EUR-Lex Access to European Union law

This document is an excerpt from the EUR-Lex website

Document 52022XC0805(04)

State aid – Czechia – State aid SA.58207 (2021/N) – Support for the construction and operation of a new nuclear power plant at the Dukovany site – Invitation to submit comments pursuant to Article 108(2) of the Treaty on the Functioning of the European UnionText with EEA relevance.

Pomoc państwa – Czechy – Pomoc państwa SA.58207 (2021/N) – Wsparcie dla budowy i działania nowej elektrowni jądrowej w Dukovanach – Zaproszenie do zgłaszania uwag zgodnie z art. 108 ust. 2 Traktatu o funkcjonowaniu Unii EuropejskiejTekst mający znaczenie dla EOG.

Pomoc państwa – Czechy – Pomoc państwa SA.58207 (2021/N) – Wsparcie dla budowy i działania nowej elektrowni jądrowej w Dukovanach – Zaproszenie do zgłaszania uwag zgodnie z art. 108 ust. 2 Traktatu o funkcjonowaniu Unii EuropejskiejTekst mający znaczenie dla EOG.

C/2022/4633

OJ C 299, 5.8.2022, p. 5–40

(BG, ES, CS, DA, DE, ET, EL, EN, FR, GA, HR, IT, LV, LT, HU, MT, NL, PL, PT, RO, SK, SL, FI, SV)

|

5.8.2022 |

PL |

Dziennik Urzędowy Unii Europejskiej |

C 299/5 |

POMOC PAŃSTWA – CZECHY

Pomoc państwa SA.58207 (2021/N) – Wsparcie dla budowy i działania nowej elektrowni jądrowej w Dukovanach

Zaproszenie do zgłaszania uwag zgodnie z art. 108 ust. 2 Traktatu o funkcjonowaniu Unii Europejskiej

(Tekst mający znaczenie dla EOG)

(2022/C 299/02)

Pismem z 30 czerwca 2022 r., zamieszczonym w autentycznej wersji językowej na stronach następujących po niniejszym streszczeniu, Komisja powiadomiła Czechy o swojej decyzji w sprawie wszczęcia postępowania określonego w art. 108 ust. 2 Traktatu o funkcjonowaniu Unii Europejskiej dotyczącego wyżej wspomnianego środka pomocy.

Zainteresowane strony mogą zgłaszać uwagi na temat środka pomocy, w odniesieniu do którego Komisja wszczyna postępowanie, w terminie jednego miesiąca od daty publikacji niniejszego streszczenia i towarzyszącego mu pisma na następujący adres lub numer faksu:

|

European Commission |

|

Directorate-General for Competition |

|

State Aid Greffe |

|

1049 Bruxelles/Brussel |

|

BELGIQUE/BELGIË |

|

Faks + 32 22961242 |

|

Stateaidgreffe@ec.europa.eu |

Otrzymane uwagi zostaną przekazane władzom Czech. Zainteresowane strony zgłaszające uwagi mogą wystąpić z odpowiednio uzasadnionym pisemnym wnioskiem o objęcie klauzulą poufności ich tożsamości lub fragmentów zgłaszanych uwag.

STRESZCZENIE DECYZJI

Władze czeskie zgłosiły przedmiotowy środek pomocy dnia 15 marca 2022 r.

Przedmiotem sprawy jest wsparcie państwa na rzecz budowy i działania nowej elektrowni jądrowej w Dukovanach o mocy do 1 200 MW. Główną podstawą prawną do realizacji tego projektu jest przyjęty we wrześniu 2021 r. akt w sprawie środków pomocy na rzecz przejścia Republiki Czeskiej do niskoemisyjnego sektora energetycznego.

Przedmiotowy środek obejmuje wsparcie trojakiego rodzaju:

|

— |

pożyczka państwowa (wsparcie finansowe podlegające zwrotowi) z niskim oprocentowaniem, pokrywająca prawie 100 % kosztów budowy, |

|

— |

umowa o odbiór w postaci umowy zakupu energii elektrycznej (PPA) zawarta pomiędzy beneficjentem a spółką celową należącą do rządu czeskiego i przez niego zarządzaną, w ramach której spółka celowa zobowiązuje się do zakupu całej energii elektrycznej wytworzonej przez beneficjenta po stałej cenie przez 60 lat. Spółka celowa sprzeda następnie tę energię elektryczną na hurtowym rynku energii elektrycznej, |

|

— |

zmiana prawa lub polityki w zakresie mechanizmu ochrony inwestorów w całym okresie inwestycyjnym. |

Beneficjentem środka pomocy jest podmiot o nazwie „Elektrárna Dukovany II” (EDU II), którego jedynym udziałowcem jest ČEZ. EDU II będzie beneficjentem pożyczki, operatorem elektrowni jądrowej, stroną umowy o odbiorze zawartej ze spółką celową oraz beneficjentem ochrony wynikającej ze zmiany prawa.

Celem przedmiotowego środka pomocy jest wypełnienie luki energetycznej, jaka ma się pojawić w latach 2030–2040 w wyniku likwidacji przestarzałych elektrowni jądrowych i węglowych w Czechach. Bezpieczeństwo dostaw energii, dekarbonizacja oraz dywersyfikacja źródeł energii to główne cele przyświecające tym działaniom.

Czechy planują rozpoczęcie rozruchu nowopowstałej elektrowni jądrowej w 2036 roku. Suma środków potrzebnych do budowy elektrowni szacowana jest obecnie na 7,74 mld EUR (według cen na 2020 r.), z czego 0,18 mld EUR będzie pochodzić z kapitału własnego CEZ, a 7,56 mld EUR pokryją środki z pożyczki państwowej.

W decyzji o wszczęciu postępowania Komisja stwierdziła istnienie pomocy państwa w rozumieniu art. 107 ust. 1 Traktatu o funkcjonowaniu Unii Europejskiej (TFUE). W odniesieniu do zgodności środka pomocy z art. 107 ust. 3 lit. c) TFUE Komisja stwierdza również niedoskonałość rynku oraz konieczność przyznania pomocy na rzecz rozwoju działalności gospodarczej.

Niemniej jednak Komisja ma wątpliwości co do następujących elementów oceny zgodności:

|

— |

odpowiedniość i proporcjonalność trzech elementów środka pomocy (PPA na wyjątkowo długi okres, pożyczka oraz zmiana prawa w zakresie mechanizmu ochrony uzupełniającego PPA), |

|

— |

ograniczenia zakłóceń konkurencji na rynku (test bilansujący), a dokładniej wybór ČEZ jako promotora projektu oraz czy negatywne skutki dla rynku zostaną ograniczone do minimum. |

PISMO

The Commission wishes to inform Czechia that, having examined the information supplied by your authorities on the measure referred to above, it has decided to initiate the procedure laid down in Article 108(2) of the Treaty on the Functioning of the European Union (TFEU).

1. THE PROCEDURE

|

(1) |

Following pre-notification contacts, pursuant to Article 108(3) TFEU, the Czech authorities notified to the Commission on 15 March 2022 their intention to provide support to the construction and operation of a nuclear power plant in Dukovany, Czechia (the ‘Project’). |

|

(2) |

Following the Commission’s questions sent on 21 April 2022, the Czech authorities replied on 5 May 2022. |

|

(3) |

On 16 May 2022, the Czech authorities exceptionally agreed to waive their rights deriving from Article 342 TFEU, in conjunction with Article 3 of Regulation 1/1958 (1) and to have this Decision adopted and notified in English. |

2. DESCRIPTION OF THE CONTEXT

2.1. Electricity generation in Czechia

|

(4) |

Czechia’s energy mix is currently dominated by coal- and nuclear-based electricity generation. The following table shows the evolution of the electricity generation capacity and gross electricity generation in Czechia between 2000 and 2021.

