ISSN 1977-1010

Jornal Oficial

da União Europeia

C 346

Edição em língua portuguesa

Comunicações e Informações

63.° ano

16 de outubro de 2020

|

ISSN 1977-1010 |

||

|

Jornal Oficial da União Europeia |

C 346 |

|

|

|

||

|

Edição em língua portuguesa |

Comunicações e Informações |

63.° ano |

|

Índice |

Página |

|

|

|

II Comunicações |

|

|

|

COMUNICAÇÕES DAS INSTITUIÇÕES, ÓRGÃOS E ORGANISMOS DA UNIÃO EUROPEIA |

|

|

|

Comissão Europeia |

|

|

2020/C 346/01 |

Autorização de auxílios estatais no âmbito das disposições dos artigos 107.o e 108.o do Tratado sobre o Funcionamento da União Europeia — Casos relativamente aos quais a Comissão não levanta objeções ( 1 ) |

|

|

V Avisos |

|

|

|

PROCEDIMENTOS RELATIVOS À EXECUÇÃO DA POLÍTICA DE CONCORRÊNCIA |

|

|

|

Comissão Europeia |

|

|

2020/C 346/02 |

Auxílio estatal — Hungria — Auxílio estatal SA.49073 (2017/FC) — Alegado auxílio estatal à Malév Ground Handling — Convite à apresentação de observações nos termos do artigo 108.o, n.o 2, do Tratado sobre o Funcionamento da União Europeia ( 1 ) |

|

|

2020/C 346/03 |

Auxílios Estatais — Bélgica — auxílio estatal SA.54915 (2019/N) — Mecanismo de remuneração da capacidade — Convite à apresentação de observações nos termos do artigo 108.o, n.o 2, do Tratado sobre o Funcionamento da União Europeia ( 1 ) |

|

|

|

|

|

(1) Texto relevante para efeitos do EEE. |

|

PT |

|

II Comunicações

COMUNICAÇÕES DAS INSTITUIÇÕES, ÓRGÃOS E ORGANISMOS DA UNIÃO EUROPEIA

Comissão Europeia

|

16.10.2020 |

PT |

Jornal Oficial da União Europeia |

C 346/1 |

Autorização de auxílios estatais no âmbito das disposições dos artigos 107.o e 108.o do Tratado sobre o Funcionamento da União Europeia

Casos relativamente aos quais a Comissão não levanta objeções

(Texto relevante para efeitos do EEE)

(2020/C 346/01)

|

Data de adoção da decisão |

7.8.2020 |

|||

|

Número do auxílio |

SA.56832 (2020/N) |

|||

|

Estado-Membro |

Croácia |

|||

|

Região |

Jadranska Hrvatska |

N.o 3, alínea a), do artigo 107.o |

||

|

Denominação (e/ou nome do beneficiário) |

Sixth amendment to the concession agreement relating to the Istrian Y Motorway (sub-phase 2B2-1: section «Vranja interchange to the Ucka tunnel/Kvarner portal») |

|||

|

Base jurídica |

— |

|||

|

Tipo de auxílio |

Auxílio individual |

Bina-Istra d.d. |

||

|

Objetivo |

— |

|||

|

Forma do auxílio |

Subvenção/Bonificação de juros |

|||

|

Orçamento |

— |

|||

|

Intensidade |

— |

|||

|

Duração (período) |

— |

|||

|

Setores económicos |

Construção de estradas e auto-estradas |

|||

|

Nome e endereço da entidade que concede o auxílio |

|

|||

|

Outras informações |

— |

|||

O texto original da decisão, expurgado dos dados confidenciais, está disponível no endereço:

http://ec.europa.eu/competition/elojade/isef/index.cfm.

|

Data de adoção da decisão |

3.7.2020 |

|

|

Número do auxílio |

SA.56943 (2020/N) |

|

|

Estado-Membro |

Letónia |

|

|

Região |

— |

— |

|

Denominação (e/ou nome do beneficiário) |

Recapitalization of Air Baltic — Latvia — Covid 19 |

|

|

Base jurídica |

The legal basis for the measure is the governmental Order no 256 of 8 May 2020 to subscribe to a capital increase of up to EUR 250 million. |

|

|

Tipo de auxílio |

Auxílio ad hoc |

Air Baltic |

|

Objetivo |

Sanar uma perturbação grave da economia |

|

|

Forma do auxílio |

Outras formas de participação de capital — The measure comprises a State capital increase of EUR 250 million. |

|

|

Orçamento |

Orçamento global: EUR 250 (em milhões) |

|

|

Intensidade |

% |

|

|

Duração (período) |

A partir de 1.7.2020 |

|

|

Setores económicos |

Transportes aéreos de passageiros |

|

|

Nome e endereço da entidade que concede o auxílio |

The granting authority is the Government of Latvia. The Ministry of Transport will be the authority administering the measure. |

|

|

Outras informações |

— |

|

O texto original da decisão, expurgado dos dados confidenciais, está disponível no endereço:

http://ec.europa.eu/competition/elojade/isef/index.cfm.

|

Data de adoção da decisão |

6.7.2020 |

|

|

Número do auxílio |

SA.57539 (2020/N) |

|

|

Estado-Membro |

Áustria |

|

|

Região |

— |

— |

|

Denominação (e/ou nome do beneficiário) |

COVID-19 — Aid to Austrian Airlines |

|

|

Base jurídica |

Ordinance issued by the Federal Minister of Finance under Section 3b(3) of the ABBAG Act. |

|

|

Tipo de auxílio |

Auxílio ad hoc |

Austrian Airlines |

|

Objetivo |

Compensação de danos causados por calamidades naturais ou por outros acontecimentos extraordinários |

|

|

Forma do auxílio |

Subvenção direta |

|

|

Orçamento |

Orçamento global: EUR 150 (em milhões) |

|

|

Intensidade |

% |

|

|

Duração (período) |

A partir de 1.7.2020 |

|

|

Setores económicos |

Transportes aéreos |

|

|

Nome e endereço da entidade que concede o auxílio |

The measure will be managed by the COVID-19 Finanzierungsagentur des Bundes GmbH («COFAG»), a federal agency of Austria. |

|

|

Outras informações |

— |

|

O texto original da decisão, expurgado dos dados confidenciais, está disponível no endereço:

http://ec.europa.eu/competition/elojade/isef/index.cfm.

|

Data de adoção da decisão |

11.8.2020 |

|||||||

|

Número do auxílio |

SA.57586 (2020/N) |

|||||||

|

Estado-Membro |

Estónia |

|||||||

|

Região |

— |

— |

||||||

|

Denominação (e/ou nome do beneficiário) |

Estonia COVID19 — Recapitalisation and Subsidised Interest Loan for Nordica |

|||||||

|

Base jurídica |

|

|||||||

|

Tipo de auxílio |

Auxílio individual |

Nordic Aviation Group AS |

||||||

|

Objetivo |

Sanar uma perturbação grave da economia |

|||||||

|

Forma do auxílio |

Instrumentos de capital próprio, Bonificação de juros |

|||||||

|

Orçamento |

Orçamento global: EUR 30 (em milhões) Orçamento anual: EUR 30 (em milhões) |

|||||||

|

Intensidade |

% |

|||||||

|

Duração (período) |

até 30.6.2021 |

|||||||

|

Setores económicos |

Transportes aéreos de passageiros |

|||||||

|

Nome e endereço da entidade que concede o auxílio |

|

|||||||

|

Outras informações |

— |

|||||||

O texto original da decisão, expurgado dos dados confidenciais, está disponível no endereço:

http://ec.europa.eu/competition/elojade/isef/index.cfm.

|

Data de adoção da decisão |

28.9.2020 |

|

|

Número do auxílio |

SA.58659 (2020/N) |

|

|

Estado-Membro |

Suécia |

|

|

Região |

— |

— |

|

Denominação (e/ou nome do beneficiário) |

Sweden COVID-19: Amendment to SA.56860 — Prolongation of the period of the State loan guarantee scheme. |

|

|

Base jurídica |

Extra ändringsbudget 2020 — kreditgarantier för lån till företag (prop. 2019/20:142), Regeringsbeslut med uppdrag till Riksgäldskontoret om att förbereda och verkställa ett statligt garantiprogram för företag (N2020/0771/EIN) |

|

|

Tipo de auxílio |

Regime de auxílios |

— |

|

Objetivo |

Sanar uma perturbação grave da economia |

|

|

Forma do auxílio |

— |

|

|

Orçamento |

— |

|

|

Intensidade |

— |

|

|

Duração (período) |

1.10.2020 — 31.12.2020 |

|

|

Setores económicos |

Todos os setores económicos elegíveis para beneficiar de auxílios |

|

|

Nome e endereço da entidade que concede o auxílio |

Riksgäldskontoret |

|

|

Outras informações |

— |

|

O texto original da decisão, expurgado dos dados confidenciais, está disponível no endereço:

http://ec.europa.eu/competition/elojade/isef/index.cfm.

|

Data de adoção da decisão |

25.9.2020 |

|||

|

Número do auxílio |

SA.58684 (2020/N) |

|||

|

Estado-Membro |

Dinamarca |

|||

|

Região |

DANMARK |

— |

||

|

Denominação (e/ou nome do beneficiário) |

Adjustment of SA.57164 — COVID-19- Loan schemes for companies in their early stage and companies in the venture segment to match with private investments. |

|||

|

Base jurídica |

Aktstk. 304 Aktstykke om udvidelse af COVID-19-matchfinansieringsordningen til venturevirksomheder |

|||

|

Tipo de auxílio |

Regime de auxílios |

— |

||

|

Objetivo |

PME, Financiamento de risco |

|||

|

Forma do auxílio |

Empréstimos em condições preferenciais |

|||

|

Orçamento |

Orçamento global: DKK 1 060 (em milhões) Orçamento anual: DKK 1 060 (em milhões) |

|||

|

Intensidade |

— |

|||

|

Duração (período) |

até 31.12.2020 |

|||

|

Setores económicos |

Todos os setores económicos elegíveis para beneficiar de auxílios |

|||

|

Nome e endereço da entidade que concede o auxílio |

|

|||

|

Outras informações |

— |

|||

O texto original da decisão, expurgado dos dados confidenciais, está disponível no endereço:

http://ec.europa.eu/competition/elojade/isef/index.cfm.

