EUROPEAN COMMISSION

EUROPEAN COMMISSION

Brussels, 30.11.2016

SWD(2016) 410 final

COMMISSION STAFF WORKING DOCUMENT

IMPACT ASSESSMENT

Accompanying the document

Proposal for a Directive of the European Parliament and of the Council on common rules for the internal market in electricity (recast)

Proposal for a Regulation of the European Parliament and of the Council on the electricity market (recast)

Proposal for a Regulation of the European Parliament and of the Council establishing a European Union Agency for the Cooperation of Energy Regulators (recast)

Proposal for a Regulation of the European Parliament and of the Council on risk preparedness in the electricity sector

{COM(2016) 861 final}

{SWD(2016) 411 final}

{SWD(2016) 412 final}

{SWD(2016) 413 final}

Abstract of the Impact Assessment of the Market Design Initiative

I.

POLICY CONTEXT AND KEY CHALLENGES

The Energy Union framework strategy puts forward a vision of an energy market 'with citizens at its core, where citizens take ownership of the energy transition, benefit from new technologies to reduce their bills, participate actively in the market, and where vulnerable consumers are protected'.

Well-functioning energy markets that ensure secure and sustainable energy supplies at competitive prices are essential for achieving growth and consumer welfare in the European Union and hence are at the heart of EU energy policy.

To live up to this vision, a series of legislative proposals have been prepared, following the objectives of secure and competitive energy supplies and building on the EU's 2030 climate commitments reconfirmed in Paris last year.

The electricity sector will be one of the main contributors to decarbonise the economy. Currently, 27.5% of Europe's electricity is produced using renewable energy and the modelling shows that close to half of our electricity will come from renewables by 2030. With increasing use of electricity in sectors like transport or heating and cooling, traditionally dominated by fossil fuels, it is ever more important to further increase the share of renewable energies in electricity and to unlock flexible demand, generation and storage solutions.

A new regulatory framework is needed to address these challenges and opportunities. The new proposals for a revised Renewable Energy Directive and for a new Market Design will precisely do this, by deepening integration of the internal energy market, empowering consumers, stepping up regional and EU-wide cooperation and providing the right signals for investment, thus ensuring secure, sustainable and competitive electricity systems.

A successful transition of the energy system delivering on the ambition to become world leader in renewables will require substantial investment in the sector, and in particular investments in low-carbon generation assets as well as network infrastructure. This requires a revised Emissions Trading System in order to address the current surplus of allowances and to deliver a strong investment signal to reach 40% greenhouse gas emissions reductions by 2030, but also specific rules to complement market revenues if those are not sufficient to attract investments in renewable electricity. In addition, measures to promote renewable energies in sectors like transport or heating and cooling are also crucial. Reaching the 2030 framework targets and achieving an Energy Union will be underpinned by a strong Energy Union governance, which will ensure the necessary ambition level in an iterative dialogue between the Commission and all Member States. Finally, a successful transition of the energy system will also require continued commitment and support for infrastructure development both locally as well as across borders.

At the same time the transition will only be successful if consumers are given the information, opportunities and rewards to actively participate in it. The availability of new technologies that allow consumers to both consume electricity in a smarter way as well as produce it themselves at costs which are more and more competitive opens up manifold possibilities. What is still needed to fully reap these opportunities is the appropriate regulatory framework accompanying the digital transformation and technological development that will empower consumers to take part in the energy transition by becoming active market participants. Empowering consumers in this way will also contribute to a more efficient use of energy and is therefore an integral part of implementing the efficiency first principle.

Finally, the EU will only be able to manage the energy transition successfully and cost-effectively in a more deeply integrated internal electricity market. Only a more competitive and better interconnected market will allow Europe to drive cost-efficient investment and in particular to integrate the rising share of renewable energy production in a cost-efficient and secure manner into the system, profiting fully from complementarities between Member States and broader regions.

Such a deeply integrated and competitive market is also a key building block for guaranteeing security of supply and policies and mechanisms intended to reach this objective should follow a cooperative logic. National security of supply policies need to be better coordinated and aligned. This will ensure that Member States are duly prepared to tackle possible crisis situations, in particular those that affect several countries at the same time.

The present package of legislative measures directly contributes to the Energy Union dimensions of energy security, solidarity and trust, a fully integrated internal energy market as well as decarbonisation of the economy, while also indirectly contributing to the other two.

II.

LESSON LEARNED AND PROBLEM DEFINITION

Three consecutive legislative packages have transformed what used to be fragmented energy markets in Europe into a more integrated Internal Electricity Market, thus increasing competition. However, Europe's energy markets are undergoing further profound changes.

The transition towards a low-carbon electricity production poses a number of challenges for the secure and cost-effective organisation and operation of Europe’s power grids and electricity markets. The increasing penetration of variable and decentralised renewable energy – driven inter alia by the EU’s goals for climate change and energy in line with the 2020 and 2030 targets – requires the electricity sector to be operated more flexibly and efficiently.

Today, most new installed capacity is based on wind and solar power which are inherently more variable and less predictable when compared to conventional sources of energy (predictable central, large-scale fossil fuel-based power plants) or flexible renewable energy technologies (e.g. biomass, geothermal or hydropower). By 2030, this trend is expected to be ever more pronounced. As a result, there will be times when variable renewables could cover a very large share - even 100% - of electricity demand and times when they only cover a minor share of total consumption. The overall electricity supply and demand needs to be in balance in physical terms at any given point in time (including production or storage of electricity). This balance is a precondition for the secure operation and stability of the electricity grid, thus avoiding the risk of black-outs.

Current market arrangements do not adequately incentivize all market participants – including renewable energy generation - to adjust their portfolios by revising production and consumption plans on short notice. The manner in which the trading of electricity is arranged and in which the methods for allocating the network capacity to transport electricity are organized, allow only for efficient trading of electricity in timeframes of one or more days ahead of physical delivery. Yet, the increasing penetration of variable renewable sources of electricity ('RES E') requires efficient and liquid short-term markets that can operate as close to real time as possible – until very shortly before the time of physical delivery (i.e. the moment when electricity is consumed). Indeed, most renewable generation can only be accurately predicted shortly before the actual production (due to weather uncertainties). Flexibility is essential to deal effectively with an increased share of variable renewable generation. Besides, these markets do not fully take into account possible contribution of cross-border resources.

Retail markets for energy in most parts of the EU suffer from persistently low levels of competition, consumer choice and engagement. In spite of falling prices on wholesale markets, retail prices have risen steadily for households as a result of significantly increased network charges, taxes and levies in recent years. Market concentration remains generally high due to persisting barriers to new entrants. Switching related fees such as contract termination charges continue to constitute a significant financial barrier to consumer engagement. In addition, the high number of complaints related to billing suggests that there is still scope to improve the comparability, clarity and accuracy of billing information.

