EUR-Lex Access to European Union law

This document is an excerpt from the EUR-Lex website

Document 32013Y0425(01)

Recommendation of the European Systemic Risk Board of 20 December 2012 on funding of credit institutions (ESRB/2012/2)

Recommendation of the European Systemic Risk Board of 20 December 2012 on funding of credit institutions (ESRB/2012/2)

Recommendation of the European Systemic Risk Board of 20 December 2012 on funding of credit institutions (ESRB/2012/2)

OJ C 119, 25.4.2013, p. 1–61

(BG, ES, CS, DA, DE, ET, EL, EN, FR, IT, LV, LT, HU, MT, NL, PL, PT, RO, SK, SL, FI, SV)

In force

In force

|

25.4.2013 |

EN |

Official Journal of the European Union |

C 119/1 |

RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

of 20 December 2012

on funding of credit institutions

(ESRB/2012/2)

2013/C 119/01

THE GENERAL BOARD OF THE EUROPEAN SYSTEMIC RISK BOARD,

Having regard to Regulation (EU) No 1092/2010 of the European Parliament and of the Council of 24 November 2010 on European Union macro-prudential oversight of the financial system and establishing a European Systemic Risk Board (1), and in particular Article 3(2)(b), (d) and (f) and Articles 16 to 18 thereof,

Having regard to Decision ESRB/2011/1 of the European Systemic Risk Board of 20 January 2011 adopting the Rules of Procedure of the European Systemic Risk Board (2), and in particular Article 15(3)(e) and Articles 18 to 20 thereof,

Whereas:

|

(1) |

Funding conditions for credit institutions have been significantly affected by the current crisis. Credit and interbank markets have remained impaired as a result of the strong links between credit institutions and sovereigns as well as the uncertainties over asset quality and the sustainability of some credit institutions’ business models. Credit institutions have responded to this situation by making changes to their funding structures and asset portfolios. |

|

(2) |

On 29 June 2012 the euro area summit took an important step towards breaking the negative link between sovereigns and credit institutions. It envisaged a single supervisory mechanism and the direct use of European funds from the EFSF and ESM for bank recapitalisation/bailout and resolution. However, certain credit institutions still weigh negatively on sovereigns, and vice versa. This vicious circle needs to be broken in order to bring about the better functioning of the funding markets. |

|

(3) |

In order to improve funding conditions it is necessary to re-establish the resilience of credit institutions and confidence in them. The recommendation of the European Banking Authority (EBA) for a minimum 9 % Core Tier 1 capital ratio for credit institutions (3) has partly contributed to this aim. However, the current macroeconomic outlook imposes further strains on credit institutions’ balance sheets. |

|

(4) |

The ongoing reform of the European Union regulatory regimes governing credit institutions (CRD IV package (4), in particular its provisions regarding the liquidity regime and the framework for recovery and resolution (5)) remains at the negotiation stage. The date on which the proposed packages will receive final approval and enter into force remains uncertain, as does the nature of the interrelations among the different instruments. Achieving clarity as to the regulatory framework would be beneficial not only for the credit institutions subject to it but also for investors. |

|

(5) |

While public authorities, in particular central banks, have used extraordinary measures to reduce funding strains and create the conditions for credit institutions to strengthen funding structures in the future, credit institutions also need to actively strive to achieve sustainable funding structures. |

|

(6) |

The monitoring and assessment of credit institutions’ funding risks and funding risk management by national supervisory authorities is fundamental to the evaluation of the institutions’ capacity to execute their own funding plans and reduce reliance on public sector funding sources. Likewise, the monitoring by national supervisory authorities of the recourse to innovative instruments and to the provision of uninsured deposit-like financial instruments may contribute to the timely detection of risks, allowing for further supervisory actions to be taken whenever necessary. |

|

(7) |

The introduction of risk management policies on asset encumbrance is vital to ensure that credit institutions follow their own encumbrance levels and are therefore better able to cope with possible stress situations. |

|

(8) |

The monitoring of asset encumbrance by the national supervisory authorities should cover encumbered assets and unencumbered but encumberable assets, as well as the sources of encumbrance, and the policies and contingency plans developed by credit institutions. |

|

(9) |

Market transparency contributes to addressing asymmetric information. Information which is clear, simple and easy to compare is required in order to allow market participants to better differentiate risk profiles in terms of encumbrance. |

|

(10) |

Market participants are subject — when applicable — to disclosure requirements based on International Financial Reporting Standard (IFRS) 7 (6). It would be appropriate at the same time to broaden the range of credit institutions disclosing information, to widen the disclosure to all means of encumbrance, to enhance the terms of disclosure and to create more uniform practices. |

|

(11) |

The proposed terms for disclosure aim at preventing credit institutions from being subject to stigma effects and for this reason, central bank operations should not be disclosed in any way. |

|

(12) |

The identification of best practices by the European and national supervisory authorities facilitates comparison of different issuances of covered bonds and contributes to better-informed risk analysis. The identification of best practices in respect of other financial instruments that generate encumbrance can contribute to similar improvements in these other markets. The acquisition of both types of instrument will be more appealing for investors as the costs involved in understanding the regulatory framework governing them would be lowered. Accordingly, it is desirable to incentivise the use of best practices at the highest quality standards. |

|

(13) |

The Commission proposal for the establishment of a single supervisory mechanism (7) (as agreed by the Council on 12 December 2012) envisages conferring specific supervisory tasks necessary for supervision of credit institutions on the European Central Bank (ECB). For the purposes of carrying out these tasks, the ECB will be considered the competent authority under the relevant acts of Union law and have the powers and obligations which competent authorities have under those acts. |

|

(14) |

The Annex to this recommendation analyses the significant systemic risks to financial stability within the Union arising from the funding of credit institutions. |

|

(15) |

In accordance with recital 29 of Regulation (EU) No 1092/2010, the observations of the relevant private sector stakeholders have been taken into account in preparing this recommendation. |

|

(16) |

This recommendation is without prejudice to the monetary policy mandates of the central banks within the Union. |

|

(17) |

Recommendations of the European Systemic Risk Board are published after informing the Council of the General Board’s intention to do so and providing the Council with an opportunity to react, |

HAS ADOPTED THIS RECOMMENDATION:

SECTION 1

RECOMMENDATIONS

Recommendation A — Monitoring and assessment of funding risks and funding risk management by supervisors

|

1. |

National supervisory authorities with responsibility for banking supervision are recommended to intensify their assessments of the funding and liquidity risks incurred by credit institutions, as well as their funding risk management, within the broader balance sheet structure, and should in particular:

|

|

2. |

National supervisory authorities with responsibility for banking supervision are recommended to monitor credit institutions’ plans to reduce reliance on public sector funding sources and to assess the viability of such plans for each national banking system, on an aggregated basis. |

|

3. |

National supervisory authorities and other authorities with a macro-prudential mandate are recommended to assess the impact of credit institutions’ funding plans on the flow of credit to the real economy. |

|

4. |

The EBA is recommended to develop guidelines on harmonised templates and definitions, in accordance with its established consultation practices, in order to facilitate the reporting of funding plans for the purposes of the recommendations contained in paragraphs 1 to 3 above. |

|

5. |

The EBA is recommended to coordinate the assessment of funding plans at Union level, including credit institutions’ plans to reduce reliance on public sector funding sources, and to assess the viability of such plans for the Union banking system, on an aggregated basis. |

Recommendation B — Risk management of asset encumbrance by institutions

National supervisory authorities with responsibility for banking supervision are recommended to require credit institutions to:

|

1. |

Put in place risk management policies to define their approach to asset encumbrance, as well as procedures and controls that ensure that the risks associated with collateral management and asset encumbrance are adequately identified, monitored and managed. These policies should take into account each institution’s business model, the Member States in which they operate, the specificities of the funding markets and the macroeconomic situation. The policies should be approved by each institution’s appropriate management bodies. |

|

2. |

Include in their contingency plans strategies to address the contingent encumbrance resulting from relevant stress events, which means plausible albeit unlikely shocks, including downgrades in the credit institution’s credit rating, devaluation of pledged assets and increases in margin requirements. |

|

3. |

Have in place a general monitoring framework that provides timely information to the management and the relevant management bodies on:

|

Recommendation C — Monitoring of asset encumbrance by supervisors

|

1. |

National supervisory authorities with responsibility for banking supervision are recommended to closely monitor the level, evolution and types of asset encumbrance as part of their supervisory process, and should in particular:

|

|

2. |

National supervisory authorities with responsibility for banking supervision are recommended to monitor and assess risks associated with collateral management and asset encumbrance, as part of the supervisory review process. This assessment should take into account other risks, such as credit and funding risks, and mitigating factors, such as capital and liquidity buffers. |

|

3. |

The EBA is recommended to issue guidelines on harmonised templates and definitions in order to facilitate the monitoring of asset encumbrance, in accordance with its established consultation practices. |

|

4. |

The EBA is recommended to closely monitor the level, evolution and types of asset encumbrance, as well as unencumbered but encumberable assets at Union level. |

