require no geographical breakdown of tax-related information per country.

Given that companies in the EU publish their individual financial statements, it should be possible in theory for any stakeholder to reconstruct, for a given EU MNE group, the breakdown on a country-by-country basis of information such as the profit before tax, tax expense, headcount and assets. However, this ability is hampered by the limited availability of information (generally observed in third countries) and the resources necessary to engage in such exercise, even as regards information publically available in the EU. Consequently, a detailed geographical breakdown of information is not carried out, except for companies that have volunteered to disclose the information.

On several occasions, the European Parliament recommended corporate transparency by ways of a CBCR by all industry sectors. This call follows that of many civil society organizations campaigning for country-by-country reporting. Among others, these include Tax Justice Network, Transparency International, Financial Transparency Coalition, Eurodad, Christian Aid and Oxfam International. These organizations pursue a number of different goals: to increase governments' accountability, to flag up corruption risks, to aid developing countries, to help tax authorities, concerned citizens and journalist in their investigation, to ensure fair amounts of taxes paid… Eurosif, a pan-European sustainable and responsible investment (SRI) organisation whose mission is to promote sustainability through European financial markets, also supports a public CBCR in order to arrive at an effective tax system. Investigations conducted in the French Parliament in 2013 have led the rapporteurs to recommend expanding CBCR to all industry sectors. However in 2015, the French Parliament decided to not introduce a public CBCR. Further to investigations made in 2012 and 2013, select committees of the UK Parliament supported greater transparency by companies, but did not include a public CBCR in their recommendations.

The demand for more detailed information on corporate tax generally hinges on the assumption that it would assist any stakeholder to assess whether MNEs have paid their fair share of taxes. Neither international standard setters nor Member States have thus far catered to this demand. The demand is not regarded as something to be addressed in the financial statements, given that the objectives of the former (tax oriented) do not fit with those of the latter (investor protection). Some private initiative have nevertheless flourished such as fair trade & transparency labels (Fair Tax Mark in the UK, Taxparency in the Czech Republic) and a few companies in the EU volunteer to publish a CBCR. However, the scale and scope of these initiatives have thus far remained limited.

Transparency on taxes paid, in the form of country-by-country reporting, is already in place for certain sectors and industries. From 2015 onwards, credit institutions and investment firms (hereafter referred to under the generic term "banks") established in the EU must publish their CBCR reports. The aim of the reporting requirement is to regain (public) trust in the financial sector. Large extractive and logging industries will also be obliged to publish their payments to governments on a country-by-country basis from 2017 onwards. In this regard, the CBCR aims to empower local communities of resource-rich countries through disclosing information about the payments made to their governments.

In a review clause relating to the possible extension of the CBCR in the Accounting Directive, the Commission has been requested to consider any extension of the current CBCR regimes, "taking into account developments in the OECD and the results of related European initiatives".

Two years after this request was formulated, the world has been moving fast towards improving tax schemes and multilateral cooperation, under the aegis of the G20.

Besides, a few lessons can be drawn on the basis of CBCR published by banks in the EU since 2015. The measure was not intended to be a tax measure, but a tool 'essential for regaining the trust of citizens of the Union in the financial sector'. The financial sector is reported to be a significant contributor by way of corporate income tax. In 2014 the Commission reported that CBCR was not expected to have significant negative impacts economically, in particular on competitiveness, investment, credit availability or the stability of the financial system. It could even result in a slight positive impact by lowering the cost of capital. Costs relating to a CBCR did not appear to be a key factor.

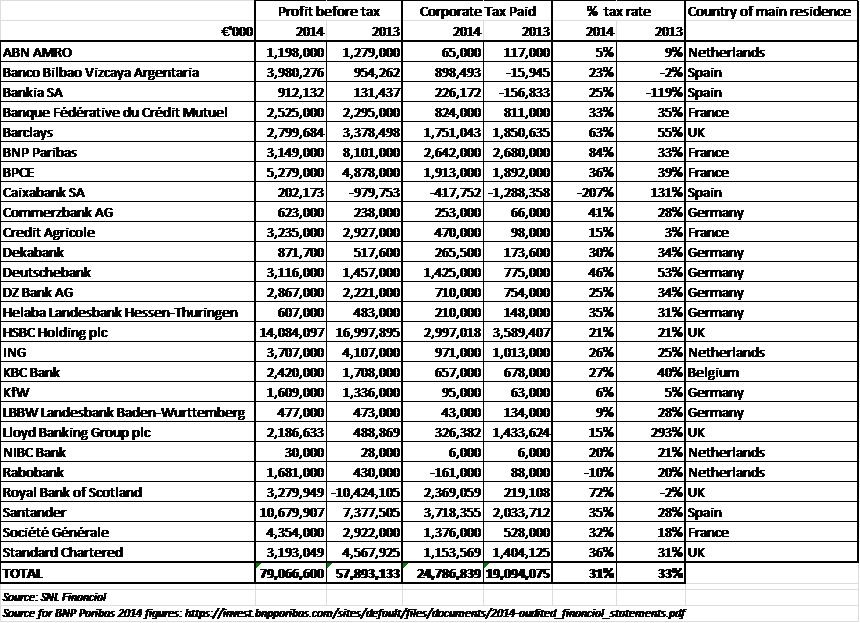

Building on the limited experience gained in 2015 with banks' CBCR, civil society sees CBCR as a useful tool to assess the alignment of profits with places of actual business activity, thus enabling e.g. NGOs to ask targeted questions to banks. Banks have confirmed that CBCR is indeed used as a tool by civil society, including NGOs, researchers and journalists. Even though disclosing 'commercially sensitive' information is a problem for businesses, banks tend to be less concerned by this than other industries. Nevertheless, a number of banks are anxious of the risks of tax disputes arising from CBCR and urge for more to be done to improve dispute resolution mechanisms. Banks report that the first year of public CBCR (2015) entailed no noticeable effect in terms of tax planning, investment or strategies. A survey commissioned by Members of the European Parliament on the basis of the 2015 CBCR of 26 banks points to indicators of artificial profit shifting in the banking sector. A key assumption of this analysis is to determine which countries are tax havens and in doing so better track any profit-shifting behaviour. The financial statements of the 26 banks surveyed yet show tax rates in the region of 30% overall, and no significant variation overall in that rate from 2013 to 2014. Banks, and surveys all point to technical difficulties leading to inconsistent implementation of CBCR by banks, despite the constructive work done by the European Banking Authority and the European Commission to overcome these difficulties.