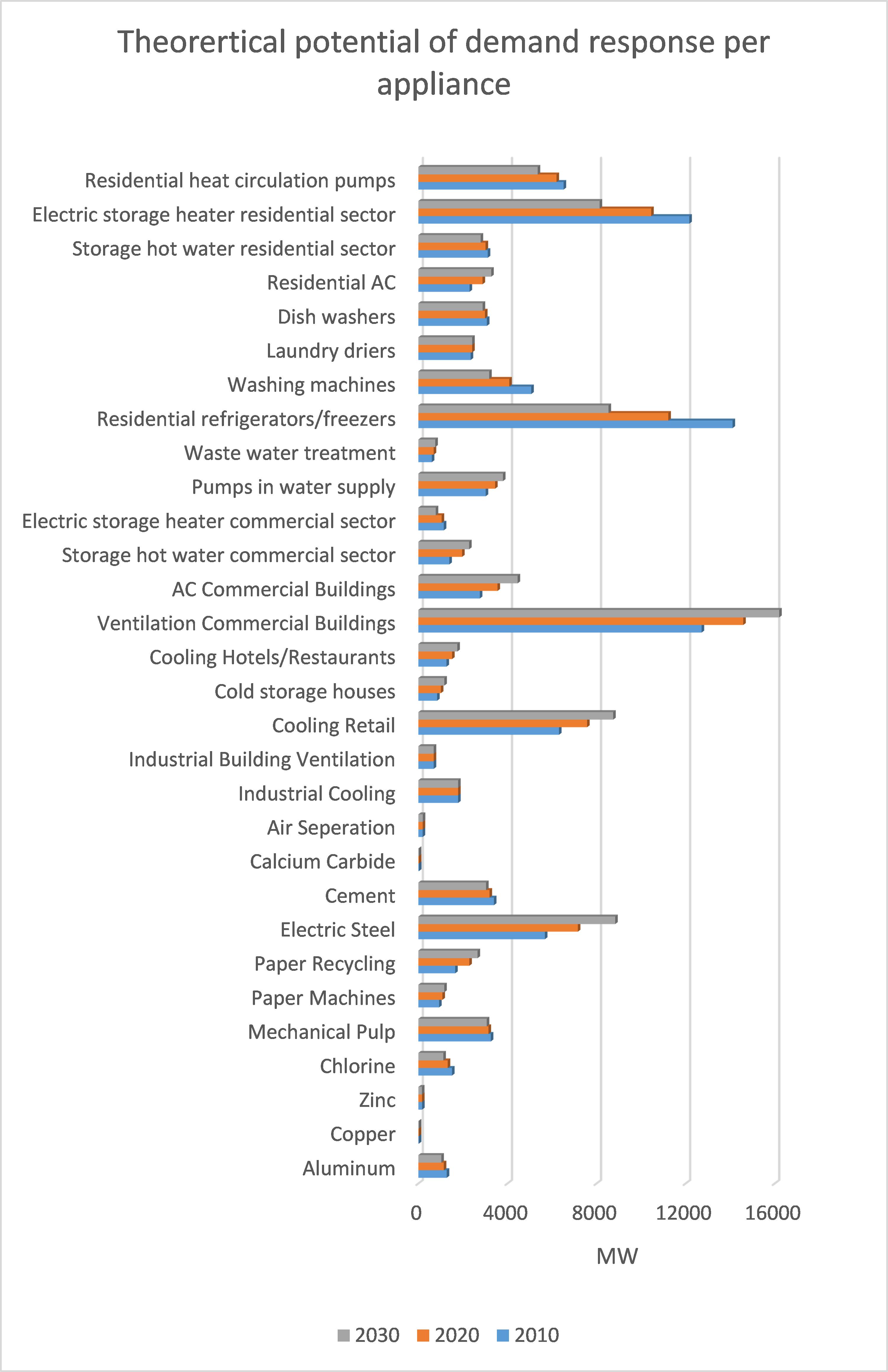

Despite technical innovations that allow consumers to better and more easily manage their energy use – smart grids, smart homes, rooftop solar panels and storage, for example – consumers are not sufficiently able to actively participate in electricity markets and match demand with supply during peak times, particularly through demand-response. This is because households and businesses often have scarce knowledge and little or no incentive to change the amount of electricity they use or produce in response to changing prices in the markets. Indeed, a host of issues such as a slow roll out of fully functional smart metering systems, regulated prices, lacklustre competition between retailers and an increasing portion of fixed charges in energy bills mean that real-time price signals are usually not passed on to final consumers.

In some Member States, up to 90% of renewable electricity generation is connected at distribution level, putting more pressure on distribution system operators ('DSOs') to actively manage their grids and to efficiently adjust to the increasing share of variable and decentralized renewable electricity injected into their networks. However – in contrast to transmission system operators ('TSOs') – the current regulatory framework does not always provide appropriate tools to DSOs to do this, resulting in network charges that are often higher than they could be for end consumers. Ensuring that all DSOs become more flexible would create a level playing field for the deployment of renewable generation that would make attaining the EU's climate and energy objectives easier.

The deployment of information technology offers the possibility to address these issues, facilitating the development of new services, improving consumer's comfort and making the market more contestable and efficient. However, to fully benefit from the digitalisation of the electricity market we need a non-discriminatory data management framework that makes the right information immediately available to the right market actors, while at the same time ensuring a high level of data protection.

With regard to consumer protection, there is a need to ensure that the move towards more efficient retail markets does not lead to any group of consumers being left behind. In particular, rising energy poverty as well as a lack of clarity on the most appropriate means of tackling consumer vulnerability and energy poverty can hamper the further deepening of the internal energy market.

In the current context, wholesale electricity prices have been decreasing due to number of coinciding drivers: a decline in primary energy prices, a surplus of carbon allowances and an overcapacity of power generation facilities in some regions of the EU caused by a drop in electricity demand, rising investments in renewables driven by EU policies and increased sharing of resources among Member States through market coupling.

For most regions in Europe, current electricity wholesale prices do not indicate the need for new investments into electricity generation. However, in the current market arrangement, prices often do not reflect the real value of electricity due to regulatory failures such as the lack of scarcity pricing and inadequately delimited price (or bidding) zones. These regulatory failures, taken together with the increasing penetration of electricity generated from renewable sources with low operating costs, affect the remuneration of conventional electricity generation units that operate less often but contribute to providing security and flexibility to the system – alongside non-conventional flexible generation, interconnections, storage and demand response.

In light of the 2030 objective for renewable energy, considerable new investment in electricity generation capacity will be required. The largest part will be provided by variable renewable generation, complemented to a certain extent by more predictable, flexible, less carbon-intensive forms of power generation. Independently of current overcapacities, there are growing concerns in some areas of Europe that current average wholesale prices may not provide appropriate signals for the necessary investments into future generation or for keeping sufficient capacity in the market. A number of Member States anticipate inadequate generation capacity in future years and introduce capacity mechanisms at national level to support investment in capacity and ensure system adequacy (i.e. the ability of the electricity system to serve demand at all times). When uncoordinated and designed without a proper assessment of the appropriate level of supply security, capacity mechanisms may risk affecting cross-border trade, distorting investment signals, affecting thus the ability of the market to deliver any new investments in conventional and low-carbon generation, and strengthening market power of incumbents by not allowing alternative providers to enter the market.

Despite best efforts to build an integrated and resilient power market, crisis situations can never be excluded. The potential for crisis situation increases with climate change (e.g. extreme weather conditions) and the emergence of new areas that are subject to criticalities such as malicious attacks and cyber-threats. Such crises tend to often have an immediate cross-border effect in electricity. Where systems are interconnected, incidents that start locally can rapidly spread beyond borders and crisis situations might also affect several Member States at the same time (e.g. prolonged heat waves or cold spells).

Today, risk assessments as well as plans and actions for dealing with electricity crisis situations focus on the national context only and there is insufficient information-sharing and transparency across Member States. In addition, there are different views on what is to be considered as a risk to security of supply. In an increasingly inter-connected electricity market, the lack of common approach and coordination can seriously imperil security of supply across borders and dangerously undermine the functioning of the internal electricity market.

In addition, missing opportunities to exchange energy with neighbours remains a key obstacle to the internal energy market. Even where interconnectors are in place, they often remain unused due to a lack of coordination between Member States. Rules are therefore needed that ensure that the use of interconnection is not unduly limited by national interventions.

Based on the above-mentioned shortcomings and underlying drivers, the present impact assessment has identified four key problem areas that are addressed in the proposed initiative: i) the current market design is not fit for integrating an increasing share of variable, decentralised generation and for reaping the potential of technological developments; ii) uncertainty about sufficient future generation investments and uncoordinated capacity mechanisms; iii) Member States do not take sufficient account of what happens across their borders when preparing for and managing electricity crisis situations; and iv) as regards retail markets, there is a slow deployment and low levels of services and poor market performance are wide-spread in the EU.