Recommendation D — Market transparency on asset encumbrance

|

1. |

The EBA is recommended to develop guidelines on transparency requirements for credit institutions on asset encumbrance. These guidelines should help ensure that the information disclosed to the market is clear, easy to compare and appropriate. In view of the limited experience in disclosing reliable and meaningful information on asset quality, the EBA should follow a gradual approach, with a view to moving to a more extensive disclosure regime after one year. The guidelines should request credit institutions to provide:

|

|

2. |

For the purposes of paragraph 1(a), the EBA is recommended to specify in the guidelines the features of the disclosed data, in terms of units and lag of disclosure. |

|

3. |

In developing these guidelines, the EBA is recommended to:

|

Recommendation E — Covered bonds and other instruments that generate encumbrance

|

1. |

National supervisory authorities are recommended to identify best practices regarding covered bonds and encourage harmonisation of their national frameworks. |

|

2. |

The EBA is recommended to coordinate actions taken by national supervisory authorities, particularly in relation to the quality and segregation of cover pools, insolvency remoteness of covered bonds, the asset and liability risks affecting cover pools and disclosure of the composition of cover pools. |

|

3. |

The EBA is recommended to consider whether it is appropriate to issue guidelines or recommendations endorsing best practices, after monitoring the functioning of the market for covered bonds by reference to these best practices for a period of two years. If the EBA identifies the need for a legislative proposal in this regard, it should report to the European Commission and inform the ESRB. |

|

4. |

The EBA is recommended to assess whether there are other financial instruments that generate encumbrance which would also benefit from the identification of best practices in national frameworks. If the EBA concludes that such instruments exist, it should: (i) coordinate the identification and encourage the harmonisation of the resulting best practices by the national supervisory authorities; (ii) act as defined in paragraph 3 regarding covered bonds, in a subsequent stage. |

SECTION 2

IMPLEMENTATION

1. Interpretation

|

1. |

For the purposes of this recommendation, the following definitions apply:

|

|

2. |

The Annex forms an integral part of this recommendation. In the case of conflict between the main text and the Annex, the main text prevails. |

2. Criteria for implementation

|

1. |

The following criteria apply to the implementation of this recommendation:

|

|

2. |

Addressees are requested to report to the ESRB and to the Council on the actions undertaken in response to this recommendation, or adequately justify any inaction. The reports should at minimum contain:

|

3. Timeline for the follow-up

Addressees are requested to report to the ESRB and the Council on the actions taken in response to this recommendation, or adequately justify any inaction, in compliance with the timelines set out below.

|

1. |

Recommendation A — National supervisory authorities with responsibility for banking supervision, national supervisory authorities and other authorities with a macro-prudential mandate, and the EBA are requested to report according to the following timeline:

|

|

2. |

Recommendation B — by 30 June 2014, national supervisory authorities with responsibility for banking supervision are requested to report to the ESRB and the Council the actions taken in response to this recommendation. |

|

3. |

Recommendation C — the EBA and national supervisory authorities with responsibility for banking supervision are requested to report according to the following timeline:

|

|

4. |

Recommendation D — the EBA is requested to report according to the following timeline:

|

|

5. |

Recommendation E — the EBA and national supervisory authorities are requested to report according to the following timeline:

|

4. Monitoring and assessment

|

1. |

The ESRB Secretariat:

|

|

2. |

The General Board assesses the actions and the justifications reported by the addressees and, where appropriate, decides whether this recommendation has not been followed and if the addressees have failed to adequately justify their inaction. |

Done at Frankfurt am Main, 20 December 2012.

The Chair of the ESRB

Mario DRAGHI

(1) OJ L 331, 15.12.2010, p. 1.

(3) EBA Recommendation on the creation and supervisory oversight of temporary capital buffers to restore market confidence (EBA/REC/2011/1).

(4) Proposal for a directive of the European Parliament and of the Council on the access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms and amending Directive 2002/87/EC of the European Parliament and of the Council on the supplementary supervision of credit institutions, insurance undertakings and investment firms in a financial conglomerate (COM(2011) 453 final), and proposal for a regulation of the European Parliament and of the Council on prudential requirements for credit institutions and investment firms (COM(2011) 452 final).

(5) Proposal for a directive of the European Parliament and of the Council establishing a framework for the recovery and resolution of credit institutions and investment firms and amending Council Directives 77/91/EEC and 82/891/EEC, Directives 2001/24/EC, 2002/47/EC, 2004/25/EC, 2005/56/EC, 2007/36/EC and 2011/35/EU and Regulation (EU) No 1093/2010 (COM(2012) 280/3).

(6) In Europe these standards are adopted by means of Commission Regulation (EC) No 1126/2008 of 3 November 2008 adopting certain international accounting standards in accordance with Regulation (EC) No 1606/2002 of the European Parliament and of the Council (OJ L 320, 29.11.2008, p. 1).

(7) Proposal for a Council regulation conferring specific tasks on the European Central Bank concerning policies relating to the prudential supervision of credit institutions (COM(2012) 511 final).

(8) OJ L 177, 30.6.2006, p. 1.

(9) OJ L 135, 31.5.1994, p. 5.

ANNEX TO THE RECOMMENDATION ON FUNDING OF CREDIT INSTITUTIONS

CONTENTS

EXECUTIVE SUMMARY

INTRODUCTION

|

I. |

EVOLUTION OF FUNDING STRUCTURES AND ASSETS |

|

I.1. |

Secured versus unsecured funding |

|

I.2. |

Evolution of secured funding |

|

I.2.1. |

Covered bonds |

|

I.3. |

Evolution of unsecured funding |

|

I.3.1. |

Customer deposits |

|

I.4. |

Innovative funding |

|

I.4.1. |

Liquidity swaps |

|

I.4.2. |

Structured products and ETFs |

|

I.5. |

Public support in the current distressed conditions |

|

I.6. |

Drivers for the development of funding structures |

|

I.6.1. |

Impact of new and upcoming regulations on bank funding |

|

I.7. |

Leverage and asset decomposition |

|

II. |

ASSET ENCUMBRANCE: INPUT FROM THE SURVEY |

|

II.1. |

Overall levels of asset encumbrance |

|

II.2. |

Impact of over-collateralisation on levels of encumbrance |

|

II.3. |

Contribution of the different transactions to encumbrance |

|

III. |

RISKS |

|

III.1. |

Risks from asset encumbrance |

|

III.1.1. |

Structural subordination of unsecured creditors |

|

III.1.2. |

Issues related to future access to unsecured markets |

|

III.1.3. |

Issues related to transparency and correct pricing |

|

III.1.4. |

Increased funding and liquidity risks |

|

III.1.5. |

Contingent encumbrance |

|

III.1.6. |

Other risks from asset encumbrance |

|

III.1.7. |

Other risks related to specific products or transactions |

|

III.1.8. |

Triggers for the materialisation of risks |

|

III.1.9. |

Sustainability of asset encumbrance |

|

III.1.10. |

Impact of asset encumbrance on the real economy |

|

III.2. |

Risks from innovative funding |

|

III.2.1. |

Transparency, confidence, difficulty of management and supervision |

|

III.2.2. |

Interconnectedness |

|

III.2.3. |

Litigation and reputation risks, consumer protection |

|

III.2.4. |

Specific risks relating to liquidity swaps |

|

III.3. |

Risks from concentration |

|

III.4. |

Risks from deleveraging pressure |

|

IV. |

SUSTAINABILITY OF FUNDING STRUCTURES (MEDIUM TO LONG-TERM PERSPECTIVE) |

|

IV.1. |

Stronger role for customer deposits |

|

IV.2. |

Role of wholesale unsecured and secured funding |

|

IV.3. |

Features of a sustainable funding structure |

|

IV.4. |

Demand and supply effects of funding |

|

V. |

POLICY |

POLICY OBJECTIVES

PRINCIPLES FOR THE IMPLEMENTATION OF THE RECOMMENDATIONS

FOLLOW-UP COMMON TO ALL POLICY RECOMMENDATIONS

RECOMMENDATIONS

|

V.1. |

Recommendation A — Monitoring and assessment of funding risks and funding risk management by supervisors |

|

V.1.1. |

Economic reasoning |

|

V.1.2. |

Assessment, including advantages and disadvantages |

|

V.1.3. |

Follow-up |

|

V.1.4. |

Communication on the follow-up |

|

V.2. |

Recommendation B — Risk management of asset encumbrance by institutions |

|

V.3. |

Recommendation C — Monitoring of asset encumbrance by supervisors |

|

V.3.1. |

Economic reasoning (Recommendations B and C) |

|

V.3.2. |

Assessment, including advantages and disadvantages (Recommendations B and C) |

|

V.3.3. |

Follow-up (Recommendations B and C) |

|

V.3.4. |

Communication on the follow-up — Recommendation B |

|

V.3.5. |

Communication on the follow-up — Recommendation C |

|

V.4. |

Recommendation D — Market transparency on asset encumbrance |

|

V.4.1. |

Economic reasoning |

|

V.4.2. |

Assessment, including advantages and disadvantages |

|

V.4.3. |

Follow-up |

|

V.4.4. |

Communication on the follow-up |

|

V.5. |

Recommendation E — Covered bonds and other instruments that generate encumbrance |