|

Data de adoção da decisão |

5.10.2020 |

|||||

|

Número do auxílio |

SA.58690 (2020/N) |

|||||

|

Estado-Membro |

Suécia |

|||||

|

Região |

— |

— |

||||

|

Denominação (e/ou nome do beneficiário) |

COVID-19: Prolongation of SA.57051 — Aid for cancelled or postponed cultural events |

|||||

|

Base jurídica |

Förordning om ändring i förordningen (2020:246) om statligt stöd för kulturevenemang som har ställts in eller skjutits upp med anledning av spridningen av sjukdomen covid-19 |

|||||

|

Tipo de auxílio |

Regime de auxílios |

— |

||||

|

Objetivo |

Compensação de danos causados por calamidades naturais ou por outros acontecimentos extraordinários |

|||||

|

Forma do auxílio |

Subvenção/Bonificação de juros |

|||||

|

Orçamento |

Orçamento global: SEK 600 (em milhões) |

|||||

|

Intensidade |

75 % |

|||||

|

Duração (período) |

— |

|||||

|

Setores económicos |

Actividades de produção de filmes; de vídeo e de programas de televisão; de gravação de som e de edição de música |

|||||

|

Nome e endereço da entidade que concede o auxílio |

|

|||||

|

Outras informações |

— |

|||||

O texto original da decisão, expurgado dos dados confidenciais, está disponível no endereço:

http://ec.europa.eu/competition/elojade/isef/index.cfm.

|

Data de adoção da decisão |

1.10.2020 |

|||

|

Número do auxílio |

SA.58718 (2020/N) |

|||

|

Estado-Membro |

Hungria |

|||

|

Região |

Hungary |

— |

||

|

Denominação (e/ou nome do beneficiário) |

COVID-19. First amendment of scheme SA.58202 regarding COVID-19 related research, development and production support |

|||

|

Base jurídica |

Amendment to Government Decree 255/2014 (X. 10.) on State aid rules concerning the financial resources allocated to the 2014–2020 period |

|||

|

Tipo de auxílio |

Regime de auxílios |

— |

||

|

Objetivo |

Sanar uma perturbação grave da economia |

|||

|

Forma do auxílio |

Subvenção direta |

|||

|

Orçamento |

Orçamento global: HUF 35 000 (em milhões) Orçamento anual: HUF 35 000 (em milhões) |

|||

|

Intensidade |

100 % |

|||

|

Duração (período) |

até 31.12.2020 |

|||

|

Setores económicos |

Todos os setores económicos elegíveis para beneficiar de auxílios |

|||

|

Nome e endereço da entidade que concede o auxílio |

|

|||

|

Outras informações |

— |

|||

O texto original da decisão, expurgado dos dados confidenciais, está disponível no endereço:

http://ec.europa.eu/competition/elojade/isef/index.cfm.

V Avisos

PROCEDIMENTOS RELATIVOS À EXECUÇÃO DA POLÍTICA DE CONCORRÊNCIA

Comissão Europeia

|

16.10.2020 |

PT |

Jornal Oficial da União Europeia |

C 346/8 |

AUXÍLIO ESTATAL — HUNGRIA

Auxílio estatal SA.49073 (2017/FC) — Alegado auxílio estatal à Malév Ground Handling

Convite à apresentação de observações nos termos do artigo 108.o, n.o 2, do Tratado sobre o Funcionamento da União Europeia

(Texto relevante para efeitos do EEE)

(2020/C 346/02)

Por ofício de 28 de outubro de 2019, publicado a seguir ao presente resumo na língua que faz fé, a Comissão notificou a Hungria da decisão de dar início ao procedimento previsto no artigo 108.o, n.o 2, do Tratado sobre o Funcionamento da União Europeia relativamente à medida acima mencionada.

As partes interessadas podem apresentar as suas observações relativamente à medida de auxílio em relação à qual a Comissão dá início ao procedimento no prazo de um mês a contar da data de publicação do presente resumo e da carta que o acompanha, enviando-as para o seguinte endereço:

|

Comissão Europeia |

|

Direção-Geral da Concorrência |

|

Registo dos Auxílios Estatais |

|

1049 Bruxelles/Brussel |

|

BELGIQUE/BELGIË |

|

Fax +32 22961242 |

|

Stateaidgreffe@ec.europa.eu |

Essas observações serão comunicadas à Hungria. As partes interessadas que apresentarem observações podem solicitar por escrito o tratamento confidencial da sua identidade, devendo justificar o pedido.

A Malév Ground Handling (a seguir «Malév GH») é uma empresa de assistência em escala que opera no aeroporto de Budapeste e era uma filial da Malév, a antiga transportadora aérea húngara. Em 2012, a Comissão adotou uma decisão negativa exigindo à Malév a recuperação de um auxílio estatal à reestruturação incompatível. Em consequência, a companhia aérea declarou falência. A Malév GH é agora propriedade do Estado húngaro através da agência responsável pela gestão dos ativos do Estado húngaro (MNV Zrt., a seguir «MNV»).

Em agosto de 2017, a Budport, um concorrente privado da Malév GH, apresentou uma denúncia alegando que a Malév GH beneficiava de auxílios estatais sob a forma de injeções de capital, de remissão de dívidas e de empréstimos da empresa MNV, de uma entidade pública denominada Tiszavíz e do banco húngaro de desenvolvimento (Banco Magyar Fejlesztési, a seguir «MFB»).

Nesta fase, embora as autoridades húngaras aleguem a ausência de auxílio argumentando que a Tiszavíz, a MNV e o MFB atuaram como operadores numa economia de mercado, a Comissão chegou à conclusão preliminar de que cinco medidas, sob a forma de empréstimo, aumento de capital ou conversão de dívida em capital, num montante de cerca de 21 milhões de EUR, parecem constituir um auxílio estatal na aceção do artigo 107.o, n.o 1, do TFUE.

Além disso, parece duvidoso, nesta fase, que as condições de compatibilidade com o mercado interno, nos termos do artigo 107.o, n.o 3, alínea c), do Tratado sobre o Funcionamento da União Europeia, aplicáveis aos auxílios à reestruturação previstos nas Orientações comunitárias relativas aos auxílios estatais de emergência e à reestruturação a empresas em dificuldade (1) e nas Orientações relativas aos auxílios estatais de emergência e à reestruturação concedidos a empresas não financeiras em dificuldade (2), sejam cumpridas: as autoridades húngaras não invocaram possíveis fundamentos para a compatibilidade das medidas; as medidas não parecem cumprir as condições de compatibilidade das Orientações E&R, nomeadamente a exigência de uma contribuição própria, medidas compensatórias ou, eventualmente, o princípio do «auxílio único».

TEXTO DO OFÍCIO

A Bizottság tájékoztatni kívánja Magyarországot, hogy a Malév GH Földi Kiszolgáló Zrt (a továbbiakban: MGH) javára nyújtott közfinanszírozással kapcsolatban a magyar hatóságok által benyújtott információk vizsgálatát követően az Európai Unió működéséről szóló szerződés (a továbbiakban: EUMSZ) 108. cikkének (2) bekezdésében előírt eljárás megindításáról határozott.

1. ELJÁRÁS

|

(1) |

2017. augusztus 30-án a Budport Handling Kft (a továbbiakban: Budport), amely az MGH versenytársa a budapesti repülőtéren, panaszt nyújtott be, azt állítva, hogy az MGH összeegyeztethetetlen állami támogatásban részesült. E panaszt a 2017. szeptember 15-i, valamint a 2017. október 9-i és 10-i, a 2017. december 5-i, a 2018. január 24-i, a 2018. április 5-i és a 2018. június 11-i beadványok egészítették ki. |

|

(2) |

A Bizottság 2017. október 26-án, 2018. február 20-án, 2018. június 13-án, 2018. október 9-én és 2019. január 17-én összesen öt információkérést küldött Magyarországnak, amelyekre Magyarország 2018. január 10-én, 2018. április 20-án, 2018. szeptember 11-én, 2018. november 9-én és 2019. február 11-én válaszolt. A Bizottság 2018. június 22-én arra is felkérte a magyar hatóságokat, hogy tegyék meg a Budport 2018. június 11-én kelt beadványára vonatkozó észrevételeiket. A magyar hatóságok ezt 2018. szeptember 11-i beadványuk részeként tették meg. |

|

(3) |

Magyarország 2019. január 11-én benyújtotta továbbá az állítólagos állami támogatási intézkedésekkel kapcsolatos álláspontjának összefoglalását. |

|

(4) |

A Bizottság észrevételezés céljából a Budport rendelkezésére bocsátotta az említett információkérésekre Magyarország által adott első két válasz nem bizalmas változatát. A Budport 2018. július 30-án válaszolt. |

2. A KEDVEZMÉNYEZETT

2.1. Az MGH bemutatása

|

(5) |

A Liszt Ferenc Nemzetközi Repülőtéren földi kiszolgálási szolgáltatásokat nyújtó MGH 2002-ben jött létre. |

|

(6) |

Az MGH, amely a bevétele alapján a vizsgálati időszakban mintegy [20–40 %] (*1)-os piaci részesedéssel rendelkezett a budapesti repülőtér földi kiszolgálási piacán, az alábbi három – szintén a budapesti repülőtéren tevékenykedő – magántulajdonban lévő szereplővel versenyez: Çelebi (török, körülbelül [50–70 %]-os piaci részesedés), Menzies (brit, körülbelül [0-20 %]-os piaci részesedés) és Budport (magyar). A Budport 2012-től 2017 júliusáig az MGH alvállalkozójaként működött, és az MGH-tól származó alvállalkozói bevételt is beleszámítva 2016-ra nagyjából [0–10 %]-os piaci részesedést ért el. A Budport kivételével mindegyik társaság nyújt utas-, rakomány -és előtéri kezelési szolgáltatásokat a budapesti repülőtéren. |