III.

SUBSIDIARITY

Article 194 of the Treaty of the Functioning of the EU consolidated and clarified the competences of the EU in the field of energy and is the legal basis of the current proposal.

Electricity markets have become more integrated and interdependent physically, economically and from a regulatory point of view, due to increasing cross-border electricity trade, growing share of renewable energy sources and more interconnections in the European electricity grid. The challenges can no longer be addressed as effectively by individual Member States. New frameworks to further integrate the internal energy market and improve the conditions for competition while at the same time adjusting to the decarbonisation targets and ensuring a more coordinated policy response to security of supply, can most effectively be achieved at European level.

IV.

SCOPE AND OBJECTIVES

Against this background and in line with the Union's policy on climate change and energy, the general policy objective of the present initiative is to make electricity markets more secure, efficient and competitive, while ensuring that electricity is generated in a sustainable way and remains affordable to all consumers. The present impact assessment reflects and analyses the need and policy options for a possible revision of the main framework governing electricity markets and security of supply policies in Europe.

There are four specific objectives: i) adapt the market design for the cost effective operation of variable and often decentralised generation, taking into account technological developments; ii) facilitate investments in generation capacity in the right amount and type of resources for the EU: iii) improve Member States' resilience on each other in times of system stress and reinforce their coordination and cooperation regarding crisis situations; and iv) address the root causes of weak competition on energy retail markets and improve consumer protection and engagement.

Interlinkages with parallel initiatives

The proposed initiative is strongly linked to other energy and climate related legislative proposals brought forward in parallel, including the renewable energy package which covers a number of measures deemed necessary to attain the EU binding objective of reaching a level of at least 27% renewables in final EU energy consumption by 2030. The renewable energy directive has synergies with the present initiative, which seeks to adapt the current market design to the increasing share of variable decentralised generation and technological development and to create an environment conducive for investments in renewables.

In particular, the reflections on a revised Renewables Energy Directive will include framework principles on support schemes for market-oriented, cost-effective and more regionalised support to RES E up to 2030, in case Member States were opting to have them as a tool to facilitate target achievement. Conversely, measures aimed at the integration of RES E in the market, such as provisions on priority dispatch and access previously contained in the Renewables Directive are part of the present market design initiative. The Renewable Package also deals with legal and administrative barriers for self-consumption, whereas the present package addresses market related barriers to self-consumption.

Both the market design and renewable energy impact assessments come to the conclusion that the improved electricity market, supported through a revised Emission Trading System ('ETS'), could, under certain conditions, by 2030 deliver investments in the most mature low-carbon technologies (such as PV and onshore wind). However, until such conditions materialise, market-based support schemes will still be needed in order to provide investment certainty. Less mature RES E technologies, such as offshore wind, will likely need some form of support throughout the transitional period.

The Energy Union governance initiative also has synergies with the present initiative and will contribute to ensure policy coherence and reduce administrative impact. It will also streamline the reporting obligations by Member States and the Commission that are presently enshrined in the Third Package.

In general terms, energy efficiency measures also interact with the present initiative as they affect the level and structure of electricity demand. In addition, energy efficiency measures can alleviate energy poverty and consumer vulnerability. Besides consumer income and energy prices, energy efficiency is one of the major drivers of energy poverty. The provisions previously contained in the energy efficiency legislation on demand response, billing and metering will be set out in the present initiative.

The present initiative is furthermore consistent with the findings of the sector inquiry on capacity mechanisms. Pointing out that there is a lack of adequate assessment of the actual need for capacity mechanisms, the sector inquiry emphasizes that where needed capacity mechanisms need to be designed with transparent and open rules of participation that does not undermine the functioning of the electricity market, taking into account cross border participation.

The Commission Regulation establishing a Guideline on Electricity Balancing ('Balancing Guideline') is also closely related to the present initiative as it aims to harmonise certain aspects of the EU's balancing markets and to optimise cross-border usage. Indeed, efficient, integrated balancing markets are an important building block for the consistent functioning and flexibility of the market which in turn is needed for a cost effective integration of RES E into the electricity market.

V.

DESCRIPTION OF POLICY OPTIONS AND METHODOLOGY

In assessing all possible options (ranging from non-regulatory to legislative policy options) the following approach was taken:

-

Identification of a set of high level options for each problem area. Each of these high level options contains sub-options for specific measures;

-

Assessment of each specific measure, comparing a number of options in order to select the preferred approach.

The following policy options have been considered:

Regarding Problem Area I: the need to adapt the market design to the increasing share of variable decentralised generation and technological developments,

Option 0+ (Non-regulatory approach) provides little scope for improving the market and the level-playing field among resources. Indeed, the current EU regulatory framework is limited in certain areas (e.g., balancing and intraday markets) and even non-existent for other areas (e.g., role of DSOs in data management). Besides, voluntary cooperation may not provide for the appropriate levels of harmonisation or certainty to the market and legislation. This option was therefore discarded.

Two possible paths going beyond the baseline scenario were however identified and assessed: (i) enhancing current market rules through EU regulatory action in order to increase the flexibility of the system, retaining to a certain extent the national operation of the systems (Option 1) and, (2) moving to a fully integrated approach via relatively far-reaching changing to the current regulatory framework (Option 2).

Option 1 of enhancing the current market rules comprises three different sub-options:

Option 1(a)

Creating a level-playing field among all generation technologies and resources and remove existing market distortions. It addresses rules that discriminate between resources and which limit or favour the access of certain technologies to the electricity grid (such as so-called 'must-run' provisions and rules on priority dispatch and access). In addition, all market participants would bear financial responsibility for the imbalances caused on the grid and all resources would be remunerated in the market on equal terms. Barriers to demand-response would be removed. Exemptions from certain regulatory provisions may, in some cases, be required, notably for certain small-scale installations and emerging technologies.

Option 1(b)

(In addition to sub-option (a)) Strengthening the short-term markets by bringing them closer to real-time in order to provide maximum opportunity to meet the flexibility needs and balance the market. The sizing of balancing reserves and their use would be harmonised in larger balancing zones in order to optimally exploit interconnections and cross-border exchange in shorter term markets.

Option 1(c)

(In addition to sub-option (a) and (b)) Pulling all flexible distributed resources concerning generation, demand and storage, into the market via proper incentives and a market framework better adapted to them. This would be based on smart-metering allowing consumers to directly react to price signals and measures to incentivise DSOs to manage their networks in a flexible and cost-efficient way.

Option 2 (fully integrated market) considers measures that would aim to deliver a truly integrated pan-European electricity market through the adoption of far-reaching measures changing the current regulatory framework.

Regarding Problem Area II: uncertainty about sufficient future generation investments and uncoordinated capacity mechanisms, four options were considered.

As regards Option 0+ (Non-regulatory approach), existing provisions under EU legislation are not sufficiently clear and robust to cope with the challenges facing the European electricity system. In addition, voluntary cooperation may not provide for appropriate levels of harmonisation across all Member States or certainty to the market. Legislation is needed in this area to address the issues in a consistent way. This Option was therefore discarded.

Various policy options going beyond the baseline scenario were assessed. They differ according to which extent market participants can rely on energy market payments. Each policy option also considers varying degrees of alignment and coordination among Member States at EU-level.

Option 1 (energy-only market without capacity mechanisms) builds upon Option 1(a) to 1(c) under problem area I and would be based on additional measures to further strengthen the internal electricity market. Under this option, it is assumed that European markets, if sufficiently interconnected and undistorted, can provide for the necessary price signals to incentivise investments in new generation thus also reducing the need for government interventions in support thereof. This option consists of improving price signals by removing price caps in order to allow scarcity pricing during peak time. At the same time, price signals could drive the geographical location of new investments and production decisions, via price zones aligned with structural congestion in the transmission grid.

