EUROPEAN COMMISSION

EUROPEAN COMMISSION

Brussels, 9.10.2017

SWD(2017) 330 final

COMMISSION STAFF WORKING DOCUMENT

Accompanying the document

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS

My region, My Europe, Our future:

The seventh report on economic, social and territorial cohesion

{COM(2017) 583 final}

Figure 4

1: Government effectiveness, 1996 and 2015

Figure 4

2: Citizens' confidence in institutions, 1996 and 2015

Figure 4

3: Economic impact of government effectiveness

Figure 4

4: Social impact of government effectiveness

Figure 4

5: Transparency International corruption perception index, 2012 – 2016

Figure 4

6: Trust in local authorities and perception of corruption in local government

Figure 4

7: Sustainable governance indictors – policy performance

Figure 4

8: Sustainable governance indictors – capacity and accountability of government

Figure 4

9: Macroeconomic effect of structural reforms

Figure 4

10: Professionalism, impartiality and 'closedness' of the public sector

Figure 4

11: Local Autonomy Index per country, 1990, 2000 and 2014

Figure 4

12: Local and regional self-rule, 2014

Figure 4

13: e-Government use by citizens, 2011-2016

Figure 4

14: Availability, usability, ease and speed of use of public online services

Figure 4

15: Transparency of e-Government

Figure 4

16: Ease of doing business, 2010-2017.

Figure 4

17: Regional differences in starting a company

Figure 4

18: Registration of companies online

Figure 4

19: Regional differences in dealing with construction permits and enforcing contracts

Figure 4

20: Discontinuity in the allocation of funds for entrepreneurship and SMEs

Table 4

1

Summary of analysis of effects of quality of government and other factors on growth of GDP per head

Table 4

2: e-Government benchmark: performance and progress

Map 4

1 European Quality of Government index, 2017

Map 4

2: Measuring meritocracy in the public sector in European regions

Map 4

4: Share of single bidders in public procurement (levels and changes)

Map 4

3: Public procurement using an open call for tender

KEY MESSAGES

·There is substantial evidence that the quality of government matters for social and economic development across the EU and that it is an important determinant of regional growth.

·The way that national regulations are implemented and their effect on development varies within countries reflecting differences in the efficiency of regional and local authorities.

·Institutional capacity affects the attainment of long-term policy objectives and the ability to implement structural reforms which have the potential to boost growth and employment.

·The perception of corruption remains widespread in a number of EU Member States and this erodes trust in governments and their policies.

·Professional and impartial public authorities are of major importance in combating corruption; however the degree to which meritocracy is a feature of the public sector, rather than nepotism, varies greatly between and within EU countries.

·Doing business is easier in the north of Europe than elsewhere in the EU, but central and eastern European countries are making significant efforts to catch up. There are major variations in the ease of doing business between regions in a number counties which point to differences in the administrative capacity of regional and local governments.

·In many regions across the EU, public procurement is open to the risk of corruption and a lack of competition for contracts as reflected in a number of instances where a contract was awarded when only one bid had been submitted.

·Governments in many parts of the EU have made significant progress in providing online access to services, but there has been insufficient focus on their quality and ease of use, so limiting their take-up and growth.

·A suitable institutional framework is important to facilitate the creation of new firms and to boost the effectiveness of cohesion policy support for entrepreneurship and business start-ups.

4.1.GOOD GOVERNANCE AFFECTS ECONOMIC GROWTH AND THE QUALITY OF LIFE

According to the dominant economic theories, economic growth is the result of a combination of three factors – physical capital, human capital (or labour) and innovation (or technical progress). By and large, investment in these areas has borne fruit in terms of greater convergence. However, there has been an apparent decline in the return on investment in all three areas and the variation in economic growth across EU regions that they are capable of explaining. This suggests that an important factor underlying growth is missing. According to a number of studies that factor is the quality of governance.

Many studies in recent years have highlighted the importance of this factor for economic performance and the fact that poor government in lagging areas in the EU represents a significant obstacle to development. Indeed, it has been found not only to adversely affect economic growth, but also the returns to cohesion policy investment and regional competitiveness, while corrupt or inefficient government undermines the regional potential for innovation and entrepreneurship. It has equally been found that low quality of government affects regional environmental performance and decisions on public investment and threatens inclusiveness and participation in the political process.

Institutional quality is a determinant of investment, and foreign direct investment (FDI) in particular, for a number of reasons. First, good governance is associated with higher economic growth, which should attract more FDI inflows. Secondly, low-quality institutions that enable corruption to occur add to the costs of investment and reduce profits. Thirdly, the high sunk cost involved in FDI makes investors highly sensitive to the political uncertainty inherent in low-quality institutions.

High-quality government has been found to be of outmost importance for the well-being of society, and there is broad consensus that good governance is a pre-requisite for long-term, sustainable increases in living standards. It has equally been found that the quality of governance strongly influences people’s health, their access to basic services, social trust and political legitimacy. It helps to explain why living conditions vary between countries and regions with much the same level of GDP per head.

High quality institutions can be defined as those which feature an “absence of corruption, a workable approach to competition and procurement policy, an effective legal environment, and an independent and efficient judicial system. [...] strong institutional and administrative capacity, reducing the administrative burden and improving the quality of legislation” (European Commission, 2014, p. 161). Such a broad definition is in line with academic studies which view good governance as the impartial exercise of public power, focusing on policy implementation rather than the content of policies or the democratic process through which they are decided.

In sum, there is a growing consensus that the quality of governance and institutions is a fundamental precondition for sustained increases in prosperity, well-being and territorial cohesion in the EU.

4.2. QUALITY OF GOVERNANCE VARIES SUBSTANTIALLY IN EUROPE

Governance encompasses the traditions and institutions by which authority in a country is exercised. This includes the process by which governments are selected, monitored and replaced; the capacity to formulate and implement sound policies and the respect of citizens for the institutions that govern economic and social interactions between them. The institutional environment of a country depends on the efficiency and behaviour not only of public but also of private stakeholders.

Every year the World Bank produces the Worldwide Governance Indicators (WGI), covering over 200 economies, to denote the quality of the institutions responsible for governance. Governance itself is defined according to dimensions related to accountability, political stability, government effectiveness, regulatory quality, confidence in institutions and absence of violence and control of corruption. The changes between 1996 and 2015 in the indicators of the effectiveness of government and citizens' confidence in institutions are set out in

Error! Reference source not found.

and

Error! Reference source not found.

.

|

Figure 01: Government effectiveness, 1996 and 2015

|

Figure 02: Citizens' confidence in institutions, 1996 and 2015

|

|

|

|

Data source: World Bank Worldwide Government Indicators 2015

|

The indicator for government effectiveness takes account of government policies, the quality of public services provided and the extent of independence of the civil service from political pressure as well as the credibility of the government. All these aspects contribute to creating the stable political environment needed for sustained economic growth.

The EU countries assessed as having the most effective governments in 2015 were Denmark, the Netherlands, Finland and Sweden. Those with the least effective were Romania, Bulgaria, Greece and Italy, the difference between the two groups being substantial. While Denmark, Netherlands, Finland and Sweden were among the 10 best performing countries in the world, Romania was ranked below the global average.

Between 1996 and 2015, government effectiveness diminished in 7 EU countries (Luxembourg, Austria, Belgium, Spain, Hungary, Italy and Greece) and increased in 8, all of them in the EU-13, most notably in Latvia, Lithuania and Estonia, which climbed to the middle of the EU ranking. Among the Member States with the least effective governments, the situation improved in Romania, Bulgaria and Croatia and worsened in Greece, Italy and Hungary.

Guaranteeing opportunities for democratic participation and respect for the rules of a society, its institutions and civil rights help to generate the confidence of people in the legitimacy of actions taken by political leaders and to establish the support for them which is necessary to make them effective.

The indicator of citizens' confidence in institutions relates to the confidence people have in social rules (like contract enforcement or property rights), social institutions (the police and law courts) and their own safety (measured by the likelihood of being affected by crime and violence). It shows a similar pattern to the government effectiveness indicator (

Error! Reference source not found.

). Finland, Sweden, Denmark and the Netherlands are ranked highest, Romania and Bulgaria, lowest. The three Baltic countries again show the biggest improvement, once more climbing to the middle of the EU ranking, and there is a similar improvement for Croatia, though it remains at the lower end of the ranking.

There is a close correlation between government effectiveness and economic competitiveness (

Error! Reference source not found.

). Whereas, however, the most competitive countries tend to have the most effective governments, the fastest growing EU economies in recent years (Bulgaria, Romania and Poland) tend to have the least effective ones. This suggests perhaps that in the early stages of development, other factors play a dominant role, but to sustain growth requires improvements in the quality of government. The correlation between government effectiveness and life satisfaction is equally close and confirms the importance of the quality of government for people’s lives.

|

Figure 03: Economic impact of government effectiveness

|

Figure 04: Social impact of government effectiveness

|

|

|

|

|

|

Data source: World Bank Government Effectiveness 2015; World Economic Forum. Global Competitiveness 2016-2017.

|

|

Data source: World Bank Government Effectiveness 2015; Standard Eurobarometer 83, Spring 2015.

|

There are significant variations across regions in the quality of government which reflect the way in which national regulations are implemented and differences in the efficiency of regional and local authorities in this respect. These differences are important to take into account when assessing the quality of governance in relation to economic and social development. A reginal European quality of governance index (EQI), constructed by the Gothenburg Institute of Quality of Government, which measures people’s perceptions of this in different policy areas, enables this to be done.

The perceived quality of government varies markedly between and within EU Member States. People in Sweden, Finland, Denmark, the Netherlands and Germany are the most positive about the quality and impartiality of education, healthcare and law enforcement. People living in regions in Romania, Bulgaria and Italy are the least positive.

The index shows the greatest variation between regions in Spain, Italy, Belgium, Romania, Bulgaria, Hungary and the Czech Republic. This suggests that the quality of services provided locally may vary substantially in countries with regions that are both politically and administratively relatively autonomous (Spain, Italy and Belgium) as well as in countries which are more centralised.

The quality of government and institutions appears to be the main obstacle to development in regions with persistently low growth rates. Indeed, the 2017 EQI results for Italy, Greece and Spain imply that some less advantaged regions in these countries may be stuck in a low-administrative quality, low-growth trap. In regions in the east of the EU, especially in those in Bulgaria and Romania, which have enjoyed relatively high growth over the past decade or so, the poor quality of government which is evident may eventually put a break on development and the move to a higher value-added economy (A. Rodriguez-Pose, T. Ketterer, 2016).

The results of the 2017 survey are much the same as for 2013 indicating that improvements in government may take time. Indeed, for them to occur is likely to require concerted efforts at all levels of the administration as well as the active involvement of the public at large.

Map 01 European Quality of Government index, 2017

4.2.1. Quality of governance as a determinant of regional growth

A recent study on the determinants of regional growth between 1999 and 2013 (Rodriguez-Pose & Ketterer, 2016) was aimed at differentiating between the role of traditional aspects of investment policy, such as infrastructure, human capital and innovation, and that of various institutional aspects.

The effect of the quality of regional government and changes in this is included in the regression analysis as both an aggregate measure (

Table 0

1

, left panel) and separately in terms of the four main constituent aspects distinguished: corruption confidence in police and regional law enforcement, government effectiveness, and government accountability (

Table 0

1

, right panel).

Table 01 Summary of the analysis of the effects of quality of government and other factors on growth of GDP per head

Source: own calculations on the basis of A. Rodriguez-Pose, T. Ketterer (2016).

Note: Panel data analysis for 249 NUTS 2 regions in the EEU using a standard Solow-Swan-type growth model. Investment is measured by gross fixed capital formation as a % of GDP. All independent variables are included with a 5-year lag. Variables are expressed in terms of natural logarithms apart from population growth. All regressions include a constant time trend.

In line with the predictions of neoclassical growth theory, there is a significant and negative relationship between growth rates and initial GDP per head, so implying a tendency towards convergence.

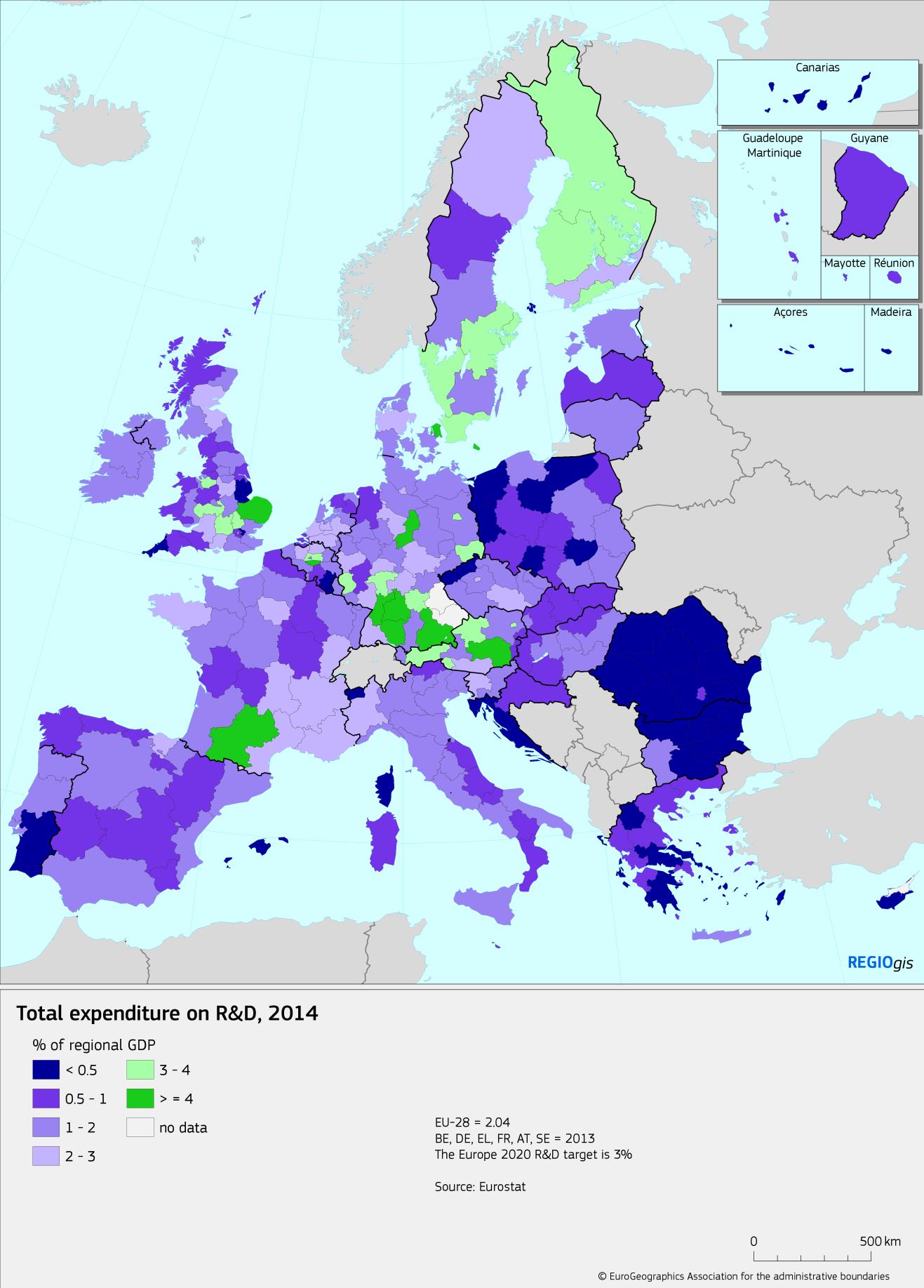

The three basic factors identified by growth theory do not seem to have been important in determining changes in GDP per head of regions over the period of economic expansion followed by recession. Following the abrupt change in economic conditions in 2008, the determinants of growth during the boom years no longer seem to work in the same way. The initial level of regional investment, accessibility, population growth and the quality of regional institutions do not appear to be important in explaining differences in the growth of GDP per head between regions over the crisis years. The same is true of Human capital accumulation and R&D expenditure relative to GDP (as a measure of innovation efforts), though employment of those with tertiary education continues to have a significant positive effect on growth. On the other hand, changes in the quality of institutions show a continuously positive and statistically significant effect over the period.

Indeed, improvements in the quality of institutions appear to have been among the most consistent factors underlying economic growth and resilience across the EU. Accordingly, the implication is that bringing about such improvements by either tackling widespread corruption or introducing measures aimed at making government decisions more efficient and transparent is important for regional development, as important, indeed, as physical investment.

4.2.2. Corruption remains widespread in many EU countries and may erode social capital

Corruption is a drag on economic growth. The true social cost of corruption cannot be measured solely by the amount of bribes paid or public funds diverted. It also includes the loss of output due to the misallocation of resources, distortion of incentives and other inefficiencies that it causes. Corruption can also have perverse effects on the distribution of income and give rise to a disregard for environmental protection. Most importantly, corruption undermines trust in legitimate institutions, diminishing their ability to provide adequate public services and an environment conducive to business development. In extreme cases, it may lead to the state losing its legitimacy, giving rise to political and economic instability, so reducing business investment and making sustainable development harder to achieve. (OECD, 2013b).

The Corruption Perceptions Index (CPI), first launched in 1995 by Transparency International, has been widely credited with putting the issue of corruption on the international policy agenda. The CPI each year ranks countries by their perceived levels of corruption, as assessed by experts and through opinion surveys. Corruption is defined as the misuse of public power for private benefit and the index combines data from 13 sources to judge this. As the methodology was updated in 2012, the following focuses on the changes since then

.

In 2016, the CPI ranked 176 countries on a scale from 100 (very clean) to 0 (highly corrupt). The global average score is 43, indicating endemic corruption in many governments across the world. The average score of EU countries is 65, with 6 countries having a score below 50 and 7 in Northern and Western Europe having one above 80.

Figure 05: Transparency International corruption perception index, 2012 – 2016

|

Panel 1: Results in 2016

|

|

|

|

Panel 2: Change 2012 – 2016

|

|

|

|

Source: Transperency international

|

While the general trend over the 5 years 2012-2016 is upwards, there were some significant downward movements in the last year. On average, there was a decline in EU countries of 0.75 of a point and three places in the ranking. Respondents in 12 EU Member States assessed corruption as being worse than a year earlier, with the biggest reduction in scores being in Cyprus (6 points.), the Netherlands (4), Hungary (3) and Greece, Croatia, Lithuania and Ireland (2 in each), which meant a fall of 10 or more places in the ranking for Cyprus and Greece (as well as for the Czech Republic and Malta because of increased scores for other countries). It remains to be seen whether this is a long-term reduction or the reaction to one-off events (like a corruption scandal in the Netherlands which happened shortly before the survey). At the same time, there was increase in the score in Italy (by 3 points) and Romania and Latvia (by 2 points in each).

The ranking of the best performers among EU Member States did not change much over the 5 years. In particular, Denmark was ranked first throughout the period with Finland and Sweden close behind. There are more changes in the middle-ranking countries with Estonia, Latvia, Lithuania, the Czech Republic and Poland having the biggest increases.

Over the 5 years, 5 countries stand out as not following the general trend towards improvement. In Cyprus, Spain and Hungary, there was a significant increase in perceived corruption while in Bulgaria and Malta, it remained unchanged.

4.2.3. Trust in local authorities in line with perceptions of corruption

Corruption erodes trust in public services. According to various surveys carried out for the European Commission and information from the World Justice project, trust in local authorities and people’s perception of corruption in them go hand in hand.

Countries and cities in which people trust their local government are also those in which people believe the authorities concerned are not corrupt (such as in the Nordic countries or Austria) while in a large parts of central, eastern and southern Europe, local authorities are perceived as being prone to corruption. Hungary, Romania and Belgium are somewhat different in that there is a relatively high level of trust in local authorities even though they are regarded as being relatively corrupt. The three countries with the lowest level of trust in local authorities (less than 35% of those surveyed reporting having trust) were Bulgaria, Poland and Italy, in all three of which perceptions of corruption among local officials were the most widespread.

Figure 06: Trust in local authorities and perception of corruption in local government

Source: Cities report

National averages hide some marked differences in how people perceive the situation in different cities. For example, Marseille stands out from other French cities with only 30% expressing trust in the local government (as opposed to 55% in Lyon) and as many as 40% believing that local officials are involved in corrupt practices (as against just 15% in Lyon). Equally, in Hungary, a much larger proportion of people trust local officials in Miskolc (80%) in the north-east of the country than in Szeged (50%) in the south.

4.3. INSTITUTIONAL CAPACITY AFFECTS POLICY PERFORMANCE AND CAPACITY TO CONDUCT REFORMS

Public administration reflects the institutional basis on which countries are run and its quality determines performance in all areas of public policy. Public administration is responsible for responding to the needs of society and as such it has significant effect on the pace of economic and social development and its sustainability.

4.3.1. Professional and impartial administrations provide better policy outcomes for citizens

In a context of a rapidly changing environment and challenges such as globalisation, social inequality and demographic change, any assessment of sustainable governance needs to focus on policy outcomes, the underlying democratic order and people’s confidence in institutions as well as in the capacity of government to implement policies successfully.

The Sustainable Governance Indicators, developed by Bertelsmann Stiftung, are intended to indicate how well policies have performed in achieving long-term objectives by examining outcomes in 16 areas. The indicators are built on three indices – the Policy performance index, the Democracy index and the Governance index– which together determine the sustainability of governance (see Box). As the confidence in institutions was discussed above, the focus here is on policy performance and governance.

|

Sustainable Governance Indicators explained

The Policy Performance Index aggregates data compiled on policy outcomes in 16 areas that cover the three dimensions of sustainability (economic development, environmental protection and social policies).

The Democracy Index is based on an analysis of each country’s democratic order and people’s confidence in institutions on which it is founded. It assesses the substantive and procedural features of a system that enable long-term oriented governance to be sustained.

The Governance Index assesses a government’s capacity to steer and implement policies, its capacity for institutional learning and reform and the extent of executive accountability.

Source:

http://www.sgi-network.org

|

The Sustainable Governance Indicators (SGI) show major differences between EU Member States in terms of both the design of economic and social policies and the capacity of institutions to implement them and achieve desired outcomes. Sweden, Denmark and Finland score the highest on policy performance, while Cyprus and Greece score the lowest (Figure 4-7). Germany, Luxembourg and the UK are ranked only slightly below the three Nordic countries, though also Estonia and Lithuania, while Hungary Romania, Croatia and Bulgaria are ranked only a little above Greece and Cyprus.

France, Slovenia, the Czech Republic and Austria score better on the implementation of social policies than the EU average but worse as regards economic policies. On the other hand, Latvia and Malta score well above the EU average on economic policy but below average on social policy.

Figure 07: Sustainable governance indictors – policy performance

The Governance index of the SGI is intended to capture the extent to which, on the one hand, a country’s institutional arrangements increase the government’s capacity to act (‘executive capacity’) and, on the other, NGOs, other organisations and the public in general have the ability to hold government accountable for its actions (‘executive accountability’).

Again the Nordic countries, followed by Germany, Luxembourg and the UK, have the most capable and accountable governments in the EU (

Figure 0

8

), while Greece, Cyprus, Croatia, Hungary, Romania and Bulgaria have the least capable and accountability. In Belgium and the Czech Republic, stakeholders are relatively closely involved in policy making, but governments are less capable than the EU average. In Lithuania and Latvia, on the other hand, the authorities are relatively capable, but there is less involvement of stakeholders than average.

Figure 08: Sustainable governance indictors – capacity and accountability of government

4.3.2. Potential benefits of conducting structural reforms is huge

Putting in place conditions conducive for investment, growth and jobs is an important pre-condition for sustainable economic development. According to European Commission analysis, large potential benefits in terms of GDP, productivity and employment growth can be obtained through structural reforms relating to market competition and regulation, taxation, the labour market, unemployment benefits and investment in human capital and R&D.

Simulations using the Quest model of structural reforms that would halve the gap with the best performers show that they could boost GDP by 3% after 5 years over what it otherwise would be, almost 6% after 10 years and 10% after 20 years (

Figure 0

9

, which shows the effect on GDP in panel 1 and on employment in panel 2 assuming all Member States were to implement reforms). The effect on employment is smaller because of the boost to productivity but still significant.

According to the model, the reforms with the largest impact relate to increasing the participation rates of women and of people of 50 and over in the labour force and increasing the proportion of workers in employment who have tertiary-level education, and correspondingly reducing the proportion with only basic schooling. Improving the business environment also has a significant effect.

Figure 09: Macroeconomic effect of structural reforms

|

Panel 1

|

|

|

|

Panel 2

|

|

|

|

The figures show the results of the Quest model simulation in terms of the % difference in GDP and employment compared to a ‘no-reform’ scenario assuming all Member States implement reforms. Source: Varga J. and J. in’t Veld (2014) 'The potential growth impact of structural reforms in the EU. A benchmarking exercise", European Economy, Economic Paper no. 541'

|

Structural reforms can potentially have a big impact on lagging regions, accelerating the process of catching-up.

4.3.3. Meritocracy of the public sector varies greatly between and within EU countries

The Quality of Government Expert Survey, which is intended to assess the organisation of public bureaucracies and their behaviour in different countries worldwide, is based on the views of over 1 000 experts. It covers such issues as recruitment procedures, internal promotion, career stability and salaries. The results are presented in three indices relating to professionalism, 'closedness' and impartiality.

They show that Western and Nordic EU counties tend to have more professional and impartial public administrations than the southern and eastern Member States, Poland, Lithuania and Estonia being the only ones of the EU-13 that are assessed as being above the EU average in terms of both professionalism and impartiality.

Whether the model is more ‘public-like’ (or ‘closed) or 'private-like’ (or ‘open’) is not the decisive factor in determining professionalism or impartiality. Sweden, Finland, Denmark, Estonia and Netherlands have 'private-like' rules of hiring and career building but are assessed as being relatively impartial and professional. On the other hand, France and Germany have a more closed and formalised system but have officials who are assessed as being professional and impartial.

Figure 010: Professionalism, impartiality and 'closedness' of the public sector

|

|

|

|

Note: Professionalism index: higher values indicate a more professional public administration. Closedness index: higher values indicate a more closed public administration. Source: own calculations on the basis of The QoG Expert Survey Dataset II.

|

According to a recent study carried out by Charon, Dahlström and Lapuente (2016), based on the results of the European Quality of Government Survey, regional and local governments across the EU vary markedly in terms of the perceived level of meritocracy, as opposed to nepotism, in appointments of public officials and their promotion (

Map 0

2

). Whereas meritocratic principles tend to predominate in large parts of the UK, Germany and Finland (which have scores of less than 5 – low scores signifying an absence of nepotism), ‘luck and connections’ are considered the main determinants in most parts of the EU-13, Italy and Greece.

Map 02: Measuring meritocracy in the public sector in European regions

The degree of local autonomy also varies across the EU (

Box 1

).

|

Box 1: Local autonomy and self-rule

The extent of autonomy of local governments in European countries has increased since 1990 according to the Local Autonomy Index. There are, however, significant differences in autonomy across Europe.

Figure 011: Local Autonomy Index per country, 1990, 2000 and 2014

Local authorities in the Nordic countries have a high degree of autonomy as do those in Germany, Switzerland and Poland, while those in Cyprus, Malta and Ireland have the lowest levels in the EU (

Figure 0

11

). There were increases in local autonomy in the EU-13 countries between 1990 and 2014, especially in the early years of the transition, but it still remains less than in the EU-15 where there was only a small increase over the period.

In most countries, local authorities have more autonomy than regional authorities (

Figure 0

12

). Only in Belgium, Italy, Austria, Spain, Germany - countries with a strong regional or federal structure of government as well as in Ireland - is the degree of regional self-rule greater than at local level, though even in these countries, local authorities have significant discretion over policy.

Figure 012: Local and regional self-rule, 2014

|

4.3.4. Governments have advanced in making public services available online, but have focussed less on the quality of the delivery from the user’s perspective

The use of ICT in the public sector, if implemented correctly, is beneficial for both people and governments. It can reduce administrative costs and the burden of bureaucracy, lead to institutions being re-organised in more citizen-friendly ways and increase transparency. Accordingly, it can increase the general efficiency of government and result in the interaction of people and businesses with public authorities being easier and less time-consuming. The extent of e-Government, its quality and the take up of public e-services varies markedly across the EU (

Box 2

).

|

Box 2: e-Government Benchmark project

The e-Government Benchmark assesses the priority areas of the e-Government Action Plan 2011-2015. Progress in each area is measured by one or more indicators:

·User-centric government assesses the availability and usability of public e-Services and the ease and speed of using them.

·Transparent government assesses the transparency of government operations, service provision procedures and the level of control users have over their personal data.

·Cross-border mobility measures the availability and usability of services for people and businesses abroad.

·Key enablers assess the availability of 5 functions, such as e-ID cards.

The assessment in each area is based on responses to a number of questions regarding the quality or quantity of e-Government services on a specific aspect.

Source: EU e-government benchmark project

|

Table 0

2

shows how EU Member States performed in 2016 compared to the average of 34 European countries. The Nordic countries, the Baltic States, the Benelux countries, Germany, France and Austria performed best and show the most growth in e-Government.

Table 02: e-Government benchmark: performance and progress

|

Moderate performers

(both growth and absolute score below European average)

|

Steady performers

(absolute score above and growth below European average)

|

Accelerators

(both growth and absolute score above European average)

|

|

United Kingdom, Ireland, Poland, Czech Republic, Slovakia, Hungary, Italy, Slovenia, Croatia, Romania, Bulgaria, Greece, Cyprus,

|

Finland, Spain, Portugal, Malta

|

Sweden, Denmark, Estonia, Latvia, Lithuania, Germany, Austria, Netherlands, Belgium, Luxembourg, France

|

|

Notes: European average means average for: EU member states, Norway, Iceland, Switzerland, Serbia, Montenegro and Turkey. Average score: 61%. Average growth: 8%.

Source: Own calculations based on the EU e-government benchmark project.

|

In 2016, almost one in two of those in the EU (48%) used e-Government, and around four in every five or more in Denmark (88%), Finland (82%) and Sweden (78%). The share increased over the preceding 5 years in all Members States, except Slovakia, the Czech Republic and Bulgaria (

Figure 0

13

), the biggest increases being in Latvia (28 percentage points) and Estonia (24 percentage points). In the four countries with the smallest usage, Poland, Italy, Romania and Bulgaria, there was little change over the period in the first three and a reduction in the last.

Figure 013: e-Government use by people, 2011-2016

Source: Eurostat

E-Government services potentially provide flexible and personalised ways of interacting and performing transactions with public authorities. However, the 'use of e-government' indicator reveals nothing about the frequency of use or the completeness of online services and their quality. Nor does it indicate their transparency, which can help to build trust between the government and the general public, as well as making policy-makers more accountable.

According to the e-Government benchmark project, governments have advanced in making public services digital but have tended to focus less on quality. While the online availability of services and their usability have increased, quality and functionality, which are important for fast and easy take-up, have barely increased at all which is equally true of the transparency of procedures in large parts of the EU.

Most countries score more highly on online availability and usability than on indicators relating to the take-up of online services (

Figure 0

14

, right panel, which shows all EU countries as being below the diagonal). Accordingly, simply providing information and services online is not sufficient to create user-centric e-Government services.

Figure 014: Availability, usability, ease and speed of use of public online services

|

|

|

|

Source: Own calculation on the basis of EU E-Government Benchmark project data set.

|

There are marked differences between countries in terms of transparency as well as variations between the three indicators used to measure this, which might indicate a lack of coordination between different parts of government (

Figure 0

15

).

Malta, Estonia and Latvia score highest in terms of the publication of information and delivery of services, while Bulgaria, Hungary and Romania score lowest on the publication of information and Greece and Slovakia on the delivery of services. Malta also scores highest on transparency in relation to personal data followed by France with Slovakia, Hungary, Romania and the Czech Republic scoring lowest.

Figure 015: Transparency of e-Government

Source: EU E-Government Benchmark

Online public services are becoming increasingly accessible across the EU but growth is uneven and many Member States are lagging behind. For successful implementation of e-Government, there is a need for demand-side measures as well as supply-side ones, which means online services being designed with the user in mind.

4.3.5. Doing business is easier in the North of Europe, but central European countries are trying to catch up

Effective government policies are crucial to prevent market failure, distribute income and wealth more equitably and minimise social inequalities. Simplicity, clarity and coherence of business regulations can provide stable and predictable rules for enterprises to function effectively, so encouraging long-term growth and sustainable economic development.

The World Bank ’Doing Business‘ indicators assess 10 regulatory areas which affect economic activity: starting a business, dealing with construction permits, getting electricity, registering property, getting credit, protecting minority investors, paying taxes, trading across borders, enforcing contracts and resolving insolvency. The 2017 edition compares the efficiency and quality of business regulations for SMEs in 190 economies across the world, the overall ranking being constructed on the basis of how far they are from the best performing economy (‘distance to frontier’).

The Nordic countries (Denmark is ranked third in the world) and Baltic States together with the UK, Germany and Ireland are assessed as having the most friendly business environments in the EU, while , Cyprus, Italy, Luxembourg and Malta (which is ranked 76th in the world) have the least friendly.

|

Figure 016: Ease of doing business, 2010-2017.

|

|

Source: Own calculations on the basis of World Bank Doing Business.

|

Many policy reforms have been introduced over the past decade to make business environments more ‘enterprise friendly’ and conducive to firm creation and growth. Between 2010 and 2017, the distance to the highest ranking economy shortened for all EU countries, except the UK, Belgium and Ireland (see

Figure 0

16

). The biggest improvements were in Poland, the Czech Republic and Slovenia, each of which jumped from the bottom of the EU ranking to the middle. There were significant improvements too in Croatia and Romania, but they remain among the Members States furthest from the frontier.

The sub-national doing business indicators, however, reveal substantial regional differences despite operating within the same legal and regulatory framework. So far, the indicators exist for only 6 EU countries: Italy (2012), Spain (2015), and Poland (2015) and Bulgaria, Hungary and Romania (2017). (Indicators for Portugal, the Czech Republic, Slovakia and Croatia will be produced for 2018-2019.) The indicators for 5 of these countries, all apart from Italy, are considered below.

Starting a company is easiest and quickest in Hungary, while it takes longest to do so in Polish cities (except in Poznan) - up to 42 days in Szczecin as compared with only 6 days in Szeged in Hungary. The cost of registration is also higher in Polish cities than in Hungarian ones, due to the use of online registration (which is why it is lower in Poznan). However, online registration in itself does not necessarily speed up the process – as, for example, in Kielce (also in Poland), where 40% of registrations were made online but it still took as long. To make online platforms work, they need to be accompanied by both measures stimulating business take-up and the possibility of completing the entire process online (i.e. without the need for paper copies). In some of the regions in Poland, the introduction of online registrations did not remove the need for paper copies of documents since communication with the local court remained paper-based.

In all countries, except Hungary, there is a large variation between different cities: in Romania, registration takes 12 days in Timisoara but 25 days in Craiova; in Spain, it takes 14 days in Gijon but 31 days in Ceuta.

Figure 017: Regional differences in starting a company

|

|

|

Source: Subnational doing business reports for: Poland, Spain and Bulgaria, Romania and Hungary.

Figure 018: Registration of companies online

Similar differences between cities relate to the time needed to deal with construction permits. This is especially so in Spain, where in Logrono (in La Rioja), the process takes 100 days but in Vigo (in Galicia) almost 300 days. In general, it is relatively easy to deal with construction permits in Bulgaria – all 6 cities are in the upper half of the ranking – and relatively difficult in Romania (all cities being in the bottom half of the ranking).

Enforcing a contract shows the most variation in all 5 countries for which data are available

, ranging in Bulgaria from 289 days in Pleven to 564 in Sofia, while in Poland, it takes more than a year longer in Gdansk than in Olsztyn.

|

Figure 019: Regional differences in dealing with construction permits and enforcing contracts

|

|

|

|

Note: No subnational data for Spain for enforcing contracts. Source: Subnational doing business reports for: Poland, Spain and Bulgaria, Romania and Hungary.

|

The wide differences in time, procedures and costs between different places within countries imply that improving local and regional administrative capacity can produce significant gains in the ease of doing business.

4.3.6. Public procurement is open to the risk of corruption and lack of competition in many EU regions

Public procurement, the process of purchasing of goods and services by the public sector, plays a crucial role in economic and social development across the EU. It covers, on average, 29% of government spending, equivalent to some 13% of EU GDP (European Commission, 2016; OECD, 2015). It is a principal means through which governments can influence the quality of investment and public services and so affect economic growth. In addition, the ESI Funds are largely spent through public procurement. It is a genuinely cross-cutting government function which concerns virtually every public body from federal ministries to local state-owned utilities, making it representative of the quality of government in general.

Recent research has attempted to assess different aspects of the quality of governance on the basis of public procurement data (Fazekas, 2017, upcoming; Fazekas and Kocsis, 2017). Indicators relating to use of open procurement procedures, the ratio of single bidders may provide an insight into transparency, competition and corruption (see

Error! Reference source not found.

).

|

Principles and indicators used for measuring the performance in public procurement

The principle of transparency implies that information on public procurement should be readily available in a precise, reliable, and structured form (Kovacic, Marshall, Marx, & Raiff, 2006). In a narrower sense, it can be defined as compliance with the information disclosure requirements in EU Public Procurement Directives.

The principle of competition implies that the beneficial effects of multiple bidders competing against each other and having equal opportunity to participate take the form of low prices, high quality and on-time delivery of the goods, facilities or services procured (Arrowsmith, 2009).

Corruption in public procurement is defined as the allocation and performance of government contracts by bending rules and principles of open and fair public procurement in order to benefit a closed network while denying access to all others (Fazekas, Tóth, & King, 2016).

Definitions of public procurement governance indicators:

-use of open procedures: contracts awarded in an open or restricted procedure as a % of all contracts awarded;

-single bidding: contract awarded when only one bid was submitted as a % of all contracts awarded.

The indicators are based on information published in the Tenders Electronic Daily (TED) database.

Source: Fazekas, M., Assessing the quality of government at the regional level using public procurement data (upcoming)

|

The number of instances where there was only a single bidder as a share of all contracts awarded through public procurement might indicate potential corruption or a lack of competition, including collusion between companies in a given sector of the economy. The single bidder-ratio varies significantly across regions (

Map 0

3

(left panel)). The cases where there was only one bid exceeds 40% in many regions in Greece, Poland, Slovakia and Italy. In regions in Sweden, Ireland, UK and Denmark, the ratio rarely exceeds 10%, pointing towards more competitive markets and less sign of corruption. The single bidder ratio shows wide regional differences in Romania, Bulgaria, Poland, Hungary, the Czech Republic and Spain, whereas in Sweden and Greece, there is almost no variation. Between 2007 and 2015, the ratio declined markedly in Lithuania, Latvia and in many regions in Poland, the Czech Republic and Slovakia. By contrast, in Greece, Italy and Estonia – countries with high levels of single bidding – the proportion of contracts issued where there was only one bid increased.

Map 03: Share of single bidders in public procurement (levels and changes)

|

|

|

|

Source: Own elaboration on the basis of Fazekas, M., (upcoming)

|

|

|

It is worth noting that, while in general public procurement governance scores correlate with the European quality of government index, regions in Spain score considerably better than on the EQI. On the other hand, Finland and Estonia scores are lower (Fazekas 2017, upcoming), perhaps because of a lack of transparency suggesting weaknesses in national regulatory and information systems or less competition from international suppliers.

The use of open procedures is one of the indicators to measure transparency of procurement. The results (

Map

0

4

) do not show the usual North-West versus East-South divide like many indicators of governance. Counter-intuitively, countries with a high level of single bidding (Poland, Greece) are among those with the most use of open procedures, which may indicate a prevalence of informal connections over formal requirements. Use of open procedures is relatively infrequent in a number of regions in Hungary, Austria, Estonia, France and Bulgaria. There is a need for caution, however, when interpreting the results, since while not using open procedures hampers competition, their overuse might indicate a lack of administrative capacity to run more complicated procedures (such as negotiated ones).

Map 04: Public procurement using an open call for tender

|

|

|

|

Source: Fazekas, M., Assessing the quality of government at the regional level using public procurement data (upcoming)

|

4.4.

Suitable institutions increases the effects of EU support on entrepreneurship

As evidenced by the 6th Cohesion report a lower standard of governance can affect the impact of Cohesion Policy and lead to funding losses. The report also noted that quality of government may reduce the returns from public investment, including that financed under cohesion policy (Rodriguez-Pose, Garcilazo, 2014).

According to a recent study by Diaz Ramirez, Kleine-Rueschkamp and Veneri on the relationship between the growth of businesses, institutions and support of entrepreneurship by the ESI Funds, the ‘right’ set of institutions tends to increase the effects of cohesion policy.

Figure 01: Discontinuity in the allocation of funds for entrepreneurship and SMEs

|

|

|

Source: Diaz Ramirez, M., Kleine-Rueschkamp, L., Veneri, P. (2017), “Does quality of governance affect the returns of policy for entrepreneurship?”, Paper presented at the 57th Congress of the European Regional Science Association, Groningen 29 August – 1 September 2017

|

The amount of EU funding received in the 2007-2013 period was found to significantly affect business growth. Regions with GDP per head just below 75% of the EU average, which accordingly received relatively large amounts of funding, recorded considerably more enterprise births as well as deaths than regions that had GDP per head just above the 75% threshold and so received much less funding. (

Figure 0

1

shows this 'discontinuity' in allocations from ESI funds for entrepreneurship and SMEs.) Overall, there was no relationship between the amount of funding and the total number of enterprises. At the same time, the ‘right’ set of institutions seems to affect the relationship, in that the rate of business creation was significantly larger in regions where corruption is perceived as being relatively limited than in those where it considered to be relatively widespread. This was particularly the case for ‘employer’ firms (i.e. those with employees).

4.5.

Conclusions

The way that national regulations are implemented varies across regions, reflecting differences in the efficiency of regional and local authorities which are important to take account of when assessing the quality of government in relation to economic and social development.

The quality of government matters for regional development across the EU. The institutional dimension, therefore, needs to become an integral element in development strategies. Along with strengthening infrastructure endowment and human capital, it is important that there are improvements in administrative capacity and the effectiveness of government as well as reductions in the incidence of corruption, which erodes trust in government and their policies.

While governments have advanced in making public services digital and providing access to them online, there has been insufficient focus on the quality of online services from a user’s perspective and their ease of use. .

Institutional capacity affects the ability of government to attain of long-term policy objectives and to make structural reforms which have significant potential to boost growth and employment.

Independent and impartial administrations, in which officials are appointed and promoted on merit according to their ability, are of major importance in combating corruption and in implementing effective policies which benefit people.

Companies in different parts of the same Member State can face substantial differences in the time, number of procedures and costs needed to comply with regulations and to do business. Improving local and regional administrative capacity and making appropriate changes in the way public authorities are organised and managed can, therefore, give rise to significant gains in business efficiency.

The evidence suggests that the ‘right’ set of institutions can increase the rate of new business creation as well as the effect of cohesion policy support for enterprises.

References

Agerberg M., (2017), Failed expectations: Quality of government and support for populist parties in Europe. European Journal of Political Research 56:3, 578-600.

Annoni, P. & Dijkstra, L. (2016). EU regional competitiveness index (RCI 2013). Publications Office.

Arrowsmith, S. (2009). EC Regime on Public Procurement. In K. V Thai (Ed.), International handbook of public procurement (pp. 254–290). New York: CRC Press.

Becker, S., Egger, P., & von Ehrlich, M. (2010). Going NUTS: The effect of EU Structural Funds on regional performance, Journal of Public Economics, 94, 578-590.

BertelsmannStiftung, Sustaiable Governance Indicators 2016,

http://www.sgi-network.org/2016/

Cappelen, A., Castellacci, F., Fagerberg, J., & Verspagen, B. (2003). The impact of EU regional support on growth and convergence in the European Union. JCMS: Journal of Common Market Studies, 41(4), 621-644.

Charron, N., Dahlström, C., Fazekas, M., & Lapuente, V. (2017). Careers, Connections, and Corruption Risks: Investigating the impact of bureaucratic meritocracy on public procurement processes. Journal of Politics, 79(1), 89–103.

Charron, N., Dahlström, C., & Lapuente, V. (2016). Measuring Meritocracy in the Public Sector in Europe: a New National and Sub-National Indicator. European Journal of Criminal Policy and Research2, 22(3), 499–523.

Charron, N., Dahlström, C. & Lapuente, V. Eur J Crim Policy Res (2016)

Charron, N., Dijkstra, L., & Lapuente, V. (2014). Regional Governance Matters: Quality of Government within European Union Member States. Regional Studies, 48(1), 68–90.

Charron, N., Dijkstra, L., & Lapuente, V. (2015). Mapping the Regional Divide in Europe: A Measure for Assessing Quality of Government in 206 European Regions”. Social Indicators Research, 122(2), 315–346.

Charron, N., Lapuente, V. (2013). Why do some regions in Europe have a higher quality of government?. The Journal of Politics, 75(3), 567-582.

Charron, N., Lapuente V., & Rothstein, B. (2011). Measuring Quality of Government and Sub-national Variation, Report for the EU Commission of Regional Development European Commission Directorate-General Regional Policy Directorate Policy Development.

Charron, N., Lapuente, V., & Rothstein, B. (2013). Quality of Government and Corruption from a European Perspective: A Comparative Study of Good Government in EU Regions. Cheltenham: Elgar.

Cingolani, L., & Fazekas, M. (2017). The administrative capacities behind competitive public procurement processes: a comparative assessment of 32 European countries. Cambridge, UK.

Cingolani, L., Fazekas, M., Kukutschka, R. M. B., & Tóth, B. (2015). Towards a comprehensive mapping of information on public procurement tendering and its actors across Europe. Cambridge, UK.

Crescenzi, R., Di Cataldo, M., & Rodríguez-Pose, A. (2016). Government quality and the economic returns of transport infrastructure investment in European regions. Journal of Regional Science (forthcoming).

Crescenzi, R., & Rodríguez‐Pose, A. (2012). Infrastructure and regional growth in the European Union. Papers in Regional Science, 91(3), 487-513.

Crescenzi, R. & Rodríguez-Pose, A. (2012).

Infrastructure and regional growth in the European Union

,

Papers in Regional Science

, 91(3), 487-513.

Dahlström, C., Lapuente, V., & Teorell, J. (2012). The Merit of Meritocratization Politics, Bureaucracy, and the Institutional Deterrents of Corruption”. Political Research Quarterly, 65(3), 656–668.

Dahlström, C., Teorel J., Dahlberg S., Hartmann F., Lindberg A., and Nistotskaya M. (2015). The QoG Expert Survey Dataset II. University of Gothenburg: The Quality of Government Institute

Dahlström, C., Teorell, J., Dahlberg, S., Hartmann, F., Lindberg, A., & Nistotskaya, M. (2015). The QoG Expert Survey Dataset II. University of Gothenburg: The Quality of Government Institute.

Dellepiane-Avellaneda, S. (2010) 'Review Article: Good Governance, Institutions and Economic Development: Beyond the Conventional Wisdom', British Journal of Political Science, 40 195- 224.

European Commission. (2014). Investment for jobs and growth. Promoting development and good governance in EU regions and cities. Sixth report on economic, social and territorial cohesion. (L. Dijkstra, Ed.). Brussels: Publications Office of the European Union.

European Commission. (2016). Public Procurement Indicators 2014. Brussels.

European Commission, Standard Eurobarometer 83, Spring 2015.

European Commission (2016); European semseter thematic factshhets: quality of public administration;

https://ec.europa.eu/info/strategy/european-semester/thematic-factsheets/public-administration_en

European Commission (2017); Single market scoreboard, http://ec.europa.eu/internal_market/scoreboard/

European Commission, eGovernment Benchmark 2016 A turning point for eGovernment development in Europe? (Insight report, background report and data set available at https://ec.europa.eu/digital-single-market/en/news/eu-egovernment-report-2016-shows-online-public-services-improved-unevenly)

Evans, P., & Rauch, J. (1999). Bureaucracy and Growth: A Cross-National Analysis of the Effects of ‘Weberian’ State Structures on Economic Growth. American Sociological Review, 64(5), 748–65.

Fazekas M., (2017); Assessing the quality of government at the regional elvel usijng the public procurement data (upcoming)

Fazekas, M. (2016). Options for benchmarking contracting authority performance using readily available databases. Brussels.

Fazekas, M., Cingolani, L., & Tóth, B. (2016). A comprehensive review of objective corruption proxies in public procurement: risky actors, transactions, and vehicles of rent extraction (Government Transparency Institute Working Paper Series No. GTI-WP/2016:03). Budapest.

Fazekas, M., & Kocsis, G. (2017). Uncovering High-Level Corruption: Cross-National Objective Corruption Risk Indicators Using Public Procurement Data. British Journal of Political Science, 1-10. doi:10.1017/S0007123417000461

Fazekas, M., Tóth, I. J., & King, L. P. (2016). An Objective Corruption Risk Index Using Public Procurement Data. European Journal of Criminal Policy and Research, 22(3), 369–397.

Halleröd, B., Rothstein, B., Adel, D. & Nandy, S. (2013) 'Bad Governance and Poor Children: A Comparative Analysis of Government Efficiency and Severe Child Deprivation in 68 Low- and Middle-Income Countries', World Development, 48 19-31.

Habib, M., ZurawickiI L. (2002), “Corruption and Foreign Direct Investment”, Journal of International Business Studies 33 (2).

Halkos, G. E., Sundström, A., & Tzeremes, N. G. (2015). Regional environmental performance and governance quality: a nonparametric analysis. Environmental Economics and Policy Studies, 17(4), 621-644.

Henderson, J., Hulme, D., Jalilian, H., & Phillips, R. (2007). Bureaucratic Effects: ‘Weberian’ State Agenciesand Poverty Reduction”. Sociology, 41(3), 515–532.

Holmberg, S. & Rothstein, B. (eds.) (2012) Good Government: The Relevance of Political Science, Cheltenham: Edward Elgar Publishing.

Kaufmann, D., Kraay, A., & Mastruzzi, M. (2009). Governance Matters VIII: Aggregate and Individual Governance Indicators, 1996-2008, World Bank Policy Research Working Paper No. 4978.

Kaufmann, D., Kraay A. (2002), Growth Without Governance, The World Bank.

Kaufmann, D., Kraay A, Zoido-Lobatón, (1999), Aggregating Governance Indicators, Policy Research Paper 2195, The World Bank

Kinoshita, Y., Campos N. (2003), “Why Does FDI Go Where it Goes ? New Evidence from the Transition Economies, IMF, WP/03/228

Kovacic, W. E., Marshall, R. C., Marx, L. M., & Raiff, M. E. (2006). Bidding rings and the design of anti-collusive measures for auctions and procurements. In N. Dimitri, G. Piga, & G. Spagnolo (Eds.), Handbook of Procurement (pp. 381–411). Cambridge, UK: Cambridge University Press.

Levchenko, A. (2004), “Institutional Quality and International Trade”, IMF Working Paper, 04/231.

Lewis-Faupel, S., Neggers, Y., Olken, B. A., & Pande, R. (2016). Can Electronic Procurement Improve Infrastructure Provision? Evidence from Public Works in India and Indonesia. American Economic Journal: Economic Policy, 8(3), 258–283.

Lucas, R. E. (1988). On the mechanics of economic development. Journal of Monetary Economics, 22(1), 3-42.

Mungiu-Pippidi, A. (2015). The Quest for Good Governance. How Societies Develop Control of Corruption. Cambridge, UK: Cambridge University Press.

Nistotskaya, M., Charron, N., & Lapuente, V. (2015) The wealth of regions: quality of government and SMEs in 172 European regions. Environment and Planning C: Government and Policy, 33(5): 1125-1155.

North, D. C. (1990) Institutions, Institutional Change and Economic Performance, Cambridge, Cambridge University Press.

North, D. C., Wallis, J. J., & Weingast, B. R. (2009). Violence and Social Orders. A Conceptual Framework for Interpreting Recorded Human History. Cambridge, UK: Cambridge University Press.

Mankiw, N., Romer, P., & Weil, D. (1992). A contribution to the empirics of economic growth. Quarterly Journal of Economics 107, 407–437.

OECD. (2007). Integrity in Public Procurement. Good Practice from A to Z. Paris: OECD.

OECD (2013a), Investing Together: Working Effectively across Levels of Government, OECD Publishing, Paris.

http://dx.doi.org/10.1787/9789264197022-en

OECD (2013b), Issue paper on Corruption and economic growth, http://www.oecd.org/g20/topics/anti-corruption/Issue-Paper-Corruption-and-Economic-Growth.pdf

OECD. (2015). Government at a glance. 2015. Paris: OECD.

OECD/Sigma. (2014). The Principles of Public Administration. Paris: OECD/Sigma.

GOVERNING THE COMMONS

Ostrom, E. (1990) Governing the Commons: The Evolution of Institutions for Collective Action, New York, Cambridge University Press.

Pellegrini, G., Terribile, F., Tarola, O., Muccigrosso, T., & Busillo, F. (2013). Measuring the effects of European Regional Policy on economic growth: A regression discontinuity approach. Papers in Regional Science, 92(1), 217-233.

Persson, A., Rothstein, B., & Teorell, J. (2013). Why anticorruption reforms fail—systemic corruption as a collective action problem. Governance, 26(3), 449-471.

Peters, B. G., & Pierre, J. (Eds.). (2001). Politicians, bureaucrats and administrative reform. London: Routledge.

Peters, B. G., & Pierre, J. (Eds.). (2004). Politicization of the Civil Service in Comparative Perspective. London: Routledge.r

Diaz Ramirez, M., Kleine-Rueschkamp, L., Veneri, P. (2017), “Does quality of governance affect the returns of policy for entrepreneurship?”, Paper presented at the 57th Congress of the European Regional Science Association, Groningen 29 August – 1 September 2017.

Rauch, J., & Evans, P. (2000). Bureaucratic structure and bureaucratic performance in less developed countries. Journal of Public Economics, 75(1), 49–71.

Rodríguez-Pose, A. (2013). Do institutions matter for regional development? Regional Studies, 47(7), 1034-1047.

Rodríguez-Pose, A. and Di Cataldo, M. (2015) Quality of government and innovative performance in the regions of Europe. Journal of Economic Geography 15, 4, 673-706.

Rodríguez-Pose, A., & Garcilazo, E. (2015). Quality of government and the returns of investment: Examining the impact of cohesion expenditure in European regions. Regional Studies, 49(8), 1274-1290.

Rodríguez-Pose A. and Ketterer T. (2016), Institutional change and the development of lagging regions in Europe (a study for DG for Regional Policy).

Romer, P.M. (1986). Increasing returns and long-run growth, Journal of Political Economy, 94(5), 1002-37.

Rose-Ackerman, S. (1978). Corruption: a study in political economy. New York: Academic Press.

Rothstein, B., & Teorell, J. (2008). What Is Quality of Government? A Theory of Impartial Government Institutions. Governance, 21(2), 165–190.

Rothstein, B. (2011). The Quality of Government: Corruption, Social Trust and Inequality in International Perspective. Chicago: University of Chicago Press.

Rothstein, B., & Teorell, J. (2012). Defining and measuring quality of government. In S. Holmberg & B. Rothstein (Eds.). Good Government: The Relevance Of Political Science. Cheltenham: Edward Elgar.

Solow, R. (1956) A contribution to the theory of economic growth. Quarterly Journal of Economics, 70(1), 65-94.

Soreide, T. (2002). Corruption in public procurement. Causes, consequences and cures. Bergen, Norway.

Sundström, A. (2013). Women’s local political representation within 30 European countries. University of Gothenburg, QoG Working Paper Series, 2013:18.

Sundström, A., & Wängnerud, L. (2014). Corruption as an obstacle to women’s political representation Evidence from local councils in 18 European countries. Party Politics, 1354068814549339.

Swan, T. (1956). Economic growth and capital accumulation. Economic Record, 32, 334-361.

Svallfors, S. (2013) 'Government Quality, Egalitarianism, and Attitudes to Taxes and Social Spending: A European Comparison', European Political Science Review, 5 (3): 363-380.

Tavits, M. (2008) 'Representation, Corruption, and Subjective Well-Being', Comparative Political Studies, 41 (12): 1607-1630.

Teorell, J, Charron, N,. Dahlberg, S,. Holmberg, S,. Rothstein, B,. Sundin, P. & Svensson. R. (2013). The Quality of Government Dataset, version 15May13. University of Gothenburg: The Quality of Government Institute,

http://www.qog.pol.gu.se

.

Teorell, J., Dahlström, C., & Dahlberg,.S. (2011). The QoG Expert Survey Dataset. University of Gothenburg: The Quality of Government Institute

Transparency International, Corruption Perception Index 2016; https://www.transparency.org/news/feature/corruption_perceptions_index_2016

Uslaner, E. M. (2008) 'The Foundations of Trust: Macro and Micro', Cambridge Journal of Economics, 32 (2): 289-294.

Varga, J., in 't Veld, J. (2014), ‘The potential growth impact of structural reforms in the EU. A benchmarking exercise’ European Economy. Economic Papers 541.

Wash, J.P., Yu, J. (2010), ‘Determinants of Foreign Direct Investment: A Sectoral and Institutional Approach’, IMF Working Paper.

World Bank (2016), Doing Business reports - Measuring Regulatory Quality and Efficiency

World Bank (2017), Doing Business in the European Union 2017: Bulgaria, Hungary and Romania; http://www.doingbusiness.org/reports/subnational-reports/eu-bulgaria-hungary-romania

World Bank (2015), Doing Business in Poland 2015; http://www.doingbusiness.org/Reports/Subnational-Reports/poland

World Bank (2015), Doing Business in Spain 2015; http://www.doingbusiness.org/Reports/Subnational-Reports/spain

World Bank, Worldwide Governance Indicators, http://data.worldbank.org/data-catalog/worldwide-governance-indicators

World Bank. (2009). Fraud and Corruption. Awareness Handbook. Washington DC: World Bank.

World Economic Forum, The Global Competitiveness Report 2016–2017, https://www.weforum.org/reports/the-global-competitiveness-report-2016-2017-1