|

V.5.1. |

Economic reasoning |

|

V.5.2. |

Assessment, including advantages and disadvantages |

|

V.5.3. |

Follow-up |

|

V.5.4. |

Communication on the follow-up |

|

V.6. |

The ESRB takes note of other initiatives |

|

VI. |

RESULTS OF THE SURVEY ON ASSET ENCUMBRANCE AND INNOVATIVE FUNDING: METHODOLOGICAL AND STATISTICAL NOTE |

|

VI.1. |

Methodological note |

|

VI.1.1. |

General description of the data set |

|

VI.1.2. |

Some methodological aspects |

|

VI.1.3. |

Data quality control |

|

VI.2. |

Encumbrance |

|

VI.2.1. |

Encumbrance levels |

|

VI.2.2. |

Maturity of encumbered assets and matching liabilities |

|

VI.3. |

Secured funding |

|

VI.4. |

Counterparties |

EXECUTIVE SUMMARY

Banks’ funding structures have undergone significant change in recent years. This Annex presents the developments in Union banks’ funding sources and structures, the risks stemming from such developments and a set of policy proposals to address such risks.

The most notable development has been the increase in the relative importance of secured funding as a consequence of investors’ risk aversion and of regulatory developments, notably the Basel frameworks for capital and liquidity and Solvency II. These developments have set the scene for rising demand for collateral (including from public sector funding sources) with a tightening supply of quality collateral, at a time when banks need stable funding sources to maintain their lending into the real economy. The heightened investor uncertainty associated with the current sovereign debt crisis has led banks to rely increasingly on public sector funding sources, while central banks have responded with extraordinary measures that have included longer-term operations and extended lists of collateral.

Banks have also increased reliance on, and competition for, customer deposits. Increased reliance on deposits has been partially successful; it has also been accompanied by risks, as deposits may become more volatile with competition and customer offerings have become more innovative and not always well understood. Finally, a few banks have moved to innovative products, notably liquidity swaps, in order to obtain funding at competitive prices. In an attempt to review these phenomena comprehensively, the Annex contains an assessment of the sustainability of funding structures as well as of their impact on the financial sector and on the real economy.

The Annex highlights and reviews three sources of risks in greater depth: (1) asset encumbrance; (2) innovative funding; and (3) concentration.

Secured funding has proved to be a lifeline for banks during the current period of stress, as it allows for diversification of funding sources and decreases counterparty risk. While recognising the benefits derived from secured funding during the crisis, the Annex also assesses the risks of an excessive encumbrance level. First, it implies further subordination of other creditors, in particular depositors, which has consequences in terms of potential usage of funds from deposit guarantee schemes. High levels of encumbrance may also negatively affect future access to the unsecured markets and create challenges in pricing risks correctly, with implications for efficient resource allocation. In addition, contingent encumbrance tends to be pro-cyclical since it increases in stress periods as a result of automatic increases in collateralisation requirements. More broadly, system-wide increases in encumbrance create difficulties in liquidity and funding management and reinforce the risks related to collateral reuse. Further difficulties are associated with the effective management and oversight of institutions with high encumbrance.

Innovative funding tends to be less transparent and, as a result, more difficult to manage and supervise. Given the potential opaqueness, there are also increased chances of the materialisation of litigation and reputation risks, primarily if these products are sold to retail consumers. Risks from concentration are analysed from four different perspectives: the investor base, instruments, maturity profiles and geographical scope.

Viewing funding structures from a holistic perspective, it is argued in the Annex that a well-diversified funding structure is crucial to guaranteeing credit institutions’ capacity to withstand stress events. This implies avoiding over-reliance on individual funding sources and, in particular, on secured funding. Furthermore, it requires that institutions also take account of the actions of other institutions in determining their capacity to implement their funding plans, in particular with regard to reliance on customer deposits, which, owing to increased competition, may become a less stable funding source. There is already evidence of credit institutions resorting to retail funding instruments, which may look similar to deposits but which entail different risks as they may not be covered by deposit guarantee schemes.

On the basis of the analysis undertaken, several policy recommendations are made.

In the short run, given the still impaired market conditions and credit institutions’ need to develop robust funding plans, national supervisory authorities and the European Banking Authority (EBA) are recommended to monitor and assess funding and liquidity risks and the viability of funding plans, on aggregate, at national and Union levels respectively. At this juncture, authorities are, in particular, recommended to assess institutions’ plans to reduce reliance on public sector funding sources. When analysing funding and liquidity risks, authorities are advised to pay special attention to the use of innovative instruments that may pose systemic risks and to consider the risks of uninsured deposit-like instruments when sold to retail customers and their possible negative effects on traditional deposits.

A key thrust of the proposals is to address issues of encumbrance with a comprehensive strategy. In the short run, it is suggested that a concerted effort be made to further improve credit institutions’ management of liquidity and funding risks where encumbrance is involved. Supervisors are also recommended to be more consistent in their monitoring and assessing of the levels, evolution and types of encumbrance, as well as of the effect on encumbrance of stress events. Importantly, a recommendation on market transparency is included to address the supply of funding by facilitating the better pricing of risks, in particular those related to encumbrance.

Considering the relative importance that covered bonds have assumed in banks’ funding structures and the risks identified for these instruments, for instance in terms of legal uncertainties in some Member States and differences in disclosure habits, national supervisory authorities are recommended to incentivise the implementation of best practices, either public or private. Following this first stage, the European Banking Authority is recommended to coordinate such initiatives and to identify best practices as well as to consider the functioning of the marketplace in accordance with the principles identified. It should also consider whether it is appropriate to use its own powers as formal mechanisms for imposing such best practices or to refer the matter to the European Commission for potential further action, taking into account the potential impact on otherwise well-functioning markets. In a second phase, it is recommended that the EBA consider whether there are other financial instruments that also encumber assets that would call for a similar approach.

Without proposing formal recommendations to stimulate other funding markets, the ESRB takes note of some private initiatives, for instance with regard to the labelling of securitisation and covered bonds, as these may help to restore confidence in certain financial products.

INTRODUCTION

The recent crisis has its roots in the events of 2007-08 when developments in wholesale and retail markets exposed the vulnerabilities inherent in some asset classes (e.g. subprime residential mortgages in the United States and elsewhere) and in some business models (e.g. reliance on short-term wholesale funding). The crisis has subsequently morphed and extended over a lengthy period. In the Union and, in particular, in the euro area, the current vulnerabilities of some sovereigns, together with fragilities in some banking systems, have negatively reinforced themselves in a context of poor economic growth. In this setting, the strong link between bank and sovereign funding costs, combined with uncertainties over the asset quality of some banks and the sustainability of their business models, mean that credit and interbank markets have remained impaired and that banks have faced difficulties in managing their balance sheets.

Against this background, public authorities have intervened, with central banks implementing decisive measures to allow banks to fund themselves and with supervisors taking steps to shore up capital levels, improve transparency and tackle asset quality.

To cope with this situation, banks have also responded by making changes in their funding structures and in their asset portfolios. This Annex also devotes attention to changes in banks’ funding sources and structures and assesses whether such developments pose systemic risks.

This Annex reviews the funding structures of EU banks and how they have evolved in recent years and focuses on the increasing role played by secured funding and by other collateralised transactions and their consequences in terms of asset encumbrance. Potentially in response to the crisis, a few banks have also turned to more innovative funding sources, which are frequently opaque and in some cases can have an impact on asset encumbrance. Finally, the Annex examines more broadly the consequences of these developments in relationship to the sustainability of banks’ funding structures.

The Annex contains an assessment of whether and how these developments warrant policy attention. It concludes that some of these risks are significant and therefore presents policy options. These options take due account of the nature of the current situation, which is still one of crisis and market instability and therefore requires special care.

This analytical exercise makes use of several different data sets in order to better depict the evolution and current state of affairs. Although banks’ balance sheets are monitored by supervisors and other public authorities and are subject to market transparency rules, it was necessary to conduct an ad hoc survey to obtain information, particularly on the levels and types of encumbrance and on innovative funding sources.

This Annex is organised into six sections. Following the introduction, Section I presents the evolution and current state of EU banks’ funding structures. Section II is devoted to the analysis of the data on asset encumbrance collected by the ESRB. The analysis of the risks entailed in such evolution is discussed in Section III. Section IV addresses more broadly the issue of the sustainability of funding structures and Section V concludes with the ESRB’s policy recommendations. A methodological and statistical annex on the ESRB survey on asset encumbrance and innovative funding is included (Section VI).

I. EVOLUTION OF FUNDING STRUCTURES AND ASSETS

The evolution of funding sources and structures in recent years cannot be analysed separately from the context of the current, long-lasting crisis. In response to severely impaired credit and interbank markets and in a context of vulnerabilities in both sovereigns and financial systems, particularly in the euro area, banks have adapted both their funding structures and their asset portfolios.