Option 2 and 3 include the measures presented in Option 1, but allow capacity mechanisms under certain conditions and propose possible measures to better align them among Member States in order to avoid negative consequences for the functioning of the internal market. These options build on the European Commission's 'EEAG' state aid Guidelines and the Sector Inquiry on capacity mechanisms. In Option 2, capacity mechanisms are based on a transparent and EU-wide resource adequacy assessment carried-out by the European Network of Transmission System Operators for electricity ('ENTSO-E'). Such EU-wide assessment would also allow for effective cross-border participation. Additionally, Option 3 would provide for common design features for better compatibility between national capacity mechanisms and harmonised cross-border cooperation.

Under Option 4 based on regional or EU-wide generation adequacy assessments, entire regions or ultimately all EU Member States would be required to roll out capacity mechanisms on a mandatory basis. This option was found to be disproportionate and was discarded.

Regarding Problem Area III: the lack of coordination among Member States when preparing for and managing electricity crisis situations, five policy options ranging from the baseline scenario (Option 0) to the full harmonization and decision making at regional level have been identified.

Option 0+ (Non-regulatory approach). As current legislative provisions do not prescribe how Member States should prevent and manage crisis situations nor mandate any form of cross-border co-operation, better implementation and enforcement actions will be of no avail. In addition, whilst there is some voluntary cross-border cooperation in this area, it is limited to a few regional parts of the EU. This option was discarded.

Under Option 1 (Common minimum EU rules), Member States would have to respect a set of common rules and principles regarding crisis prevention and management, agreed at the European level ('minimum harmonisation'). Accordingly, non-market measures should only be introduced as a means of last resort, when duly justified. Member States would be obliged to address electricity crisis situations, in particular situations of a simultaneous crisis, in a spirit of co-operation and solidarity. Member States should inform each other and the Commission without undue delay when they see a crisis situation coming or when being in a crisis situation. Member States would be obliged to develop national Risk Preparedness Plans ('Plan') with the aim to avoid or better tackle crisis situations. Plans could be prepared by TSOs, but need to be endorsed at the political level. On cyber-security, Member States would need to set out in the Plan how they will prevent and manage cyberattack situations.

Option 2 (EU rules + regional cooperation) would include all common rules included in Option 1. In addition, it would put in place rules and tools to ensure that effective cross-border co-operation takes place in a regional and EU context. Thus, there would be a systematic assessment of rare/extreme risks at the regional level. The identification of crisis scenarios would be carried out by ENTSO-E in a regional context and tasks would be delegated to Regional Operation Centres (ROCs). For cybersecurity, the Commission would propose the development of a network code/guideline which would ensure a minimum level of harmonization in the energy sector throughout the EU. The Risk Preparedness Plans would contain two parts – a part reflecting national measures and a part reflecting measures to be pre-agreed in a regional context (including regional 'stress tests', procedures for cooperation in different crisis scenarios and agreement on how to deal with simultaneous electricity crisis situations).

Option 3 (Full harmonisation) entails full harmonisation and decision-making at regional level. The risk preparedness plans would be developed on regional level in order to allow a harmonised response to potential crisis situation in each region. On cybersecurity, Option 3 would go one step further and nominate a dedicated body (agency) to deal with cybersecurity in the energy sector. Crisis would have to be managed according to the regional plans agreed among Member States. A detailed 'emergency rulebook' for crisis handling would be put in place, containing an exhaustive list of measures that can be taken by Member States in crisis situations.

Regarding Problem Area IV: retail markets and the slow deployment and low levels of services and poor market performance, four policy options have been considered ranging from baseline scenario (Option 0) to full harmonization and extensive safeguards for consumers.

Option 0+ (Improved implementation/enforcement and non-regulatory approach) consists in sharing of good practices and increasing the efforts to correctly implement the legislation. This non-regulatory approach addresses competition and consumer engagement issues by strengthening the enforcement of the existing legislation as well as through bilateral consultation with Member States to progressively phase-out price regulation, starting with prices below costs. It also considers developing a Recommendation on energy bills. However, this option does not tackle the third problem driver of the market failures that prevent effective data flow between market actors.

Under Option 1 (Flexible legislation), all problem drivers are addressed through new legislation. To improve competition, Member States progressively phase-out blanket price regulation by a deadline specified in new EU legislation, starting with prices below costs, while allowing transitional price regulation for vulnerable consumers. To increase consumer engagement, the use of contract termination fees is restricted. Consumer confidence in comparison websites is fostered through national authorities implementing a certification tool. In addition, high-level principles ensure that energy bills are clear and easy to understand, through minimum content requirements. A generic adaptable, definition of energy poverty based on household income and energy expenditure is proposed in the legislation for the first time. Finally, to allow the development of new services by new entrants and energy service companies, non-discriminatory access to consumer data is ensured.

Building on Option 1, Option 2 (Full harmonisation and extensive consumer safeguards) aims to provide maximum safeguards for consumers and extensive harmonisation of Member States action throughout the EU. Exemptions to price regulation are defined at EU level on the basis of either a consumption threshold or a price threshold. A standard data handling model is enforced and assigns the responsibility to a neutral market actor such as a TSO. All switching fees including contract termination fees are banned and the content of energy bills is partially harmonized. Finally, an EU framework to monitor energy poverty based on an energy efficiency survey done by Member States of the housing stock as well as preventive measures to avoid disconnections are put in place.

VI

POLICY TRADE-OFFS

The measures considered in this impact assessment are highly complementary. Most of the different options considered in each problem area would reinforce the effect of options in other problem areas, with little trade-offs between the different areas. The overall beneficial effects will be achieved only if all measures are implemented as a package

The measures under Problem Area I and II are strongly linked in that they collectively aim at improving market functioning, including the delivery of investment by the market. Measures under Problem Area I and Option 1 of Problem area II thus reduce the need for market government intervention by means of capacity mechanisms. The other measures under Problem Area II reduce their distortive effects if such mechanisms are nonetheless justified.

Scarcity pricing and capacity mechanisms can to a certain degree be seen as alternative measures to foster investments. With assets remunerated by capacity mechanisms, the effectiveness of scarcity prices may be reduced. It needs also to be noted that scarcity prices and market-wide capacity mechanisms incentivise different investment decisions: whereas such capacity mechanisms may reward any firm capacity, scarcity pricing will improve remuneration of flexible capacity in particular.

The measures aiming at providing adequate price signals (measures under Problem Area I and Problem Area Option 1) are no-regret options. Until these conditions are achieved and under specific circumstances (like energy isolation), State intervention in the form of some type of capacity mechanism may be necessary. That is why it is essential that such mechanisms are properly designed, taking into account the wider regional and European resources and allowing cross-border participation in a technology-neutral manner.

The measures assessed under various options in the impact assessment seek to improve the overall flexibility of the electricity system. However, they do this by employing different means. Investment in new interconnection capacity may reduce the need for new generation and vice-versa, new generation can reduce the incentives for new interconnector capacity. Similarly, pulling demand response into the market will reduce the profits of generation capacity. Ultimately, the efficient markets should opt for the most cost-efficient solutions.

Energy poverty safeguards whose costs directly accrue to suppliers – particularly, the disconnection safeguards considered in Option 2 (Harmonization and extensive consumer safeguards) of Problem Area IV (Retail markets) – may act as a barrier to retail-level competition, and diminish the associated benefits to consumers, including lower prices, new and innovative products, and higher levels of service. Although the implementation costs of these safeguards will be passed on to consumers, and therefore socialized, different energy suppliers may have different abilities to do this, and to deal with the additional consumer engagement costs. Some may therefore choose not to enter markets with such safeguards in place.

VII.

ANALYSIS OF IMPACTS AND CONCLUSIONS

All options have been compared against each other using, the baseline scenario as a reference and applying the following criteria:

-

Effectiveness: the options proposed should first and foremost be effective and thus be suitable to addressing the specified problem;

-

Efficiency: this criterion assesses the extent to which objectives can be achieved at the least cost (benefits versus the costs).