Figure 1 Evolution of electricity generation capacity in GW and gross electricity generation in TWh in Czechia, 2000-2021

Source: Czech authorities |

|

(5) |

In October 2019, CZ Transmission System Operator ČEPS presented a resource adequacy outlook (2), presenting two scenarios — Scenario A: baseline scenario which assumes electricity will be produced in modernised coal-power plants (Prunéřov II, Tušimice, Mělník I and Ledvice PP) and Scenario B: low-carbon scenario assuming that all coal power-plants besides new Ledvice PP will be phased-out. Both scenarios lead to adequacy issues (Scenario A: Loss of Load Expectation (‘LOLE’)= 256 hours/year in 2030, 678 hours in 2040 and Scenario B: LOLE=3 622 hours/year in 2040). Another more recent study also done by CEPS, called MAF CZ 2021 (3), detects problems with generation adequacy starting 2025 caused by rising imports to cover Czech demand to levels exceeding 20 %. Issues with electricity shortages occur through all scenarios starting 2035. |

|

(6) |

According to this, in 2025, exports will be reduced to 5,4 TWh with a total balance of 1,8 TWh in favour of Czechia. The balance would already be negative in 2030, with imports of 8,2 TWh of electricity and a total negative balance of 5,4 TWh in the baseline scenario. Under the 2030 low carbon scenario, the total negative balance would be of 9,2 TWh. While electricity production is expected to decline, consumption is expected to increase slightly from currently around 67 TWh to around 77,5 TWh in 2040, despite energy efficiency measures under Directive (EU) 2018/2002 of the European Parliament and of the Council of 11 December 2018 amending Directive 2012/27/EU on energy efficiency. |

|

(7) |

The Czech authorities explained that the decision to invest in new nuclear capacities was based, amongst others, on the results of the 2019 adequacy assessment, which was part of the key elements for quantifying the need for new investments in nuclear energy. This conclusion is consistent with the findings of the 2021 adequacy outlook of ČEPS. The later adequacy outlook (based on an assumption of a maximum import dependency at 10 % and including the new nuclear in its assumptions post 2035) stresses that the LOLE levels would remain unsatisfactory. |

|

(8) |

The studies presented by the Czech authorities take into account the expected cross-border flows between Czechia and its neighbouring countries. Czechia is currently a net exporter of electricity to countries in Central and Eastern Europe, but according to ČEPS, this would not last. The day-ahead electricity market is connected by Multi-Regional Coupling (4) based on the implicit allocation of cross-border capacity on the basis of net transmission capacity. In June 2022, the Core (5) Flow-Based Market Coupling project (6) is expected to go-live. Czechia will thus be fully integrated in electricity day-ahead and intraday markets, which will mean achieving the target model of the electricity market in the European Union as defined in the Commission Regulation (EU) 2015/1222 of 24 July 2015 establishing a guideline on capacity allocation and congestion management (7). |

|

(9) |

Although Czechia is well connected with surrounding countries, electricity flows vary considerably at different times of the year. The 2019 adequacy outlook has pointed out that in the Central European region (Core region for the calculation of transmission capacities), periods of electricity shortage in the system are expected to occur in several countries at the same time because of similar climatic conditions, coal phase out plans and supply shortages. (8) The Czech authorities consider that the decline in industrial production resulting from the expected shortage of electricity would result in weakening economic growth and the competitiveness of the Czech economy, which may also lead to major shortfalls on the revenue side of public budgets. Any power outages or its longer term shortage can thus have a significant impact on the social stability of the country with all the associated negative consequences. |

|

(10) |

The abovementioned studies set out that variable renewable energy sources (‘RES’) will not be able to cover the expected supply gap (recital (19)). Natural gas is found to not be suitable due to its high emission factor (499 tonnes CO2e/GWh vs. 29 by nuclear or 85 by solar within lifecycle) and gas import dependency. Gas dependency is generally higher during the winter as the RES are not producing enough electricity during that period, and heating increases demand. According to the abovementioned studies (see recital (5)), nuclear energy therefore emerges as a more secure option for future energy investments. |

|

(11) |

Furthermore, in view of the current geopolitical situation and its impact on (future) gas supply to the European Union in particular from Russia, higher electricity demand can be expected as a result of switching from gas-fired to electric heating. |

2.2. Objectives and background

|

(12) |

Among other things, the Czech authorities envisage addressing the security of supply concerns described above through investments in new nuclear power generation. Nuclear investment will also address decarbonisation, job creation and industrial competitiveness. The Project is part of a wider programme to support low carbon generation sources, aiming at nuclear power generation accounting for approximately 50 % of the overall generation capacity in Czechia. Indeed, the National Action Plan for the Development of Nuclear Energy (9) in Czechia, approved in June 2015, already elaborated on the strengthening of the role of nuclear power. |

|

(13) |

There are currently six nuclear power units operating in Czechia, in Temelín and Dukovany. According to Czechia, the existing four units at the Dukovany site are expected to shut down between 2045 and 2047. |

|

(14) |

The National Energy and Climate Plan (NECP) (10) for Czechia sets energy diversification targets for the share of individual fuels in (i) total primary energy sources (excluding electricity) and (ii) in electricity generation. The Czech authorities explained that the share of nuclear energy for 2020 was respectively 19,1 % and 36,9 %, while the target level for 2040 was set at 25–33 % in primary energy outside electricity and at 46–58 % for electricity generation. |

|

(15) |

An increase in the share of nuclear energy and renewable sources at the expense of fossil fuels is also considered essential in the NECP for achieving the long-term commitments to reduce greenhouse gas emissions. |

|

(16) |

Czechia has committed to become climate neutral by 2050. In order to achieve that goal, the structure of the Czech energy market and the sources of electricity generation will need to change significantly. High-carbon fossil electricity generating plants will need to be phased out, in parallel to the decommissioning of aging nuclear power generation capacity. |

|

(17) |

In the context of the scale of replacement capacity needs and the national security objectives, given the reliance of the Czech economy and industrial base on power resources, Czechia has concluded that substantial new nuclear replacement capacities are needed. |

2.3. Alternative options for security of supply

|

(18) |

The Czech authorities have examined several options for securing a low carbon energy mix, namely investments in RES, gas power generation, increase in imports, demand response and nuclear power. Extending the operation of gas, lignite and coal resources was excluded for environmental reasons and because of regulatory uncertainties and CO2 prices. |

|

(19) |

RES energy production in Czechia should increase up to 22 % by 2030, while the share of RES in electricity consumption is expected to represent 17 % (11). The Czech authorities evaluate the maximum wind energy potential at 2300 MW and the solar energy potential at 5800 MW. The maximum capacity factor for the use of photovoltaic power plants in Czechia is 1 000 hours per year (i.e. 11,4 % of the overall time), and for wind farms it is around 2 000 hours per year (i.e. 22,8 % of the overall time). The potential for biomass for electricity production is considered limited. For those reasons, renewables are not considered by the Czech authorities as sufficient to substitute the coal capacity to be phased out (12). |

|

(20) |

Furthermore, according to the estimations provided, natural gas-fired generation, including high efficiency power plants, should reach a share of 15 % of the total installed capacity of the Czech electricity system by 2040. The Czech authorities stress that Czechia is fully dependent on imports of natural gas from abroad with low diversification possibilities because of gas network limitations. Gas generation is therefore considered as offering limited self-sufficiency added value and thus cannot fully address the decrease of generation capacity because of coal phase-out in Czechia. |

|

(21) |

The Czech authorities considered to which extent imports can address the generation deficit. In that respect, they have set a self-sufficiency of electricity supply objective as maintaining a generation capacity on a permanent basis within the corridor of - 5 % up to + 15 % of the load of the system. However, the electricity generated in the coal-fired power plants and the existing nuclear reactors in Dukovany planned to be shut down would account for approximately 55 % of the domestic electricity consumption. According to the calculation of the grid model, it is technically possible to import approximately 20 TWh, which represents around 25-30 % of Czechia’s net energy consumption and which would not suffice to cover the capacity not available any longer because of the decommissioned generation sources. In addition, it is likely that the coal phase out in neighbouring countries also limits the available imports. |

|

(22) |

Finally, the development of a strategic nuclear capacity has been examined. Because of the geographical specificities and difficulties to develop large scale renewable projects in Czechia, nuclear has emerged as a favoured option for the Czech authorities. The long lifespan, low CO2 emissions, high utilisation factor of the capacity, high fuel concentration and its stable, reliable and predictable operation are seen as major advantages. The two nuclear power plants in Dukovany and Temelín are well connected to the industrial and research and innovation sites. For those reasons, the development of nuclear energy has been identified as a strategic objective, which adds to the other objectives of Czechia for addressing energy security and sustainability (increasing the share of RES, phasing out of coal power plants etc.). |

2.4. Alternative options on financing mechanisms for nuclear energy

|

(23) |

On 1 October 2021, Czechia adopted the Act on Measures for the Transition of Czechia to a Low-carbon Energy Sector (13) (‘Low-carbon Act’ or ‘LCA’). The LCA sets the framework for the construction and operation after 2030 of nuclear power plants above 100 MW in Czechia, including the Project (14). |

|

(24) |

Before adopting the LCA, the Czech authorities examined the efficiency of different support mechanisms for the development of nuclear investments. The options considered included tax credits, capacity mechanisms, direct investment aid (grants), setting a regulated investment prices (RAB) model (recital (28)), contract for difference and support through a low carbon electricity purchase contract between the State and an eligible investor. |

|

(25) |

The Czech authorities have used tax relief for the construction of electricity generating facilities for RES in the past, but found that that type of aid had significant impact on the national budget and had to be abolished. Furthermore, because of the major changes in market conditions and electricity price fluctuations, tax reliefs in themselves are not considered suitable for securing long-term project-specific investments. |

|

(26) |

Furthermore, the Czech authorities highlight that capacity mechanisms aim at compensating the readiness of plants to supply electricity in pre-defined periods, regardless of whether they produce or not. Thus, capacity mechanisms are not considered suitable for investments in nuclear resources, which aim at providing for stable and continuous low carbon energy sources in the national mix. |

|

(27) |

In addition, the Czech authorities envisaged using direct subsidies or public low-interest loans for the construction of a generation installation. Investment aid from the State budget or EU funds was considered as a secure and strong incentive for the realisation of a specific project allowing reasonable return on investment. Czechia also stresses that in 2014, a tender for the completion of the Temelín nuclear power plant was cancelled specifically due to the fact that there was no guarantee of return on investment. Support in the form of a loan also reduces the cost of financing and is therefore considered suitable for the development of nuclear investments. |

|

(28) |

The Czech authorities also envisaged a support mechanism on a RAB model. Under that model, the amount of the aid would take into account the investments made throughout the life-cycle of the resource, from construction to decommissioning. The price paid would be determined at regular intervals by an independent regulator taking into account efficient investments and other legitimate costs, including a reasonable profit level. A similar regulatory model is used to regulate the price of related electricity and gas transmission or distribution system services in Czechia (15). Under that option, the potential investor (most likely the incumbent ČEZ) would also sell the electricity produced on the markets itself. That model significantly reduces the investment risk and allows third-party financing, as the risk of increase of the capital costs (capital expenditure, CAPEX) and delays in completion are shared between the State and the investor. The price would be determined on a regular basis and would reflect the actual costs. However, since the electricity would be sold directly on the Czech market by the incumbent, there are risks, according to the Czech authorities, that that would reinforce the position of that incumbent and thus may raise competition concerns. They consider that those risks can be eliminated if the electricity is sold by a different entity. |

|

(29) |

The last option considered is a power purchasing agreement (‘PPA’) between the State and the eligible investor. A 100 % owned State entity would purchase the electricity produced at a predetermined strike price (i.e. the ‘PPA price’). The electricity would then be sold on the electricity markets. The PPA price would reflect the costs of the construction and operation. The PPA will also allow the operator to provision the costs for decommissioning. The contract examined in the context of the prior political discussion would be concluded for a minimum of 30 years and the costs for financing the measure might be either covered by the State budget or (in part or in full) passed on to consumers via a surcharge. That option would reduce the risks for the investor and guarantee a long-term, stable and secure operation of the power plant. |

|

(30) |

According to the Czech authorities, the PPA and a contract for difference both transfer the market price volatility risk to the State. They consider that the PPA with a special purpose vehicle (‘SPV’) further minimises the market impacts by avoiding strengthening the market power of the potential beneficiaries. Furthermore, unlike the RAB model, this option would allow to return the excess of profits to the State through the SPV. |

|

(31) |

That latter option was the preferred option for the Czech authorities for the adoption of the LCA, which is also the basic framework for the Project subject to the present State Aid decision. |

3. DESCRIPTION OF THE MEASURES

3.1. General description of the Project

|

(32) |

The notified measure covers the construction and operation of a new nuclear power plant at Dukovany site, Czechia, with a capacity of up to 1 200 MW. The LCA, which only creates a broad framework for support for nuclear investment, is not assessed as a scheme. |

|

(33) |

The State support consists of a package of three measures:

|

|

(34) |

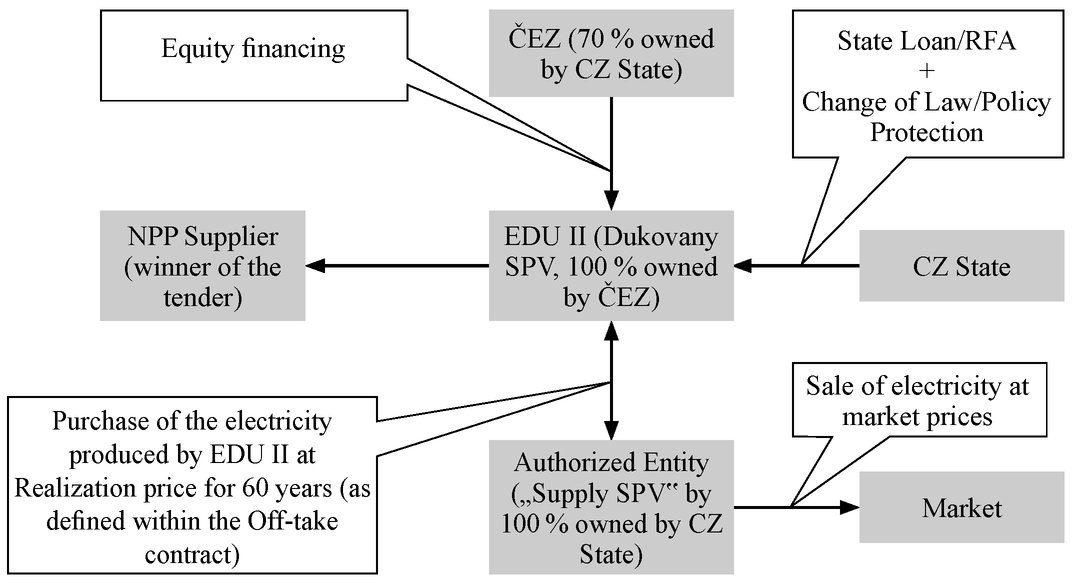

The beneficiaries (see also section 3.9) and the structure of the Project are summarised in the following figure:

Figure 2 Dukovany Project structure

Source: the Czech authorities |

|

(35) |

The life-cycle of the Project is divided in five stages:

|

|

(36) |

The new-built nuclear power plant is expected to be commissioned in 2036 and have a lifetime of 60 years. |

3.2. Technical characteristics

|

(37) |

The Project targets the construction of a III+ generation pressurised water reactor (PWR). A range between 850 MW to 1 200 MW is considered as offering sufficient technical solutions for the selection of the technology provider. The Czech authorities explain that the technology and delivery partners for the Project would be selected via a competitive and transparent tender process. |

|

(38) |

The engineering, procurement and construction (‘EPC’) supplier will be responsible for the engineering, construction and commissioning of the Project. Following the State decision to exclude applicants from States that are not party to the Agreement on Government Procurement (16), there are three possible technology choices:

|

|

(39) |

Other suppliers include suppliers who provide supplies with respect to the Project beyond the EPC supplier and who will be in a contractual relationship with EDU II. All those suppliers will support the Project during the pre-construction development and the operations stage. |

|

(40) |

The Czech authorities also explained that the Project would likely meet the technical screening criteria set out in point 4.27 of the proposed delegated act adopted pursuant to the Taxonomy Regulation (17), even though those are not yet in force. For example, the Czech authorities explain that there will be resources available at the end of the estimated useful life of the nuclear power plant corresponding to the estimated cost of radioactive waste management and decommissioning. Furthermore, the Czech authorities take into account of section 4.27 of the proposed Delegated Regulation for delegated act for the regulation of the final disposal facilities for the radioactive waste. As regards two criteria set out in the delegated act (namely, having a documented plan with detailed steps to have in operation, by 2050, a disposal facility for high-level radioactive waste, and use of accident-tolerant fuel from 2025), Czech authorities explain that they aim to realise the Project in line with those criteria. |

|

(41) |

The Czech authorities explained that because of the specificities of the Project in terms of essential national security interest, the State had to include conditions in the contractual framework, ensuring it has sufficient control on the Project. Those conditions are in particular set in a First Implementing Contract, including on confidential information sharing and State security matters. Within that contract, the parties consider that national security interest constitutes a valid reason for a derogation from the national public procurement rules based on Section 29(a) of Act No 134/2016 on Public Procurement (18) for the selection of a contracting party for the construction of the power plant. ČEZ and EDU II commit to discuss the tender organisation outside the Public Procurement Act regime with the national Office for the Protection of Competition and obtain a positive opinion before proceeding with the call for tenders. |

3.3. Measure 1: Offtake contract (PPA)

3.3.1. General principles for the offtake contract

|

(42) |

The first measure is a contract for the purchase of electricity from the plant (‘offtake contract’ or ‘PPA’). |

|

(43) |

According to Article 3 of the LCA, the Ministry shall submit a proposal for concluding a PPA to the nuclear power plant operator, which covers a number of elements, such as:

|

3.3.2. Financing of the offtake contract

|

(44) |

Article 9 of the LCA specifies that the financing of the support for nuclear energy may be covered by the Ministry from funds that are created by: (i) the revenues from electricity sales of the SPV; (ii) a levy (19) charged by the network operators to final electricity consumers, similar to the existing financing of RES; and (iii) contributions from the State budget. |

|

(45) |

Czechia argues that the choice between utilising taxpayers or consumers for any charges or rebates is a question of policy and should remain at the State’s discretion. The Czech authorities explained that they intend using all the revenue streams described in Article 9 LCA. The funds earmarked for financing measures for a transition to the low-carbon energy sector will be kept by the Ministry or by the SPV separately in special accounts at banks based in Czechia. |

|

(46) |

It is envisaged that the terms of the offtake contract would cover the operating period of the plant (currently estimated at 60 years). The law itself sets a contract duration of a minimum of 30 years with prolongation options. On the other hand, the Czech authorities explain that the planned contract duration for the Project is 60 years and that the contract provides neither for prolongation nor for shortening options. |

|

(47) |

The offtake contract will be concluded at a later stage, after selection of the technology and delivery partners and before the commissioning of the new built power plant and once the SPV has been established. |

3.3.3. The SPV

|

(48) |

As mentioned above, the offtake contract is planned between EDU II, the main beneficiary of the Project and the Ministry/ Czechia. All the electricity that will be produced by the beneficiary of the Project will be purchased by the SPV, a 100 % state-owned legal entity holding a license for trading with electricity. |

|

(49) |

The Czech authorities explained that the objective of that structure is to lower the risk of potential market distortions due to concentration of market power within the ČEZ Group. The SPV may contract in an open selection procedure a third party to assume contractually the electricity trading role on an arms-length basis. |

|

(50) |

The SPV will either sell the electricity on the wholesale market using its own trading desk, or externalise its operation by contracting with a third party, who will then undertake to sell the electricity on the market on behalf of the SPV. The SPV may also conclude bilateral contracts for the sale of electricity or hedging contracts with individual customers in addition to selling on the day ahead and intraday (spot) markets. |

|

(51) |

Czechia also explained that the SPV is expected to be set up not earlier than 2030, but not later than 12 months before the commissioning of the new nuclear power plant, especially to avoid unnecessary costs and due to uncertainties about the market and regulatory environment after 2030. |

|

(52) |

According to Czechia, the SPV will also be established in accordance with the applicable national and European Union law, i.e. ensuring in particular the principles of independence, competence and transparency. |

|

(53) |

There are no specific provisions on the marketing strategy of the SPV yet. Czechia evaluates different trading models based on the current market perspective and focuses on key principles to be pre-defined at the moment of its incorporation, while a certain degree of flexibility should be maintained to adjust the strategy to the market structure and conditions prevailing at the time close to the expected date of commissioning of the new nuclear power plant. According to Czechia, the trading model envisaged from the current market perspective is based on a conservative approach for a large base load power plant, with too much uncertainty regarding market design and structure after 2036. The SPV will enter into the following contractual agreements to execute its trading:

Figure 3 Envisaged contracts of the SPV

Source: Czech authorities |

|

(54) |

Czechia will ensure, when establishing the SPV, that it is not part of a vertically integrated group controlled by ČEZ. The corporate structure of the SPV will be construed under Act. No. 90/2012 Coll. on Commercial Companies and Cooperatives (Business Corporations Act), including rules of managerial duty of care by the members of the SPV’s bodies. The SPV’s supervisory board will be set up to ensure principles of competence and transparency in particular. Furthermore, an independent auditing committee should be setup to supervise all accounting and audit activities of the SPV. |

|

(55) |

Article 8 of the LCA sets the rules allowing the SPV to establish a charge that the transmission and distribution system operators can require from electricity consumers and pay the SPV back. The national energy regulator (the Energy Regulatory Office) would determine the method and timing of accounting and disbursing the levy to cover the relevant costs. |

|

(56) |

The SPV will be selling the electricity on the market, included through bilateral contracts.

|

|

(57) |

The offtake contract will contain a Minimum Output Volume for Day Ahead (Daily Forecast) and a Longer Period (an agreed output over an agreed period of time between the State and the investor), which EDU II will have to comply with. The Czech authorities explain that the power plant will be connected with a high load factor (90 %), which should ensure that there will be no motivation or incentive for market manipulation in the form of production volume adjustments. The PPA price, which will be EDU II’s only source of revenue, will only be payable on volume delivered, which — according to the Czech authorities — should guarantee that the maximum capacity will be used and outages would be prevented. |

|

(58) |

During the offtake period (currently estimated at 60 years corresponding to the economic lifetime of the project), electricity will be exclusively sold to the SPV owned by the State. After the offtake period, the EDU II may sell electricity directly on the wholesale market. |

|

(59) |

The Energy Regulatory Office shall determine the price components of transmission and distribution grid tariffs for support of electricity generation from low-carbon power plants in line with Act no. 165/2012. The components may have both positive and negative values. |

3.3.4. Price setting for the offtake contract

3.3.4.1.

|

(60) |

According to the Czech authorities, the purpose of the offtake contract is to provide a high degree of certainty over the level of revenues that EDU II will obtain over the duration of that contract. |

|

(61) |

Article 5 of the LCA reads as follows:

|

|

(62) |

The strike price of the contract will be determined in mutual agreement between the Czech government and EDU II, subject to adjustments (21), if the strike price is found to be disproportionate. According to the Czech authorities, the fixing of the offtake contract price level is based on a formula, i.e. a financial model that calculates the equity internal rate of return (IRR), taking into account several assumptions such as for capital expenditure, operating costs, financing or operation. The PPA price determines the revenue input for the model and it can be fixed in a way to ensure that the resulting equity IRR equals the specified target equity IRR for the investor. The EPC tender outcome will be a key input to determine actual parameters (such as for costs) in the model, while ensuring the minimum necessary total quantum is defined by the competitive market process. |

|

(63) |

Before the EPC tender outcome is known, the business plan uses indicative cost estimates based on benchmarking and public information available from the design, development and operations of existing plans. The overall capital expenditures, i.e. costs for construction (‘overnight cost’), are estimated at […], taking into account benchmarking based on similar technologies. The operating cost estimates include fuel costs, waste management fees paid to the State, operations and maintenance costs excluding fuel costs, and an ongoing reserving requirement for decommissioning and lifecycle renewal capital expenditures. In total, the Czech authorities estimate the operating costs at approximately […] (with estimates for fuel procurement costs of […], for decommissioning & waste management fee of […], for operation and maintenance costs of […] and ongoing renewal costs of […]), based on ČEZ’s current operating costs of ca. […] at the Temelin NPP and Dukovany NPP. |

|

(64) |

The off-take contract is intentionally designed to maintain both cost delivery and operating efficiency incentives for the investor and to allow a shortening of its term, if market conditions allow for it and upon common agreement of the parties to the offtake contract. The Czech authorities estimate that the strike price can be set at between 50 and 60 EUR/MWh with a contract duration of 60 years. |

|

(65) |

According to the LCA, the offtake contract shall stipulate ‘rules for the assessment of its proportionality by the Ministry to be carried out no later than 5 years from the beginning of the electricity supply from the low-carbon power plant to the electricity grid of Czechia, and then in regular intervals of at least once every 5 years’. |

3.3.4.2.

|

(66) |

The financial model discussed in recital (63) aims at estimating the PPA price necessary to achieve the target equity IRR for the investor. According to the Czech authorities, the target equity IRR for the investor is determined by comparison to the required return on equity (RoE). The Czech authorities explain that the State and the Project promoter, EDU II, have analysed the required RoE in line with accepted market practices: (a) bottom up analysis based on capital asset pricing model (‘CAPM’), and (b) benchmarking analysis referencing to other nuclear projects but also nuclear utilities and other infrastructure projects/investments with similar risk profile characteristics. |

|

(67) |

In ČEZ’s business plan submitted by the Czech authorities, the CAPM estimate for the required RoE falls within the range of [9,5 — 12 %] in the base case. This is based on contemporaneous risk free rates (Rf) of [0,4 — 0,8 %], a market risk premium (MRP) of [5,5 — 6,5 %], an unlevered beta of [0,40 — 0,55], gearing (= debt / (equity + debt)) of [55 — 65 %], and a nuclear construction and operating premium of [2,75 — 3,75 %]. |

|

(68) |

For the equity beta estimate, the business plan considers a range estimate based on the market cap weighted average and the median of a comparator set of betas. For this set, the Czech authorities explain that it considers a number of European listed energy utility companies (including ČEZ), refining the list to primarily consider betas for companies with nuclear energy operations in their portfolios. |

|

(69) |

The business plan explains that to incorporate risks specifically related to a NPP, the analysis includes a nuclear construction and operating premium. However, since the risk allocation of the Project has not yet been finalised between the stakeholders, ČEZ presents a preliminary estimate of this premium. According to the business plan, this range is provisional and would need to be refined once the risks of the Project are fully allocated. |

|

(70) |

According to the business plan, the Czech authorities explain than the required RoE is cross-checked based on RoE estimates from comparator benchmarks. According to the business plan, the findings from this comparison indicate that the RoE estimates for the Project are consistent with those of other NNPs, energy infrastructure projects and regulated returns for energy utilities in Czechia after taking into account the differences and risk and the risk return trade off. |

|

(71) |

The Czech authorities explain that the expected equity IRR range is set at [9 to 11] %, which sits at the lower end of the investor’s requirements for the Project according to the Czech authorities. By applying a realistic scenario (of 10 % cost-overrun) the equity IRR would fall to 7,2 %. |

|

(72) |

The Czech authorities claim that the rate of return projected as a target for the offtake contract is consistent with a range of analyses carried out to prepare the government for the offtake contract negotiations. |

|

(73) |

The Czech authorities submit that the preliminary analysis on envisaged Project costs indicates commercial returns are feasible for the investor under the terms of the offtake contract. |

|

(74) |

Moreover, the Czech authorities argue that based on varied power price projections from independent sources, preliminary analysis by the Czech authorities indicates feasibility of adequate returns for the State from onward power sales to the market to both compensate for the RFA and to deliver typical market level returns. |

|

(75) |

In particular, the State return would be driven by the following primary cash inflows:

|

|

(76) |

The pricing of the offtake contract would be set such that ČEZ, as an investor, receives the permitted equity return and such that the RFA is repaid. |

|

(77) |

In particular, the Czech authorities explain that the State, by taking on the merchant power price risk, may make a profit or a loss depending on the future evolution of power prices. the Czech authorities also explain that the investor was unwilling to take the risk of the project not to reach the necessary return of investment because of the too low market prices. |

|

(78) |

According to the Czech authorities, investments in nuclear sources are characterised by very high capital expenditure, long construction, and operational timelines. Nuclear power plant projects are considered by the Czech authorities as being exposed to significant political and regulatory risks throughout their asset life. Additionally, ongoing structural changes in the energy sector and developments in the electricity market add further complexity to long term investments. For those reasons, Czechia considers that nuclear power plants (‘NPPs’) require strong State support to compensate for the significant risks and uncertainty faced by investors. New nuclear generation construction projects across the world are supported by governments, and the aid package is a key project enabler as well as a political and economic necessity for long-term success. |

|

(79) |

Moreover, if all the power is sold under the offtake contract under favourable market conditions, this would not lead to overcompensation for the investor as that benefit remains with the SPV and EDU II receives the PPA price regardless of the market price. |

3.3.4.3.

|

(80) |

During the operating period, EDU II will be selling produced electricity exclusively to the SPV at a pre-agreed PPA price defined by the off-take contract with a duration of 60 years. The SPV will be selling the electricity on the market. After the PPA period, EDU II could sell electricity directly to the wholesale market or extend the PPA period with the SPV (only if asset life is extended beyond current technical assumptions). |

|

(81) |

Czechia explained that long term power price development in the operating period is of relevance for the ultimate returns to the State (market price can be higher or lower than the PPA price). Profit generated by the SPV would be ultimately passed on to the final consumers via a reduced cost of renewable financing. Given the very distant forecast period and the high level of interventions that were noted in the description of the project, relying on any such long term forecasts is a challenge for market participants. The price forecasts that are available publicly or through subscription, cover only the initial period of the operations. Therefore, long term forecasts that cover the operational lifetime of the plant are just inflation-linked extrapolations. |

|

(82) |

Noting those limitations, the State-level analysis has been conducted on a wide range of possible price levels and verifies meaningful positive returns. From first principles on price signals needing to cover the levelised cost base to incentivise any new entrants at or below the Levelised cost of electricity (‘LCOE’) of the price setting plant, it is rational to assume that market prices in the future would be set by peaking gas plants. This would imply higher long-term prices than the LCOE of a nuclear project (range of approximately 50 to 60 EUR/MWh on a range of credible assumptions) and hence a possible positive return for the State. The Czech authorities explain that the low price ranges compared to other nuclear projects were achieved thanks to the favourable financing conditions of the RFA and following the lessons learned through OECD countries (22). |

|

(83) |

According to the Czech authorities, the most current EY study ‘Analysis of electricity price development on the relevant EU markets by 2040’ from March 2020 has an estimation of wholesale electricity prices in 2040 around 90 EUR/MWh (at 2020 prices) (23). Other studies estimate for the relevant period a price level of electricity at 70 EUR/MWh (Aurora for Germany). Newest electricity forecast of ICIS (2020) expect for Czechia prices above 90 EUR/MWh already in 2030. |

|

(84) |

The Czech authorities explain that the offtake contract is based on assumptions that take into account the future decommissioning and nuclear waste levy costs. Those are part of the justified costs included in Section 5(1) of the LCA. The current estimate for decommissioning and waste management fees is included in the operational expenditures of the Project at 4 EUR/MWh as stated in a Business Plan elaborated by the investor and based on ČEZ experience at their other nuclear power plants. |

3.3.4.4.

|

(85) |

As per section 3(3)(e) of the LCA, the Ministry will have to carry out an assessment of proportionality of the strike price no later than five years from the beginning of the electricity supply and then in regular intervals of at least once every five years. The assessment will be based on the most recent version of the financial model by a reference to a threshold specified in the offtake contract of [9 to 11 %] equity IRR or the IRR which was subject to previous overcompensation settlement. If circumstances arise that lead to significantly stronger cash flows than assumed, the overcompensation mechanism will adjust the PPA price such as to share (50:50) the gain with the State and void excessive return on equity (24). |

|

(86) |

Overcompensation adjustments may take the form of PPA price adjustment or a lump sum to be paid to the State. |

3.4. Measure 2: State loan (repayable financial assistance, RFA)

|

(87) |

Czechia intends to provide a State loan, the RFA, of an expected amount of EUR 7,56 billion (exact loan amount will be defined based on the outcome of the tender and signature of the EPC contract) in order to finance the development of the Project. |

|

(88) |

According to Article 4 of the LCA, it is possible that the investor in nuclear generation obtains an RFA from the government. The LCA fixes the main terms for such an RFA as well as the modalities for its payment. The Czech authorities submit that such an RFA is necessary for the realisation of the Project. |

|

(89) |

The beneficiary will pay an interest rate of 0 % during the construction phase of the Project. The annual interest rate is set as a fixed one until the repayable financial assistance due date and corresponds to the amount of the state debt costs determined by the Ministry of Finance as a percentage rate for the given year and increased by 1 percentage point, with the annual interest rate to be at least 2 %. The RFA will be negotiated once the tendering process for the construction of the nuclear power plant is finalized. To the extent that the RFA would not be refinanced earlier, the Czech authorities estimate that the RFA would have a 30-year repayment period post commercial operation date on an amortising straight-line profile. |

|

(90) |

The RFA is expected to cover 100 % of the costs involved during Stages 2 and 3 (see recital (35)). The RFA will be secured by assets of EDU II and there will be no recourse to ČEZ or a guarantee by ČEZ for the RFA. |

3.5. Measure 3: Change of Law or Policy Protection mechanism

|

(91) |

The third measure for supporting the Project is a cost recovery protection for ČEZ in case Czechia decides to change national policy on nuclear energy or not to grant measures 1 or 2 or to stop the implementation by rejecting the bidders for the construction of the plant. As such, the Change of Law protection consists in a put option for ČEZ or a call option for the State in case certain circumstances occur. |

|

(92) |

This measure has a contractual basis. More specifically, the Czech authorities concluded with ČEZ and EDU II a Master Agreement and a First Implementing Contract setting the framework for cooperation on the Project, including the Change of Law or Policy Protection mechanism for the first Stage of the Project. |

|

(93) |

The Czech authorities explain that the Change of Law protection was necessary to enable the investment and to guarantee the protection of EDU II in relation to events beyond its control (e.g. in case of ‘Legitimate Grounds’ (25)). The aim of the risk sharing is to protect EDU II from certain risks (see annex). At the same time, EDU II will bear the risk of Project cost overruns for reasons other than Legitimate Grounds. |

|

(94) |

The First Implementing Contract fixes the procedures and modalities for renegotiation of the terms of the contract in case of Legitimate Grounds and on the sale of shares to the State for Legitimate Grounds during Stage 1 of the Project. The First Implementing Contract details the modalities of the share purchase arrangements in view of guaranteeing that the operation is neutral to both parties (e.g. by ensuring that the purchase price value corresponds to the funds invested in EDU II, that there are no revenue transfers from EDU II to ČEZ, etc.). The modalities to apply the risk sharing will be further detailed in the PPA/ offtake contract for the other Stages of the Project. |

|

(95) |

The Czech authorities explain that the objective of this measure is to minimise the amount of aid needed when determining the strike price by creating an acceptable framework of risk allocation. The impact of this measure is to limit the risk for the investor and at the same time to reduce the investment return range. The Change of Law protection aims at ensuring the overall acceptability of the Project for the investor and for the State. |

|

(96) |

The Czech authorities furthermore explain that the purchase price for the sale of all shares to the State until the end of Stage 1 is fixed at CZK 4 509 591 000 with a possible additional fee due to Legitimate Grounds not exceeding CZK 200 000 000 corresponding to the overall amount of capital contributions which ČEZ will provide. In a separate agreement, the parties have fixed the conditions under which those amounts will include an economic return of investment and the conditions under which they will not. As a general rule, if the Project is shut on Legitimate Grounds, a return of investment will also be due to ČEZ. |

3.6. Implementation of the different stages of the Project

|

(97) |

The First Implementing Contract regulates stage 1 of the Project, i.e. until selection of the EPC contractor. That step is expected in 2024. For the stages 2 and 3 of the Project (i.e. preliminary works, construction and commissioning) the First Implementing Contract provides that on or before 28 July 2024 the Second Implementing Contract or Power Purchase Agreement shall be signed and shall replace the First Implementing Contract. The contractual setup after 2024 currently under preparation includes a Power Purchase Agreement, an Investor Agreement and a decision of the State to provide the RFA. |

|

(98) |

The PPA will define obligations and rights of the State and of the investor (EDU II and ČEZ), including detailed specifications of protection of the investor in case of Legitimate Grounds occurrence as defined in the footnote 26. EDU II would be entitled to a compensation in case of cost increases in capital (CAPEX) or operating (OPEX) expenses or loss of Project revenue or other adverse impact on the Project due to Legitimate Grounds. Such compensation can be a lump sum payment of recalculation of the PPA price. The PPA would specify events or situations which trigger a put option of the investor or a call option of the State. Moreover, it provides the principles under which the price of such option shall be calculated. As mentioned in recital (88), the Government may decide to grant the RFA. This decision will contain conditions specifying the payments to the investor and then repayment of the RFA to the State, subject to the requirements set out in the LCA (see recital (87)). |

3.7. The national legal basis and transparency

|

(99) |

The national legal basis for this measure is the Act on Measures for the Transition of Czechia to Low-Carbon Energy and on Amendment of Act No. 165/2012. |

|

(100) |

The modalities for implementing the Project are set out in the Master Agreement between the Ministry and EDU II with the involvement of ČEZ and the First Implementing Contract between the Ministry and EDU II with the involvement of ČEZ. |

|

(101) |

The Project is made conditional in the Master Agreement on prior State aid approval. |

|

(102) |

The aid will also be governed by Act No. 218/2000 Sb., Act on Budgetary Rules and Amendment of Some Relating Acts (Budgetary Rules), as amended. |

|

(103) |

The Czech authorities explained that the information on the measure will be published on the Ministry website https://www.mpo.cz/cz/energetika/. |

3.8. Financing structure of the Project

|

(104) |

The estimated capital expenditures costs of the Project amount to EUR 7,74 billion. Those costs are distributed as follows:

Figure 4 Estimated costs of the Project during its construction period (stage 3)

Source: Czech authorities |

|

(105) |

The total funding requirement of the Project has been estimated at EUR 7,74 billion in nominal terms which will be financed via EUR 0,18 billion initial equity from ČEZ in stage 1 (26), and by a EUR 7,56 billion State loan, the RFA, in stage 2. |

|

(106) |

An additional EUR 1,77 billion committed contingent equity might be provided by ČEZ to finance any potential cost overruns not caused by Legitimate Grounds. The details on the approach for financing of any cost overrun will be agreed by ČEZ and the State. The total maximum equity commitment from ČEZ for the Project in the development and construction phase will be EUR 1,95 billion. |

|

(107) |

The Czech authorities explain that the overruns cap is the result of the commercial negotiation between parties and the result of effective and optimal risk allocation for the Project. They consider that the Project could not be realised with an open-ended financial commitment. |

|

(108) |

As mentioned under recital (63), the Czech authorities anticipate the construction costs of the Project to be […] (overnight, thus without interest during the construction period, at 2020 price level) and assume the operating costs to be around […] (at 2020 price level) comprising fuel, O&M, lifecycle renewal capex and decommission and waste management costs. In an alternative scenario (27), the Czech authorities estimate the construction costs for the Project, not related to overruns caused by Legitimate grounds, to be 10 % higher. |

|

(109) |

In case a Legitimate Ground is preventing or delaying the performance of any legal obligations of EDU II, EDU II will be excused from non-performance or delay in the performance of such legal obligations. In case of a Legitimate Ground leading to CAPEX/OPEX increase or loss of Project revenue or other adverse impact on the Project, EDU II will be entitled to monetary compensation. Such compensation can be a lump sum payment or recalculation of the PPA price. |

|

(110) |

The cost estimates are indicative at this stage and have been developed based on precedents. The actual costs will be determined by the outcome of the EPC tender and the technology selected. Over its 60-year asset life the Project will benefit from a 60-year power purchase agreement (PPA) with the State under which the State will commit to purchase the total electricity output generated by the Project. The PPA will be denominated in EUR and indexed in line with the assumed cost indexation. |

3.9. The beneficiaries

3.9.1. Selection of the beneficiary

3.9.1.1.

|

(111) |

The direct beneficiary of the measure is EDU II, a fully owned subsidiary of CEZ. EDU II has for purpose to construct and operate the new nuclear generation in Dukovany. It will conclude the offtake contract and receive the RFA. It is also the entity in charge of the construction and operation of the new nuclear installation. EDU II and ČEZ are also benefiting from investment protection under the Change of Law mechanism. |

3.9.1.2.

|

(112) |

EDU II is a fully owned subsidiary of ČEZ. ČEZ is the Project sponsor in charge of performing the strategic control and oversight for the Project, while EDU II is a separate entity with its own structure implementing the Project. EDU II will perform all the management functions with effective control and oversight by ČEZ. The Project will be overseen by two boards and an executive leadership team with experience in nuclear and conventional power plants. |

|

(113) |

ČEZ is the only nuclear plant operator in Czechia. It is a public company listed on the Prague and Warsaw Stock Exchanges and the parent company of the ČEZ Group operating in several European countries. Its majority shareholder is Czechia with 69,78 % and the shareholder rights are exercised by the Ministry. |

|

(114) |

The Czech authorities explain that the choice of the current Project model and of ČEZ as Project promoter was the result of a detailed assessment by the Government, but was not preceded by a tender, a selection process or a public call for expression of interest. |

|

(115) |

In June 2017, the Standing Committee for Nuclear Energy drafted and discussed a report (28), which summarised the analysis undertaken and the assessment of various investor models (including consortiums of private companies) and financing models considered for the Project. The report detailed three options. The first option was a private investor consortium with three sub-options: (i) investor consortium completely excluding participation from the Czech State or ČEZ Group; (ii) investor consortium with a minority stake held by ČEZ Group; (iii) investor consortium with a minority stake held by the State. This first option was not preferred because of the low control the State could exercise on the Project completion. The second option was to realise the Project fully by a separate State owned entity to be entrusted with the construction and operation of new nuclear power plant. While that option was considered as offering sufficient security, it was rebutted because of the high impact on the budget and the lack of sufficient technical knowledge. |

|

(116) |

The third option where ČEZ was the Project promoter (29) was considered by the Czech authorities as optimal since it provided the necessary State control (in particular through the SPV set up) and took advantage of ČEZ’s experience with the construction and operation of nuclear power plants. According to the Czech authorities, ČEZ is the most suitable entity to act as the developer and investor for the Project also due to the majority ownership interest held by Czechia represented by the Ministry in the company, which provides the Czech Government with comfort regarding national security aspects and availability of funds for the required equity capital. That option was approved following the Government Resolution No. 485 of 8 July 8 2019. |

|

(117) |

The Czech authorities explain that ČEZ has extensive experience in the market as a credible and capable nuclear power plant developer and operator in Czechia and is very familiar with the legislative and regulatory framework, including licencing procedures. As one of the ten largest energy companies in Europe, the ČEZ group has experience also in nuclear research, planning, construction and maintenance of energy facilities and the processing of energy by-products. Thus, the Czech authorities explain that ČEZ has highly qualified staff experienced not only in nuclear energy, but also in public procurement and negotiations, which should be an asset for the Project realisation. |

|

(118) |

According to the Czech authorities, the availability of suitable sites for the construction of a nuclear power plant and the economic rationality of its construction constitutes another important aspect. Czechia has limited geological, geographical and technical conditions for the construction of a new nuclear power plant as regards the stability of the subsoil, availability of water and the possibility of transmission of the produced power. The Czech authorities consider that the best conditions, verified by more than 30 years of operation of the existing units, are in Dukovany. |

|

(119) |

The Czech authorities explained that ČEZ has already undertaken enabling works on the site (such as feasibility studies, main site and adjacent land acquisition), which reduced the Project timeline by 10 to 12 years and potentially reduced the cost of the Project by several hundred million euros. |

|

(120) |

ČEZ/EDU II has already a number of essential licences and approvals for the realisation of the Project, such as an Environmental Impact assessment and siting permission according to Atomic Act and State Authorisation or a new nuclear power plant. The process for obtaining building licence and planning permission, required under national rules, is also progressing. |

|

(121) |

The Czech authorities explained that the country’s economy is largely exposed to the threats from the external sources for provision of energy resources. The public ownership of the majority of ČEZ shares is an important aspect of the selection, not only from the perspective of ensuring national security interests are safeguarded. |

|

(122) |

By expanding the nuclear generation capacity in the Group portfolio to replace the forecast decommissioning of some of the existing generation capabilities, the Project forms a central part of ČEZ’s medium to long-term business strategy. |

|

(123) |

Finally, Czechia contends that there was no viable alternative to ČEZ. |

3.9.1.3.

|

(124) |

The Czech authorities explained that the two beneficiaries EDU II and ČEZ will be governed independently from each other for the following reasons. |

|

(125) |

First, there will be clear legal and financial separation between EDU II and ČEZ. The governance structure (30) should ensure EDU II’s independence from ČEZ and effectively eliminate the incentives for ČEZ to unduly interfere in EDU II’s day-to-day operation. |

|

(126) |

Second, the terms of the offtake contract will aim to safeguard the State’s interest for securing supplies. This implies that there would be clauses on daily output forecasts and longer-term output forecast details (to be further negotiated) and related penalty mechanisms. In any event, the State could, through its ownership in ČEZ (31), also interfere directly in case there are actions taken that undermine the full operation of the EDU II power plant. |

|

(127) |

Third, Czechia explains that there is a strong economic incentive for EDU II to produce at full capacity and receive the offtake contract price. This is the only source of revenue of EDU II. Therefore, any reduction in EDU II output will mean lost cash flows and potential financial issues given the low headroom for profitability under which the Project operates at the currently proposed 50 — 60 EUR/MWh price (at 2020 prices). EDU II’s operating margin is estimated at 45 % on average. The operating margin would drop to 6 % once the cost and repayment of the RFA are included. A reduction in load factor from the anticipated 90 % below 84,6 % would eliminate the cash available for debt service and potentially result in EDU II not being able to service the RFA, while a reduction below 50 % would lead to cash flows not being sufficient to cover operating costs. Any activity aiming at reducing EDU II revenues would therefore be against the company’s economic interest. |

|

(128) |

Fourth, Czechia explains that the Project is of critical importance to ČEZ Group’s generation portfolio and financial results, especially after the coal and Dukovany I retirement. According to the Business Plan, the ČEZ Group estimates the EDU II’s average annual EBITDA over the life of the Project to represent an increase of approximately 24 % to the current Group EBITDA (assuming full consolidation). As such, revenue from EDU II represents a critical stream of income for ČEZ. In fact, instead of being incentivised to curtail production, ČEZ would be negatively impacted from any production curtailment. |

|

(129) |

Fifth, nuclear power plants have low operating costs and are not technically designed to accommodate regular significant changes in output volume, which makes curtailment, even under unfavourable market conditions unlikely. |

3.9.1.4.

|

(130) |

EDU II will conclude a PPA with the State and with the SPV under Article 6 of the LCA. If the electricity prices are above the PPA price, the SPV will function autonomously and will not require any additional resources from the State. However, if the PPA price is above the market prices of electricity, the State will need to finance the price difference through State resources, namely through the State budget and/or through consumption levies. Article 8 of the LCA leaves the option for the State to use any of those or both financial mechanisms. The Czech authorities explain that it would likely be a combination of both State budget and specific levies. |

|

(131) |

The design of Measure 1 has as effect to channel the cash flows through the SPV (see section 3.3.3.). The SPV will therefore assume the losses and receive revenues from selling to the market the electricity produced by EDU II. In favourable market conditions, the SPV will therefore retain the gains from the activity of electricity sales. The Czech authorities explain that these revenues will be eventually fed into the State budget since the SPV will be fully owned and controlled by Czechia. |

3.9.2. Preparatory work for the Project

|

(132) |

In view of the need for new nuclear capacity, ČEZ approved an initial business plan in 2010 for adding up to 1 200 MW capacity to the Dukovany NPP by 2036. A feasibility study for the expansion of the current nuclear capabilities at the Dukovany site was completed in the same year. A detailed business plan prepared by CEZ was submitted to the Commission in June 2021. |

|

(133) |

ČEZ started acquiring the land necessary for the Project already in April 2008, process which has been almost completed at the date of adoption of this decision. |

|

(134) |

The Project had to undergo an Environmental Impact Assessment (EIA) to identify, describe and comprehensively assess the foreseeable impact on the environment and public health. The process began in early 2016 and included international consultations and public discussions in 2018. The EIA was followed by a positive independent assessment and the Ministry of Environment issued a positive binding statement on the Project’s EIA in August 2019 (32), a necessary step to start the Project’s permitting. |

|

(135) |

In March 2020, ČEZ and EDU II started the process to assess the site for a nuclear installation in terms of nuclear safety, radiation protection, technical safety, radiation situation, monitoring, radiation extraordinary event management and security during the life cycle of a nuclear installation. EDU II obtained license for the siting of the nuclear installation in March 2021, which is the first license required for a new nuclear unit. |

3.10. Market impact of the Project

|

(136) |

With respect to the effect of the Project on competition and trade, Czechia argues as follows:

|

4. ASSESSMENT OF THE MEASURES

4.1. Scope of the decision

|

(137) |

The scope of the decision covers measures 1, 2 and 3 described above. |

|

(138) |

As regards the financing of measures 1, 2 and 3, the decision on whether any levy will contribute to financing part of the measures has not been taken yet. Potential exceptions from any such possible levy are thus not in the scope of this decision. |

|

(139) |

Furthermore, measures 1 to 3 ensure that a new nuclear power plant will be able to generate electricity and sell it through the SPV on the market. The effects of these measures should therefore be assessed with respect to the potential distortions of the electricity markets. The construction works (and associated tender procedure) are not covered by the measures 1 to 3 and not subject to the present notification. Those works can be dissociated from the measures 1 to 3 to the extent that the tender winners will not be the beneficiaries of the notified aid, but it will be CEZ through EDU II. The presence of aid is analysed for measures 1 to 3 and the construction works will be organised afterwards by EDU II. |

|

(140) |

Finally, as precised under the footnote 26, the equity contribution of CEZ to the project was not notified as aid and does not fall within the scope of this decision. In any event, CEZ seems to be acting as a private investor by contributing to this project as mentioned under the recital (105). Moreover, there is no indication that the contribution could contain State resources. |

4.2. Existence of Aid

|

(141) |

Under Article 107(1) TFEU, any aid granted by a Member State or through State resources in any form whatsoever which distorts or threatens to distort competition by favouring certain undertakings or the production of certain goods, in so far as it affects trade between Member States, is incompatible with the internal market. |

|

(142) |

In determining whether a measure constitutes State aid within the meaning of Article 107(1) TFEU, the Commission has to verify whether:

|

|

(143) |

The three measures notified were planned together. Measures 1 and 2 were established by the same legislative act, the LCA (see recitals (43) and (88)). Measure 3, the ‘Change of Law or Policy Protection mechanism’, has a separate contractual basis (recital (92)). Nevertheless, measure 3 is entirely linked to measures 1 and 2 and would not exist in the absence of those measures. Notably, measure 3 has the objective to minimise the amount of aid needed when determining the strike price under measure 1 (see recital (91)). Those three measure are inseparable from each other. Under point 81 of the Commission’s Notice on the Notion of Aid, different measures could be considered as a ‘single intervention’. This could be the case, in particular, where consecutive interventions are so closely linked to each other, especially having regard to their chronology, their purpose and the circumstances of the undertaking at the time of those interventions, that they are inseparable (33). For instance, a series of State interventions which take place in relation to the same undertaking in a relatively short period of time, are linked to each other, or were all planned or foreseeable at the time of the first intervention, may be assessed as one intervention. |

|

(144) |

All three measures have the same subject matter and objective, namely to enable the construction and operation of a new nuclear power plant at Dukovany site. The measures are planned and negotiated together in a way that each measure has a direct impact on the others, and that the measures jointly create the financial preconditions to enable construction and operation of the plant. It is undisputed that the grantor of the measures 1 to 3 is the Czech State and that chronologically they coincide. More specifically, all the interventions were planned (and were thus foreseeable when negotiated) together (34). For example, lowering the commercial risks through a Change of Law Protection mechanism and lowering initial capital requirements through the RFA impact the amount of aid needed for the offtake contract. The three measures at issue are closely linked and it would have been impossible to separate them. The Commission considers therefore that the three measures should be examined together as a single intervention, as they are interdependent and have mutually enhancing effects for the performance of the Project. |

4.2.1. Imputability and existence of State resources

|

(145) |

For advantages to be capable of being categorised as aid within the meaning of Article 107 TFEU, they must be granted directly or indirectly through State resources. It is established case-law (35) that measures financed through compulsory charges imposed by the legislation of the Member State, managed and apportioned in accordance with the provisions of that legislation, may be regarded as State resources within the meaning of Article 107(1) TFEU even if they are managed by private or public entities separate from the public authorities. |

|

(146) |

Furthermore, it is not necessary to establish, in all cases, that there has been a transfer of State resources in order to assess the measure as State aid within the meaning of Article 107(1) TFEU (36). |

|

(147) |

For advantages to be capable of being categorised as aid within the meaning of Article 107 TFEU, they must be granted directly or indirectly through State resources. This means that both advantages which are granted directly by the State and those granted by a public or private body designated or established by the State are included in the concept of State resources within the meaning of Article 107(1) TFEU. |

|

(148) |

The combination of measures for this Project has been decided by the State with the adoption of the LCA (see recital (32)) and the conclusion of the Master Agreement and First Implementing Contract (see recital (100)). The offtake contract will also involve the creation of a fully State-owned entity, the SPV (see recital (33)(32)1)). The granting authority for all measures is the Czech State acting through the Ministry. |

|

(149) |

The Czech authorities do not contest that the measures will be financed from resources under the control of the State. As mentioned in recital (44), Article 9 of the LCA specifies that new nuclear power generation can be financed through one or a combination of: (i) the revenues from electricity sales of the SPV, (ii) a price component charged by the transmission and distribution system operators on network users, if so decided, and (iii) contributions from the State budget. The choice of the actual revenue stream for financing the different measures depends on the choice of the Ministry. It is undisputed by the Czech authorities that all revenue streams are or will be controlled by the State. |

|

(150) |

Furthermore, Article 4 LCA specifies that the RFA would be provided from the State budget (see recital (88)) and will be granted by the Czech national bank. |

|

(151) |

In the light of the above, the Commission considers that the measure is granted through State resources and is imputable to the State within the meaning of Article 107(1) TFEU. While the Commission considers that all measures should be analysed as a single intervention (see recitals (143) to (144)), it should be noted that also all three measures individually are granted through State resources and imputable to the State. The offtake contract financing is partly based on the State budget and implemented by the fully state-owned SPV, the State loan is granted from the State budget, and the Change of Law provision transfers risk to the State (see recital (96). All measures are based on law (measures 1 and 2) and a contract signed by the State (measure 3). |

4.2.2. Selective economic advantage

|

(152) |

The specific measures described in section 3 target selectively the Project, namely the construction of a new nuclear power plant at the Dukovany site. The measures, taken as a whole, allow the Project to be realised and provide for a reasonable return of investment (see recital (61)). As argued by the Czech authorities, the measures aim to enable an investment that, due to the specific risks and the long Project duration, would not have been undertaken by a private investor under normal market conditions, that is to say in the absence of State intervention. |

|

(153) |

It follows that the measures at issue confer a selective advantage within the meaning of Article 107(1) TFEU. All three measures separately would also confer an economic advantage. Measure 1 provides a stable long-term purchase price for electricity that would not, at least not for such a duration, be available on the market. Measure 2 provides an RFA with zero interest during the construction phase of the Project. Measure 3 provides protection in case of change of law or policy, thereby reducing investment risk and transferring it to the State and conferring an economic benefit that could not have been obtained under normal market conditions. |

4.2.3. Threat of distortion of competition and effect on trade

|

(154) |