If the funding structure of the balance sheets of euro area banks (1) as of the end of 2011 is compared with that prevailing before the financial crisis (as of the end of 2005), it can be concluded that deposits, excluding intra-monetary financial institutions (MFIs), still represent the largest percentage of banks’ liabilities (see Chart 1). Moreover, since 2008, the percentage of customers’ deposits in banks’ liabilities has been increasing, as have the maturities of those deposits (2) (see Section I.3.1).

Chart 1

Liabilities breakdown: 2005 vs 2011

Since 2005 liabilities have been restructured increasing the share of intra-MFI deposits. In fact, on the basis of financial transactions data, deposits have increased by 12 % since the end of 2005.

However, it should be pointed out that this statistical component encompasses central bank funding. Following the policy response by central banks and other public authorities to the impairment of credit and interbank markets, recourse to central bank funding and to the Eurosystem in particular, as well as reliance on state-guaranteed debt, have increased significantly in recent years (see Section I.5).

The third most relevant item is long-term debt securities, which accounted for 14 % of total bank liabilities. In terms of debt securities, in the past few years there has been a shift in banks’ funding structures towards secured funding, including covered bonds (see Sections I.1 and I.2). Deteriorating market confidence has also led to a significant reduction in cross-border interbank transactions, which has been reflected in shorter maturities and higher borrowing rates. This resegmentation within national boundaries is still ongoing.

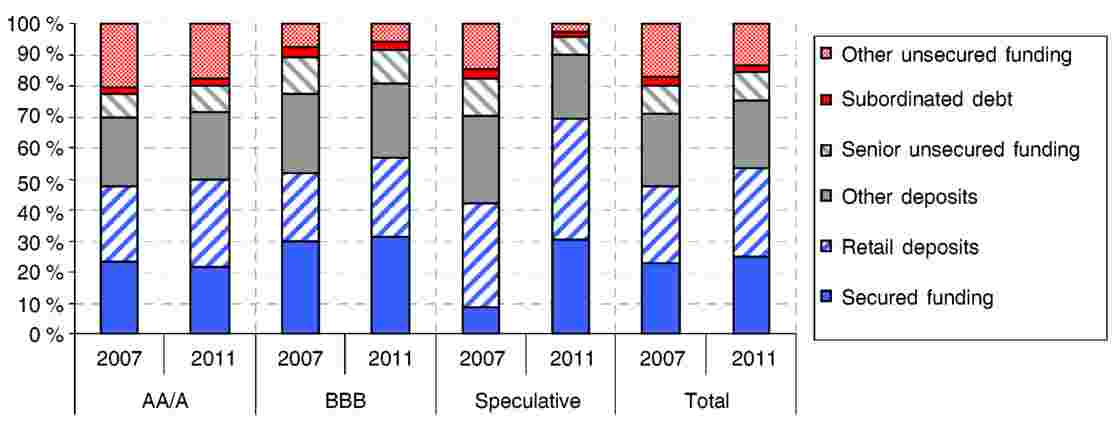

It is possible to conclude that, for a small sample of surveyed banks (3), the recomposition of liability structures is dependent on the banks’ rating (and inherently on the sovereigns’ rating), with more vulnerable banks or banks in more vulnerable sovereigns experiencing a higher increase in secured funding (which includes central bank funding) and a decrease in the reliance on unsecured debt instruments. These banks also seem to have strengthened their deposit base more than the higher rated banks (see Chart 2).

Chart 2

Structure of funding for groups of banks with different ratings, end-2007 and end-2011

These changes in banks’ liabilities are also a reflection of a change in business models. Before the crisis, EU banks mostly pursued asset-driven strategies, leading to excessive leverage, as funding was readily available at low prices, especially in wholesale markets. The crisis and its implications for the availability of liquidity and funding forced a strategic turnaround for banks, which have shifted to liability-driven strategies.

I.1. Secured versus unsecured funding

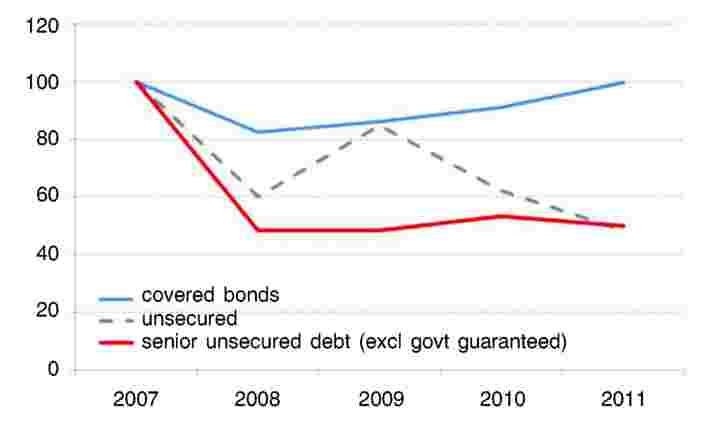

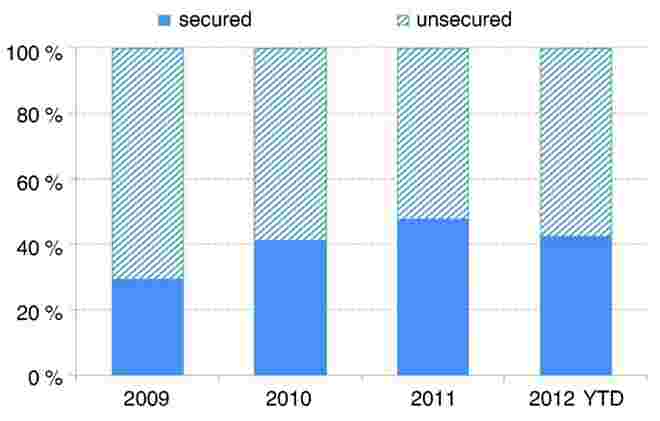

Issuance of medium and long-term debt by banks has been significantly down from late 2007 onwards compared to the pre-crisis decade. While the financial crisis adversely affected both unsecured and secured funding markets, the issuance by Union banks of covered bonds has proved much more resilient over the past few years than that of senior unsecured debt (see Chart 3), resulting in a shift towards more secured issuance (see Chart 4). This increasing trend reversed in 2012, partly due to the fact that market access for peripheral issuers, which accounted for a significant part of the increase in covered bond issuance in 2010 and 2011, was restricted for most of the year.

Chart 3

Change in the issuance of covered bonds and senior unsecured debt (2007-11; index 2007 = 100)

Chart 4

Share of secured and unsecured debt issuance (2009 — Sep. 2012; percentages)

This broad trend conceals differences in developments across countries and across banks. In the past few years, the issuance of banks in more vulnerable countries has suffered more than in other countries. Banks in those countries also resorted more significantly to secured instruments (frequently retaining the instruments to use as collateral) and to guaranteed instruments (in particular those guaranteed by the state). Lower rated banking groups, even when located in stronger sovereigns, faced more difficulties in obtaining wholesale funding in private sector markets.

Turning to interbank funding, euro money market survey data (4) show that, after years of continuous growth, total activity in the unsecured markets started to fall in 2008 and dropped significantly further in 2009-10 as a result of heightened counterparty risk concerns. While unsecured borrowing increased somewhat in 2011, it still remained well below pre-crisis levels. The decline in the relative share of unsecured lending also continued in 2012, when the turnover in the unsecured markets contracted by 36 %. The decline in unsecured interbank borrowing was offset to some extent by an increase in repo funding, which, after a drop in 2008, started to grow in 2009; however, it declined again by 15 % in 2012. The relative resilience of secured market activity can be attributed, in part, to the increased use of electronic platforms and, in particular, of trading facilities with central counterparties (CCPs) for secured transactions. According to survey data, activity in the secured market cleared through CCPs has increased markedly since 2008; in 2012 it already accounted for 55 % of secured market transactions (compared with 51 % in 2011).

I.2. Evolution of secured funding

The amount of EU banks’ secured debt outstanding (excluding Germany) was relatively stable between the end of 2009 and the first quarter of 2012, although this masked the difference in developments across the Union, with increases in several countries (e.g. Spain, Italy and Sweden) contrasting with declines in others (e.g. Ireland, the Netherlands and the United Kingdom) (5).

At the same time, some banks started increasing the issuance of retained securitisation or covered bonds in order to use those instruments as collateral, in particular for refinancing operations with central banks (see Section I.5 for further details). In particular, between 2011 and 2012, lower-rated institutions resorted more to this type of operation.

Securitisation was heavily employed at the beginning of the process: in 2008 a record EUR 711 billion in issuance volume was observed but only 5 % of total issuance was not retained by banks. The share and volume of retained asset backed securities (ABS) far exceeded that of retained covered bonds in 2008-11.

In the first nine months of 2012, retained covered bond issuance picked up and accounted for more than one-third of total covered bond issuance (see Chart 5). However, the share of retained securitisation issuances remained significantly higher, at least in the first quarter of 2012.