Policy options regarding the need to adapt the market design to the increasing share of variable decentralised generation and technological developments (Problem Area I)

Options 1(a) (level playing field), 1(b) (strengthening short-term markets) and 1(c) (demand response/distributed resources) represent an interlinked set of measures regarding the integration of the national electricity markets and present a compromise between bottom-up initiatives and top-down steering of the market development, without substituting the role of national governments, regulators and TSOs by a centralised and fully harmonised system.

However, Option 1(a) (level playing field) and Option 1(b) (strengthening short-term markets) do not cover measures to pull all distributed flexible resources (demand-response, renewable electricity and storage) into the market. These options do not take advantage of the potential offered by these resources to efficiently operate and decarbonise the electricity market.

In this context, Option 1(c) (demand response/distributed resources) provides a more holistic, effective and efficient package of solutions. While this option may lead to minor additional administrative impacts for Member States and competent authorities regarding the implementation and monitoring of the measures, these impacts will be offset by lower barriers to entry to start-ups and SMEs, by the benefits to market parties from more stable regulatory frameworks and new business opportunities as well as by the benefits to consumers from more competition and access to wider choice.

As regards Option 2 (fully integrated market), while having advantages in terms of less coordination requirements (i.e., a fully integrated EU-market can be operated more efficiently), the results of the assessment indicate that the move towards a more integrated European approach has less significant economic added value since most of the benefits will have already been reaped under the regional, more decentralised approach under option. In addition, it has significant impacts on stakeholders, Member States and competent authorities since it requires significant changes to established practices.

Preferred option for Problem Area I: Option 1(c) (demand response/distributed resources, also encompassing options 1(a) (level playing field) and 1(b) (strengthening short-term markets))

Policy options regarding uncertainty about sufficient future generation investments and uncoordinated capacity mechanisms (Problem Area II)

Option 1 (reinforced energy only market without capacity mechanisms) can in principle provide the right signals for market operation and ensure system adequacy and ensure better utilisation of resources across borders, demand participation and renewable integration without subsidies. Improving the functioning of electricity markets will improve the conditions for investment in the electricity market to ensure reliable and effective supply of electricity, even in times of scarcity. This will in turn decrease the need for capacity mechanisms.

However, markets are today still characterised by manifold regulatory distortions today and removing the distortive effects will not be possible with immediate effects in many Member States. Besides under such option, uncertainty about future policy directions or governmental interventions still exists. Such uncertainty may hamper investment and in turn create the need for mechanisms that address the lack of investments ('missing money').

It should be noted that undistorted energy price signals are fundamental irrespective of whether generators are solely relying on energy market incomes or also receive capacity payments. Therefore the measures aimed at removing distortions from energy-only markets discussed under Option 1(a) to 1(c) (e.g. scarcity pricing or reinforced locational signals) are 'no-regrets' and assumed as being integral parts of Options 2, 3 and 4.

Option 2 (Improved energy markets – Capacity Mechanisms ('CM's) only when needed, based on a common EU-wide adequacy assessment can improve the overall cost-efficiency of the electricity sector through establishing an EU-wide approach to system adequacy assessments as opposed to national-based adequacy assessments. At the same time Option 2 does not allow reaping the full benefits of cross-border participation in capacity mechanisms.

A more coordinate approach to state interventions across Member States is needed and is a clear priority for reform. Placing capacity mechanisms into a more regional/EU context is a pre-requisite to reduce market distortions. It is indeed necessary that the schemes Member States introduce are compatible with internal market rules.

Option 3 (Improved energy market – CMs only when needed, plus cross-border participation) proposes additional measures to avoid fragmentation of capacity mechanisms and ensures that foreign resource providers can effectively participate in national capacity mechanisms and avoids competition and market distortions resulting from capacity payments which are reserved to domestic participants. As a result, it reduces investment distortions that might be present in Option 2 because of uncoordinated approaches to cross-border participation.

Preferred option for Problem Area II: Option 3 (Improved energy market – CMs only when needed, plus cross-border participation) (encompassing also Options 1 and 2)

Policy options regarding the lack of coordination among Member States when preparing for and managing electricity crisis situations (Problem Area III)

Based on a set of clear common rules, Option 1 (Common minimum EU rules) would improve the level of transparency and crisis management across Europe and is likely to reduce the chances of premature market intervention. The policy tools proposed under this option would bring economic benefits to businesses and consumers by helping to prevent costly blackout situations. However, this option does not solve the issue of uncoordinated planning and preparation ahead of a crisis since Member State are not required to take into account cross-border risks and crisis.

Under Option 2 (EU rules + regional cooperation), the regionally coordinated plans ensure the regional identification of risks and the consistency of the measures for prevention and managing crisis situations while respecting national differences and competences. This significantly improves the level of preparedness (compared to Option 1) at national, regional and EU level, as the cross border considerations are duly taken into account since the beginning. A regional approach to security of supply results in a better utilisation of power plants and guarantees risk preparedness at a lesser cost.

Under Option 3 (Full harmonisation), the estimated impact on cost is likely to be high (notably with the creation of an EU agency on cyber-security) and the measures put forward appear disproportionate compared to the expected effectiveness. Indeed, this option represents a highly intrusive approach – with significant administrative impact - by resorting to a full harmonisation of principles and the prescription of concrete solutions.

Preferred option for Problem Area III: Option 2 (EU rules + regional cooperation)

Policy options regarding retail markets and the slow deployment and low levels of services and poor market performance (Problem Area IV)

Given its low implementation costs, Option 0+ (Non-regulatory approach) is a highly efficient option. However, the effectiveness of Option 0+ is significantly limited by the fact that non-regulatory measures are not suitable for tackling the poor data flow between retail market actors that constitutes both a barrier to entry and a barrier to higher levels of service to consumers. In addition, shortcomings in the existing legislation make it impossible to significantly improve consumer engagement and energy poverty safeguards. They also introduce great uncertainty around the drive to phase out price regulation which does not provide sufficient incentives to consumers to play an active role in the market and which also limits competition and new entrants into the market.

Option 1 (Flexible legislation) would lead to substantial economic benefits. Retail competition would be improved as a result of the progressive phase-out of blanket price regulation, non-discriminatory access to consumer data, and increased consumer engagement. In addition, consumers would see direct benefits through improved switching.

In Option 2 (Harmonization and extensive consumer safeguards) there is uncertainty over the size of the economic benefits. This uncertainty stems from the tension some of the measures in Option 2 may have with competition (stronger disconnection safeguards, an outright ban on all switching-related charges), and from the difficulty of prescribing EU-level solutions in certain areas (defining exceptions to price deregulation, implementing a standard EU bill design). Besides, a single EU data management model would have high implementation costs, thus reducing the efficiency of the option.

Preferred option for Problem Area IV: Option 1 (Flexible legislation)

***

Table of contents

1.

Introduction

1.1.

Background and scope of the market design initiative

1.1.1.

Context of the initiative

1.1.1.1.

The gradual process of creating an internal electricity market

1.1.1.2.

The Union's policy concerning climate change

1.1.1.3.

Paradigm shift in the electricity sector

1.1.1.4.

The vision for the EU electricity market in 2030 and beyond

1.1.2.

Scope of the initiative

1.1.2.1.

Current relevant legislative framework

1.1.2.2.

Policy development subsequent to the Third Package

1.1.2.3.

Scope and summary of the initiative

1.1.3.

Organisation and timing

1.1.3.1.

Follow up on the Third Package

1.1.3.2.

Consultation and expertise

1.2.

Interlinkages with parallel initiatives

1.2.1.

The Renewable Energy Package comprising the new Renewable Energy Directive and bioenergy sustainability policy for 2030 ('RED II')

1.2.2.

Commission guidance on regional cooperation

1.2.3.

The Energy Union governance initiative

1.2.4.