2.4Problem definition

2.4.1 Drivers

Taxation is at the core of countries' sovereignty, yet it is becoming increasingly difficult for Member States to protect their tax base. Domestic rules cannot be fully effective given the cross-border dimension of many tax planning structures and the use of arrangements which enable the relocation of tax base to another jurisdiction within or outside the Union. In addition, relying on unilateral and domestic measures may fragment the Single Market. The interaction of 28 national corporate tax systems offers, by their very heterogeneity, opportunities for aggressive tax planning.

On the other hand, tax competition exists to encourage the inflow of productive resources and to prevent capital flight.

Moreover, the globalisation of the economy has made the corporate structure of multinational companies more complex and more difficult to understand given the number of entities and ownerships in different countries. Globalisation and the digitalization of the economy pose specific challenges for ensuring taxes are paid where economic activity actually takes place. Some companies exploit the fact that corporate tax rules have not kept up with our globalised and digital economy. Companies are incentivized by their shareholders to reduce costs where this includes the taxes paid by companies.

2.4.2The problem identified

An environment of complex tax rules, fiscal secrecy and non-cooperation between Member States in the context of globalisation and fast evolving business models allows MNEs to exploit legal loopholes in tax systems and discrepancies between national rules to reduce the amount of their corporate income tax. These shortcomings are exploited to a varying extent by a number of MNEs in a non-transparent manner. Although limited liability companies established or listed in the EEA must disclose information on CIT in their publically available financial statements, it is difficult for the public to obtain a full picture of companies' tax strategies in this area.

The international community strives to improve the current setting through consensus. The OECD/BEPS initiative endorsed by the G20 (and implemented in the EU by the ATAP) proposes the disclosure of CBCR information. It is however limited towards tax authorities, recognising at the same time the need to maintain appropriate safeguards and to protect the confidentiality of taxpayer information. The CBCR requirements proposed in the ATAP is a tool that is expected to trigger more and better tax audits with the effect of ensuring further compliance of MNEs with national tax laws, depending on each tax authority. However tax authorities may face some limits given that MNEs can afford an array of non-abusive tax avoidance practices which are not illegal, yet are questionable.

This non-transparency will allow some companies to engage in tax planning strategies which are not in line with their corporate responsibilities and which, if they were known by the public (consumer, investor, civil society…), would often not be accepted. Furthermore, this opacity does not allow for a proper assessment of the roots and consequences of this situation which therefore provides little room for informed democratic debates on how to prevent mismatches, loopholes and harmful tax measures upon which such strategies can flourish.

The problem identified is the lack of public scrutiny on Member States and MNEs as regards corporate income tax, due to the absence of broadly accessible information. Public scrutiny could be an additional tool enabling to fight base erosion and profit shifting, building on reputational effects and democratic debates.

Figure 1: Problem definition

2.4.3Direct consequences

Aggressive tax planning by enterprises is a direct consequence. It is defined as taking advantage of the technicalities of a tax system or of mismatches between two or more tax systems for the purpose of reducing tax liability. Aggressive tax planning can take a multitude of forms. Its consequences include double deductions (e.g. the same loss is deducted both in the state of source and residence) and double non-taxation (e.g. income which is not taxed in the source state is exempt in the state of residence). Aggressive tax planning is a major concern in the EU as it leads to lost tax revenues for countries. It is facilitated by a lack of transparency and public scrutiny, where in conjunction with harmful tax competition, this creates incentives for multi-national taxpayers to set up structures that channel taxable profits from high tax countries (where profits are originally generated) to low tax countries.

Taking into account a number of caveats, a study by the European Parliament Research Service (2015) estimates revenue losses at the EU level to be EUR 50-70 billion. A short overview on the estimation of corporate income tax gap is presented in Annex L, which explains the drawbacks and limitations of current estimations and methods used.

According to a recent study

, 70% of profit shifting is carried out through transfer pricing between different parts of a company and the intellectual property located in low tax countries.

A recent study on aggressive tax planning

identifies the seven most commonly used structures of aggressive tax planning and a series of tax provisions (or lack thereof) necessary for these structures to work. They include structures that rely on debt shifting, exploiting hybrid mismatches, location of intangible assets and IP, and partly strategic transfer pricing. Further explanations on profit shifting are provided in Annex U.

Potentially harmful tax measures

: Certain measures are targeted by Member States towards non-residents and provide them with more favourable tax treatment than what is generally available in the Member State concerned in order to attract investments. This may unduly distort the internal market.

2.4.4Indirect consequences

Public concern: Honest taxpayers (individuals and companies) have to shoulder a disproportionate amount of the tax burden. Because of this, they might loose trust in the tax system and become less inclined to abide by the rules. Recent reports on the past and present use of aggressive tax planning structures by certain multinational enterprises have led to public criticism and public dissatisfaction. Both NGOs and Member States have urged the European Institutions to reform the system governing corporate tax avoidance

. There is a perception of unfairness, i.e. that companies, and particularly multinationals, avoid contributing their fair share to the funding of public goods by artificially lowering their taxable income. According to a 2012 Eurobarometer

, 88% of the EU population support tighter measures against tax avoidance and tax havens.

Recent press reports on the current use of aggressive tax planning structures have also led to growing discontent. The widespread view that companies may not be paying their fair share of taxes is nurtured by the lack of public transparency on tax issues. Negative sentiment has been exacerbated in particular in countries that have had to achieve fiscal consolidation. Many citizens resent that companies avoid taxes while themselves are faced with higher tax burdens. Indeed, data shows that implicit tax rate on labour rose from 35% to 36% between 2009 and 2012 and the average standard VAT rate increased from 19.3% to 21.5% between 2000 and 2012. Citizens compare the mandatory increases in their taxes payments with allegations that some multinationals have managed to drastically reduce their effective tax rate

.

Lack of a level playing field for businesses: While some businesses engage in aggressive tax planning, others do not. This is particularly true of small and medium-sized enterprises (SMEs), both listed and non-listed. Companies with no cross-border activities (including SMEs) have often neither the means nor the possibilities to develop a tax optimization strategy at the international level. The consequence is a distortion of competition. According to various studies, a company with cross-border operations in the EU pays on average 30% less tax than a similar firm active in the same country with high CIT rate. Studies show that the level of internationalisation is correlated with the size of the firm. Because SMEs are more domestically-based relative to large companies, their aggressive tax planning possibilities are fewer.

The comparable disadvantage of competitors is further worsened when Member States impacted by aggressive tax planning are forced to shift to less mobile tax bases which affect national businesses, including SMEs. A lack of transparency exacerbates this as it increases the challenges Member States' face in re-establishing a level playing field.

Tax base erosion: The result of aggressive tax planning and harmful tax practices is that some countries' tax bases are expanded at the expense of others who might lose part of their tax bases. Similarly, at EU level, there will be a loss when such third countries are involved, and the tax base will shift outside the EU. From an EU point of view this jeopardizes the functioning of the Internal Market as well as the application of growth-friendly tax policies at the national level.

2.4.5Affected stakeholders

Member States/Tax administrations: Before the implementation of the BEPS 13 initiative, Member States’ tax administrations had insufficient information on companies' tax strategies. This lack of information has put them in a position where they are less able to defend their tax base. Attempts by tax administrations to improve tax collection resulted in higher administrative costs and the design of complex counter-measures (e.g. introduction of complex anti-abuse measures, or special tax regimes to incentivise firms to shift profits to their jurisdictions)

Businesses not applying aggressive tax planning techniques: The current system induces market distortion as the lack of transparency allows some multinational companies to reduce the amount of tax paid thanks to complex and non-transparent structures. This results in a competitive disadvantage for companies unwilling or unable to engage in aggressive tax planning. This is the case for the vast majority of companies (including SMEs) which may not have the means to engage in international tax planning techniques.

Citizens: Individual taxpayers are indirectly affected. Where a multinational enterprise that uses aggressive tax planning structures does not pay a proportionate share of taxes in the Member States where they are based, this affects the tax revenues of these Member States. In the context of tight fiscal policy and budget deficits, reduced taxes on companies forces governments to raise taxes on the least mobile tax bases, such as labour income.

Third countries: Third countries (except tax havens) are affected in a similar way to Member States. According to the International Monetary Fund (IMF)

, tax base spill-overs are particularly marked when it comes to developing countries.

2.5Baseline Scenario

The OECD BEPS Action Plan released in October 2015 and adopted by G20 in November 2015 does not constitute a legal requirement for member jurisdictions to implement. The OECD BEPS Project includes Action 13 that would encompass, for the purpose of improving risk management in the area of transfer pricing, the reporting of certain obligations by enterprises to tax authorities, including country-by-country reporting. However, not all EU Member States are members of the OECD. And due to national variations, consistent implementation within the EU may not be achieved. So far, a number of Member States have started to develop and adopt legislation in order to enable data collection and exchange within the time frame agreed at the OECD. The Commission is determined to facilitate the consistent implementation of BEPS 13 by all EU Member States. The recent Anti Avoidance Tax Package adopted on 27 January 2016 includes a legislative proposal for the implementation of BEPS 13 Action through an amendment of the Directive on Administrative Cooperation. In March 2016, the ECOFIN Council reached a political agreement on this proposal. As a result, MNE groups with a turnover above EUR 750 million will report to tax authorities on a country-by-country basis by 2017. Information reported to Member States' tax authorities will have to be exchanged between EU tax authorities, but should not be published.

BEPS Action 13 encompasses 2 elements: a) a filing obligation for companies of a defined set of information consisting of a master file, a local file and a country-by-country report to national tax administrations and b) an agreement between tax administrations to exchange the information (Multilateral Competent Authority Agreement (MCAA) on the exchange of country-by-country reports). The country-by-country reports shall be filed in the Member State of the tax residence of the ultimate parent entity and shared between Member States through the automatic exchange of information.

The ATAP provides tax authorities with data relating to transfer pricing risks and other BEPS related issues. The CBCR to be submitted to tax authorities by MNEs pursuant to the implementation of the ATAP, will assist them primarily in orienting their tax audits, and thus be instrumental in ensuring further compliance with their national tax legislation.

In the baseline scenario, there would be no specific initiative by the EU to introduce further public disclosure obligations for companies. The existing CBCR regimes in the Accounting Directive and the Capital Requirements Directive would remain in force so that public tax transparency would only be ensured for certain industries.

2.6The EU's right to act, subsidiarity check

2.6.1Subsidiarity

In an increasingly globally integrated economy, corporations have grown into entities that are freer from national contingencies and for which value chains are not necessarily regional matters. By contrast, tax policies and administration remain primarily a national responsibility. Due to the cross-border nature of many tax planning structures and transfer pricing arrangements, tax bases can be easily relocated by MNEs from one jurisdiction to another within or outside the Union. The international nature of tax planning suggests the need for multilateral and co-ordinated actions by countries hosting multinational firms. One of these actions, supported by the G20, consists of further transparency towards tax authorities.

This global issue is also relevant within the Single Market. The EU Single Market has provided extensive opportunities for businesses to locate their activities according to their needs. This freedom may have, to an extent, given rise to mismatches that require counter-measures, one of which possibly consists of further corporate tax transparency. National provisions in this area cannot be fully effective, as Member States in isolation will be ill-equipped to address cross-border issues.

EU action is therefore justified on the grounds of subsidiarity.

2.6.2International dimension

The G20 take up of this issue is a clear indication of a common international problem. As formulated in Article 21 of the Treaty on European Union, the EU should have regard to multilateral solutions. However, there is no international consensus on public corporate tax transparency.

2.6.3Legal base

This work has been undertaken to contribute to the Commission’s overall objective of ensuring that the country in which a business’ profits are generated is also the country of taxation. However, measures on corporate transparency on payment of taxes would have no direct effect on the taxation of companies: transparency is expected to only indirectly contribute to this overall objective. For this reason, measures on corporate tax transparency cannot be regarded as relating to fiscal provisions affecting the establishment or functioning of the internal market in the sense of Article 115 TFEU. Therefore, there would be no need to have recourse to Article 115 TFEU as a legal basis.

Article 50, paragraph 1 TFEU, and paragraph 2, sub-paragraph (g) (ordinary legislative procedure) provides powers for adopting Directives in order to regulate the freedom of establishment, in particular by coordinating to the necessary extent the safeguards which, for the protection of interests of members and others, are required by Member States of companies and firms with a view to making such safeguards equivalent throughout the Union. According to case law (C-97/96), Article 50 TFEU has a broad application and may be applied not only for the protection of the creditors of the company but also in order to protect other interests. Therefore, Article 50 TFEU may serve as a legal basis for the initiative on tax transparency. It seems feasible to include ancillary reporting obligations for companies into the existing regimes on reporting in the Accounting Directive, an approach which would facilitate the implementation and application of the rules by the companies.

As an alternative, the adoption of measures on reporting on taxes may be based on Article 114, paragraph 1, TFEU (ordinary legislative procedure) concerning the functioning of the internal market. However, recourse to article 114 TFEU as a legal basis requires that the measures would harmonise existing national rules of the Member States in this field and that the reporting on taxes would have a direct effect on the functioning of the internal market. Article 50 TFEU and Article 114 TFEU are non-mutually exclusive legal bases and may therefore be combined.

A final assessment of the question of the legal basis should be decided on the basis of the objectives and content of a draft proposal.

3Objectives

The issue identified is a lack of public scrutiny. The specific objective is therefore to increase corporate tax transparency, i.e. to make broadly accessible information on corporate income tax to the public including shareholders. If an option is effective in achieving this end, the behavioural responses of companies and Member States will contribute to meeting the broader objectives listed below:

1.To geographically align corporate income taxes paid by MNEs with actual profits. In summary, that: enterprises should pay tax where they actually make profit;

2.To enhance the responsibility perceived by corporates to contribute to local welfare by paying taxes, and thus spread responsible practices on tax as part of corporate social responsibility. In summary: to foster corporate responsibility to contribute to welfare through taxes;

3.Through an informed democratic debate, contribute to remedy the lack of level playing field between businesses in the EU resulting from MNEs’ comparative advantage in having the capacity to exploit tax regimes for the purpose of tax planning – building on a potentially harmful combination of those regimes. In summary: fairer tax competition in the EU through democratic debate.

4Policy Options

4.1Preliminary approach on the definition of options

4.1.1Content of the information that should be disclosed

The type of information to be disclosed should be related to corporate income taxes. This information should help demonstrate that the country in which profits are actually made corresponds to the country of taxation. Country-by-country reporting is therefore the most appropriate approach.

Basic information

The annual corporate income tax accrued is the key information. It corresponds to the amount of corporate income tax expense shown in the profit and loss statement. To build disclosure on tax accrued offers the following benefits: (i) it is easy for MNEs to obtain and compute this information internally as it already appears in the income statements of entities comprised in the consolidated financial statements; (ii) the amount of tax can be consistent with the state of affairs reported overall by the MNE in its financial statements; (iii) the amount of tax accrued is consistent across an MNE group if based on the group's GAAP, and therefore consistent on a country-by-country basis.

The amount of tax paid was reported by many during the consultation stage as equally necessary information enabling to ensure that income taxes accrued are actually paid by companies. Indeed, due to timing differences, a company may in some instances pay taxes only years after accrual in the financial statements, or even never at an extreme. Information on tax paid tends to be costlier to collect and more prone to misinterpretation than tax accrued. This is due to the following reasons: (i) tax payments depend heavily on local tax regulations, which vary from one jurisdiction to another; (ii) tax payments are often inconsistent with tax accruals in the financial statements; and (iii) as it is cash based (whereas financial statements are accruals based), the collection and preparation of information on taxes paid are generally less readily available in a company's systems.

Contextual information

As explained in Annex K, contextual information is useful for analysing more precisely the fundamental information (income tax). In combination, contextual information is useful for instance to apportion the total profits of a given MNE per geographic region, hence enabling a benchmark with which to compare profits actually reported per region in the CBCR. Likewise, the tax amounts can be reported to profits in order to establish a comparison per jurisdiction between the statutory tax rate and the effective tax rate.

Some of the contextual information may be considered by businesses to be commercially sensitive either in isolation, or because the combination of those can deliver information to any party for other purposes than assessing tax amounts. Moreover, certain contextual information may be prone to misinterpretation. For this reason, the case for disclosing information other than income tax accrued needs to be filtered against criteria relating to the relevance of the information to the objective, as well as its proportionality. These aspects have inter alia regards to information that very large MNEs worldwide will prepare in any event as a result of the international implementation of the OECD BEPS plan endorsed by the G20 and at EU level for the purpose of fighting tax avoidance. Other criteria have to do with the fact that information is made public, including the sensitivity of information as regards competitiveness, and risks associated with potential misinterpretation of the information by the readers. Table 1 below summarises findings based on the above approach.

Based on this exercise, the following information can reasonably be envisaged to be given per country: location (country name), description of the nature of activities per country, turnover (total including sales with related parties), profit or loss before tax, income tax accrued, income tax paid and the number of employees.

Two possibilities are envisaged: sub-Option (i) would require companies to report, besides the location (country) and a description of the nature of activities in that country, the income tax accrued and income tax paid (essential information). Sub-Option (ii) would require companies to report in addition to (i): Net turnover, Profit before tax, Number of employees.

Table 1: Analysis of the information to be disclosed in a CBCR

|

Item

|

Availability

|

Relevance to the objectives

|

Competi-tiveness risks

|

Mis- interpretation risks58

|

Overall assessment of risks of disclosure

|

Informa-tion retained disclo-sure

|

|

|

BEPS 13

|

CRD4

|

GAAP

consolidated

|

|

|

|

|

|

|

Name

|

YES

|

"name(s)"

|

YES

|

HIGH

|

MEDIUM

|

LOW

|

MEDIUM

|

YES

|

|

Location (country)

|

YES

|

YES

|

YES

|

HIGH

|

LOW

|

LOW

|

LOW

|

YES

|

|

Nature of activities

|

YES

|

YES

|

YES

|

HIGH

|

LOW

|

LOW

|

LOW

|

YES

|

|

Net Turnover (total)

|

YES

|

"Turnover"

|

YES

|

HIGH

|

HIGH

|

LOW

|

MEDIUM

|

YES

|

|

Turnover solely with related parties

|

YES

|

-

|

NO

|

HIGH

|

HIGH

|

HIGH

|

HIGH

|

NO

|

|

Purchases

|

-

|

-

|

YES

|

LOW

|

HIGH

|

LOW

|

HIGH

|

NO

|

|

Number of employees

|

YES

|

YES

|

YES

|

HIGH

|

MEDIUM

|

MEDIUM

|

MEDIUM

|

YES

|

|

Profit or Loss Before Tax

|

YES

|

YES

|

YES

|

HIGH

|

HIGH

|

LOW

|

MEDIUM

|

YES

|

|

Income tax accrued (current)

|

YES

|

"Tax on P&L"

|

YES

|

HIGH

|

LOW

|

LOW

|

LOW

|

YES

|

|

Income tax accrued (deferred)

|

NO

|

"Tax on P&L"

|

YES (IFRS)

|

MEDIUM

|

LOW

|

HIGH

|

MEDIUM

|

NO

|

|

Income tax paid

|

YES

|

"Tax on P&L"

|

YES (IFRS)

|

HIGH

|

LOW

|

HIGH

|

MEDIUM

|

YES

|

|

Stated Capital

|

YES

|

-

|

YES

|

LOW

|

MEDIUM

|

HIGH

|

HIGH

|

NO

|

|

Accumulated earnings

|

YES

|

-

|

YES

|

LOW

|

MEDIUM

|

HIGH

|

HIGH

|

NO

|

|

Tangible assets

|

YES

|

-

|

YES

|

MEDIUM

|

HIGH

|

HIGH

|

HIGH

|

NO

|

|

List of subsidiaries of the parent enterprise operating in each country

|

YES

|

-

|

YES

|

MEDIUM

|

MEDIUM

|

LOW

|

MEDIUM

|

NO

|

|

Public subsidies received

|

-

|

YES

|

-

|

LOW

|

MEDIUM

|

HIGH

|

HIGH

|

NO

|

|

Tax rulings

|

-

|

-

|

-

|

MEDIUM

|

HIGH

|

HIGH

|

HIGH

|

NO

|

|

Employees working through subcontractors

|

-

|

-

|

-

|

LOW

|

MEDIUM

|

HIGH

|

HIGH

|

NO

|

|

Pecuniary tax-related penalties administered by a country

|

-

|

-

|

-

|

LOW

|

MEDIUM

|

HIGH

|

HIGH

|

NO

|

|

Narratives explaining tax-related information

|

YES

|

-

|

-

|

HIGH

|

LOW

|

LOW

|

LOW

|

YES

|

4.1.2Transparency: provided by whom?

In case of public disclosure, the information could be provided directly by either companies, tax administrations or both. Tax administrations are the primary recipients of corporate tax information. However, the onus of preparation will in any case fall on companies, and tax administrations are bound by international treaties and conventions regarding the use and confidentiality of tax related information. There was limited support in the public consultation for a solution whereby tax authorities would deliver information to the public on taxes paid by companies. It should therefore be for companies to directly inform the public.

4.1.3Which companies should be in the scope of a potential initiative

A first alternative is to build on the OECD approach to cover only very large MNE groups (with turnover >EUR 750 million), i.e. at least 6,500 MNE groups. About 1,900 (lower bound estimate) of these are EU MNE groups. Table 2 provides a breakdown of MNE Groups for the largest economies/regions.

Table 2: Number of very large MNE groups

|

Country/Region

|

Total number of MNE groups

|

|

EU & EEA

|

1881

|

|

USA

|

1549

|

|

Japan

|

746

|

|

China

|

709

|

The OECD approach offers a number of benefits. First, the OECD threshold has been designed to capture 90% of the MNEs global revenues, whereas only 10-15% of those would be required to submit a CBCR. Secondly, there would thus be no additional administrative burden for those companies to comply with an EU obligation to publish a CBCR as it is assumed that they would already be submitting similar information to their respective tax authorities if, as recommended by the G20 and the OECD, countries do implement the BEPS actions. Thirdly, the EU initiative would remain consistent with the international approach. Finally, only top tier companies which, due to their size and complexity, are the best equipped to engage in tax planning, would be covered. It is worth noting for instance that the MNE groups testifying to the TAXE committee of the European Parliament in 2015 would all be included under this threshold.

A second alternative would be to capture the parent companies of 'large groups' as defined in the Accounting Directive (Article 3). Large groups exceed at least two of the following three criteria applied to the consolidated balance sheet of the parent entity: (a) balance sheet totalling EUR 20 million, (b) net turnover: EUR 40 million, (c) average number of employees during the financial year: 250. This would involve at least 20,000 EU groups. This threshold was in the CBCR amendment introduced in July 2015 by the European Parliament in its report on the Commission proposal for the revision of the Shareholder Rights Directive in July, building on existing definitions in EU acquis. Whereas this alternative would cover a significantly higher number of companies, the additional benefits may be more limited as this will have an impact on companies which may not have multinational operations, and are less able to engage in aggressive tax planning.

A third alternative would be to cover issuers of securities admitted to trading on a regulated market in the EU. This would cover around 8,500 companies, SMEs included, which have voluntarily decided to get public funding. However, such an approach would not be consistent with the objectives of the initiative as the problem defined is not one in connection with a funding decision of a company, but one in connection with the operations of companies in the EU single market. This alternative would also mean covering listed SMEs for which this transparency requirement would generate considerable administrative burden and discourage them from going public. This approach is therefore not considered.

A fourth alternative would be to cover large public-interest entities. Public interest entities are defined by the Accounting Directive as undertakings which are (a) governed by the law of a Member State and whose transferable securities are admitted to trading on a regulated market of any Member State; (b) credit institutions as defined in Article 4 of Directive 2006/48/EC; (c) insurance undertakings within the meaning of Article 2(1) of Council Directive 91/674/EEC; (d) designated by Member States as public-interest entities. For the purposes of non-financial reporting the additional criterion of more than 500 employees applies. Under this alternative, the measure would concern around at least 7,500 public-interest entities in the EU. Despite the public-interest element, this alternative would not be appropriate if the objective is to ensure a cross-sectorial level playing field, i.e. not focused on specific sectors or sources of funding.

The first and second alternatives will therefore be considered in the design of options focusing on EU MNE groups. Sub-Option (a) would cover large EU MNE groups (at least 20,000 EU groups), sub-Option (b) would cover very large EU MNE groups (at least 1,900 EU groups). Should a global approach covering EU and non-EU MNE groups be retained, only the first alternative can be considered as proportionate and consistent on the global scene, building on a widespread implementation of the OECD BEPS actions by countries.

Establishment in the EU should be based on the EU approach defined by the EU legislation, in particular the Treaty on the Functioning of the EU, as opposed to concepts such as "permanent establishment" used for tax purposes. The policy should focus on establishments commonly used by MNEs, that is branches, subsidiaries, companies and firms.