Chart 5

Retained securitisation and covered bond issuances by year in the EU

I.2.1. Covered bonds

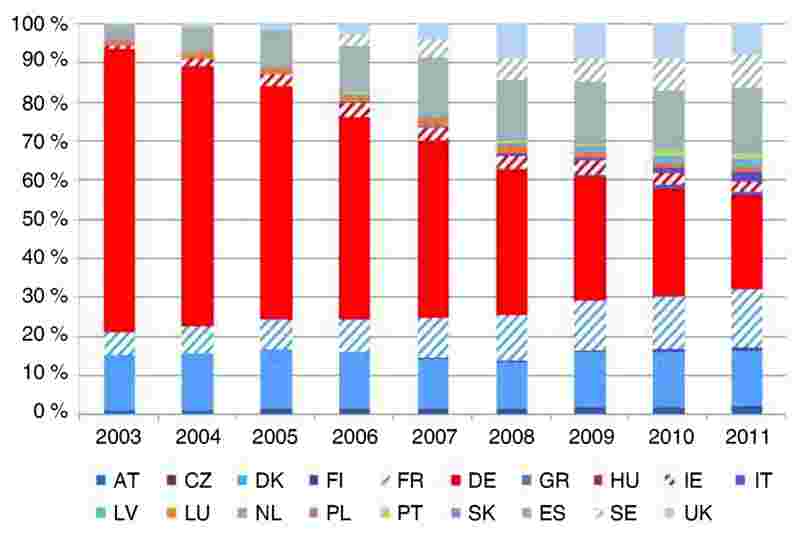

Covered bonds assume an important role in terms of secured funding. They have shifted from being a funding source in only a few countries to becoming an important source of long-term funding for banks in a much broader group of countries (see Chart 6). In 2003, 95 % of all covered bonds outstanding were issued by banks and mortgage banks located in only four countries (Denmark, France, Germany and Spain), whereas in 2010 only 66 % of all covered bonds outstanding were issued by those four countries (see Chart 7).

Chart 6

Covered bonds outstanding

Chart 7

Share of covered bonds outstanding, by country, in total of the EU

In both primary and secondary markets, covered bond spreads have remained tighter than the equivalent senior unsecured debt, thus making covered bonds more attractive as funding instruments, in particular for residential mortgages. The fact that rating agencies rate covered bonds significantly higher than the senior unsecured liabilities of the same issuer has also contributed to higher investor appetite for these instruments.

I.3. Evolution of unsecured funding

While the amount of unsecured debt outstanding was relatively stable in 2009 and 2010, it started to decline in the first quarter of 2011. The same is true for the share of unsecured debt outstanding of total debt outstanding, which was around 40 % in 2009 and 2010 and started to fall in the first quarter of 2011, reaching 30 % most recently. This development was heterogeneous across Union countries but the most significant decline in this share was seen mainly in countries on which the crisis had a pronounced impact (notably Italy and Portugal). Banking groups with lower ratings domiciled in higher-rated countries also registered a decrease in the share of unsecured debt.

I.3.1. Customer deposits

In spite of a generalised increase in customers’ deposits in banks’ liabilities (see Chart 1), banks’ attempts to maintain a larger deposit base have so far produced mixed results (see Chart 8), largely because of tighter competition in an already overbanked market and some savers’ relative reluctance to tie up funds in low-interest deposits.

Chart 8

Share of domestic non-financial private sector deposits as a percentage of total assets

In fact, the loan-to-deposit ratio remained relatively flat between 2009 and 2012 (see Chart 9): after a contraction in the first quarter of 2011, it increased again and remained relatively stable over the last quarters, at about 150 %. Overall, unlike the situation for market funds, deposit stocks have shown stability throughout the crisis, with the exception of a few countries at times of stress. To an extent, this is because of the existence of Union-wide harmonised deposit guarantee schemes. There have, however, been some movements of wholesale deposits in some countries, starting in the second half of 2011, some of which were of a cross-border nature (see Chart 10).

Chart 9

Loan-to-deposit ratio for a sample of large EU banking groups

Chart 10

Cross-border deposits by EU non-MFIs

I.4. Innovative funding

Besides the traditional types of bank funding, banks use, to differing degrees, other types of instruments in order to improve their funding or liquidity situation.

I.4.1. Liquidity swaps

Liquidity swaps can take several forms but are in general a type of secured lending whereby a lender provides a borrower with highly liquid assets (e.g. cash and government bonds) in exchange for a pledge of less liquid collateral (e.g. asset-backed securities), performing a liquidity upgrade in the process.

Information provided in the ESRB survey on asset encumbrance and innovative funding indicates that the funding obtained by liquidity swaps with cash collateral (repos) and by pledging collateral received in reverse repos (‘matched repos’) accounts for 7 % of total assets. If 2007 and 2011 data are compared, it can be seen that no significant change was reported regarding this share, other than that banks tended to prefer matched repos over repos in 2007 (6).

According to the same survey, securities lending transactions remain marginal for the majority of institutions. Indeed, the funding received in those transactions represents on average only 0,7 % of banks’ total assets and does not exceed 3,5 % for any of the reporting banks. However, securities lending transactions are highly concentrated, mainly at larger banks. In total, such transactions were reported by only 19 banks (out of 47), with four banks accounting for a 67 % share of funding received. In addition, the market is highly dominated by a few countries, namely United Kingdom (44 % of total funding received), Germany (22 %) and France (19 %), followed by the Netherlands, Italy and Sweden.

I.4.2. Structured products and ETFs

The crisis had an impact on the market for structured products (7). The annual turnover of structured securities listed on Euronext (Amsterdam, Brussels, Lisbon and Paris) increased significantly in the mid-2000s but dropped significantly following the onset of the crisis (see Table 1).

Table 1

Turnover in structured products; billion EUR

|

2005 |

2006 |

2007 |

2008 |

2009 |

2010 |

|

11,5 |

23,6 |

34,0 |

28,9 |

23,0 |

26,1 |

|

Source: NYSE Euronext. |

|||||

The use of structured products for bank funding (8) varies widely among European countries, according to the size of the market (Belgium, Germany, France and Italy account for two-thirds of structured products outstanding, with EUR 226 billion, EUR 157 billion, EUR 84 billion and EUR 82 billion respectively at the end of 2011) and the patterns in domestic bank funding structures. However, it should be noted that structured products are not innovations introduced after the crisis.

The use of exchange traded funds (ETFs) as an innovative funding instrument has been widely publicised. However, the use by banks of traded funds to obtain funding goes beyond the scope of ETFs, as other UCITS could be used as well by resorting to total return swaps and securities lending. From the information gathered through the ESRB survey, ETFs are very seldom used to obtain funding; only a couple of banks reported using this instrument for funding purposes. However, this does not mean that this activity will not pick up again in the future. This is one of the reasons why supervisors are continuing to monitor this activity. Moreover, the European Securities and Markets Authority (ESMA) published guidelines on ETFs and other UCITS issues in July 2012.

I.5. Public support in the current distressed conditions

Following the onset of the financial crisis and particularly after the Lehman collapse, central banks and public authorities intervened decisively. Given the difficulty for banks to fund themselves in unsecured credit markets, banks within the Union increased their recourse to secured funding (see Section I.2) and to central bank funding.

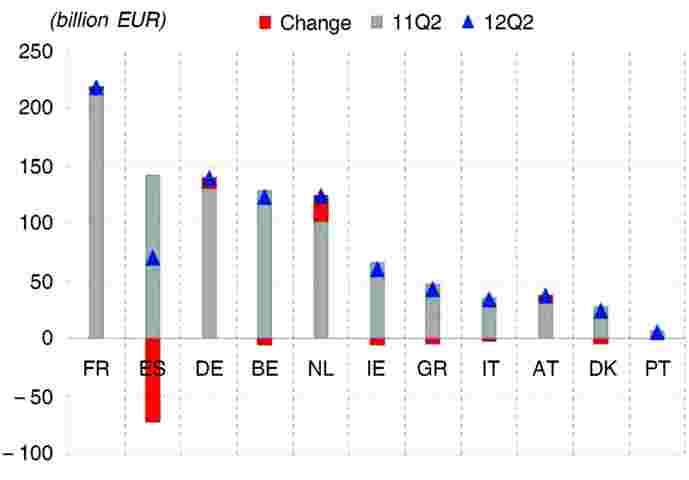

Moreover, EU Member States took several measures to support their banking systems. The bulk of public support measures can be classified into three broad categories, capital injections, guarantees on bank liabilities and asset relief measures (9). Notably, Member States agreed to a system of national state guarantees for liquidity, which was revised in 2011, in an attempt to allow viable banks to obtain funding. In January 2012, 17 EU Member States had granted guarantees on new bond issuances for a total of EUR 580 billion (EUR 480 billion in the euro area), which was down from a peak of EUR 930 billion (EUR 720 billion in the euro area) in the last quarter of 2009. The situation at country level is mixed (see Chart 11). The amount of contingent liabilities stemming from guarantees on bank liabilities declined in most countries as a result of bonds maturing, but it increased in countries such as Belgium, Greece, Italy, Portugal and Spain.

Chart 11

Guarantees on bank liabilities: country breakdown, in billion EUR

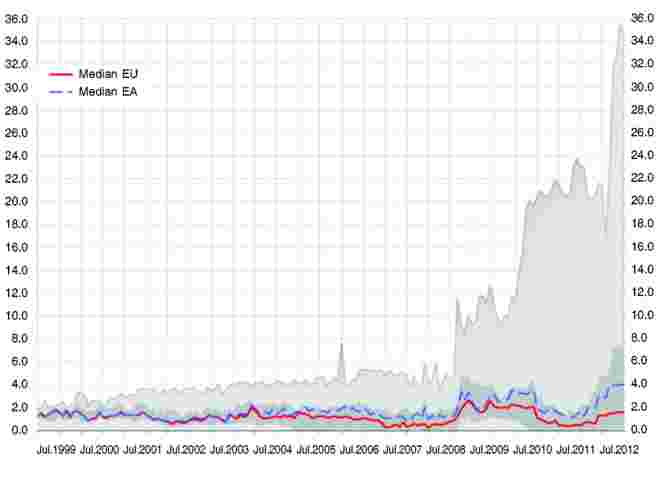

With the crisis evolving into a sovereign crisis in some euro area countries, conditions for funding worsened significantly for banks in such countries. In this context, the Eurosystem intervened with a broad range of measures, which included, inter alia, establishing longer-term refinancing operations (LTROs) at full allotment and fixed rates, broadening eligible collateral and decreasing the minimum reserves requirement. On 22 December 2011 and 1 March 2012, the ECB conducted two LTROs with a maturity of three years, which together amounted to more than EUR 1 trillion (see Chart 12 and Chart 13).

Chart 12

Operations with the EU NCBs

Chart 13

Operations with the EU NCBs

Naturally, recourse to central bank funding is correlated with sovereign fragilities, with banks from Cyprus, Greece, Ireland, Italy, Portugal, Slovenia and Spain being more reliant on financing from the Eurosystem (see Chart 13). In some countries, banks have resorted to retained securities, in particular covered bonds, in order to gather eligible collateral for operations with central banks (see Chart 5).Some banks have resorted to state guarantees for issuing debt, which was in some cases used in refinancing operations with the central bank.

I.6. Drivers for the development of funding structures

The change in the composition of banks’ liabilities is the result of several concurrent factors. Following the multi-notch downgrades of debt issued by several peripheral euro area sovereigns, which were previously highly rated and perceived to be low risk, there was an increase in demand by fixed income investors for safer assets. This led to a bias towards secured assets and, in particular, covered bonds as the cover pools consisting of relatively safer assets as a second source of repayment provided some further reassurance. Moreover, specific legal frameworks for covered bonds offer additional investor reassurance.

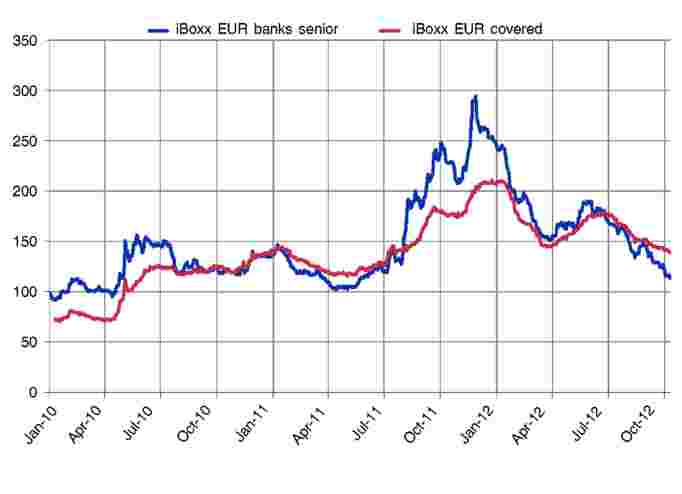

As regards developments in the cost of secured and unsecured debt, based on the respective iBoxx indices, the differential between senior unsecured debt and covered bond spreads showed changing pricing patterns during the crisis. Until around mid-2010, the average cost of senior unsecured debt remained well above that of covered bonds but subsequently the difference largely disappeared and the relationship even reversed in the first half of 2011. Increased risk aversion in credit markets due to the intensification of the sovereign debt crisis, coupled with fears about the possible impact of bail-in proposals on the cost of senior unsecured debt, led to the reappearance and the rewidening of the positive spread differential between senior unsecured debt and covered bonds in the second half of 2011.

Chart 14

Swap spreads on iBoxx indices for euro-denominated senior unsecured debt and covered bonds (Jan. 2010-Oct. 2012; basis points)

Following the Eurosystem’s three-year LTROs, senior unsecured spreads tightened significantly in early 2012 and average spreads on secured and unsecured debt moved relatively closely together for much of the first half of the year. In late June 2012, however, the average spread on senior unsecured debt fell below that of covered bonds.

As regards the cost of interbank funding, following the Lehman default, unsecured transactions became much more costly relative to repo funding, as illustrated by the sharp widening of the EURIBOR-EUREPO term spreads, which reflected a significant rise in counterparty credit risk. While spreads significantly narrowed following the implementation of the ECB’s large-scale liquidity support measures, they remained well above pre-crisis levels. The intensification of the sovereign debt crisis from mid-2011 onwards again led to rewidening of the spreads on secured versus unsecured transactions. In the first half of 2012, the rate differential between repo and unsecured transactions narrowed again after the implementation of the Eurosystem’s three-year LTROs.

It should also be noted that since the beginning of the crisis, EU banks have been focusing on strengthening their funding base by making deposit-gathering a key strategy. Retail deposits are considered by the Basel proposal for the liquidity regime as ‘stickier’ than other instruments, which may also have contributed to banks engaging in such strategies.

I.6.1. Impact of new and upcoming regulations on bank funding

I.6.1.1.

Several legislative initiatives that have been or will be implemented in the near future may have an impact on banks’ funding options, especially on the trade-off between secured versus unsecured funding sources but also on recourse to new sources of funding. Of these initiatives, the most important are the Capital Requirements Directive and Regulation (CRR/CRD IV), the Solvency II/Omnibus II Directive, the proposals for the Bank Recovery and Resolution Directive and the European Market Infrastructure Regulation (EMIR).

In summary, as covered bond issuance will have a potentially favourable treatment under future Basel III and Solvency II rules compared with securitisations, banks might have further incentives to opt for such instruments. At the same time, the ‘bail-in’ debt provisions included in the proposal on bank resolution have contributed to investor perceptions that recovery rates for unsecured creditors are likely to be lower in the future. The fact that, in the current proposal regarding the Liquidity Coverage Ratio, unsecured debt instruments issued by banks are not considered liquid assets may also negatively affect banks’ interest in holding other banks’ unsecured debt (10).

The impacts of the referred regulations are not restricted to bank funding and the potential negative effects should be considered in the wider context of the benefits not only in terms of funding and liquidity but also in terms of increased resilience of the system, decreased moral hazard, limiting contagion etc.

I.6.1.2.

CRR/CRD IV. Two of the elements of the CRD IV that could have significant effect on bank funding patterns are those related to the liquidity framework: the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Requirement (NSFR). The main purpose of the NSFR is to require banks to establish more stable, long-term sources of funding. The main purpose of the LCR is, in turn, to create a pool of easily disposable assets consisting mostly of high quality, liquid assets, including covered bonds but excluding ABSs.

An additional impact on bank funding stemming from the Capital Requirements legislation comes from the treatment of covered bonds. The CRR/CRD IV does not introduce new treatment for covered bonds in terms of capital charges as compared with the past, since it maintains the main asset classes that can be eligible for collateral to back covered bonds, as established by the previous capital requirements directives.

Solvency II Directive. The Directive aims at harmonising the regulation of insurance and reinsurance firms. Solvency rules stipulate the minimum amounts of financial resources that insurers and reinsurers must have in order to cover the risks to which they are exposed. One of the main criticisms of Solvency II is that it will incentivise investment in short-term rather than long-term debt because of the design of the capital requirements for spread risk. However, this criticism is based on a simplistic view of Solvency II, comparing parameters of the spread risk module with CRD IV parameters. This approach also fails to take account of diversification effects and the effect of interest risk submodules in the final capital requirements.

Other elements currently under discussion in the Omnibus II negotiations may preserve or enhance incentives for long-term investments. One example is the ‘long-term guarantees package’, which is designed to deal with issues arising from the impact of artificial volatility on insurance products with long-term guarantees.

Another key criticism is that the Solvency II approach penalises investment in bank participations. Again, this is based on the European Insurance and Occupational Pensions Authority (EIOPA) fifth quantitative impact study (QIS5) approach, in which participations in financial and credit institutions were deducted from own funds. Current draft delegated acts will reflect an approach similar to that of the CRD IV, in accordance with which the value of the participation in banks is deducted from the corresponding tier only where certain thresholds are exceeded. It is unlikely that this approach could have a significant effect on the reallocation of assets for insurers.

It could still be possible that Solvency II will change the asset allocation for some undertakings, given that it captures diversification effects.

Bank Recovery and Resolution Directive. The draft Directive sets out the necessary steps and powers to ensure that bank failures across the EU are managed in a way that avoids financial instability and minimises costs for taxpayers. The proposed framework contains a ‘debt write-down’ or ‘bail-in’ resolution tool. Under this tool, resolution authorities would be able to write down equity, subordinated debt and any other unsecured senior liabilities or convert them into equity. According to the Commission’s proposal, secured funding, deposits covered by deposit guarantee schemes (DGS), funds with a maturity of less than one month, trade/commercial credit, liabilities to employees or tax/social security authorities and derivatives are excluded from the bail-in regime.

While bail-in would not change the position of unsecured creditors in the creditor hierarchy, it would contribute to investor’s perceptions that recovery rates for unsecured funding are likely to be lower in the future. All in all, given a higher risk premium, ‘bail-in-able’ liabilities (e.g. unsecured funding) might be more expensive in the future. Nevertheless, impact assessments carried out by the European Commission have shown that the expected impact is contained. The Commission’s Impact Assessment (11) accompanying the draft Directive anticipates that the cost of bank funding will increase overall by between 5 and 15 basis points, whereas the change in the funding costs of ‘bail-in-able’ liabilities ranges between 15 and 40 basis points. The banking industry’s estimates of the change in the funding costs of ‘bail-in-able’ liabilities, however, range between 55 and 100 basis points (12).

Overall, the increase in the risk and funding costs of liabilities subject to bail-in should be considered in the context of the beneficial effects of the bail-in tool on bank funding. The new Regulation on the European market infrastructure (EMIR) aims at introducing greater transparency and better risk management to the ‘over the counter’ (OTC) derivatives market, as well as making this market safer by reducing counterparty credit risk and operational risk.

To reduce counterparty credit risk, the new rules introduce (i) stringent requirements for prudential (e.g. how much capital CCPs need to hold), organisational (e.g. role of risk committees) and conduct of business standards (e.g. disclosure of prices) for CCPs, (ii) mandatory CCP clearing for contracts that have been standardised (i.e. they have met predefined eligibility criteria), (iii) risk mitigation standards for contracts not cleared by a CCP (e.g. exchange of collateral). For further details on risks from CCPs, see Section III.1.6.

I.7. Leverage and asset decomposition

In the run-up to the financial crisis, banks’ leverage increased, with banks’ balance sheets expanding substantially. In the post-crisis period, in response to elevated funding costs, particularly on unsecured funding, banks aimed at decreasing their leverage, both by increasing capital and limiting asset growth, as can be seen in Chart 15. The trend was more pronounced for banks outside the euro area, but this fact was driven by banks resident in the United Kingdom.

Chart 15

Leverage multiple of EU banks

In the euro area, banks decreased their assets by approximately 10 % in 2009, with changes in 2010 and 2011 being less pronounced (see Chart 16). EU banks outside the euro area experienced, on aggregate, few adjustments in the size of assets until 2010, but these started growing again in 2011. From 2008 onwards, banks tried to recapitalise, and equity increased substantially throughout the EU by almost EUR 400 billion, albeit with a decrease of around 5 %, for the euro area banks in 2011. Total assets of banks in the euro area have increased by 14 % since 2007 but asset decomposition has also changed. Holdings of equity securities fell by 6 %, while loans to households increased by just 9 % and loans to MFIs by only 6 %. By contrast, other assets, loans to governments and debt holdings increased by more than 20 %. These figures give some evidence of weakened lending by the interbank sector as well as a relative decline in lending to households and corporations.

Chart 16

Changes in EU banks’ equity and assets

II. ASSET ENCUMBRANCE: INPUT FROM THE SURVEY

Asset encumbrance takes place when assets are used to secure creditors’ claims. These assets are therefore not available to general creditors in the event of a bank failure. This collateralisation can either be used for funding purposes (e.g. ABS, covered bonds and repos) or for trading and risk management (e.g. derivatives and securities lending). In some of these operations, banks do not encumber assets directly with their counterparty but rather with CCPs in operations which are cleared through those institutions. An encumbered asset is an asset that is, explicitly or implicitly, pledged or subject to an arrangement to secure, collateralise or credit-enhance any transaction.

Following the increased reliance on secured funding and the move towards collateralisation of other transactions (such as derivatives), asset encumbrance has expanded since the onset of the crisis. While this increase is fairly widespread, it is more significant for vulnerable banks and banks in vulnerable sovereigns. In fact, asset encumbrance cannot be disentangled from the crisis and its impact in terms of impairment of credit and interbank markets. Apart from these market constraints, the amount and types of secured debt are driven by many factors, first and foremost prices, collateral availability, over-collateralisation and maturities.

II.1. Overall levels of asset encumbrance

In the remainder of this Annex, the level of asset encumbrance is calculated as the ratio of encumbered assets to total assets (13). For methodological details, see Section VI.

The distribution of the level of encumbrance, for 2007 and 2011, is presented in Chart 17 (14). This ratio refers to all encumbered assets, including those assets received in a reverse repo (matched repos), measured against total assets. However, due to some uncertainties associated with the exact reporting methodology at some banks, intervals of encumbrance levels are presented instead of single figures. The data show that the median value of the encumbrance level for the sample of banks covered in this data collection exercise is around 25 % (or around 23 % when matched repos are excluded).

Chart 17

Distribution of the ratio of encumbered assets (including matched repos) to total assets, end-2011 (blue shading) and end-2007 (grey shading)

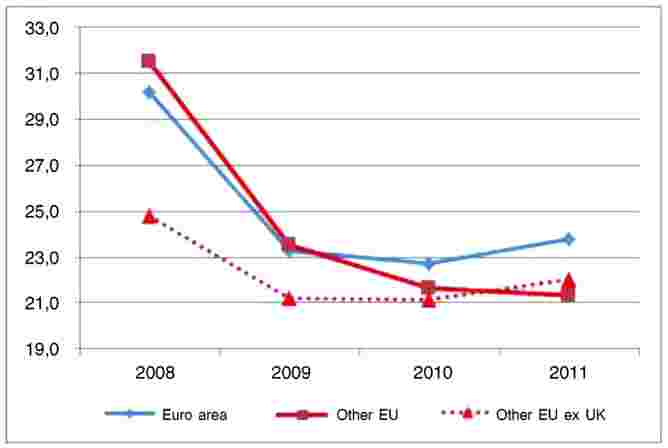

The levels of encumbrance have increased for almost all banks in the sample if the 2007 and 2011 data are compared (15). Taking a subsample of 28 banks reporting in both years, the median increased from 7 % to 27 % and the average, weighted by total assets, increased from 11 % to 32 % (when including matched repos).

Despite the widespread nature of this tendency, the significance of the increase in encumbrance levels varied depending on the banks’ characteristics. In fact, banks with lower credit ratings (lower than A) (16) systematically presented more striking increases in the level of encumbrance (Chart 18) (17).

Chart 18

Increase in encumbrance levels between 2007 and 2011 for groups of banks with different credit ratings ([percentage points) (18)

In 2011, higher rated banks (up to A) presented, on average, significantly lower levels of encumbrance (Chart 19) (19). While this is not a surprising conclusion, it should not be seen separately from the link between banks and their sovereign, as some of the banks that present higher levels of encumbrance are weighed down by sovereign risk. This difference in encumbrance patterns depending on banks’ and sovereigns’ resilience may be understood as a corroboration of the thesis that increased encumbrance is (at least partly) a consequence of the crisis.

Chart 19

Distributions of encumbrance levels for groups of banks with different credit ratings (percentages), end-2011

II.2. Impact of over-collateralisation on levels of encumbrance

Encumbrance levels depend on the type of transactions on which the asset pledge was made, notably on the inherent over-collateralisation requirements (see Chart 20). Repos, matched repos and securities lending are the type of secured funding which involves less use of collateral, as haircuts exercised are usually lower. However, higher rated institutions are those that are best positioned to take advantage of such transactions, since counterparties are more willing to engage in these operations with more resilient institutions (see also Chart 21). On the contrary, central bank funding, covered bonds and other collateralised securities require higher amounts of collateral.