The Energy Efficiency legislation ('EE') and the related Energy Performance of Buildings Directive ('EPBD') including the proposals for their amendment.

1.2.5.

The Commission Regulation establishing a Guideline on Electricity Balancing ('Balancing Guideline')

1.2.6.

Other relevant instruments

2.

Problem Description

2.1.

Problem Area I: Market design not fit for an increasing share of variable decentralized generation and technological developments

2.1.1.

Driver 1: Short-term markets, as well as balancing markets, are not efficiently organised

2.1.2.

Driver 2: Exemptions from fundamental market principles

2.1.3.

Driver 3: Consumers do not actively engage in the market and demand response potential remains largely untapped

2.1.4.

Driver 4: Distribution networks are not actively managed and grid users are poorly incentivised

2.2.

Problem Area II: Uncertainty about sufficient future generation investments and uncoordinated capacity markets

2.2.1.

Driver 1: Lack of adequate investment signals due to regulatory failures and imperfections in the electricity market

2.2.2.

Driver 2: Uncoordinated state interventions to deal with real or perceived capacity problems

2.3.

Problem Area III: Member States do not take sufficient account of what happens across their borders when preparing for and managing electricity crisis situations

2.3.1.

Driver 1: Plans and actions for dealing with electricity crisis situations focus on the national context only

2.3.2.

Driver 2: Lack of information-sharing and transparency

2.3.3.

Driver 3: No common approach to identifying and assessing risks

2.4.

Problem Area IV: The slow deployment of new services, low levels of service and questionable market performance on retail markets

2.4.1.

Driver 1: Low levels of competition on retail markets

2.4.2.

Driver 2: Possible conflicts of interest between market actors that manage and handle data

2.4.3.

Driver 3: Low levels of consumer engagement

2.5.

What is the EU dimension of the problem?

2.6.

How would the problem evolve, all things being equal?

2.6.1.

The projected development of the current regulatory framework

2.6.2.

Expected evolution of the problems under the current regulatory framework

2.7.

Issues identified in the evaluation of the Third Package

3.

Subsidiarity

3.1.

The EU's right to act

3.2.

Why could Member States not achieve the objectives of the proposed action sufficiently by themselves?

3.3.

Added-value of action at EU-level

4.

Objectives

4.1.

Objectives and sub-objectives of the present initiative

4.2.

Consistency of objectives with other EU policies

5.

Policy options

5.1.

Options to address Problem Area I (Market design not fit for an increasing share of variable decentralized generation and technological developments)

5.1.1.

Overview of the policy options

5.1.2.

Option 0: Baseline Scenario – Current Market Arrangements

5.1.3.

Option 0+: Non-regulatory approach

5.1.4.

Option 1: EU Regulatory action to enhance market flexibility

5.1.4.1.

Sub-option 1(a): Level playing field amongst participants and resources

5.1.4.2.

Sub-option 1(b): Strengthening short-term markets

5.1.4.3.

Sub-option 1(c): Pulling demand response and distributed resources into the market

5.1.5.

Option 2: Fully Integrated EU market

5.1.6.

For Option 1 and 2: Institutional framework as an enabler

5.1.7.

Summary of specific measures comprising each Option

5.2.

Options to address Problem Area II (Uncertainty about sufficient future generation investments and uncoordinated capacity markets)

5.2.1.

Overview of the policy options

5.2.2.

Option 0: Baseline Scenario – Current Market Arrangements

5.2.3.

Option 0+: Non-regulatory approach

5.2.4.

Option 1: Improved energy market - no CMs

5.2.5.

Option 2: Improved energy market – CMs only when needed, based on a common EU-wide adequacy assessment)

5.2.6.

Option 3: Improved energy market - CMs only when needed, based on a common EU-wide adequacy assessment, plus cross-border participation

5.2.7.

Option 4: Mandatory EU-wide or regional CMs

5.2.8.

Discarded Options

5.2.9.

Summary of specific measures comprising each Option

5.3.

Options to address Problem Area III (When preparing or managing crisis situations, Member States tend to disregard the situation across their borders)

5.3.1.

Overview of the policy options

5.3.2.

Option 0: Baseline scenario – Purely national approach to electricity crises

5.3.3.

Option 0+: Non-regulatory approach

5.3.4.

Option 1: Common minimum rules to be implemented by Member States

5.3.5.

Option 2: Common minimum rules to be implemented by Member States, plus regional co-operation

5.3.6.

Option 3: Full harmonisation and decision-making at regional level

5.3.7.

Discarded Options

5.3.8.

Summary of specific measures comprising each Option

5.4.

Options to address Problem Area IV (Slow deployment and low levels of services and poor market performance)

5.4.1.

Overview of the policy options

5.4.2.

Option 0: Baseline Scenario - Non-competitive retail markets with poor consumer engagement and poor data flows

5.4.3.

Option 0+: Non-regulatory approach to address competition and consumer engagement

5.4.4.

Option 1: Flexible legislation addressing all problem drivers

5.4.5.

Option 2: EU Harmonization and extensive safeguards for consumers addressing all problem drivers

5.4.6.

Summary of specific measures comprising each Option

6.

Assessment of the impacts of the various policy options

6.1.

Assessment of economic impacts for Problem Area I (Market design not fit for an increasing share of variable decentralized generation and technological developments

6.1.1.

Methodological Approach

6.1.1.1.

Impacts Assessed

6.1.1.2.

Modelling and use of studies

6.1.1.3.

Summary of Main Impacts

6.1.1.4.

Overview of Baseline (Current Market Arrangements)

6.1.2.

Policy Sub-option 1(a) (Level playing field amongst participants and resources)

6.1.2.1.

Economic impacts

6.1.2.2.

Who would be affected and how

6.1.2.3.

Administrative impact on businesses and public authorities

6.1.3.

Impacts of Policy Sub-option 1(b) (Strengthening short-term markets)

6.1.3.1.

Economic Impacts

6.1.3.2.

Who would be affected and how

6.1.3.3.

Administrative impact on businesses and public authorities

6.1.4.

Impacts of Policy Sub-option 1(c) (Pulling demand response and distributed resources into the market)

6.1.4.1.

Economic Impacts

6.1.4.2.

Who would be affected and how

6.1.4.3.

Impact on businesses and public authorities

6.1.5.

Impacts of Policy Option 2 (Fully integrated EU market)

6.1.5.1.

Economic Impacts

6.1.5.2.

Who would be affected and how

6.1.5.3.

Impact on businesses and public authorities

6.1.6.

Environmental impacts of options related to Problem Area I

6.1.7.

Summary of modelling results for Problem Area I

6.2.

Impact Assessment for Problem Area II (Uncertainty about future generation investments and fragmented capacity mechanisms)

6.2.1.

Methodological Approach

6.2.1.1.

Impacts Assessed

6.2.1.2.

Modelling

6.2.1.3.

Overview of Baseline (Current Market Arrangements)

6.2.2.

Impacts of Policy Option 1 (Improved energy markets - no CMs )

6.2.2.1.

Economic Impacts

6.2.2.2.

Who would be affected and how

6.2.2.3.

Administrative impact on businesses and public authorities

6.2.3.

Impacts of Policy Option 2 (Improved energy markets – CMs only when needed, based on a common EU-wide adequacy assessment)

6.2.3.1.

Economic Impacts

6.2.3.2.

Who would be affected and how

6.2.3.3.

Impact on businesses and public authorities

6.2.4.

Impacts of Policy Option 3 (Improved energy market – CMs only when needed, plus cross-border participation)

6.2.4.1.

Economic Impacts

6.2.4.2.

Who would be affected and how

6.2.4.3.

Impact on businesses and public authorities

6.2.5.

Environmental impacts of options related to Problem Area II

6.2.6.

Overview of modelling results for Problem Area II

6.2.6.1.

Improved Energy Market as a no-regret option

6.2.6.2.