The concept of "permanent establishment" would not be used to identify the reporting entities. This is a tax concept, which builds on international consensus, but which is not clearly defined in EU law. It is mainly enforced by national tax authorities. As a result, an entity may have no certainty whether it is a permanent establishment or not. This would imply significant issues on the scope of the CBCR as well on the enforcement of such policy. On the contrary, an approach based on company law would ensure legal certainty and clarity. In addition, the coverage of reporting entities based company law (targeting companies, subsidiaries and branches) can be functionality similar to a system building on the tax concept of a permanent establishment.

4.1.4Labelling system

It is worth examining labelling systems as an option given the array of private initiatives that have flourished lately. The European Parliament has shown support for a voluntary European 'Fair Tax Payer' label, as a 'soft measure' to promote tax compliance.

A labelling system could offer benefits. Such a system could prima facie bring about similar benefits to current private initiatives with the benefits of harmonisation and greater trust at EU level. Companies wishing to indicate they are fully tax compliant would be encouraged to act accordingly. A through description of a possible EU labelling system is given in Annex R.

This option is however discarded for two main reasons: first, there are more chances to reach the objectives with a mandatory reporting regime than with a regime with which only willing companies will adhere to. For instance, after a few years of existence, the Fair Tax mark in the UK attracted 17 companies, of which one is in the FTSE 100 and one in the FTSE 250. Those figures might however increase due to further incentive that will arise with the implementation of the BEPS/ATAP initiative.Second, if used as a complement to an obligation to disclose publicly it would be pointless to require at the same time companies to provide a public CBCR and to promote a voluntary labelling system, should they have the same features. A differentiation may be relevant on the condition that each system pursues different objectives. This cannot be the case with this initiative which pursues a single specific objective.

The potential for added value of labelling systems based on market initiatives will remain however, especially for businesses outside the scope of an EU mandatory reporting regime, with a view to pursue additional objectives, or for other reasons determined by the markets.

4.1.5Publication

A CBCR may be part of the management report, of the financial statements (a note), or be a separate report. Much would depend on the intended users as well as publication timeline and channels. As no clear driver has ben identified to constrain those features,.flexibility could be offered to companies to have a separate report or to accompany their financial / non-financial reporting. This model has been retained for the sectoral CBCRs. To ensure certainty and availability over time, the publication of tax-related information should be filed in a register managed by Member States, as is currently the case for the sectoral CBCRs.

Digitalised reporting by companies could facilitate access and processing by any party (civil society, tax authorities; investors…). For this reason, it should be envisaged that CBCR be published as well on each MNE's website, however not imposing a particular format or language.

4.1.6Enforcement and Audit

There appears to be no need for deep enforcement measures as the aim is primarily to increase public awareness of an MNE's tax affairs, that is, for indicative purposes. For very large MNEs, a public CBCR will necessarily contain information that is consistent with their CBCR submitted to tax authorities. Even though the OECD model requires no specific reconciliation of the data with e.g. the financial statements, submission to tax authorities will offer guarantees on the enforcement, consistency and accuracy of data in a public CBCR. If, as proposed, CBCR are filed with business registers and on the MNE's web sites for the purpose of publication, this will enable further enforcement by competent authorities as well as enable the public at large to trace non-compliance cases. Finally, a system of appropriate penalties should be devised. For these reasons, it may not be commensurate to specifically require e.g. an audit, but it could be envisaged to have light-touch involvement of an MNE's auditor.

4.1.7Link with the existing CBCR requirements for banks and extractive industries

Based on an analysis in Annex P, it appears that the EU could mandate the publication of a CBCR by all industry sectors, including to extractive and logging industries. This is supported by the fact that the objectives, content and scope of this sectorial CBCR differ considerably from the general CBCR sought in this document, and hence the objectives would not be fulfilled by the sectoral CBCR. Part of these industries would be subject to both public CBCR regimes, but this would cause no major problems.

EU credit institutions and investment firms must publish as from 2015 a sectorial "bank" CBCR pursuant to Article 89 of the CRD4. There is an apparent similarity between that regime and a general regime in terms of data to be reported. However there are likely to be a few differences in the details. An important question is whether the existing "bank" CBCR should continue to apply or not following the adoption of the new "general" CBCR regime. As explained in Annex P, if the existing "bank" CBCR would cease to apply, significantly less banks would fall under the CBCR reporting requirement. Such limitation of the scope of application does not seem justified given the specific objective of the "bank" CBCR which is to regain trust in the financial sector. The "bank" CBCR regime should therefore remain in force. To avoid a possible double CBCR reporting obligation for those banks that fall within the scope of application of both regimes, it seems appropriate to exclude from the scope of application of the new regime EU banks that report CBCR on the basis of Article 89 of CRD4. In this setting, non-EU MNE banking groups should not be excluded from the new "general" regime given that under CRD4, they are only required to report CBCR for a small part of their group (namely for the EU controlled operations).

4.2Option 1 - Baseline Scenario

As mentioned in Section 2.4, the country-by-country reporting to tax authorities will be made compulsory for very large MNEs in the EU, in line with the BEPS 13 Action. The Anti-Tax Avoidance Package adopted by the Commission in January will provide the necessary framework for all EU Member States to implement the OECD requirements in the most consistent way. Ultimately this will drive the overall framework of transfer pricing documentation, of which CBCR is a key component.

4.3Option 2 – Public CBCR on EU controlled operations

In this scenario, the ultimate parent of a MNE group, insofar that parent is established in the EU would have to publish tax-related information on a country-by-country basis on the operations it controls. Likewise, the reporting would have to be done by any intermediate parent(s) established in the EU that is ultimately controlled by a non-EU MNE group.

In order to avoid undue administrative burden, any undertaking in the EU could be exempted from such obligation where an intermediate or ultimate parent company would include its own information in a consolidated report. In order for subsidiaries/branches of non-EU MNEs to enter in the scope of a possible EU initiative, the defined scope would be preferably set by reference to the turnover determined at the level of ultimate parent companies, thus ensuring that subsidiaries and branches of any size have the reporting obligation in the first place, before any application of exemptions.

Two sub-Options are envisaged:

4.3.1Option 2A: Public CBCR on EU controlled operations broken down by EU Member State and aggregated for non-EU operations

EU MNEs would have to report publicly the breakdown of tax related information on a country-by-country basis. The information would be itemised on a country-by-country basis as regards operations made in the Member States, and aggregated as regards activities outside the European Union. Aggregated means that for each caption (tax amount, turnover, number of employees, etc…), the MNE would add up the figures relating to its operations in each third country, thus publishing a single aggregated amount per caption relating to its non-EU operations.

4.3.2Option 2B: Public CBCR on EU controlled operations broken down by Member State and third country

The EU would require EU MNE groups to publically disclose tax-related information on a country-by-country basis for all their operations.

4.4Option 3 – Public CBCR on worldwide operations

In this scenario, the CBCR would be published by the ultimate parent of a EU MNE group, insofar that parent is established in the EU. The non-EU ultimate parent (established in a third country) of a non-EU MNE group would see the obligation fall on its subsidiaries/branches in the EU to publish that ultimate parent's CBCR. On both accounts, the obligation would arise where the ultimate parent's turnover exceeds EUR 750 million. This would cover at least 6,500 MNE groups representing more than 90% of the MNEs' global turnover (EU and non-EU). It is estimated that a maximum of 10% (and probably even less) of the very large MNEs worldwide have no subsidiaries in the EU. This does not preclude that some of these may operate through branches in the EU, though, and option 3 would seek to capture them as well in order to avoid loopholes.

The Option would impose on the subsidiaries/branches in the EU of a non EU MNE a duty to publish the consolidated CBCR of their ultimate parent company. Certain mechanisms could be designed to mitigate or avoid the unnecessary duplication of requirements. For instance, to address branches tend to be necessary only in the cases where a non-EU MNE would operate solely through branches in the EU.

In order to avoid undue burden, yet remain effective, it should be envisaged that only medium-sized and large EU entities (subsidiaries and branches) of a non-EU MNE group have the above obligation.

This takes account of the current situation in the EU, as described in Annex D: small subsidiaries of a non-EU MNE group have currently no obligation to identify their ultimate parent, whereas medium-sized and large already have this obligation (Accounting Directive). The efficiency of this filter is ensured by the relative size of the turnover of MNEs covered (> EUR 750 million) which warrant that generally at least one subsidiary will exceed the thresholds to be regarded as medium-sized (EUR 8 million as per the Accounting Directive). A clause in the policy could be envisaged to avoid abuses of this setting. Besides, a branch opened in a Member State by a company which is not governed by the law of a Member State shall file the financial statements of that company in the relevant business register of a Member State. That branch is generally considered to be a permanent establishment for tax purposes in the country. Possible ways to address only branches of a comparable size could have regards to their turnover of the size of the company that opened the branch.

With this setting, in any event, the operations of all subsidiaries and branches, disrespect of their size, would be consolidated by the parent in its CBCR.

The enforcement of Option 3 on non-EU MNEs would undoubtedly be more challenging than on EU MNEs.

Two sub-Options are envisaged:

4.4.1Option 3A: Public CBCR on worldwide operations broken down by EU Member State and aggregated for non-EU operations.

This scenario would require all very large ultimate parent MNE groups with a medium-sized or larger subsidiary/branch in the EU to disclose publicly tax-related information on a country-by-country basis on their EU operations. This information would be aggregated in third-countries.

4.4.2Option 3B: Public CBCR on worldwide operations broken down by Member State and third country

It would require that all very large ultimate parent MNE groups with a medium-sized or larger subsidiary/branch in the EU disclose tax-related information on a country-by-country basis on all their operations (no aggregation).

4.5Summary of the Options

Table 3: Summary of the Options

|

|

OPTIONS

|

Type of transparency

|

Who should do it?

|

Information covered

|

Granularity of the reporting

|

Legal basis

|

|

|

Option 1:

Status quo: implementation of BEPS 13

|

Transparency towards tax administrations on a country-by-country basis

|

Very large companies of EU Member States + G20/OECD countries

|

BEPS 13 information

|

All countries covered

|

/

|

|

EU

CONTROL L

E

D

OPERAT I

ONS

|

Option 2A:

Public CBCR on EU controlled operations broken down by EU Member State and aggregated for non-EU operations

|

Transparency towards the public on a country-by-country basis

|

Sub-Option (a):

Large EU parent companies

Sub-Option (b): Very large EU parent companies.

|

Sub-Option (i):

- Income tax accrued

- Income tax paid

Sub-Option (ii):

- Income tax accrued

- Income tax paid

- Turnover

- Profit before tax

- Number of employee

|

Split information on EU controlled operations by EU MS and report aggregated figure for the rest of the world.

|

Art

114/

50 TFEU

|

|

|

Option 2B:

Public CBCR on EU controlled operations broken down by Member State and third country

|

Transparency towards the public on a country-by-country basis

|

Sub-Option (a):

Large EU parent companies

Sub-Option (b): Very large EU parent companies.

|

Sub-Option (i):

- Income tax accrued

- Income tax paid

Sub-Option (ii):

- Income tax accrued

- Income tax paid

- Turnover

- Profit before tax

- Number of employee

|

Split information by country on all operations controlled from the EU.

|

Art

114/

50 TFEU

|

|

GLOBAL

OPERAT

I

ONS

|

Option 3A:

Public CBCR on worldwide operations broken down by EU Member State and aggregated for non-EU operations

|

Transparency towards the public on a country-by-country basis

|

Very large parent companies with a subsidiary/ branch in the EU.

|

Sub-Option (i):

- Income tax accrued

- Income tax paid

Sub-Option (ii):

- Income tax accrued

- Income tax paid

- Turnover

- Profit before tax

- Number of employee

|

Split information on all operations of the ultimate parent company by EU MS and report aggregated figure for the rest of the world.

|

Art 114/

50 TFEU

|

|

|

Option 3B:

Public CBCR on worldwide operations broken down by Member State and third country

|

Transparency towards the public on a country-by-country basis

|

Very large parent companies with a subsidiary/ branch in the EU.

|

Sub-Option (i):

- Income tax accrued

- Income tax paid

Sub-Option (ii):

- Income tax accrued

- Income tax paid

- Turnover

- Profit before tax

- Number of employee

|

Split information by country on all operations of the ultimate parent company

|

Art 114/

50 TFEU

|

5Analysis of Impacts

5.1Economic impacts

5.1.1Impact on Growth and Jobs

Regarding the impact of increased corporate tax transparency on productivity growth, the analysis is based on the assumption that further tax transparency will, on average, increase substantially corporate income tax revenue. If this is the case, the overall impact on productivity growth will depend on the use of the extra revenue. If the additional tax revenue were used to ensure and potentially increase the provision of public infrastructure and/or policies and institutions that increase the productivity of capital this would be expected to have a positive impact on growth and employment. Alternatively, those Member States facing an increase in corporate income tax revenue could apply a tax shift approach where the fiscal pressure on labour is reduced in a revenue-neutral manner.

Under competitive market conditions, increasing fiscal pressure at the level of the firm may impact investment decisions as, at least in the short run, a lower level of investment may be a feasible option for the firm to protect its profitability (share dividend). Alternatively, firms may choose to increase their financial leverage sufficiently as to restore the previously prevailing level of distributed profits. In the worst case, the economy goes to a new situation where firms have reduced their average investment spending and at the same time increased their financial leverage. Obviously, this scenario hinges on the assumption of a competitive market environment; it should not be taken for granted in the case of industries characterized by super-normal profits/economic rents, and/or high implicit subsidies (e.g. banking).

Otherwise, based on the findings in the economics and corporate finance literature, the impact of higher transparency on firms' behaviour seems to depend to a large degree on the power relations between firms’ management and its shareholders, and there more precisely on shareholder structure. In principle, shareholders’ bargaining power vis-à-vis the firm’s management is presumed to increase with additional public transparency. However, according to the findings in the literature, the impact on firm behaviour of such a reduction in the informational asymmetry between management and shareholders is ambiguous. The academic literature has in particular identified two main channels: first, in firms where shareholders have strong influence on management decisions, there is statistical evidence that shareholders positively sanctioned additional effort on behalf of the management to lower the firm's fiscal pressure; the literature explains this with shareholders' expectation to capture a large part of the resulting increase in distributed profits. In contrast, in more opaque firms, no such positive sanctioning was identified. Second, in firms where the shareholder base is characterized by large (institutional) shareholders with (nominal) short-term revenue objectives, the firm may face higher pressure to “eat up” its capital stock in order to protect the level of distributed profits. In cases where both circumstances are united, and despite this pressure an increase in transparency that could motivate a continuation of aggressive tax planning behaviour of firms, as well as sub-optimal (from a growth and employment perspective) firm responses in terms of investment and financial leverage. Nevertheless, an increased public scrutiny would make it less likely that in extremis this could then result in lower levels of investment, employment, and growth of the economies these firms are operating in. Where such circumstances do not apply, based on findings in the relevant literature, one would not expect significant and lasting changes in firm behaviour after the increased public transparency, while in the short run an increase in financial leverage could signal either strategic profit stabilization by the firm, or improved access to external funding, or both.

Whereas, based on this analysis overall outcome on growth and jobs is uncertain, a fairer distribution of fiscal pressure across the size spectrum could further SMEs' capacity to support growth and job creation, and could further market entry, competition, and innovation. It could for instance certainly be more rewarding and motivating for start-ups to no longer face the stark contrast in effective tax rates compared to well-established incumbents, and certainly corporate income taxation should not, as it seems to do currently, give incumbents further means to protect their market against new entrants.

5.1.2Impact on Market efficiency

5.1.2.1Threshold effects

For some of the large, or very large MNE groups that come just marginally under the scope of a public CBCR scheme there could emerge a trade-off between firm size and corporate disclosure, and for some firms facing this trade-off it may become more attractive to scale down sufficiently to remain outside the scope of the CBCR requirement. Given the high threshold defined by the OECD/BEPS initiative (EUR 750 million annual turnover), while the decision to remain below the threshold could be relevant from the firm’s point of view, e.g. to avoid reputational risk attached to public CBCR, it is not expected to be harmful from the perspective of optimal firm size. However, this benign assessment cannot be made with the same level of reassurance in the case of the lower threshold that applies in the option of public CBCR for large MNEs. A negative (growth-adverse) threshold effect could potentially materialize were firms to limit their growth in order to remain outside of the public CBCR scope, and where such behaviour resulted in a sub-optimal firm size in a specific sector.

5.1.2.2 Impact on cost of capital

A traditional argument calling for more public transparency is that it helps firms gain access to sources of finance and as a consequence reduces firms’ cost of capital. According to this line of reasoning firms could (i) benefit from more competition among potential lenders, (ii) broaden the investor base, (iii) lower the cost of credit and improve access to external finance more broadly. This can be expected to produce benefits in particular for private firms falling under the scope, i.e. private firms’ access to finance could improve relative to public firms. However, given that public transparency will increase for all firms entering into the scope of the initiative simultaneously, the measure cannot be expected to improve any given firm's visibility relative to other firms entering the scope of the requirement.

5.1.2.3Impact on market monitoring

Another possible consequence is the intensification of market monitoring. Indeed increased transparency about the geographical complexity of MNEs could expose managerial decisions to increased market scrutiny, e.g. on behalf of investment fund managers. This may incentivize managers to optimize the structure of their firms and better align the incentives of both managers and shareholders. However, in the case where shareholders have strong influence on management decisions, investors could exploit this additional monitoring power over managers. As a result depending on the investor interest it may increase or decrease incentive to reduce tax costs.

5.1.2.4Impact on organisational efficiency

Increased transparency could help reduce costly and management failure-prone complexity especially in the case of very large MNEs. Long-term oriented shareholders are more likely to be critical about highly aggressive tax avoidance practices. To the extent that these practices require highly complex corporate structure; the latter could lead to excessive costs of complexity as well as additional reputational risks.

5.1.3Impact in terms of level playing field

Impact in terms of level playing field could differ widely depending on the options analysed. Within the public consultation, the business respondents have emphasised the need to achieve a level playing field in terms of reporting requirement.

5.1.3.1Level playing field in terms of size – Implication for SMEs

Studies have shown that in the case of high CIT jurisdictions a cross-border company pays on average 30% less tax than a company active in only one country. The additional transparency requirement would be imposed only on large or very large companies, and would therefore avoid administrative burden on smaller companies (SME). This difference is justified as smaller companies have typically less capabilities to shift profit and erode tax bases as they have less financial means and operate in fewer jurisdictions. Hence the disclosure would help to mitigate this issue. The MNEs that are not very large that will not have this disclosure obligation should potentially keep an advantage over the larger ones, at the expense of SMEs. This risk seems acceptable since they represent only 10% of the total activities of MNEs.

5.1.3.2Level playing field between EU and third country companies