Chart 20

Distribution of the over-collateralisation ratio by types of funding, end-2011

Chart 21

Distribution of the over-collateralisation ratio by collateral type, end-2011

The case of covered bonds requires further clarification. The level of over-collateralisation of covered bonds depends, broadly, on three factors: (1) regulatory requirements; (2) rating agencies’ requirements; and (3) institutions’ strategic choices regarding the over-collateralisation buffer that they wish to hold. Some national regulations require covered bonds to maintain significant minimum over-collateralisation levels (e.g. Spain (20)), some have over-collateralisation requirements which are fairly low (21) and another group requires the whole portfolio of eligible assets to be set apart for collateralising covered bonds (e.g. Slovakia), while others have no such requirements. This different treatment has non-negligible consequences in terms of over-collateralisation and therefore on levels of asset encumbrance. Whereas over-collateralisation can be partially justified by the regulatory regime, it also depends on the rating that institutions desire to achieve for their secured debt instruments, as higher over-collateralisation offers extra security for investors and thus permits higher ratings. Moreover, institutions decide on the buffer that they wish to hold on top of regulatory and rating agencies’ requirements. This is a strategic decision and practices differ among banks and across Member States as to whether this buffer is held inside or outside the cover pool.

II.3. Contribution of the different transactions to encumbrance

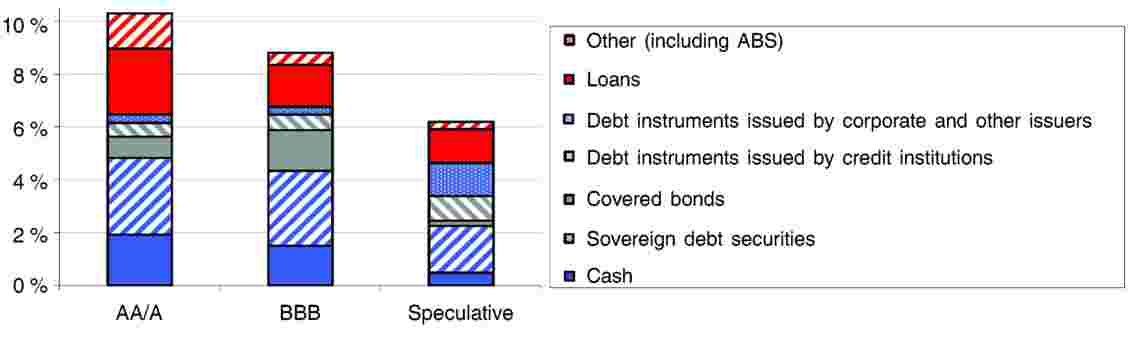

Unsurprisingly, more vulnerable banks (when assessed by their credit rating) tend to rely more heavily on secured funding and particularly on central bank funding, while higher rated banks have a more diversified structure of secured funding, with repos, securities lending and collateralised debt securities playing a very relevant role among funding sources. It should also be noted that while banks with a speculative rating appear to have only slightly higher levels of secured funding than banks with ratings up to BBB, given the amount of retained assets already ‘packaged’, but not yet used to obtain funding, by speculative-rated banks, those levels may rise.

Chart 22

Breakdown of secured funding for groups of banks with different credit ratings, end-2011

This leads to a relatively high encumbrance level at banks with the lowest rating; there are several reasons why this occurs. First, central bank funding involves a high amount of encumbered assets due to more pronounced over-collateralisation than for other types of funding (see Chart 20). Second, banks with the lowest rating may be excluded from private sector unsecured markets but may be able, in some cases, to issue secured funding instruments if they can post good quality collateral. Third, these banks have already exhausted a large portion of their assets that are eligible as collateral in central bank refinancing operations (see Chart 24, middle panel) and are increasingly using their own retained covered bonds and other collateralised securities as collateral to obtain funding from central banks. Fourth, such collateral nonetheless implies slightly higher haircuts than for banks with the highest rating (see Chart 24, left-hand panel).

III. RISKS

This section analyses the risks involved in (1) asset encumbrance; (2) innovative funding; and (3) concentration. The table below summarises the main risks and conclusions.

Table 2

Main risks stemming from funding developments

|

Asset encumbrance |

Innovative funding |

Concentration |

||||||

|

|

|

||||||

|

|

|

||||||

|

|

|

||||||

|

|

|

||||||

|

|

|

||||||

|

|

|

||||||

|

|

|

III.1. Risks from asset encumbrance

Risks arising from asset encumbrance can be broadly divided into the following groups: (1) structural subordination of unsecured creditors; (2) issues related to future access to unsecured markets; (3) issues related to transparency and correct pricing; (4) increased liquidity risks; (5) issues related to contingent encumbrance; (6) issues related to pro-cyclicality; and (7) other risks. In this section reference is also made to specific risks related to covered bonds and to operations with CCPs.

III.1.1. Structural subordination of unsecured creditors

One of the effects of asset encumbrance is that it shifts risks among investors. The claims of unsecured creditors, such as senior unsecured bondholders or depositors, tend to become riskier as a result of increased asset encumbrance, becoming increasingly subordinated as more secured debt is positioned above them. The magnitude of the risk shifting between creditors depends, among other things, on the degree of over-collateralisation (i.e. the extent of protection of more senior creditors), the type of other creditors, the business models and the general asset quality, as well as on the relative sizes of secured vs. unsecured debt and on the probability of default. The extent to which risk-shifting is a risk for unsecured creditors depends on their capacity to price that risk. Consequently, unexpected changes more than absolute levels of encumbrance are more problematic for existing unsecured creditors, since they do not have an opportunity to price such encumbrance changes.

III.1.1.1.

Since deposits are a form of senior unsecured funding for banks, encumbrance also increases the riskiness of deposits and ultimately the liability of deposit insurance funds (22). Structural subordination of deposits can be less of a concern in countries where deposit insurance funds are ex ante financed by premia paid by covered institutions. In such cases, the risk of increased tax-payers’ liabilities from asset encumbrance is partly reduced. To compensate deposit insurance funds for increased riskiness, premia paid by covered institutions could be risk-sensitive, namely with regard to risks stemming from encumbrance and subsequent subordination of depositors.

The increased riskiness of deposits is of particular concern in Member States without special depositor preference laws. Such laws grant seniority to deposit insurance funds, reducing a possible burden to tax-payers in case of credit institutions’ insolvency (23). Increased riskiness of deposits is also less of a concern in Member States where asset encumbrance tends to be low because of regulatory limits. Some Member States have placed direct limits on encumbrance due to covered bonds, while others have separated deposit-taking and mortgage lending. From the viewpoint of unsecured depositors and investors, it is important to analyse whether the remaining unencumbered assets could cover the unsecured liabilities. According to the survey conducted by the ESRB, for a majority of banks, this is still the case (see Chart 23), although two issues should be raised. First, the unencumbered assets do not sufficiently cover the unsecured funding for some reporting banks. Second, this coverage is lower among banks with lower ratings.

Chart 23

Distribution of the ratio of unencumbered assets to total unsecured funding for groups of banks with different credit ratings, end-2011

III.1.2. Issues related to future access to unsecured markets

1. Crowding-out of unsecured creditors

High levels of asset encumbrance, both for institutions whose levels are already high or for those with potential future increases, may feed expectations of further encumbrance. Such expectations may increase the cost of unsecured funding to levels that banks are unable or unwilling to meet. Moreover, as a result of strict criteria, the quality of encumbered assets is likely to be better than that of unencumbered assets. In the extreme case, banks’ funding may be skewed significantly towards secured debt, with over-collateralisation funded either by retail deposits (the only source of unsecured debt) and/or own funds.

Based on the ESRB survey, there is some evidence that the credit risk related to encumbered assets is generally lower than the credit risk related to unencumbered assets, once assessed by the risk weights. Conversely, there is no significant difference between encumbered and unencumbered assets when assessed by distribution into loan-to-value (LTV) buckets. The data show that this conclusion is also robust across individual reporting banks. Nevertheless, the different composition of assets in the two categories may cause some distortion in the comparison.

Such a development undermines financial stability since it worsens the structural subordination of depositors and banks’ liquidity position. This risk is less likely to materialise in a banking system with a liability set-up in which there is little subordination of other creditors or which has sufficient capital to deal with high encumbrance (e.g. the Nordic banking systems).

2. Retaining market access and discipline

High asset encumbrance can also reduce the variety of counterparties willing to invest in bank debt, potentially over-concentrating the market. Given that some institutions have limits on how large an exposure to a counterparty can be, this could add further limitations to their funding management.

With regard to market functionality, finance theory relies on the premise that unsecured debt investors have the right incentives to carry on monitoring activity and adjust prices accordingly. A bank that increases its reliance on secured funding (and consequently its encumbrance) would pay less attention to the discipline that unsecured creditors would try to impose via pricing of unsecured debt, as it would be less reliant on them.

3. Increased sensitivity of senior unsecured debt spread to fundamentals

In a low default environment, default is remote and the resulting structural subordination has limited or no real consequences for unsecured creditors. However, as the probability of default starts to increase, the effect of structural subordination should be rationally factored into spreads. Unexpected negative events could therefore lead to sharp jumps in the cost of unsecured funding, increasing the potential for disturbances in unsecured markets.

III.1.3. Issues related to transparency and correct pricing

Models and information used by rating agencies and others to factor in asset encumbrance and potential structural subordination deviate from actual empirical conditions and require continuous changes and updates. As models and information are updated and improved, there is a risk that senior unsecured debt may be downgraded, which in turn may also trigger the downgrading of secured funding (due to the current link between issuer rating and covered bond rating).