Comparison of Options 1 to 3

6.2.6.3.

Delivering the necessary investments

6.2.6.4.

Level and volatility of wholesale prices

6.3.

Impact Assessment for problem Area III (reinforce coordination between Member States for preventing and managing crisis situations)

6.3.1.

Methodological Approach

6.3.2.

Impacts of Policy Option 1 (Common minimum rules to be implemented by Member States)

6.3.2.1.

Economic impacts

6.3.2.2.

Who would be affected and how

6.3.2.3.

Impact on businesses and public authorities

6.3.3.

Impacts of Policy Option 2 (Common minimum rules to be implemented by Member States plus regional co-operation)

6.3.3.1.

Economic impacts

6.3.3.2.

Who would be affected and how

6.3.3.3.

Impact on businesses and public authorities

6.3.4.

Impacts of Policy Option 3 (Full harmonisation and full decision-making at regional level)

6.3.4.1.

Economic impacts

6.3.4.2.

Who would be affected and how

6.3.4.3.

Impact on businesses and public authorities

6.4.

Impact Assessment for Problem Area IV (Increase competition in the retail market)

6.4.1.

Methodological Approach

6.4.2.

Impacts of Policy Option 0+ (Non-regulatory approach to improving competition and consumer engagement)

6.4.2.1.

Economic Impacts

6.4.2.2.

Who would be affected and how

6.4.2.3.

Impact on businesses and public authorities

6.4.3.

Impacts of Policy Option 1 (Flexible legislation addressing all problem drivers)

6.4.3.1.

Economic Impacts

6.4.3.2.

Who would be affected and how

6.4.3.3.

Impact on businesses and public authorities

6.4.4.

Impacts of Policy Option 2 (Harmonization and extensive safeguards for consumers addressing all problem drivers)

6.4.4.1.

Economic Impacts

6.4.4.2.

Who would be affected and how

6.4.4.3.

Impact on businesses and public authorities

6.4.5.

Environmental impacts

6.4.6.

Impacts on fundamental rights regarding data protection

6.5.

Social impacts

7.

Comparison of the options

7.1.

Comparison of options for adapting market design for the cost-effective operation of variable and often decentralised generation, taking into account technological developments

7.2.

Comparison of Options for facilitating investments in the right amount and in the right type of resources for the EU

7.3.

Comparison of options for improving Member States' reliance on each other in times of system stress and reinforcing coordination between Member States for preventing and managing crisis situations

7.4.

Comparison of options for addressing the causes and symptoms of weak competition in the energy retail market

7.5.

Synergies, trade-offs between Problem Areas and sequencing

7.5.1.

Synergies

7.5.2.

Trade-offs

7.5.3.

Sequencing of measures

8.

Monitoring and evaluation

8.1.

Future monitoring and evaluation plan

8.2.

Annual reporting by ACER and evaluation by the Commission

8.2.1.

Annual reporting by ACER

8.2.2.

Evaluation by the Commission

8.3.

Monitoring by the Electricity Coordination Group

8.4.

Operational objectives

8.5.

Monitoring indicators and benchmarks

9.

Glossary and Acronyms

1.Introduction

1.1.Background and scope of the market design initiative

1.1.1.Context of the initiative

1.1.1.1.The gradual process of creating an internal electricity market

Well-functioning energy markets that ensure secure energy supplies at competitive prices are key for achieving growth and consumer welfare in the European Union.

Since 1996, the European Union has put in place legislation to enable the transition from an electricity system traditionally dominated by vertically integrated national incumbents that owned and operated all the generation and network assets in their territories to competitive, well-functioning and integrated electricity markets. The first step was the adoption of the First Energy Package (1996 for the electricity sector and 1998 for the gas sector), which allowed for the partial opening of the market where the largest consumers were given the right to choose their supplier. The Second Energy Package (2003) introduced changes concerning the structure of the vertically integrated companies (legal unbundling), the preparation of the full opening of the market by 1 July 2007 and the reinforcement of the powers of the national regulators. The most recent comprehensive reform of European energy market rules, the Third Internal Energy Market Package (2009)

('Third Package') has principally aimed at improving the functioning of the internal energy market and resolving structural problems.

Since the adoption of the Third Package, electricity policy decisions have enabled competition and increasing cross-border flows of electricity, notably with the introduction of so called "market coupling"

and "flow-based" capacity allocation. In spite of significant differences in the maturity of markets in Europe, overall electricity wholesale markets are increasingly characterised by fair and open competition, and – though still insufficient – competition is also taking root at the retail level.

1.1.1.2.The Union's policy concerning climate change

The decarbonisation of EU economies is at the core of the EU’s agenda for climate change and energy. The targets in the Climate and Energy Package (2007) require Member States to cut their greenhouse gas emissions by 20% (from 1990 levels), to produce 20% of their energy from renewable energy sources (RES), and to improve energy efficiency by 20 % (the '2020 targets').

In 2011, the European Union committed to reduce greenhouse gas emissions to 80-95% below 1990 levels by 2050. For this purpose, the European Commission adopted an Energy Roadmap

and a roadmap for moving to a competitive low carbon economy exploring the transition of the energy system in ways that would be compatible with this greenhouse gas reductions target while also increasing competitiveness and security of supply. The 2050 roadmap will require a higher degree of decarbonisation from the electricity sector compared to other economic sectors.

These ambitions were reaffirmed by the European Council of October 2014, which endorsed targets for 2030 of at least 40 % for domestic greenhouse gas emissions reduction (compared to 1990 levels), at least 27 % for the share of renewable energy consumption, binding at EU level and at least 27 % energy savings, to be reviewed by 2020, having in mind an EU level of 30% (the '2030 targets').

At the Paris climate conference (COP21) in December 2015, 195 countries adopted the first-ever legally binding global climate deal. The European Council of March 2016 confirmed the EU's commitment to implement the 2030 targets. The Paris Agreement was ratified by the European Union and entered into force on 4 November 2016..

1.1.1.3.Paradigm shift in the electricity sector

The Union's goals for climate change and energy have led to a paradigm shift in the means employed to generate electricity: since the adoption of the Third Package, there has been a move towards the deployment of capital-intensive low marginal cost, variable and often decentralised electricity from RES E (mostly from solar and wind technologies) that is expected to become more pronounced by 2030.

The increasing penetration of RES E is driven inter alia by the objective to reduce greenhouse gas emissions in line with the 2020 and 2030 targets. The 2030 greenhouse gas emission reduction target is to be delivered through reducing emissions by 43% compared to 2005 for the sectors in the EU's ETS

(including the electricity sector and industry) and by 30% compared to 2005 for the sectors outside the ETS. Within the electricity sector, the reduction of greenhouse gas emissions is supported by the Renewable Energy Directive

, the ETS and the additional national policies by Member States to increase the share of renewables in the energy mix.

The Renewable Energy Directive established a European framework for the promotion of renewable energy, setting mandatory national renewable energy targets for achieving a 20% EU share of renewable energy in the final energy consumption and a 10% share of energy from renewable sources in transport by 2020. These objectives have translated into a need to foster the increased production of electricity from reneweble energy sources.

In parallel with the increased deployment of variable and decentralized RES E, the increasing digitalisation of electricity networks and the environment behind the meter now enables many elements of the electricity system to be operated more flexibly and efficiently in the context of RES E generation. It also allows smaller actors to play an increasingly important part in the market on both the supply side and – crucially – the demand side, potentially untapping a vast new system resource.

From the consumer's perspective, increasingly intelligent grids unlock a host of other possibilities, including innovative new products and services, lower entry barriers for new suppliers, and improved billing and switching. This promises to unlock value and improve the consumer experience – provided the legislative framework adapts to the changing needs and possibilities. Indeed, fully engaging end consumers will be essential to realizing the full benefits that the digital transformation can bring in terms of grid flexibility.

Moreover, electricity demand will progressively reflect the increasing electrification of transport and heating.