|

(7) |

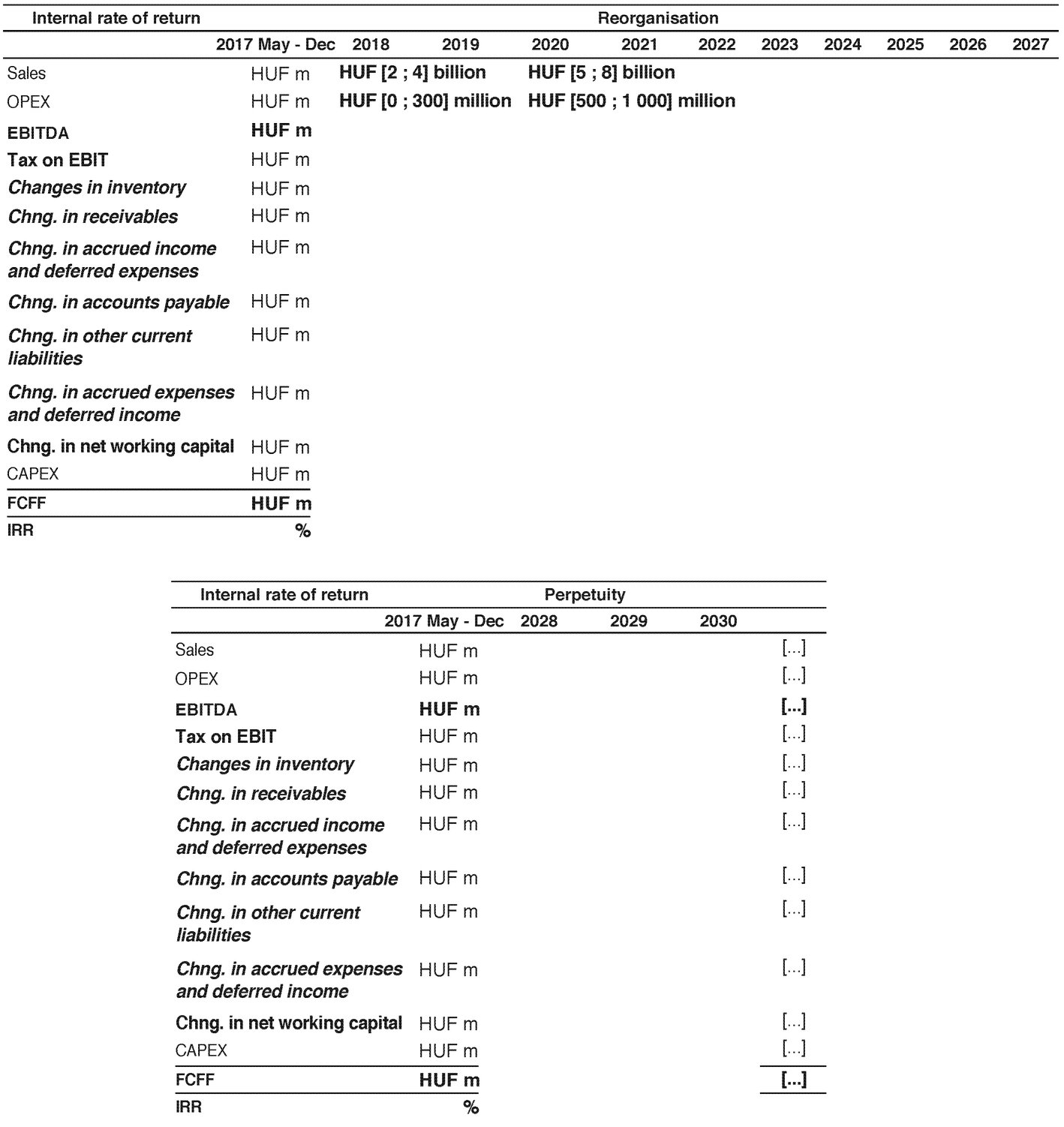

Az MGH korábban a Magyar Légiközlekedési Zrt. (a továbbiakban: Malév), a piacról 2012 februárjában kilépett hagyományos magyar légitársaság 100 %-os tulajdonában állt. A Malév biztosította az MGH árbevételének több mint [50 %–100 %][…]-át. A Malév 2012. februári felszámolását követően az MGH elvesztette legnagyobb ügyfelét. A MGH saját tőkéje 2011-ben negatívba fordult, amikor céltartalékot kellett képeznie a Malév [0–5 milliárd] HUF-t ([0–17] millió EUR) kitevő követeléseivel szemben. Ebből következően – amint az 1. ábrán szerepel – az MGH saját tőkéje a 2010 végi 2,1 milliárd HUF-ról 2011 végére mínusz 85 millió HUF-ra csökkent. Ennélfogva az MGH 2011 végén a nehéz helyzetben lévő vállalkozások megmentéséhez és szerkezetátalakításához nyújtott állami támogatásokról szóló közösségi iránymutatás (3) (a továbbiakban: a 2004. évi megmentési és szerkezetátalakítási iránymutatás) értelmében nehéz helyzetben lévő vállalkozásnak minősült. Jóllehet 2012-ben és 2013-ban az MGH pozitív EBITDA-val rendelkezett, 2014 és 2017 között EBITDA veszteséget termelt. 2018-ban, a jelentős feltőkésítést magában foglaló reorganizációs terv (lásd az 5. intézkedés, v pontját a (17) bekezdésben) végrehajtásának megkezdését, az MGH és [az MGH egyik kulcsfontosságú ügyfele] közötti szerződés újratárgyalását, valamint a Budporttal kötött szerződésének felmondását követően, az MGH körülbelül [0–2] milliárd […] HUF-tal ([0–6] millió EUR) növelte az árbevételét, és az anyagi és a személyi ráfordítások is ennek megfelelő mértékben növekedtek. Ennek eredményeként az MGH 40 millió HUF (0,1 millió EUR) összegű, kis mértékben pozitív EBITDA-t ért el.

1. táblázat Az MGH historikus pénzügyi adatai

|

|

(8) |

A Nemzeti Fejlesztési Minisztérium felügyelete alá tartozó Magyar Nemzeti Vagyonkezelő Zrt. (4) (a továbbiakban: MNV) 2012. június 14-én megvásárolta az MGH-t a Malév felszámolás alá tartozó vagyonából. |

|

(9) |

Az MNV általi felvásárlást követően az MGH számos szerkezetátalakítási intézkedést hajtott végre. Az MGH csoportos létszámcsökkentést kezdeményezett (elbocsátott mintegy [0–500][…] munkavállalót) és észszerűsítette a költségeit. Az MGH-nak 2012 óta sikerült megőriznie harmadik felekből álló ügyfélportfóliójának jelentős részét – amelyekkel jellemzően [3–6] évre kötnek szerződést – és új ügyfeleket (WizzAir, Air China, Emirates stb.) is szerzett, bár másokat (LOT, Brussel Airlines) elvesztett. 2012 novemberében az MGH elnyert egy szerződést a WizzAir (5) diszkont légitársasággal, amelyet 2015-ben […]-ig megújítottak. |

|

(10) |

Mivel [az MGH egyik kulcsfontosságú ügyfele] az MGH tevékenységének jelentős részét képviseli, [az MGH egyik kulcsfontosságú ügyfele] szolgáltatási szerződéseinek […] alacsony árrése komoly hatást gyakorol az MGH nyereségességére. 2017-ben az MGH-nak a feltőkésítés keretein belül sikerült újratárgyalnia és […]-val/-vel emelnie [az MGH egyik kulcsfontosságú ügyfelének] felszámított díjakat [az MGH egyik kulcsfontosságú ügyfele] gyorsított tendere során (6). |

2.2. Az MGH és a Budport közötti együttműködés és konfliktus története

|

(11) |

A Budportnak az MGH-val való együttműködése 2012-ben kezdődött, amikor az MGH a Budport részére alvállalkozásba adta a 2015. [hónap]-ig érvényes […] jegyértékesítési […] (7). A jegyértékesítési alvállalkozói szerződés 2014 és 2016 között évi mintegy […] EBIT-et hozott a Budportnak. |

|

(12) |

2017 júliusában, a gyorsított tendert és [az MGH egyik kulcsfontosságú ügyfelével] […] kötött új megállapodást követően az MGH felmondta a Budporttal kötött alvállalkozói szerződést. Ez végül ahhoz vezetett, hogy a Budport állami támogatással kapcsolatos panaszt nyújtott be. A Budport emellett sikertelenül kísérelte meg elérni az MGH felszámolását. |

|

(13) |

[…] 2016 augusztusában keresetet indított az MGH ellen a Fővárosi Törvényszéken (amely még folyamatban van), és kártérítést követelt az MGH-tól az alvállalkozói szerződés felmondása miatt, valamint az alvállalkozói szerződés alapján az MGH által a […] részére fizetendő díjak összegével kapcsolatosan a két vállalkozás között kialakult vitával összefüggésben. […] szerint a Bíróság előtti jogvita kimenetelétől függően [a peres eljárások lehetséges pozitív vagy negatív hatásai az MGH pénzügyeire]. |

2.3. A Budport panasza

|

(14) |

2017. augusztus 30-án a Budport panaszt nyújtott be, amelyben azt állította, hogy az MGH összeegyeztethetetlen állami támogatásban részesült a 465 millió HUF (kb. 1,5 millió EUR (8)) összegű 2014. évi tőkeemelés (lásd a 3. intézkedést a (17) bekezdésben) révén, valamint az 5,4 milliárd HUF (kb. 17,6 millió EUR) összegű 2017. évi tőkeemelésre vonatkozó, ezután tervezett intézkedésből (lásd az 5. intézkedést a (17) bekezdésben). 2017. szeptemberi, júniusi és 2018. júliusi további beadványaiban a Budport hozzáfűzte, hogy álláspontja szerint három másik intézkedés (az MNV, illetve a teljesen állami tulajdonban álló bank, az MFB által az MGH-nak nyújtott kölcsönök alaptőkévé konvertálása) összeegyeztethetetlen állami támogatásnak minősül (lásd az 1., 2. és 4. intézkedést a (17) bekezdésben). |

|

(15) |

A Budport állítása szerint ezek az intézkedések lehetővé tették az MGH számára, hogy fenntartsa piaci jelenlétét azáltal, hogy költségeinél alacsonyabb áron nyújt szolgáltatásokat a légitársaságoknak. A Budport mindenekelőtt azt állítja, hogy az MGH 2014-ben jelentős árengedményekre kényszerült néhány fontos ügyfelének megtartása érdekében. |

|

(16) |

A Budport szerint ezen intézkedéseknek nincs összeegyeztethetőségi alapja. |

3. AZ INTÉZKEDÉSEK LEÍRÁSA

|

(17) |

A Budport panasza és későbbi beadványai összességében a következő intézkedésekre irányulnak:

|

|

(18) |

A fenti intézkedések összességében láthatólag mintegy 20 millió EUR összegnek (12) felelnek meg. |

4. MAGYARORSZÁG ELŐZETES ÉSZREVÉTELEI

4.1. Általános észrevételek

|

(19) |

Magyarország azt hangsúlyozta, hogy a Malév csődjét követően az MGH 2012-ben nehézségekkel küzdött, ami arra kényszerítette az MGH-t, hogy a piacon maradás érdekében alacsony árrésű szerződést kössön [az MGH egyik kulcsfontosságú ügyfelével]. |

|

(20) |

Magyarország szerint az MGH-nak strukturális kihívásokkal kellett szembenéznie amiatt, hogy régi eszközkészlete magas karbantartási költségeket igényelt, valamint amiatt, hogy viszonylag magas foglalkoztatási költségek jelentkeztek, mivel […]. |

|

(21) |

Az MGH emellett 2012-ben állítólag kedvezőtlen alvállalkozói szerződést kötött a Budporttal, alvállalkozásba adva a Budportnak [az MGH egyik kulcsfontosságú ügyfele] utasai számára történő jegykiadás jövedelmező üzletágát. Magyarország kifejti, hogy az MGH akkori vezetése által elfogadott alvállalkozás egyértelműen hibás lépés és fenntarthatatlan volt az MGH számára, viszont szokatlanul jövedelmező volt a Budportnak. |

|

(22) |

E nehézségek ellenére az MGH 2012 óta elért bizonyos fokú kedvező eredményeket (2013-ban korlátozott mértékű, de pozitív nyereség, 2016-tól bővülő értékesítés). A jövőben még jobb teljesítmény is várható annak fényében, hogy az MGH 2017-ben újratárgyalta [az MGH egyik kulcsfontosságú ügyfelével] megkötött szerződését (13), valamint felmondta a Budporttal kötött alvállalkozói szerződését. A 2018-as pénzügyi év tekintetében rendelkezésre álló auditált adatok szerint az MGH 2018-ban 40 millió HUF összegű (kb. 0,1 millió EUR) EBITDA eredményt ért el. |

|

(23) |

Magyarország azt állítja, hogy az MGH 2013 óta már pozitív EBITDA eredményt termelt volna, ha egyrészt 2013-tól élvezte volna [az MGH egyik kulcsfontosságú ügyfelével] megkötött új szerződési feltételek előnyeit, másrészt pedig saját maga érte volna el a Budport EBITDA eredményét, ha – alvállalkozásba adás helyett – a társaságon belül biztosították volna a jegykiadási szolgáltatást [az MGH egyik kulcsfontosságú ügyfele] számára. |

4.2. Magyarország egyedi intézkedésekre vonatkozó álláspontja

4.2.1. Az MGH-nak nyújtott előny

|

(24) |

A magyar hatóságok szerint az állítólagos intézkedések nem minősülnek állami támogatásnak, mivel megfelelnek a piacgazdasági szereplő elvének. |

1. intézkedés: az MFB által 2012. április 27-én nyújtott 400 millió HUF összegű hitel és annak későbbi módosításai

|

(25) |

Magyarország azzal érvel, hogy az MFB-hitel az alábbiak miatt nem tartalmaz támogatást:

|

2. intézkedés: A Tiszavíz által nyújtott, 580 millió HUF értékű 2012-es tulajdonosi kölcsön, és annak MNV általi felvásárlása és részleges meghosszabbítása

|

(26) |

Ami a tulajdonosi kölcsön piacgazdasági szereplő tesztnek való megfelelését illeti, Magyarország azt állítja, hogy az MNV utasításai alapján eljáró Tiszavíznek a tulajdonosi kölcsön nyújtását megelőzően nem kellett előzetes tanulmányt megrendelnie, mivel támaszkodhatott a BDO tanácsadó cég (16) által az MGH felvásárlásával összefüggésben készített tanulmányra. Magyarország rámutat, hogy mindössze két nap telt el a BDO-tanulmány által lefedett felvásárlás és a tulajdonosi kölcsön nyújtása között. Magyarország szerint a tulajdonosi kölcsön, valamint a vételár és a [500–1000] millió HUF összegű 2012-es tőkeemelés együttesen megfelel a piacgazdasági szereplő tesztnek, mivel a BDO-tanulmány szerint a saját tőke diszkontált cash flow megközelítés szerint számított valós piaci értéke magasabb volt, mint az MGH vételára ([0–1] millió HUF), az MGH 2012-es tőkeemelése ([500–1000] millió HUF […]), és a tulajdonosi kölcsön (580 millió HUF) együttes összegei. A BDO-tanulmány az MGH tulajdoni hányadának becsült értékét is megadja (nettó eszközértéken [400–800] millió HUF), amit a BDO kevésbé tart relevánsnak az MGH saját tőkéje valós piaci értékének meghatározása tekintetében. |

|

(27) |

Magyarország továbbá azzal érvel, hogy a tulajdonosi kölcsön nem tartalmazott támogatást, mivel a referencia-kamatlábról szóló közleménnyel összhangban lévő kamatláb mellett nyújtották.

2. táblázat A BDO-tanulmány pénzügyi előrejelzéseinek kivonata (17)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

3. intézkedés: az 580 millió HUF összegű tulajdonosi kölcsönnek az MNV általi 250 millió HUF összegű részleges tőkekonverziója

|

(28) |

Magyarország szerint a tőkekonverzió nem független a 2. intézkedéstől. Magyarország azt állítja, hogy a 2013-as intézkedés hiányában az MGH jegyzett tőkéje két egymást követő évben a jogszabályban előírt minimális szint alá esett volna, és ezért felszámolásra, fúzióra vagy feltőkésítésre lett volna szükség. |

|

(29) |

Magyarország szerint a 3. intézkedés keretében nem biztosítottak további forrásokat az MGH számára. |

|

(30) |

Tekintettel arra, hogy a tulajdonosi kölcsönt nem látták el fedezettel, az MNV állítólagosan nem került jobb helyzetbe fedezett nélküli kölcsönadóként, mint részvényesként. Emellett Magyarország kezdetben azzal érvelt, hogy mivel akkor az MNV volt az MGH egyetlen, fedezettel nem rendelkező hitelezője és részvényese, nem volt szükség arra, hogy külön értékelést készítsenek erről az ügyletről. Magyarország később előadta, hogy álláspontja szerint erre az ügyletre röviddel a BDO értékelése után került sor, és az nem járt olyan következménnyel, hogy az MNV-nek az MGH-ba eszközölt összes befektetése meghaladta volna azt a maximális összeget, amelyet egy magánbefektető kész lett volna befektetni az MGH-ba az említett értékelés szerint. |

4. intézkedés: a 2015-ös tőkeinjekció

|

(31) |

Magyarország azt állítja, hogy az MGH vezetése által készített előzetes tanulmány alapján, amely alátámasztotta a két beruházás várható nyereségességét, az MNV meg volt győződve a beruházás ésszerűségéről. E tanulmány szerint 8 év […] alatt [0,5–5] milliárd HUF […] összegű nyereség várható [az X projektbe] történő befektetéstől, [az Y projekt] pedig várhatóan összesen [0,3–3] milliárd HUF nyereséget termel. Magyarország szerint eképpen nem volt szükség arra, hogy az MNV „saját előzetes gazdasági értékelést készítsen az MGH vállalkozásáról”, mivel „ismerte” az MGH helyzetét.

3. táblázat Az MGH által készített tanulmánynak [az X projektre] és [az Y projektre] vonatkozó pénzügyi előrejelzései

|

|

(32) |

Magyarország azt állítja továbbá, hogy ez az ügylet azonos feltételek mellett jött létre, mivel nem voltak lényeges eltérések az MGH-nak és a […]-nak/-nek a […] projektben való részvétele között. |

5. intézkedés: a 2017. évi tőkeinjekció (5364 millió HUF összegű tőkeemelés)

|

(33) |

Magyarország kifejti, hogy az MNV jogilag köteles volt feltőkésíteni az MGH-t, mivel annak saját tőkéje 2015-ben és 2016-ban a jogszabályban meghatározott határérték alá csökkent. Az MGH vezetése 2017-ben olyan tervet készített, amely előirányozta a […]-val/-vel (magántulajdonban lévő üzemeltető) és [az MGH egyik kulcsfontosságú ügyfelével] kötött jelentős szerződések újratárgyalását, a Budporttal kötött szerződésének felmondását, valamint egy eszközkorszerűsítési programot. |

|

(34) |

Magyarország kifejti, hogy a 2017-es tőkeinjekció a következő célra szolgált:

|

|

(35) |

Magyarország szerint a piacgazdasági szereplő teszt teljesült: A Deloitte elkészítette az MGH tervének előzetes „magas szintű felülvizsgálatát”, amely szerint 2019-ben várhatóan helyreáll a nyereségesség, és [8–20] %-os belső megtérülési ráta keletkezik, mely meghaladja a piacgazdasági befektető megtérülési követelményét([8–20] %-os súlyozott átlagos tőkeköltség („WACC”)). Magyarország szerint ez a WACC figyelembe veszi, hogy a hasonló társaságok finanszírozási költsége alapján az MGH adósságát [0–3] %-os kockázati prémium terheli az államkötvényekhez képest.

4. táblázat A Deloitte magas szintű felülvizsgálata alá vont reorganizációs terv pénzügyi kimutatásai

|

|

(36) |

Magyarország emellett azt állítja, hogy egy, a vállalattal szemben már gazdasági kitettséggel rendelkező magánbefektető szempontjából gazdaságilag racionális döntés volt az MNV azon döntése, hogy az MGH felszámolása helyett inkább feltőkésíti a vállalkozást. |

|

(37) |

Bár a 0. és az I. ütemről már döntés született és azokat végrehajtották, Magyarország kifejti, hogy Magyarország 2018. szeptember 11-i beadványának megfelelően a II. ütemet még nem hajtották végre. Magyarország szerint a II. ütemet akkor fogják végrehajtani, ha az MNV úgy ítéli meg, hogy az MGH a reorganizációs tervnek megfelelően fejlődik. |

4.2.2. Az államnak való betudhatóság

|

(38) |

A magyar hatóságok az államnak való betudhatóságot nem vitatták (lásd a (45). és a (48) bekezdést). |

5. ÉRTÉKELÉS

|

(39) |

Ez a határozat a fenti (17) bekezdésben említett öt szerkezetátalakítási támogatási eszközre vonatkozik. |

|

(40) |

A Bizottság először azt vizsgálja meg, hogy a szóban forgó intézkedések a Szerződés 107. cikkének (1) bekezdése szerinti állami támogatással járnak-e. A Bizottság ezután megvizsgálja, hogy a támogatást már végrehajtották-e, és az a belső piaccal összeegyeztethetőnek tekinthető-e. |

5.1. A Szerződés 107. cikkének (1) bekezdése értelmében vett állami támogatás megléte

5.1.1. Bevezetés

|

(41) |

Az EUMSZ 107. cikkének (1) bekezdése szerint „a belső piaccal összeegyeztethetetlen a tagállamok által vagy állami forrásból bármilyen formában nyújtott olyan támogatás, amely bizonyos vállalkozásoknak vagy bizonyos áruk termelésének előnyben részesítése által torzítja a versenyt, vagy azzal fenyeget, amennyiben ez érinti a tagállamok közötti kereskedelmet”. |

|

(42) |

Ebből következően ahhoz, hogy egy intézkedés állami támogatásnak minősüljön az EUMSZ 107. cikkének (1) bekezdése értelmében, az alábbi halmozott feltételeknek kell teljesülniük: i. az államtól vagy állami forrásokból kell származnia és az államnak betudhatónak kell lennie; ii. előnyt kell nyújtania egy vállalkozás számára; iii. szelektívnek kell lennie, vagyis előnyt kell nyújtania bizonyos vállalkozásoknak vagy bizonyos áruk termelésének; és iv. torzítania kell a versenyt, vagy a verseny torzításával kell fenyegetnie, és érintenie kell a tagállamok közötti kereskedelmet. |

5.1.2. Állami eredet: állami források használata és az államnak való betudhatóság

|

(43) |

Amint azt a Bíróság kimondta (18), az intézkedéseket akkor lehet az EUMSZ 107. cikkének (1) bekezdése szerinti állami támogatásnak minősíteni, ha a) azokat közvetlenül vagy a rá ruházott hatáskörében eljáró közvetítőn keresztül közvetve állami forrásokból finanszírozzák, és b) azok az államnak betudhatók. A tagállam fogalma a hatóságok összes szintjét magában foglalja függetlenül attól, hogy az országos, regionális vagy helyi szerv (19). |

5.1.2.1. Állami források felhasználása

|

(44) |

Az 1–5. intézkedés állami források felhasználásával jár, mivel állami tulajdonú szervezetek (MFB, MNV, Tiszavíz (20)) nyújtották azokat. |

5.1.2.2. Az államnak való betudhatóság

|

(45) |

A Bizottság megjegyzi, hogy Magyarország nem vitatja az öt fent említett intézkedés államnak való betudhatóságát. |

|

(46) |

Az illetékes minisztérium jóváhagyta az MNV és a Tiszavíz intézkedéseit. Ezenfelül a határozathozatali gyakorlat során (21) az MNV tekintetében már megállapítást nyert az államnak való betudhatóság, a Tiszavizet – amelynek részvétele főként […] jellegű volt – pedig az MNV képviselte. |

|

(47) |

Úgy tűnik, hogy az államnak tudható be 2. intézkedésnek az MNV és a Tiszavíz – két állami tulajdonban lévő társaság – általi, valamint a 3., 4. és 5. intézkedésnek az MNV általi biztosítása.

|

|

(48) |

Bár Magyarország nem állította, hogy az MFB-hitel nem az államnak tudható be, beadványa szerint az MFB-hitelről nem született külön kormányzati határozat. Mindazonáltal úgy tűnik, hogy az 1. intézkedés nyújtása és annak későbbi módosítása a Stardust Marine kritériumokon alapuló alábbi okokból az államnak tudható be (23):

|

|

(49) |

A fentiek alapján az öt intézkedés az államnak tudható be. |

5.1.3. Gazdasági előny

Előzetes megjegyzés

|

(50) |

Amint a (23) bekezdésben szerepel, Magyarország azt állítja, hogy az MGH 2013 óta már pozitív EBITDA-val rendelkezett volna, ha egyrészt 2013-tól […] a(z) […]-val/-vel újratárgyalt feltételek […], másrészt pedig saját maga érte volna el a Budport EBITDA-ját, ha alvállalkozásba adás helyett a társaságon belül biztosították volna a jegykiadási szolgáltatást [az MGH egyik kulcsfontosságú ügyfele] számára. Ezek az érvek azonban nem oszlatják el az MGH számára nyújtott előny esetleges fennállásával kapcsolatos aggályt. Magyarország ugyanis nem igazolta meggyőzően, hogy 2013-tól észszerűen elvárható volt egyrészt, hogy [az MGH egyik kulcsfontosságú ügyfele] észszerű időn belül hajlandó újratárgyalni a feltételeket oly módon, hogy az MGH-val megkötött szerződését nyereségessé tegye az utóbbi számára, másrészt pedig, hogy az MGH képes lett volna a társaságon belül legalább a Budporthoz hasonló hatékonysággal biztosítani a Budport szolgáltatásait. Mindenesetre, még ha a magyar hatóságok azt feltételezik is, hogy az MGH nyereséges lett volna [az MGH egyik kulcsfontosságú ügyfelével] 2017-ben ismételten újratárgyalt feltételek mellett, valamint akkor, ha saját maga végzi a Budport számára alvállalkozásba adott tevékenységet, az ilyen utólagosan kialakított érvelés nem releváns annak értékelése tekintetében, hogy milyen megfontolások vezérelték az intézkedések biztosítóit a döntéshozatal idején. |

|

(51) |

Ezen túlmenően a Bizottság a társaság finanszírozásával kapcsolatosan megjegyzi, hogy (a iii. pontban említett [0–400] millió HUF rulírozó hitel kivételével) a magyar hatóságok semmilyen bizonyítékot nem nyújtottak be arra nézve, hogy 2012 óta valamely magánbank vagy befektető az MNV-hez és az MFB-hez hasonló pénzösszeget (azaz mintegy 7 milliárd HUF) adott volna kölcsön az MGH-nek vagy fektetett volna be az MGH-ba: tehát az MGH által 2012 óta megkötött legtöbb finanszírozási szerződés, valamint a társaság teljes közép/hosszú távú finanszírozása láthatólag állami tulajdonban lévő szervezetek közreműködésén nyugszik. Következésképpen előzetesen úgy tűnik, hogy az MGH hosszú távú szükségleteit csak az állami tulajdonban lévő szervezetek beavatkozása tette lehetővé. Bár ez a megállapítás önmagában nem bizonyítja az MGH-nak nyújtott előny fennállását, rávilágít arra, hogy a társaság 2012 óta folyamatosan állami tulajdonban lévő szervezetek pénzügyi támogatására szorult. |

1. intézkedés: az MFB által 2012. április 27-én nyújtott 400 millió HUF összegű hitel és annak későbbi módosításai

|

(52) |

A következő okok miatt kétséges, hogy az MFB által nyújtott hitel és annak későbbi módosításai megfelelnek-e a piaci feltételeknek:

|

|

(53) |

A fentiek és különösen az (52) bekezdés ii. és iii. pontja alapján a Bizottságnak kétségei vannak afelől, hogy egy piaci hitelező hajlandó lett volna hitelt nyújtani. |

|

(54) |

Még ha egy piaci szereplő hajlandó is lett volna ilyen hitelt nyújtani, a Bizottság az (52) bekezdés iv. pontjában ismertetett indokok miatt előzetesen kétségbe vonja azt is, hogy a felszámított kamatteher mértéke összhangban volt az MGH hitelképességével és a hitel biztosítékokkal való fedezettségével. Tekintettel a biztosíték alacsony értékére, az MFB-nek – ha már nem tagadta meg a hitelt – legalább azt biztosítania kellett volna, hogy a kamatláb magasabb legyen, mint az 1000 bázisponttal megnövelt referencia-kamatláb. Mivel ez nem történt meg, úgy tűnik, hogy az MGH legalább a kamatláb-különbözetből fakadóan előnyhöz jutott. |

2. intézkedés: A Tiszavíz által nyújtott, 580 millió HUF értékű 2012-es tulajdonosi kölcsön, és annak MNV általi felvásárlása és részleges meghosszabbítása

|

(55) |

Kétséges, hogy ez – az MGH felvásárlása után két nappal nyújtott – tulajdonosi kölcsön megfelel a piacgazdasági szereplő elvének:

|

|

(56) |

A Bizottság előzetesen úgy ítéli meg, hogy a tulajdonosi kölcsön előnyt biztosított az MGH számára. |

3. intézkedés: az 580 millió HUF összegű tulajdonosi kölcsön 250 millió HUF összegű részleges tőkekonverziója

|

(57) |

Előzetesen úgy tűnik, hogy a 3. intézkedés az MGH-nak nyújtott előnynek minősül, mivel egy piaci szereplő csak akkor döntött volna a tőkekonverzió mellett, ha a jövőbeni tőkenyereség valószínűsíthetően meghaladta volna a kölcsön konverziója nélküli felszámolás nyomán az MGH eszközeiből befolyó bevételt.

|

|

(58) |

A Bizottság előzetesen úgy ítéli meg, hogy a 3. intézkedés előnyt biztosított az MGH számára. |

4. intézkedés: a 2015-ös tőkeinjekció

|

(59) |

A következő okok miatt kétséges, hogy ez az intézkedés megfelel a piacgazdasági szereplő elvének:

|

|

(60) |

A Bizottság előzetesen úgy ítéli meg, hogy a 4. intézkedés előnyt biztosított az MGH számára. |

5. intézkedés: a 2017. évi tőkeinjekció (5364 millió HUF összegű tőkeemelés)

|

(61) |

A Magyarország által szolgáltatott információk alapján a Bizottság előzetesen kétségesnek találja, hogy egy piacgazdasági befektető a rendelkezésre álló információk alapján végrehajtott volna egy ilyen befektetést. E megállapítás indokai a következők:

|

|

(62) |

A Bizottság ezért előzetesen úgy ítéli meg, hogy az 5. intézkedés gazdasági előnyt biztosított az MGH számára. |

5.1.4. Szelektivitás, a verseny torzítása és a kereskedelem befolyásolása

|

(63) |

Az intézkedéseket csak az MGH számára biztosították, és azok nem voltak elérhetőek a budapesti repülőtér földi kiszolgálási piacán tevékenykedő más társaságok számára. Amint azt a Bíróság megállapította, az egyedi támogatások esetében a gazdasági előny azonosítása főszabály szerint lehetővé teszi az intézkedés szelektivitásának vélelmezését (30). Az intézkedések tehát egyértelműen szelektívek voltak. |

|

(64) |

Emellett a földi kiszolgálás piaca nyitva áll a verseny előtt, és az MGH a Budporton kívül török és az egyesült királyságbeli társaságok uniós leányvállalataival is versenyez, ezért az intézkedések torzíthatják a versenyt és befolyásolhatják az Unión belüli kereskedelmet. Továbbá a budapesti repülőtéren – Magyarország legnagyobb repülőterén – keresztül Magyarországra érkező és azt elhagyó nemzetközi utasokat és árukat szállító légitársaságokat szolgál ki. |

5.1.5. A támogatás meglétére vonatkozó következtetés

|

(65) |

A 1–5. intézkedés az államnak betudható, állami forrásokat érint, és úgy tűnik, hogy szelektív gazdasági előnyt biztosít az MGH számára. Mivel az intézkedések torzítják a versenyt és befolyásolják az Unión belüli kereskedelmet, a Bizottság előzetesen arra a következtetésre jutott, hogy az intézkedések az EUMSZ 107. cikkének (1) bekezdése értelmében az MGH-nak juttatott állami támogatásnak minősülnek. |

5.2. A támogatás jogszerűsége

|

(66) |

A Bizottság megjegyzi, hogy az intézkedéseket a Bizottságnak történő bejelentést megelőzően, az EUMSZ 108. cikke (3) bekezdésének és az abban megállapított felfüggesztési kötelezettségeknek a megsértésével nyújtották. Ezért a Bizottság előzetes következtetése az, hogy az intézkedések az MGH-nak juttatott jogellenes állami támogatásnak minősülnek. |

5.3. Az összeegyeztethetőség előzetes értékelése

|

(67) |

A nehéz helyzetben lévő vállalkozások megmentéséhez és szerkezetátalakításához nyújtott állami támogatásokról szóló 2004. évi iránymutatás, valamint a nehéz helyzetben lévő, nem pénzügyi vállalkozásoknak nyújtott megmentési és szerkezetátalakítási állami támogatásról szóló iránymutatás (31) (a továbbiakban: a 2014. évi megmentési és szerkezetátalakítási iránymutatás) meghatározza a nehéz helyzetben lévő vállalkozások fogalmát a megmentési és szerkezetátalakítási támogatások összeegyeztethetőségének a Szerződés 107. cikke (3) bekezdésének c) pontja értelmében történő értékelése céljából. |

|

(68) |

A 2014. évi megmentési és szerkezetátalakítási iránymutatás 137. pontja értelmében „[m]inden olyan megmentési vagy szerkezetátalakítási támogatás belső piaccal való összeegyeztethetőségét, amelyet a Bizottság engedélye nélkül és ezáltal a Szerződés 108. cikke (3) bekezdésének megsértésével nyújtottak, a Bizottság ezen iránymutatás alapján vizsgálja meg, amennyiben a támogatás egy részét, illetve egészét az iránymutatásnak az Európai Unió Hivatalos Lapjában való közzététele után nyújtották”. |

|

(69) |

A 2014. évi megmentési és szerkezetátalakítási iránymutatás 138. pontja szerint „[a] Bizottság minden egyéb esetben a támogatás nyújtásának időpontjában alkalmazandó iránymutatás alapján folytatja le a vizsgálatot”. |

|

(70) |

Amint azt a (17) bekezdés kifejti, az 1–3. intézkedések végrehajtására 2012 és 2013 között, a 2014. évi megmentési és szerkezetátalakítási iránymutatás közzétételét megelőzően került sor. A 4. és az 5. intézkedést 2015-ben, a 2014. évi megmentési és szerkezetátalakítási iránymutatás közzététele után hajtották végre. |

|

(71) |

Az MGH 2012-ben és 2014 első félévében nehéz helyzetben lévő vállalkozásnak minősült a 2004. évi megmentési és szerkezetátalakítási iránymutatás értelmében, mivel saját tőkéje nem érte el a jegyzett tőkéje felét, és emellett jegyzett tőkéjének egynegyedét (25 millió HUF-ot) elvesztette az azt megelőző 12 hónapban. Amint azt Magyarország elismerte, az MGH 2014 második fele és 2016 között is nehéz helyzetben lévő vállalkozásnak minősült a 2014. évi megmentési és szerkezetátalakítási iránymutatás értelmében, mivel saját tőkéje ezen időszak alatt kevesebb volt, mint a jegyzett részvénytőke fele. |

|

(72) |

2013-ban és 2017-ben az MGH hivatalosan nem felelt meg a 2004. évi megmentési és szerkezetátalakítási iránymutatás 10. cikkének a) pontjában, illetve a 2014. évi megmentési és szerkezetátalakítási iránymutatás 20. cikkének a) pontjában foglalt kritériumoknak. Pénzügyi szempontból azonban ez csak a fent említett intézkedések miatt volt így. Az 5. szakaszban kifejtettek szerint a Bizottság úgy véli, hogy ezek a tőkeinjekciók állami támogatásnak minősülhettek, mivel kétséges, hogy azokat piaci feltételek mellett nyújtották. Így torzíthatták az MGH valós pénzügyi helyzetét, mivel az, hogy az MGH ezekben az években növelte saját tőkéjét, nem pénzügyi teljesítménye javulásának, hanem kizárólag olyan, az állam által nyújtott finanszírozásnak volt köszönhető, amelyre a vállalat piaci körülmények között nem lett volna képes szert tenni. Ezért a Bizottság úgy véli, hogy az MGH pénzügyi helyzetéről csak az intézkedések hatásainak kizárásával és az MGH korrigált saját tőkéjének kiszámításával lehet valós képet kapni. A Bizottság előzetes következtetése az, hogy az MGH 2013-ban és 2017-ben nehéz helyzetben lévő vállalkozásnak volt tekinthető, mivel a 2. és 4. intézkedés keretében végrehajtott tőkeemelés nélkül elvesztette volna jegyzett tőkéjének felét (lásd a korrigált tőke értékét az 5. táblázatban).

5. táblázat Az MGH korrigált tőkéje 2012 és 2017 között

|

||||||||||||||||||||||||||||||||||||

|

(73) |

Magyarország nem szolgált olyan indokokkal, amelyek alapján az intézkedések összeegyeztethetőnek minősülhetnének. |

|

(74) |

Mivel az MGH nehéz helyzetben volt, az 1., a 2. és a 3. intézkedés tekintetében a 2004. évi megmentési és szerkezetátalakítási iránymutatás, a 4. és az 5. intézkedés tekintetében pedig a 2014.évi megmentési és szerkezetátalakítási iránymutatás szolgálhat az összeegyeztethetőség alapjaként. Úgy tűnik, hogy az 1–5. intézkedés nem felel meg az említett iránymutatásokban foglalt összeegyeztethetőségi feltételeknek, nevezetesen a tényleges, valós és támogatástól mentes saját hozzájárulás követelményének (Magyarország a 2012–2017-es időszak tekintetében csak egyetlen magánfinanszírozásról – egy [0–400] millió HUF értékű rulírozó hitelről – tett említést, ezzel szemben az intézkedések összesített értéke körülbelül 7 milliárd HUF volt), a kompenzációs intézkedésekre vagy az „először és utoljára” elvre vonatkozó követelményeknek, tekintettel arra, hogy i. az intézkedéseket hosszú időn keresztül (2012 és 2017 között) biztosították, valamint arra, ii. hogy az intézkedésekre látszólag nem egyetlen szerkezetátalakítási művelet részeként került sor. Ezért úgy tűnik, hogy az 1–5. intézkedés nem egyeztethető össze a belső piaccal. A Bizottság azt is megjegyzi, hogy ez az előzetes következtetés akkor is változatlan maradna, ha az 1., 2. és 3. intézkedést a 2014. évi megmentési és szerkezetátalakítási iránymutatás szerint értékelné, figyelembe véve a hitelek 2014 utáni meghosszabbításait, amelyekre kiterjed az 1. és 2. intézkedés meghatározása. |

|

(75) |

A fent ismertetett okokból kifolyólag a Bizottság arra az előzetes következtetésre jutott, hogy komoly kétségek merülnek fel azzal kapcsolatban, hogy az intézkedések az EUMSZ 107. cikke (3) bekezdésének c) pontja értelmében összeegyeztethetők-e a belső piaccal, valamint felkéri Magyarországot és az érdekelt feleket észrevételeik megtételére. |

6. HATÁROZAT

Az említett megfontolások fényében a Bizottság az Európai Unió működéséről szóló szerződés 108. cikkének (2) bekezdés megállapított eljárásnak megfelelően felkéri Magyarországot, hogy e levél kézhezvételétől számított egy hónapon belül tegye meg észrevételeit, és adjon meg minden olyan információt, amely segítheti a jelen eljárás tárgyát képező intézkedések értékelését.

A Bizottság felkéri a magyar hatóságokat, hogy e levél másolatát haladéktalanul továbbítsák a támogatás potenciális kedvezményezettjének.

A Bizottság emlékeztetni kívánja Magyarországot, hogy az Európai Unió működéséről szóló szerződés 108. cikkének (3) bekezdése felfüggesztő hatállyal bír, és felhívja a figyelmet az (EU) 2015/1589 tanácsi rendelet 16. cikkére, amely előírja, hogy a jogellenes támogatást vissza lehet téríttetni a kedvezményezettel.

A Bizottság emlékezteti Magyarországot, hogy e levélnek és érdemi összefoglalójának az Európai Unió Hivatalos Lapjában történő közzététele útján tájékoztatni fogja az érdekelt feleket. Az Európai Unió Hivatalos Lapjának EGT-kiegészítésében való közzététel útján tájékoztatni fogja továbbá az EGT-megállapodást aláíró EFTA-országok érdekelt feleit, valamint e levél másolatának megküldésével az EFTA Felügyeleti Hatóságot is. Minden érdekelt felet fel fog kérni arra, hogy észrevételeit e közzététel időpontjától számított egy (1) hónapon belül tegye meg,

Ha e levél olyan bizalmas információt tartalmaz, amely nem hozható nyilvánosságra, kérjük, erről a kézhezvételtől számított tizenöt munkanapon belül tájékoztassa a Bizottságot. Amennyiben az említett határidőig a Bizottsághoz nem érkezik be indokolt kérelem, úgy tekintjük, hogy hozzájárult a levél teljes szövegének közzétételéhez.

Kérjük, hogy a kérelmet elektronikus úton küldjék meg a következő címre:

|

European Commission, |

|

Directorate-General for Competition |

|

State Aid Greffe |

|

1049 Bruxelles/Brussel |

|

BELGIQUE/BELGIË |

|

Stateaidgreffe@ec.europa.eu |

(1) Comunicação da Comissão — Orientações comunitárias relativas aos auxílios estatais de emergência e à reestruturação a empresas em dificuldade (JO C 244 de 1.10.2004, p. 2).

(2) Comunicação da Comissão — Orientações relativas aos auxílios estatais de emergência e à reestruturação concedidos a empresas não financeiras em dificuldade (JO C 249 de 31.7.2014, p. 1).

(*1) Bizalmas információ

(3) A Bizottság közleménye – A Közösség iránymutatása a nehéz helyzetben lévő vállalkozások megmentéséhez és szerkezetátalakításához nyújtott állami támogatásról (HL C 244., 2004/02. o.).

(4) Magyarország szerint [okok] miatt egy másik állami tulajdonban lévő vállalat, a Tiszavíz Vízerőmű Kft. (a továbbiakban: Tiszavíz) is részt vett az MGH felvásárlásában. A Tiszavíz 2012. október 31-én eladta az MGH-n belüli részesedését az MNV-nek, így az MGH az MNV 100 %-os tulajdonába került.

(5) A Budport szerint a WizzAir a budapesti repülőtér teljes utasforgalmának mintegy 40 % -át teszi ki.

(6) [Az MGH egyik kulcsfontosságú ügyfele] 2016. […]-án/-én írta ki a gyorsított tendert; a panaszos szerint [az MGH egyik kulcsfontosságú ügyfele] körülbelül [2 –5] évvel az MGH-val megkötött […] szerződésének rendes lejárata előtt tette közzé a gyorsított tendert; [az MGH egyik kulcsfontosságú ügyfele] az MGH pénzügyi nehézségei miatt írta ki a gyorsított tendert.

(7) A Budport ebben az időben olyan tevékenységeket végzett, amelyekhez nem volt szüksége földi kiszolgálási engedélyre, és a szükséges földi kiszolgálási engedélyek egy részét 2013-ban, más részét pedig 2015-ben kapta meg.

(8) Ellenkező jelzés hiányában valamennyi összeg HUF-ban értendő, és az annak megfelelő EUR-ban megadott összeg csak tájékoztatásul, 1 EUR = 305 HUF árfolyamon szerepel.

(9) Magyarország kifejti, hogy a felvásárlás azon alapult, hogy BDO diszkontált cash flow módszerek alapján megállapította az MGH értékét.

(10) A Bizottság közleménye a referencia-kamatláb és a leszámítolási kamatláb megállapítási módjának módosításáról (HL C 14., 2008.1.19. o.).

(11) Ez az MFB-hitel kintlevő egyenlegének behajtásához kapcsolódott.

(12) Nem számítva a 3. és az 5. intézkedés részét képező tőkekonverziót (2. intézkedés).

(13) A járatonkénti földi kiszolgálási díj az új szerződés alapján 2017 negyedik negyedévében [50 –200] EUR-val emelkedett 2016 negyedik negyedévéhez képest.

(14) Eredeti feltételek: biztosíték: valamennyi tárgyi eszköz a lízingelt eszközök kivételével (1 ranghely). […]

(15) A Bizottság közleménye a referencia-kamatláb és a leszámítolási kamatláb megállapítási módjának módosításáról (HL C 14., 2008.1.19.).

(16) A BDO 2012. áprilisi becslése szerint az MGH saját tőkéjének diszkontált cash flow megközelítés szerinti valós piaci értéke 2012. február 29-én [1000–2000] millió HUF volt. Magyarország szerint az MNV/Tiszavíz azért rendelte meg ezt a tanulmányt, mivel „tisztában voltak azzal, hogy az MGH »megmentése« állami támogatással kapcsolatos problémákat vethet fel”.

(17) Az üzleti terv két forgatókönyvet mérlegelt. Az első abból a feltételezésből indult ki, hogy a bevételek a jelenlegi bevételi struktúra szerint alakulnak. A második forgatókönyv esetében a vállalat figyelembe vette a […]-t is. A pénzügyi előrejelzés 2016-ig mindkét terv szerint viszonylag közel áll egymáshoz, és a második forgatókönyv esetében [0–1] millió HUF 2017-es üzemi eredményre vonatkozó kiegészítő előrejelzést tartalmaz.

(18) Lásd: C-482/99, Franciaország kontra Bizottság (Stardust Marine) ügy, ECLI:EU:C:2002:294.

(19) C-248/84, Németország kontra Bizottság ügy, ECLI:EU:C:1987:437, 17. pont.

(20) A Tiszavíz a 2. intézkedés időpontjában, 2012. június 16-án közvetlenül állami tulajdonban volt. (említést érdemel, hogy a későbbiekben a Tiszavíz az MNV közbeiktatásával közvetett állami tulajdonba került 2012. november 28-tól, amikor az MNV megvásárolta a Tiszavízen belüli állami részesedést).

(21) A Magyar Légiközlekedési Zrt.-ről szóló 2012. január 9-i határozat, SA.30584, HL L. 92., 2013.

(22) A Magyar Légiközlekedési Zrt.-ről szóló 2012. január 9-i határozat, SA.30584, HL L. 92., 2013.

(23) A Bíróság 2002. május 16-i ítélete, Franciaország kontra Bizottság, C-482/99, ECLI:EU:C:2002:294.

(24) Az MFB weboldalán 2018. szeptember 6-án található szöveg – https://www.mfb.hu/en/about-the-bank-s1812

(25) A Bizottság 2011/269/EU határozata (2010. október 27.) a Magyarország által a Péti Nitrogénművek Zrt. részére nyújtott C 14/09 (korábbi NN 17/09) állami támogatásról (HL L 118., 2011., 9. o).

(26) A Bizottság 2015. június 8-i határozata a Szlovénia által a Cimos csoport javára megvalósítani tervezett SA.37792. (2014/C) (korábbi 2013/N.) számú állami támogatásról.

(27) Magyarország tájékoztatása szerint az MFB 2012. május és 2016. június között általános minőségűnek, 2016. júliusban és augusztusban pedig magas minőségűnek értékelte a biztosítékot.

(28) T-93/17. számú Duferco Long Products SA kontra Európai Bizottság ügyben hozott, 2018. szeptember 18-i ítéletében a Törvényszék megállapította, hogy Belgium előnyhöz juttatta a Duferco Long Products vállalatot, mivel az FSIH, a SOGEPA leányvállalata (a Vallon régió teljes tulajdonában álló vállalat) nem felelt meg a piacgazdasági szereplő elvének, amikor 100 millió EUR összegű tőkeemelést hajtott végre a Duferco Long Products vállalatban. a Törvényszék úgy vélte, hogy a Bizottság helyesen ítélte elégtelennek a belga hatóságok által benyújtott tanulmányokat, amelyek nagyrészt a Duferco belső dokumentumain alapultak.

(29) A Deloitte kifejti, hogy az MGH reorganizációs tervére vonatkozó „magas szintű felülvizsgálat” egy „korlátozott felülvizsgálat”, amely nem helyettesíti a hitelintézetek esetében alkalmazott részletes átvilágítást.

(30) Lásd: a Bíróság 2015. június 4-i ítéletét, Bizottság kontra MOL, C-15/14 P EU:C:2015:362, 60. pont.

(31) A Bizottság közleménye – Iránymutatás a nehéz helyzetben lévő, nem pénzügyi vállalkozásoknak nyújtott megmentési és szerkezetátalakítási állami támogatásról, HL C 249., 2014.7.31., 1. o.

|

16.10.2020 |

PT |

Jornal Oficial da União Europeia |

C 346/27 |

AUXÍLIOS ESTATAIS — BÉLGICA

auxílio estatal SA.54915 (2019/N) — Mecanismo de remuneração da capacidade

Convite à apresentação de observações nos termos do artigo 108.o, n.o 2, do Tratado sobre o Funcionamento da União Europeia

(Texto relevante para efeitos do EEE)

(2020/C 346/03)

Por ofício de 21 de setembro de 2020, publicado a seguir ao presente resumo na língua que faz fé, a Comissão notificou a Bélgica da decisão de dar início ao procedimento previsto no artigo 108.o, n.o 2, do Tratado sobre o Funcionamento da União Europeia relativamente à medida acima mencionada.

As partes interessadas podem apresentar as suas observações sobre a medida em relação à qual a Comissão dá início ao procedimento no prazo de um mês a contar da data de publicação do presente resumo e do ofício que o acompanha, enviando-as para o seguinte endereço:

|

Comissão Europeia |

|

Direção-Geral da Concorrência |

|

Registo dos Auxílios Estatais |

|

1049 Bruxelles/Brussels |

|

BELGIQUE/BELGIË |

|

Fax +32 2 296 12 42 |

|

Stateaidgreffe@ec.europa.eu |

Essas observações serão comunicadas à Bélgica. As partes interessadas que apresentarem observações podem solicitar por escrito o tratamento confidencial da sua identidade e/ou de partes de observações apresentadas, devendo justificar o pedido.

RESUMO

1. Procedimento

A Bélgica notificou previamente a medida em 3 de julho de 2019. Foram trocadas várias listas de perguntas e respostas com as autoridades belgas e foram organizadas reuniões para debater o processo de notificação prévia. A Bélgica notificou a medida em 19 de dezembro de 2019.

2. Descrição da medida relativamente à qual a Comissão dá início ao procedimento

O mecanismo de remuneração da capacidade proposto visa garantir a segurança do aprovisionamento, tal como definido através de uma norma de fiabilidade prevista na lei da eletricidade de 29 de abril de 1999. A Bélgica identificou um risco para a segurança do aprovisionamento devido à futura eliminação progressiva do seu parque nuclear em 2025.

No mecanismo de capacidade belga, o operador da rede de transporte (ORT) compra a capacidade aos fornecedores de capacidade sob a forma de opções de fiabilidade. Os fornecedores de capacidade selecionados no leilão vendem as opções de fiabilidade ao ORT e recebem, em contrapartida, uma remuneração fixa da capacidade. Sempre que o preço de referência (ou seja, o preço da eletricidade para o dia seguinte) exceda um nível predefinido — o chamado preço de exercício —, o fornecedor de capacidade tem de devolver ao ORT a diferença entre o preço de referência e o preço de exercício.

O ORT organiza um leilão para o mecanismo de remuneração da capacidade em função do nível de recursos de capacidade necessários para garantir um nível satisfatório de adequação dos recursos para cumprir as normas de fiabilidade. O leilão de capacidade realiza-se todos os anos para o fornecimento num prazo de quatro anos («leilão Y-4»). No ano imediatamente anterior ao ano de fornecimento do leilão principal, realiza-se outro leilão («leilão Y-1»).

Os custos do mecanismo de remuneração da capacidade (ou seja, os incorridos para financiar pagamentos de capacidade aos prestadores) serão financiados com base numa «obrigação de serviço público» através das tarifas de rede dos ORT.

A base jurídica da medida é a lei da eletricidade de 29 de abril de 1999, relativa à organização do mercado belga da eletricidade, alterada por uma lei publicada em 16 de maio de 2019 no Jornal Oficial da Bélgica («Belgisch Staatsblad»/«Moniteur belge»). Será adotada legislação derivada sob a forma de aditamentos, decretos reais e regras de mercado, com vista a desenvolver as modalidades do mecanismo de remuneração da capacidade. Os projetos destes textos estão disponíveis no sítio Web do Ministério da Energia (1).

3. Apreciação da medida

3.1. Existência de um auxílio na aceção do artigo 107.o, n.o 1, do TFUE

A Comissão considera que o mecanismo de remuneração da capacidade é financiado a partir de recursos estatais, uma vez que é financiado a partir do produto de uma imposição parafiscal imposta pelo Estado e que é gerido e repartido de acordo com as disposições legislativas. A Comissão observa que os adjudicatários dos leilões recebem, através do mecanismo notificado, um rendimento que não receberiam se continuassem a operar no mercado da eletricidade em condições económicas normais, limitando-se a vender serviços de eletricidade e serviços auxiliares. Além disso, a medida apenas confere uma vantagem a determinadas empresas capazes de ajudar a resolver o problema de adequação identificado, que concorrem com outros produtores de eletricidade. A medida notificada irá, assim, conferir uma vantagem económica a empresas que se encontram numa situação factual e jurídica comparável à de outros produtores de eletricidade. A medida é, assim, seletiva. A produção de eletricidade, bem como os mercados grossistas e retalhistas da eletricidade, são atividades abertas à concorrência em toda a UE. Por conseguinte, uma vantagem proveniente de recursos estatais concedida a qualquer empresa desse setor pode afetar as trocas comerciais intra-União e falsear a concorrência. Consequentemente, a Comissão conclui que a medida constitui um auxílio estatal na aceção do artigo 107.o, n.o 1, do TFUE.

3.2. Legalidade do auxílio

Ao notificarem o regime antes da sua execução, as autoridades belgas cumpriram a sua obrigação decorrente do artigo 108.o, n.o 3, do TFUE.

3.3. Compatibilidade da medida

A Comissão apreciou a compatibilidade da medida com o mercado interno com base nas condições previstas na secção 3.9 das Orientações relativas a auxílios estatais à proteção ambiental e à energia 2014-2020 (2) (EEAG), que estabelecem condições específicas para os auxílios à adequação da produção e são aplicáveis desde 1 de julho de 2014. Em 2 de julho de 2020, a Comissão adotou uma comunicação que prorroga as EEAG até 31 de dezembro de 2021 e que as altera (3).

3.3.1. Objetivo de interesse comum e necessidade do auxílio

A Bélgica identificou a necessidade de um mecanismo de remuneração da capacidade num estudo de adequação e flexibilidade publicado em 2019 pelo ORT Elia (4). O estudo identifica riscos para a adequação dos recursos na Bélgica, remetendo para a norma nacional de fiabilidade descrita especialmente no cenário «EU-HiLo» (elevado impacto e baixa probabilidade a nível da UE), que pressupõe a indisponibilidade de várias unidades nucleares em França (para além da indisponibilidade «normal»). A Comissão considera que o recurso ao cenário «EU-HiLo» num mecanismo de capacidade que abrange o conjunto do mercado não parece adequado para determinar a dimensão do problema de adequação dos recursos, uma vez que corre o risco de sobreavaliar o problema e de falsear o mercado da eletricidade. A metodologia adotada no estudo da Elia foi criticada pela entidade reguladora nacional (CREG) (5).

Por conseguinte, a Comissão tem dúvidas quanto à questão de saber se o problema de adequação dos recursos foi identificado com suficiente precisão e se foi devidamente analisado e quantificado pelas autoridades belgas, em especial no que se refere aos pontos 221 e 222 das EEAG.

3.3.2. Adequação do auxílio

A Comissão tem dúvidas de que a medida seja adequada nos termos do ponto 226 das EEAG, tendo em conta a sua forma restritiva de calcular os limiares de investimento conducentes a contratos plurianuais (de três, oito ou quinze anos). Os limiares têm em conta a capacidade instalada (ou seja, a capacidade máxima que a unidade está concebida para explorar) e não a capacidade reduzida (ou seja, a sua taxa de disponibilidade predefinida e a sua contribuição para o objetivo de adequação dos recursos). A Comissão considera que esta característica pode impedir uma concorrência leal entre as tecnologias que contribuem de forma equitativa para a adequação dos recursos e desencorajar, em especial, a participação de tecnologias intermitentes com elevados fatores de redução (nomeadamente fontes de energia renováveis solares e eólicas intermitentes).

3.3.3. Efeito de incentivo

O objetivo da medida consiste em garantir a segurança do aprovisionamento, mantendo capacidades disponíveis suficientes. Sem um mecanismo de capacidade proporcionado, é provável que não exista capacidade suficiente para garantir a segurança do aprovisionamento, uma vez que as projeções indicam que uma percentagem significativa de centrais não consegue obter rendimentos suficientes para cobrir os seus custos de um mercado apenas centrado na energia. Além disso, a obrigação de reembolso cria um incentivo financeiro para estar disponível em situações de escassez. Por outro lado, a Bélgica criou um procedimento de controlo da disponibilidade antes e durante o período de entrega, bem como testes e sanções adequadas para assegurar o cumprimento da obrigação de disponibilidade. Por conseguinte, a Comissão conclui, a título preliminar, que a medida tem, em princípio, um efeito de incentivo.

3.3.4. Proporcionalidade

A Comissão procura obter esclarecimentos sobre se a medida é proporcionada em conformidade com a secção 3.9.5 das EEAG. A Comissão tem dúvidas sobre se: i) o procedimento de concurso é baseado em critérios não discriminatórios tendo em conta os limiares de investimento referidos na secção 3.3.2 supra; ii) a metodologia que define a curva da procura utilizada para calcular o volume de capacidade a adquirir em cada leilão é proporcionada, uma vez que pode basear-se numa sensibilidade EU-HiLo irrealista ou noutras sensibilidades baseadas numa indisponibilidade adicional das centrais nucleares francesas.

3.3.5. Prevenção de efeitos negativos sobre a concorrência e as trocas comerciais

A Bélgica aplicará um limite de preço intermédio às capacidades no âmbito dos contratos de um ano, a fim de evitar lucros inesperados. Por conseguinte, estas capacidades não serão autorizadas a apresentar propostas a um preço superior a este limite, nem a receber um preço de compensação superior a este limite. Não está prevista uma apreciação individual das capacidades para lhes conceder uma derrogação se se depararem com custos mais elevados.

Nos mecanismos de remuneração da capacidade, a capacidade indireta estrangeira será sujeita ao limite de preço intermédio. A Comissão considera, a título preliminar, que a conjugação da ausência de contratos plurianuais com a aplicação do preço intermédio impedirão estas capacidades de apresentar propostas no leilão que representem os seus custos reais, caso estes sejam superiores ao limite de preço intermédio. Por conseguinte, podem ser pura e simplesmente desencorajadas de participar no mecanismo de remuneração da capacidade. A Comissão considera que esta situação cria uma discriminação contra as capacidades estrangeiras, em violação do ponto 232 das EEAG.

Além disso, o ponto 233, alínea c), das EEAG prevê que os mecanismos de capacidade não devem «minar as decisões de investimento anteriores à medida». No entanto, o preço intermédio poderia ter o efeito de impedir as capacidades existentes de apresentar propostas que representem os seus custos reais, sem poder candidatar-se a contratos plurianuais, conduzindo à sua exclusão do mecanismo de remuneração da capacidade e até mesmo à sua saída do mercado da eletricidade. Por conseguinte, a Comissão procura obter informações adicionais para apreciar o efeito do limite de preço intermédio e a sua compatibilidade com este ponto das EEAG.

A Bélgica explicou que iria afetar as receitas de congestionamento resultantes da atribuição de bilhetes transfronteiriços (ou seja, dos direitos de acesso que permitem aos fornecedores de capacidade estrangeiros participar no mecanismo de remuneração da capacidade), tal como previsto no artigo 19.o, n.o 2, do Regulamento (UE) 2019/943 do Parlamento Europeu e do Conselho (6). A Comissão considera que são necessárias mais informações para apreciar a compatibilidade do mecanismo de remuneração da capacidade com o ponto 233, alínea a), das EEAG, ou seja, para assegurar que as receitas de congestionamento serão utilizadas de modo a que o mecanismo de remuneração da capacidade incentive de forma adequada o investimento em capacidades de interligação.

3.3.6. Conformidade da medida de auxílio com disposições intrinsecamente associadas do direito da União

Se uma medida de auxílio estatal implicar aspetos indissoluvelmente ligados ao objetivo do auxílio e que violem outras disposições do direito da União, tal violação pode afetar a apreciação da compatibilidade desse auxílio estatal. A este respeito, a Comissão conclui, a título preliminar, que o mecanismo de financiamento do mecanismo de remuneração da capacidade não cria quaisquer restrições que violem o artigo 30.o ou o artigo 110.o do TFUE, uma vez que a Bélgica permitirá a participação de capacidades estrangeiras no mecanismo de remuneração da capacidade. No entanto, a Comissão tem dúvidas quanto ao facto de o mecanismo de remuneração da capacidade estar em conformidade com o artigo 22.o, n.o 1, alínea c), e com o artigo 24.o, n.o 1, do Regulamento (UE) 2019/943, uma vez que tanto o estudo nacional de adequação e flexibilidade como o cenário de referência utilizado para determinar o volume de capacidade a leiloar se baseiam em pressupostos sobre o fornecimento estrangeiro de eletricidade (indisponibilidade adicional das centrais nucleares francesas).

Em conformidade com o artigo 16.o do Regulamento (UE) 2015/1589 do Conselho (7), qualquer auxílio ilegal pode ser objeto de recuperação junto do beneficiário.

TEXTO DA CARTA

|

Subject: |

State Aid SA. 54915 (2019/N) — Belgium Capacity remuneration mechanism |

Excellency,

The Commission wishes to inform Belgium that, having examined the information supplied by your authorities on the aid/measure referred to above, it has decided to initiate the procedure laid down in Article 108(2) of the Treaty on the Functioning of the European Union.

1. THE PROCEDURE

|

(1) |

Belgium pre-notified the measure on 3 July 2019. Several questions were sent to the Belgian authorities and meetings were organised to discuss the pre-notification file. |

|

(2) |

Belgium notified the measure on 19 December 2019. On the same day, Belgium exceptionally agreed to waive its rights deriving from Article 342 of the TFEU, in conjunction with Article 3 of Regulation 1/1958 (8) and to have this Decision adopted and notified in English. |

|

(3) |

A first formal request for information was sent to Belgium on 23 January 2020. Belgium replied on 19 March 2020 and provided updated documents on 20 April 2020. |

|

(4) |

A second request for information was sent on 29 May 2020 and Belgium replied on 9 July 2020. Belgium sent further information on 24 July 2020 and 13 August 2020. |

2. DETAILED DESCRIPTION OF THE MEASURE

2.1. Legal basis

|

(5) |

The legal basis of the measure is the Electricity Act of 29 April 1999 on the organisation of the Belgian electricity market modified by a law (9) published on the 16 May 2019 in the Belgian Official Gazette (‘Belgisch Staatsblad’/‘Moniteur belge’). On 24 July 2020, the Belgium authorities sent to the Commission a draft law modifying the law published on 16 May 2019. |

|

(6) |

Additionally, Royal Decrees and Market Rules will be adopted and will elaborate the Capacity Remuneration Mechanism (CRM) modalities further: the Royal Decree to determine the methodology for the capacity calculation and auction parameters in the context of the capacity remuneration mechanism (10), the Royal Decree on eligibility criteria related to cumulative support and minimal participation threshold (11), the Royal Decree on Investment Thresholds and Eligible Costs (12) and the Royal Decree on the determination of the conditions based on which capacity holders of foreign capacities can participate to the CRM (13). These texts are available on the website of the Ministry of Energy (14). Moreover, Market Rules are being consulted upon (15). |

2.2. Objective of the scheme

2.2.1. Reliability standard

|

(7) |

The primary objective of the proposed CRM is to ensure security of supply, as defined in a reliability standard. In the absence of harmonised European and regional reliability standards, the reliability criteria in Belgium is currently defined by a two-part Loss of Load Expectation (LOLE) criterion: the anticipated number of hours during which it will not be possible for all the generation resources available to the Belgian electricity grid to cover the load and need for operating reserves, taking into account also demand response, storage and interconnectors, for a statistically normal year shall not exceed 3 hours. As a second criterion, the LOLE shall remain below 20 hours for a statistically abnormal year (LOLE95) (16). These values are also enshrined in the Electricity law. |

|

(8) |

This standard has been set based on an estimate (17) of value consumers attach to avoiding disconnections of their electricity supply (the value of lost load or VOLL), and the expected cost of new capacity in Belgium (cost of new entry or CONE). In a study from 2017, the Federal Planning Bureau took 65 EUR/kW/y as an estimated value for the CONE in Belgium (18). In the same study, the Federal Planning Bureau estimated a Value of Lost Load for Belgium of 23,3 EUR/kWh. |

|

(9) |

The regulation (EU) 2019/943 (hereafter ‘electricity regulation’) provides the creation of an EU methodology for defining CONE, VOLL and reliability standards. At the time of the notification, the different methodologies were not available. Notwithstanding the fact that the methodologies are not yet finalised, Belgium explained that the estimation of the reliability standard is based on the latest available methodology proposal from ENTSO-E, the European Network of Transmission System Operators for Electricity. |

|

(10) |

Furthermore, Belgium explained that if by 15 September 2020 the new methodology indicated in recital (9) above has become applicable, a new reliability standard will be calculated and used for the determination of the capacity to be purchased in the first auction (see section 2.3.2 below). Otherwise, for the first auction, Belgium will use the LOLE value as fixed in article 7 undecies § 3 of the Electricity law and the new reliability standard will be used for the second auction. More generally, the calculations relevant for the CRM will be carried out based on the reliability standard in force on 15 September of the year preceding the auction. |

|

(11) |