The challenges the EU's electricity systems face are reflected in the European Commission Communication of February 2015 on “A Framework Strategy for a Resilient Energy Union with a Forward-Looking Climate Change Policy”

where the Commission announced a new electricity market design linking wholesale and retail markets. As part of the legislative reform process needed to establish the Energy Union, it also announced new legislation on security of electricity supply.

In the light of the Energy Union Framework Strategy, the present impact assessment reflects and analyses the need and policy options for a possible revision of the main framework governing electricity markets and security of electricity supply policies in Europe. The new electricity market design contributes strongly to the overall Energy Union objectives of securing low carbon energy supplies to the European consumers at least costs.

1.1.1.4.The vision for the EU electricity market in 2030 and beyond

The Energy Union Framework Strategy sets out the vision of an Energy Union "with citizens at its core, where citizens take ownership of the energy transition, benefit from new technologies to reduce their bills, participate actively in the market, and where vulnerable consumers are protected". Well-functioning energy markets that ensure secure energy supplies at competitive prices are important for achieving growth and consumer welfare in the European Union. The future of the entire energy sector will, to a significant extent, be shaped by the evolution of the electricity sector, which is key to addressing climate change. With the quick ratification of the global Paris Agreement on climate change and its subsequent entry into force, it becomes clear how important it is for all parties to the agreement, including the EU, to deliver on the clean energy transition on the ground. In fact, amongst all sectors that make up our energy system, electricity is the most cost-effective to decarbonise. Currently 27.5% of Europe's electricity is produced from renewable energy sources. The share of RES E in electricity generation needs to almost double by 2030 in order for the EU to meet its 2030 energy and climate targets cost-effectively. This will require creating the right conditions for the massive amount of investment needed for this energy transition to come about. At the same time electricity markets will have to adapt to the radical change in the structure of the generation pattern which will foremost require creating a more flexible market, going across borders, that is able to allow more active participation of a much wider range of actors.

The EU's vision of the electricity system in 2030 is therefore based on a functioning market that is adapted to implementing the decarbonisation agenda at least cost together with a revised EU ETS. A well-functioning electricity market is also the most efficient tool to ensure secure electricity supplies at the lowest reasonable cost.

The transition of the energy system towards the 2030 vision

The starting point is the existing reality, which dates back to an era with large-scale, centralised power plants, largely fuelled by fossil fuels, had the key aim of supplying every home and business in a delineated area – typically a Member State – with as much electricity as they wanted, and in which consumers – households, businesses and industry – were passive users.

However, the electricity market is undergoing profound change and requires a new set of rules to ensure secure supplies, competitiveness while enabling cost-effective decarbonisation. The electricity market of the next decade will be characterised by more variable and decentralised electricity production, an increased interdependence between Member States and new technological opportunities for customers to reduce their bills and actively participate in electricity markets through demand response, self-consumption or storage.

The electricity market design initiative aims to improve the functioning of the internal electricity market in order to allow electricity to move freely to where and when it is most needed, empower consumers, reap maximum benefits for society from cross-border competition and provide the right signals and incentives to drive the right investments compatible with climate change, renewable energy and energy efficiency ambitions.

The proposed initiative constitutes a next-step in a wider and longer evolutionary process that will guide the EU's electricity markets towards the 2030 vision.

The 2030 electricity market is highly flexible and provides a level playing field amongst all forms of generation as well as demand response…

The bulk of the new generation capacity is likely to come from renewable sources, mainly wind and sun that are variable and predictable only to a limited extent. The future electricity market will therefore need to be more flexible and liquid than today and allow for integrated short-term trading. This would also set the ground for renewable energy producers – who will over time acquire increasing share in generation - to equally access energy wholesale markets and to compete on an equal footing with conventional energy producers. Short-term markets will also allow Member States to share their resources across all "time frames" (forward trading, day-ahead, intraday and balancing), taking advantage of the fact that peaks and weather conditions across Europe do not occur at the same time. This would provide maximum opportunity to meet the flexibility needs and balance the market. The sequence of forward markets and spot markets - day-ahead, intraday and balancing - will optimise prices and the system in the short-run and will reveal the true value of electricity and, therefore, provide appropriate investments signals in the long-run.

The closer to real time electricity is traded (supply and demand matched), the less the need for costly interventions by TSOs to maintain a stable electricity system. Although TSOs would have less time to react to schedule deviations and unexpected events and forecast errors, the liquid, better interconnected balancing markets, together with the regional procurement of balancing reserves and more balancing actors and products available from both demand and supply side, would be expected to provide them adequate and more efficient resources in order to manage the grid and facilitate RES E integration.

All this will help to create a level playing field not only among all modes of generation but also the demand side. At the same time market distortions and rules that artificially limit or favour the access of certain technologies to the grid would be removed. All market participants would become gradually responsible for balancing their position in the market, bearing financial responsibility for the imbalances they cause and would, therefore, be incentivised to reduce the risk of such imbalances. The most cost-efficient sources of electricity would be used first, curtailment of generation due to limited transmission and distribution infrastructure would be a measure of last resort and confined to situations in which no market-based responses (including storage and demand response) are available, and subject to transparent rules known in advance to all market actors and adequate financial compensation. All resources would be remunerated in the market on equal terms.

…and active consumers.

Ensuring that all consumers – big and small – can actively participate in the energy market would unlock a vast system resource that could play an important role in reducing system costs. Technology – including smart grids and smart homes - is already available and will further develop to enable consumers to modulate their demand while maintaining comfort and reducing costs.

In the future, consumers would be sufficiently incentivised to benefit from these opportunities and thus demand response would be provided by all willing consumer groups, including residential and commercial consumers either directly or through intermediaries (like aggregators). This would further increase the flexibility of the electricity system and the resources for the TSOs and DSOs to manage it. At the same time it should lead to a much more efficient operation of the whole energy system.

Consumers would be able to react to price signals on electricity markets both in terms of consumption and production; they would consume when prices are low, when there is plenty of electricity available, and reduce their consumption at times of low electricity production and high prices. To make this possible, consumers have access to a fit-for-purpose smart metering system, smart homes and storage as well as electricity supply contracts with prices linked dynamically to the wholesale markets.

More and more consumers would produce their own electricity. Such decentralised production further strengthens security of supply and helps to implement the decarbonisation agenda as most of this production comes from renewable sources. If combined with local storage solutions, consumers could significantly contribute to balancing the distribution grids at local level. Analysis suggests that this development will be progressive, and that most consumers would still remain connected to the distribution grid to use it as back-up for when the prosumers' own generation is inadequate (e.g. for sustained periods of low sunlight) or for the opportunity to sell excess electricity to the market (e.g. during prolonged sunny periods when their installed storage is at full capacity).

Reducing barriers to market entry for electricity suppliers and consumer engagement – notably phasing out price regulation – results in increased competition at the retail level allowing consumers to save money through better information and a wider choice of action. This also helps drive the uptake of innovative new products and services that increase system flexibility through demand response whilst catering to consumers' changing needs and abilities.

In addition, DSOs would be enabled and incentivised, without compromising their neutrality as system operators, to manage their networks in a flexible and cost-efficient way – inter alia through revised tariff structures.

Increased cross-border trade is a pillar of the electricity market.

Competition and cross-border flows of electricity would further increase, with fully coupled markets where price differences between Member States are smoothened out. Electricity wholesale markets will be characterised by fair and open competition, including across borders. Cooperation between TSOs will be enhanced by regional operational centres. The cross-border cooperation of TSOs would be accompanied by an increased level of cooperation between regulators and governments. An adequate cross-border infrastructure remains crucial to underpin a well-functioning electricity market.

Increasingly investments are triggered by the market with a decreasing need for state subsidies.

The enhanced market design, the revised renewables directive and the strengthened ETS will all help to improve the viability of RES E investments, in particular as follows: