ISSN 1977-0677

Official Journal

of the European Union

L 347

English edition

Legislation

Volume 60

28 December 2017

|

ISSN 1977-0677 |

||

|

Official Journal of the European Union |

L 347 |

|

|

|

||

|

English edition |

Legislation |

Volume 60 |

|

Contents |

|

I Legislative acts |

page |

|

|

|

REGULATIONS |

|

|

|

* |

||

|

|

* |

||

|

|

* |

|

EN |

Acts whose titles are printed in light type are those relating to day-to-day management of agricultural matters, and are generally valid for a limited period. The titles of all other Acts are printed in bold type and preceded by an asterisk. |

I Legislative acts

REGULATIONS

|

28.12.2017 |

EN |

Official Journal of the European Union |

L 347/1 |

REGULATION (EU) 2017/2401 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL

of 12 December 2017

amending Regulation (EU) No 575/2013 on prudential requirements for credit institutions and investment firms

THE EUROPEAN PARLIAMENT AND THE COUNCIL OF THE EUROPEAN UNION,

Having regard to the Treaty on the Functioning of the European Union, and in particular Article 114 thereof,

Having regard to the proposal from the European Commission,

After transmission of the draft legislative act to the national parliaments,

Having regard to the opinion of the European Central Bank (1),

Having regard to the opinion of the European Economic and Social Committee (2),

Acting in accordance with the ordinary legislative procedure (3),

Whereas:

|

(1) |

Securitisations are an important constituent part of well-functioning financial markets insofar as they contribute to diversifying the funding and risk diversification sources of credit institutions and investment firms (‘institutions’) and releasing regulatory capital which can then be reallocated to support further lending, in particular the funding of the real economy. Furthermore, securitisations provide institutions and other market participants with additional investment opportunities, thus allowing portfolio diversification and facilitating the flow of funding to businesses and individuals both within Member States and on a cross-border basis throughout the Union. Those benefits should however be weighed against their potential costs and risks, including their impact on financial stability. As seen during the first phase of the financial crisis starting in the summer of 2007, unsound practices in securitisation markets resulted in significant threats to the integrity of the financial system, namely due to excessive leverage, opaque and complex structures that made pricing problematic, mechanistic reliance on external ratings or misalignment between the interests of investors and originators (‘agency risks’). |

|

(2) |

In recent years, securitisation issuance volumes in the Union have remained below their pre-crisis peak for a number of reasons, including the stigma generally associated with such transactions. In order to prevent a recurrence of the circumstances that triggered the financial crisis, the recovery of securitisation markets should be based on sound and prudent market practices. To that end, Regulation (EU) 2017/2402 of the European Parliament and of the Council (4) lays down the substantive elements of an overarching securitisation framework, with criteria to identify simple, transparent and standardised (‘STS’) securitisations and a system of supervision to monitor the correct application of those criteria by originators, sponsors, issuers and institutional investors. Furthermore, that Regulation provides for a set of common requirements on risk retention, due diligence and disclosure for all financial services sectors. |

|

(3) |

In accordance with the objectives of Regulation (EU) 2017/2402, the regulatory capital requirements laid down in Regulation (EU) No 575/2013 of the European Parliament and of the Council (5) for institutions originating, sponsoring or investing in securitisations should be amended to adequately reflect the specific features of STS securitisations when such securitisations also meet the additional requirements laid down in this Regulation, and to address the shortcomings which became apparent during the financial crisis, namely mechanistic reliance on external ratings, excessively low risk weights for highly-rated securitisation tranches and, conversely, excessively high risk weights for low-rated tranches, and insufficient risk sensitivity. On 11 December 2014 the Basel Committee on Banking Supervision (the ‘BCBS’) published its ‘Revisions to the securitisation framework’ (the ‘Revised Basel Framework’) setting out various changes to the regulatory capital standards for securitisations to address specifically those shortcomings. On 11 July 2016, the BCBS published an updated standard for the regulatory capital treatment of securitisation exposures that includes the regulatory capital treatment for ‘simple, transparent and comparable’ securitisations. That standard amends the Revised Basel Framework. The amendments to Regulation (EU) No 575/2013 should take into account the provisions of the Revised Basel Framework as amended. |

|

(4) |

Capital requirements for positions in a securitisation under Regulation (EU) No 575/2013 should be subject to the same calculation methods for all institutions. In the first instance and to remove any form of mechanistic reliance on external ratings, an institution should use its own calculation of regulatory capital requirements where the institution has permission to apply the Internal Ratings Based Approach (the ‘IRB Approach’) in relation to exposures of the same type as those underlying the securitisation and is able to calculate regulatory capital requirements in relation to the underlying exposures as if these had not been securitised (‘KIRB’), in each case subject to certain pre-defined inputs (the Securitisation IRB Approach — ‘SEC-IRBA’). A Securitisation Standardised Approach (SEC-SA) should then be available to institutions that are not able to use the SEC-IRBA in relation to their positions in a given securitisation. The SEC-SA should rely on a formula using as an input the capital requirements that would be calculated under the Standardised Approach to credit risk in relation to the underlying exposures as if they had not been securitised (‘KSA’). When the first two approaches are not available, institutions should be able to apply the Securitisation External Ratings Based Approach (SEC-ERBA). Under the SEC-ERBA, capital requirements should be assigned to securitisation tranches on the basis of their external rating. However, institutions should always use the SEC-ERBA as a fallback when the SEC-IRBA is not available for low-rated tranches and certain medium-rated tranches of STS securitisations identified through appropriate parameters. For non-STS securitisations, the use of the SEC-SA after the SEC-IRBA should be further restricted. Moreover, competent authorities should be able to prohibit the use of the SEC-SA when the latter is not able to adequately tackle the risks that the securitisation poses to the solvability of the institution or to financial stability. Upon notification to the competent authority, institutions should be allowed to use the SEC-ERBA in respect of all rated securitisations they hold when they cannot use the SEC-IRBA. |

|

(5) |

Agency and model risks are more prevalent for securitisations than for other financial assets and give rise to some degree of uncertainty in the calculation of capital requirements for securitisations even after all appropriate risk drivers have been taken into account. In order to capture those risks adequately, Regulation (EU) No 575/2013 should be amended to provide for a minimum 15 % risk-weight floor for all securitisation positions. Resecuritisations, however, exhibit greater complexity and riskiness and, accordingly, only certain forms of resecuritisations are permitted under Regulation (EU) 2017/2402. In addition, positions in resecuritisations should be subject to a more conservative regulatory capital calculation and a 100 % risk-weight floor. |

|

(6) |

An institution should not be required to apply a higher risk weight to a senior position than that which would apply if it held the underlying exposures directly, thus reflecting the benefit of credit enhancement that senior positions receive from junior tranches in the securitisation structure. Regulation (EU) No 575/2013 should therefore provide for a ‘look-through’ approach according to which a senior securitisation position should be assigned a maximum risk weight equal to the exposure-weighted-average risk weight applicable to the underlying exposures, and such approach should be available irrespective of whether the relevant position is rated or unrated and the approach used for the underlying pool (Standardised Approach or IRB Approach), subject to certain conditions. |

|

(7) |

An overall cap in terms of maximum risk-weighted exposure amounts is available under the current framework for institutions that can calculate the capital requirements for the underlying exposures in accordance with the IRB Approach as if those exposures had not been securitised (KIRB). Insofar as the securitisation process reduces the risk attached to the underlying exposures, this cap should be available to all originator and sponsor institutions, regardless of the approach they use for the calculation of regulatory capital requirements for the positions in the securitisation. |

|

(8) |

As pointed out by the European Supervisory Authority (European Banking Authority) (‘EBA’), established by Regulation (EU) No 1093/2010 of the European Parliament and of the Council (6), in its report on qualifying securitisation of July 2015, empirical evidence on defaults and losses shows that STS securitisations exhibited better performance than other securitisations during the financial crisis, reflecting the use of simple and transparent structures and robust execution practices in STS securitisation which deliver lower credit, operational and agency risks. It is therefore appropriate to amend Regulation (EU) No 575/2013 to provide for an appropriately risk-sensitive calibration for STS securitisations, provided that they also meet additional requirements to minimise risk, in the manner recommended by the EBA in that report which involves, in particular, a lower risk-weight floor of 10 % for senior positions. |

|

(9) |

Lower capital requirements applicable to STS securitisations should be limited to securitisations where the ownership of the underlying exposures is transferred to a securitisation special purpose entity or SSPE (‘traditional securitisations’). However, institutions retaining senior positions in synthetic securitisations backed by an underlying pool of loans to small and medium-size enterprises (‘SMEs’) should also be allowed to apply to these positions the lower capital requirements available for STS securitisations where such transactions are regarded as of high quality in accordance with certain strict criteria, including on the eligible investors. In particular, such subset of synthetic securitisations should benefit from the guarantee or counterguarantee either by the central government or central bank of a Member State or a promotional entity, or by an institutional investor provided that the guarantee or counterguarantee provided by the latter is fully collateralised by cash on deposit with the originator institutions. The preferential regulatory capital treatment for STS securitisations that would be available to those transactions under Regulation (EU) No 575/2013 is without prejudice to compliance with the Union State aid framework, as set out in Directive 2014/59/EU of the European Parliament and of the Council (7). |

|

(10) |

In order to harmonise supervisory practices throughout the Union, the power to adopt acts in accordance with Article 290 of the Treaty on the Functioning of the European Union (TFEU) should be delegated to the Commission, having taken account of the report by the EBA, in respect of further specifying the conditions for the transfer of credit risk to third parties, the notion of commensurate transfer of credit risk to third parties and the requirements for competent authorities assessment of transfer of credit risk, both with regard to traditional and synthetic securitisations. It is of particular importance that the Commission carry out appropriate consultations during its preparatory work, including at expert level, and that those consultations be conducted in accordance with the principles laid down in the Interinstitutional Agreement of 13 April 2016 on Better Law-Making (8). In particular, to ensure equal participation in the preparation of delegated acts, the European Parliament and the Council receive all documents at the same time as Member States’ experts, and their experts systematically have access to meetings of Commission expert groups dealing with the preparation of delegated acts. |

|

(11) |

Technical standards in financial services should ensure adequate protection of investors and consumers across the Union. As a body with highly specialised expertise, it would be efficient and appropriate to entrust the EBA with the elaboration of draft regulatory technical standards which do not involve policy choices, for submission to the Commission. |

|

(12) |

The Commission should be empowered to adopt regulatory technical standards developed by the EBA, with regard to what constitutes an appropriately conservative method for measuring the amount of the undrawn portion of the cash advance facilities in the context of calculating the exposure value of a securitisation and with regard to further specifying the conditions to allow institutions to calculate KIRB for the pool of underlying exposures of a securitisation like in the case of purchased receivables. The Commission should adopt those draft regulatory technical standards by means of delegated acts pursuant to Article 290 TFEU and in accordance with Articles 10 to 14 of Regulation (EU) No 1093/2010. |

|

(13) |

Only consequential changes should be made to the remaining regulatory capital requirements for securitisations laid down in Regulation (EU) No 575/2013 insofar as necessary to reflect the new hierarchy of approaches and the specific provisions for STS securitisations. In particular, the provisions related to the recognition of significant risk transfer and the requirements on external credit assessments should continue to apply in broadly the same terms as they do currently. However, Part Five of Regulation (EU) No 575/2013 should be deleted in its entirety with the exception of the requirement to hold additional risk weights which should be imposed on institutions found in breach of the provisions in Chapter 2 of Regulation (EU) 2017/2402. |

|

(14) |

It is appropriate for the amendments to Regulation (EU) No 575/2013 provided for in this Regulation to apply to all securitisation positions held by an institution. However, in order to mitigate transitional costs insofar as possible and to allow for a smooth migration to the new framework, institutions should continue to apply, until 31 December 2019, the previous framework, namely the relevant provisions of Regulation (EU) No 575/2013 that applied prior to the date of application of this Regulation, to all outstanding securitisation positions that they hold on the date of application of this Regulation, |

HAVE ADOPTED THIS REGULATION:

Article 1

Amendment of Regulation (EU) No 575/2013

Regulation (EU) No 575/2013 is amended as follows:

|

(1) |

Article 4(1) is amended as follows:

|

|

(2) |

In point (k) of Article 36(1), point (ii) is replaced by the following:

|

|

(3) |

Article 109 is replaced by the following: ‘Article 109 Treatment of securitisation positions Institutions shall calculate the risk-weighted exposure amount for a position they hold in a securitisation in accordance with Chapter 5.’. |

|

(4) |

In Article 134, paragraph 6 is replaced by the following: ‘6. Where an institution provides credit protection for a number of exposures subject to the condition that the nth default among the exposures shall trigger payment and that this credit event shall terminate the contract, the risk weights of the exposures included in the basket will be aggregated, excluding n-1 exposures, up to a maximum of 1 250 % and multiplied by the nominal amount of the protection provided by the credit derivative to obtain the risk-weighted exposure amount. The n-1 exposures to be excluded from the aggregation shall be determined on the basis that they shall include those exposures each of which produces a lower risk-weighted exposure amount than the risk-weighted exposure amount of any of the exposures included in the aggregation.’. |

|

(5) |

In Article 142(1), point (8) is deleted. |

|

(6) |

In Article 153, paragraphs 7 and 8 are replaced by the following: ‘7. For purchased corporate receivables, refundable purchase price discounts, collaterals or partial guarantees that provide first loss protection for default losses, dilution losses, or both, may be treated as a first loss protection by the purchaser of the receivables or by the beneficiary of the collateral or of the partial guarantee in accordance with Subsections 2 and 3 of Section 3 of Chapter 5. The seller providing the refundable purchase price discount and the provider of a collateral or a partial guarantee shall treat those as an exposure to a first loss position in accordance with Subsections 2 and 3 of Section 3 of Chapter 5. 8. Where an institution provides credit protection for a number of exposures subject to the condition that the nth default among the exposures shall trigger payment and that this credit event shall terminate the contract, the risk weights of the exposures included in the basket will be aggregated, excluding n-1 exposures, where the sum of the expected loss amount multiplied by 12,5 and the risk-weighted exposure amount shall not exceed the nominal amount of the protection provided by the credit derivative multiplied by 12,5. The n-1 exposures to be excluded from the aggregation shall be determined on the basis that they shall include those exposures each of which produces a lower risk-weighted exposure amount than the risk-weighted exposure amount of any of the exposures included in the aggregation. A 1 250 % risk weight shall apply to positions in a basket for which an institution cannot determine the risk-weight under the IRB Approach.’. |

|

(7) |

In Article 154, paragraph 6 is replaced by the following: ‘6. For purchased retail receivables, refundable purchase price discounts, collaterals or partial guarantees that provide first loss protection for default losses, dilution losses, or both, may be treated as a first loss protection by the purchaser of the receivables or by the beneficiary of the collateral or of the partial guarantee in accordance with Subsections 2 and 3 of Section 3 of Chapter 5. The seller providing the refundable purchase price discount and the provider of a collateral or a partial guarantee shall treat those as an exposure to a first loss position in accordance with Subsections 2 and 3 of Section 3 of Chapter 5.’. |

|

(8) |

In Article 197(1), point (h) is replaced by the following:

|

|

(9) |

Chapter 5 of Title II, Part Three is replaced by the following: ‘CHAPTER 5 Securitisation

Article 242 Definitions For the purposes of this Chapter, the following definitions apply:

Article 243 Criteria for STS securitisations qualifying for differentiated capital treatment 1. Positions in an ABCP programme or ABCP transaction that qualify as positions in an STS securitisation shall be eligible for the treatment set out in Articles 260, 262 and 264 where the following requirements are met:

In the case of trade receivables, point (b) of the first subparagraph shall not apply where the credit risk of those trade receivables is fully covered by eligible credit protection in accordance with Chapter 4, provided that in that case the protection provider is an institution, an insurance undertaking or a reinsurance undertaking. For the purposes of this subparagraph, only the portion of the trade receivables remaining after taking into account the effect of any purchase price discount and overcollateralisation shall be used to determine whether they are fully covered and whether the concentration limit is met. In the case of securitised residual leasing values, point (b) of the first subparagraph shall not apply where those values are not exposed to refinancing or resell risk due to a legally enforceable commitment to repurchase or refinance the exposure at a pre-determined amount by a third party eligible under Article 201(1). By way of derogation from point (a) of the first subparagraph, where an institution applies Article 248(3) or has been granted permission to apply the Internal Assessment Approach in accordance with Article 265, the risk weight that institution would assign to a liquidity facility that completely covers the ABCP issued under the programme is equal to or smaller than 100 %. 2. Positions in a securitisation, other than an ABCP programme or ABCP transaction, that qualify as positions in an STS securitisation, shall be eligible for the treatment set out in Articles 260, 262 and 264 where the following requirements are met:

Article 244 Traditional securitisation 1. The originator institution of a traditional securitisation may exclude underlying exposures from its calculation of risk-weighted exposure amounts and, where relevant, expected loss amounts if either of the following conditions is fulfilled:

2. Significant credit risk shall be considered as transferred in either of the following cases:

Where the possible reduction in risk-weighted exposure amounts, which the originator institution would achieve by the securitisation under points (a) or (b), is not justified by a commensurate transfer of credit risk to third parties, competent authorities may decide on a case-by-case basis that significant credit risk shall not be considered as transferred to third parties. 3. By way of derogation from paragraph 2, competent authorities may allow originator institutions to recognise significant credit risk transfer in relation to a securitisation where the originator institution demonstrates in each case that the reduction in own funds requirements which the originator achieves by the securitisation is justified by a commensurate transfer of credit risk to third parties. Permission may only be granted where the institution meets both of the following conditions:

4. In addition to the requirements set out in paragraphs 1, 2 and 3, all of the following conditions shall be met:

5. The competent authorities shall inform the EBA of those cases where they have decided that the possible reduction in risk-weighted exposure amounts was not justified by a commensurate transfer of credit risk to third parties in accordance with paragraph 2, and the cases where institutions have chosen to apply paragraph 3. 6. The EBA shall monitor the range of supervisory practices in relation to the recognition of significant risk transfer in traditional securitisations in accordance with this Article. In particular, the EBA shall review:

The EBA shall report its findings to the Commission by 2 January 2021. The Commission may, having taken into account the report from the EBA, adopt a delegated act in accordance with Article 462, to supplement this Regulation by further specifying the items listed in points (a), (b) and (c) of this paragraph. Article 245 Synthetic securitisation 1. The originator institution of a synthetic securitisation may calculate risk-weighted exposure amounts, and, where relevant, expected loss amounts with respect to the underlying exposures in accordance with Articles 251 and 252, where either of the following conditions is met:

2. Significant credit risk shall be considered as transferred in either of the following cases:

Where the possible reduction in risk-weighted exposure amounts, which the originator institution would achieve by the securitisation, is not justified by a commensurate transfer of credit risk to third parties, competent authorities may decide on a case-by-case basis that significant credit risk shall not be considered as transferred to third parties. 3. By way of derogation from paragraph 2, competent authorities may allow originator institutions to recognise significant credit risk transfer in relation to a securitisation where the originator institution demonstrates in each case that the reduction in own funds requirements which the originator achieves by the securitisation is justified by a commensurate transfer of credit risk to third parties. Permission may only be granted where the institution meets both of the following conditions:

4. In addition to the requirements set out in paragraphs 1, 2 and 3, all of the following conditions shall be met:

5. The competent authorities shall inform the EBA of the cases where they have decided that the possible reduction in risk-weighted exposure amounts was not justified by a commensurate transfer of credit risk to third parties in accordance with paragraph 2, and the cases where institutions have chosen to apply paragraph 3. 6. The EBA shall monitor the range of supervisory practices in relation to the recognition of significant risk transfer in synthetic securitisations in accordance with this Article. In particular, the EBA shall review:

The EBA shall report its findings to the Commission by 2 January 2021. The Commission may, having taken into account the report from the EBA, adopt a delegated act in accordance with Article 462, to supplement this Regulation by further specifying the items listed in points (a), (b) and (c) of this paragraph. Article 246 Operational requirements for early amortisation provisions Where the securitisation includes revolving exposures and early amortisation provisions or similar provisions, significant credit risk shall only be considered transferred by the originator institution where the requirements laid down in Articles 244 and 245 are met and the early amortisation provision, once triggered, does not:

Article 247 Calculation of risk-weighted exposure amounts 1. Where an originator institution has transferred significant credit risk associated with the underlying exposures of the securitisation in accordance with Section 2, that institution may:

2. Where the originator institution has decided to apply paragraph 1, it shall calculate the risk-weighted exposure amounts as set out in this Chapter for the positions that it may hold in the securitisation. Where the originator institution has not transferred significant credit risk or has decided not to apply paragraph 1, it shall not be required to calculate risk-weighted exposure amounts for any position it may have in the securitisation but shall continue including the underlying exposures in its calculation of risk-weighted exposure amounts and, where relevant, expected loss amounts as if they had not been securitised. 3. Where there is an exposure to positions in different tranches in a securitisation, the exposure to each tranche shall be considered a separate securitisation position. The providers of credit protection to securitisation positions shall be considered as holding positions in the securitisation. Securitisation positions shall include exposures to a securitisation arising from interest rate or currency derivative contracts that the institution has entered into with the transaction. 4. Unless a securitisation position is deducted from Common Equity Tier 1 items pursuant to point (k) of Article 36(1), the risk-weighted exposure amount shall be included in the institution’s total of risk-weighted exposure amounts for the purposes of Article 92(3). 5. The risk-weighted exposure amount of a securitisation position shall be calculated by multiplying the exposure value of the position, calculated as set out in Article 248, by the relevant total risk weight. 6. The total risk weight shall be determined as the sum of the risk weight set out in this Chapter and any additional risk weight in accordance with Article 270a. Article 248 Exposure value 1. The exposure value of a securitisation position shall be calculated as follows:

The EBA shall develop draft regulatory technical standards to specify what constitutes an appropriately conservative method for measuring the amount of the undrawn portion referred to in point (b) of the first subparagraph. The EBA shall submit those draft regulatory technical standards to the Commission by 18 January 2019. Power is delegated to the Commission to supplement this Regulation by adopting the regulatory technical standards referred to in the third subparagraph of this paragraph in accordance with Articles 10 to 14 of Regulation (EU) No 1093/2010. 2. Where an institution has two or more overlapping positions in a securitisation, it shall include only one of the positions in its calculation of risk-weighted exposure amounts. Where the positions partially overlap, the institution may split the position into two parts and recognise the overlap in relation to one part only in accordance with the first subparagraph. Alternatively, the institution may treat the positions as if they were fully overlapping by expanding for capital calculation purposes the position that produces the higher risk-weighted exposure amounts. The institution may also recognise an overlap between the specific risk own funds requirements for positions in the trading book and the own funds requirements for securitisation positions in the non-trading book, provided that the institution is able to calculate and compare the own funds requirements for the relevant positions. For the purposes of this paragraph, two positions shall be deemed to be overlapping where they are mutually offsetting in such a manner that the institution is able to preclude the losses arising from one position by performing the obligations required under the other position. 3. Where point (d) of Article 270c applies to positions in an ABCP, the institution may use the risk weight assigned to a liquidity facility in order to calculate the risk-weighted exposure amount for the ABCP, provided that the liquidity facility covers 100 % of the ABCP issued by the ABCP programme and the liquidity facility ranks pari passu with the ABCP in a manner that they form an overlapping position. The institution shall notify the competent authorities where it has applied the provisions laid down in this paragraph. For the purposes of determining the 100 % coverage set out in this paragraph, the institution may take into account other liquidity facilities in the ABCP programme, provided that they form an overlapping position with the ABCP. Article 249 Recognition of credit risk mitigation for securitisation positions 1. An institution may recognise funded or unfunded credit protection with respect to a securitisation position where the requirements for credit risk mitigation laid down in this Chapter and in Chapter 4 are met. 2. Eligible funded credit protection shall be limited to financial collateral which is eligible for the calculation of risk-weighted exposure amounts under Chapter 2 as laid down under Chapter 4 and recognition of credit risk mitigation shall be subject to compliance with the relevant requirements as laid down under Chapter 4. Eligible unfunded credit protection and unfunded credit protection providers shall be limited to those which are eligible in accordance with Chapter 4 and recognition of credit risk mitigation shall be subject to compliance with the relevant requirements as laid down under Chapter 4. 3. By way of derogation from paragraph 2, the eligible providers of unfunded credit protection listed in points (a) to (h) of Article 201(1) shall have been assigned a credit assessment by a recognised ECAI which is credit quality step 2 or above at the time the credit protection was first recognised and credit quality step 3 or above thereafter. The requirement set out in this subparagraph shall not apply to qualifying central counterparties. Institutions which are allowed to apply the IRB Approach to a direct exposure to the protection provider may assess eligibility in accordance with the first subparagraph based on the equivalence of the PD for the protection provider to the PD associated with the credit quality steps referred to in Article 136. 4. By way of derogation from paragraph 2, SSPEs shall be eligible protection providers where all of the following conditions are met:

5. For the purposes of paragraph 4, the amount of the protection adjusted for any currency and maturity mismatches (Ga) in accordance with Chapter 4 shall be limited to the volatility adjusted market value of those assets and the risk weight of exposures to the protection provider as specified under the Standardised Approach (g) shall be determined as the weighted-average risk weight that would apply to those assets as financial collateral under the Standardised Approach. 6. Where a securitisation position benefits from full credit protection or a partial credit protection on a pro-rata basis, the following requirements shall apply:

7. In all cases not covered by paragraph 6, the following requirements shall apply:

8. Institutions using the Securitisation Internal Ratings Based Approach (SEC-IRBA) or the Securitisation Standardised Approach (SEC-SA) under Subsection 3 shall determine the attachment point (A) and detachment point (D) separately for each of the positions derived in accordance with paragraph 7 as if these had been issued as separate securitisation positions at the time of origination of the transaction. The value of KIRB or KSA, respectively, shall be calculated taking into account the original pool of exposures underlying the securitisation. 9. Institutions using the Securitisation External Ratings Based Approach (SEC-ERBA) under Subsection 3 for the original securitisation position shall calculate risk-weighted exposure amounts for the positions derived in accordance with paragraph 7 as follows:

10. The derived position with the lower seniority shall be treated as a non-senior securitisation position even if the original securitisation position prior to protection qualifies as senior. Article 250 Implicit support 1. A sponsor institution, or an originator institution which in respect of a securitisation has made use of Article 247(1) and (2) in the calculation of risk-weighted exposure amounts or has sold instruments from its trading book to the effect that it is no longer required to hold own funds for the risks of those instruments shall not provide support, directly or indirectly, to the securitisation beyond its contractual obligations with a view to reducing potential or actual losses to investors. 2. A transaction shall not be considered as support for the purposes of paragraph 1 where the transaction has been duly taken into account in the assessment of significant credit risk transfer and both parties have executed the transaction acting in their own interest as free and independent parties (arm’s length). For these purposes, the institution shall undertake a full credit review of the transaction and, at a minimum, take into account all of the following items:

3. The originator institution and the sponsor institution shall notify the competent authority of any transaction entered into in relation to the securitisation in accordance with paragraph 2. 4. The EBA shall, in accordance with Article 16 of Regulation (EU) No 1093/2010, issue guidelines on what constitutes “arm’s length” for the purposes of this Article and the circumstances under which a transaction is not structured to provide support. 5. If an originator institution or a sponsor institution fails to comply with paragraph 1 in respect of a securitisation, the institution shall include all of the underlying exposures of that securitisation in its calculation of risk-weighted exposure amounts as if they had not been securitised and disclose:

Article 251 Originator institutions’ calculation of risk-weighted exposure amounts securitised in a synthetic securitisation 1. For the purpose of calculating risk-weighted exposure amounts for the underlying exposures, the originator institution of a synthetic securitisation shall use the calculation methodologies set out in this Section where applicable instead of those set out in Chapter 2. For institutions calculating risk-weighted exposure amounts and, where relevant, expected loss amounts with respect to the underlying exposures under Chapter 3, the expected loss amount in respect of such exposures shall be zero. 2. The requirements set out in paragraph 1 of this Article shall apply to the entire pool of exposures backing the securitisation. Subject to Article 252, the originator institution shall calculate risk-weighted exposure amounts with respect to all tranches in the securitisation in accordance with this Section, including the positions in relation to which the institution is able to recognise credit risk mitigation in accordance with Article 249. The risk weight to be applied to positions which benefit from credit risk mitigation may be amended in accordance with Chapter 4. Article 252 Treatment of maturity mismatches in synthetic securitisations For the purposes of calculating risk-weighted exposure amounts in accordance with Article 251, any maturity mismatch between the credit protection by which the transfer of risk is achieved and the underlying exposures shall be calculated as follows:

Article 253 Reduction in risk-weighted exposure amounts 1. Where a securitisation position is assigned a 1 250 % risk weight under this Section, institutions may deduct the exposure value of such position from Common Equity Tier 1 capital in accordance with point (k) of Article 36(1) as an alternative to including the position in their calculation of risk-weighted exposure amounts. For that purpose, the calculation of the exposure value may reflect eligible funded credit protection in accordance with Article 249. 2. Where an institution makes use of the alternative set out in paragraph 1, it may subtract the amount deducted in accordance with point (k) of Article 36(1) from the amount specified in Article 268 as maximum capital requirement that would be calculated in respect of the underlying exposures as if they had not been securitised.

Article 254 Hierarchy of methods 1. Institutions shall use one of the methods set out in Subsection 3 to calculate risk-weighted exposure amounts in accordance with the following hierarchy:

2. For rated positions or positions in respect of which an inferred rating may be used, an institution shall use the SEC-ERBA instead of the SEC-SA in each of the following cases:

3. In cases not covered by paragraph 2, and by way of derogation from point (b) of paragraph 1, an institution may decide to apply the SEC-ERBA instead of the SEC-SA to all of its rated securitisation positions or positions in respect of which an inferred rating may be used. For the purposes of the first subparagraph, an institution shall notify its decision to the competent authority no later than 17 November 2018. Any subsequent decision to further change the approach applied to all of its rated securitisation positions shall be notified by the institution to its competent authority before the 15th November immediately following that decision. In the absence of any objection by the competent authority by 15 December immediately following the deadline referred to in the second or third subparagraph, as appropriate, the decision notified by the institution shall take effect from 1 January of the following year and shall be valid until a subsequently notified decision comes into effect. An institution shall not use different approaches in the course of the same year. 4. By way of derogation from paragraph 1, competent authorities may prohibit institutions, on a case by case basis, from applying the SEC-SA when the risk-weighted exposure amount resulting from the application of the SEC-SA is not commensurate to the risks posed to the institution or to financial stability, including but not limited to the credit risk embedded in the exposures underlying the securitisation. In the case of exposures not qualifying as positions in an STS securitisation, particular regard shall be had to securitisations with highly complex and risky features. 5. Without prejudice to paragraph 1 of this Article, an institution may apply the Internal Assessment Approach to calculate risk-weighted exposure amounts in relation to an unrated position in an ABCP programme or ABCP transaction in accordance with Article 266, provided that the conditions set out in Article 265 are met. Where an institution has received permission to apply the Internal Assessment Approach in accordance with Article 265(2), and a specific position in an ABCP programme or ABCP transaction falls within the scope of application covered by such permission, the institution shall apply that approach to calculate the risk-weighted exposure amount of that position. 6. For a position in a re-securitisation, institutions shall apply the SEC-SA in accordance with Article 261, with the modifications set out in Article 269. 7. In all other cases, a risk weight of 1 250 % shall be assigned to securitisation positions. 8. The competent authorities shall inform the EBA of any notification made pursuant to paragraph 3 of this Article. The EBA shall monitor the impact of this Article on capital requirements and the range of supervisory practices in connection with paragraph 4 of this Article, and shall report annually to the Commission on its findings and issue guidelines in accordance with Article 16 of Regulation (EU) No 1093/2010. Article 255 Determination of KIRB and KSA 1. Where an institution applies the SEC-IRBA under Subsection 3, the institution shall calculate KIRB in accordance with paragraphs 2 to 5. 2. Institutions shall determine KIRB by multiplying the risk-weighted exposure amounts that would be calculated under Chapter 3 in respect of the underlying exposures as if they had not been securitised by 8 % divided by the exposure value of the underlying exposures. KIRB shall be expressed in decimal form between zero and one. 3. For KIRB calculation purposes, the risk-weighted exposure amounts that would be calculated under Chapter 3 in respect of the underlying exposures shall include:

4. Institutions may calculate KIRB in relation to the underlying exposures of the securitisation in accordance with the provisions set out in Chapter 3 for the calculation of capital requirements for purchased receivables. For these purposes, retail exposures shall be treated as purchased retail receivables and non-retail exposures as purchased corporate receivables. 5. Institutions shall calculate KIRB separately for dilution risk in relation to the underlying exposures of a securitisation where dilution risk is material to such exposures. Where losses from dilution and credit risks are treated in an aggregate manner in the securitisation, institutions shall combine the respective KIRB for dilution and credit risk into a single KIRB for the purposes of Subsection 3. The presence of a single reserve fund or overcollateralisation available to cover losses from either credit or dilution risk may be regarded as an indication that these risks are treated in an aggregate manner. Where dilution and credit risk are not treated in an aggregate manner in the securitisation, institutions shall modify the treatment set out in the second subparagraph to combine the respective KIRB for dilution and credit risk in a prudent manner. 6. Where an institution applies the SEC-SA under Subsection 3, it shall calculate KSA by multiplying the risk-weighted exposure amounts that would be calculated under Chapter 2 in respect of the underlying exposures as if they had not been securitised by 8 % divided by the value of the underlying exposures. KSA shall be expressed in decimal form between zero and one. For the purposes of this paragraph, institutions shall calculate the exposure value of the underlying exposures without netting any specific credit risk adjustments and additional value adjustments in accordance with Articles 34 and 110 and other own funds reductions. 7. For the purposes of paragraphs 1 to 6, where a securitisation structure involves the use of an SSPE, all the SSPE’s exposures related to the securitisation shall be treated as underlying exposures. Without prejudice to the preceding, the institution may exclude the SSPE’s exposures from the pool of underlying exposures for KIRB or KSA calculation purposes if the risk from the SSPE’s exposures is immaterial or if it does not affect the institution’s securitisation position. In the case of funded synthetic securitisations, any material proceeds from the issuance of credit-linked notes or other funded obligations of the SSPE that serve as collateral for the repayment of the securitisation positions shall be included in the calculation of KIRB or KSA if the credit risk of the collateral is subject to the tranched loss allocation. 8. For the purposes of the third subparagraph of paragraph 5 of this Article, the EBA shall issue guidelines in accordance with Article 16 of Regulation (EU) No 1093/2010 on the appropriate methods to combine KIRB for dilution and credit risk where these risks are not treated in an aggregate manner in a securitisation. 9. The EBA shall develop draft regulatory technical standards to further specify the conditions to allow institutions to calculate KIRB for the pools of underlying exposures in accordance with paragraph 4, in particular with regard to:

The EBA shall submit those draft regulatory technical standards to the Commission by 18 January 2019. Power is delegated to the Commission to supplement this Regulation by adopting the regulatory technical standards referred to in the second subparagraph of this paragraph in accordance with Articles 10 to 14 of Regulation (EU) No 1093/2010. Article 256 Determination of attachment point (A) and detachment point (D) 1. For the purposes of Subsection 3, institutions shall set the attachment point (A) at the threshold at which losses within the pool of underlying exposures would start to be allocated to the relevant securitisation position. The attachment point (A) shall be expressed as a decimal value between zero and one and shall be equal to the greater of zero and the ratio of the outstanding balance of the pool of underlying exposures in the securitisation minus the outstanding balance of all tranches that rank senior or pari passu to the tranche containing the relevant securitisation position including the exposure itself to the outstanding balance of all the underlying exposures in the securitisation. 2. For the purposes of Subsection 3, institutions shall set the detachment point (D) at the threshold at which losses within the pool of underlying exposures would result in a complete loss of principal for the tranche containing the relevant securitisation position. The detachment point (D) shall be expressed as a decimal value between zero and one and shall be equal to the greater of zero and the ratio of the outstanding balance of the pool of underlying exposures in the securitisation minus the outstanding balance of all tranches that rank senior to the tranche containing the relevant securitisation position to the outstanding balance of all the underlying exposures in the securitisation. 3. For the purposes of paragraphs 1 and 2, institutions shall treat overcollateralisation and funded reserve accounts as tranches and the assets comprising such reserve accounts as underlying exposures. 4. For the purposes of paragraphs 1 and 2, institutions shall disregard unfunded reserve accounts and assets that do not provide credit enhancement, such as those that only provide liquidity support, currency or interest rate swaps and cash collateral accounts related to those positions in the securitisation. For funded reserve accounts and assets providing credit enhancement, the institution shall only treat as securitisation positions the parts of those accounts or assets that are loss-absorbing. 5. Where two or more positions of the same transaction have different maturities but share pro rata loss allocation, the calculation of the attachment points (A) and the detachment points (D) shall be based on the aggregated outstanding balance of those positions and the resulting attachment points (A) and detachment points (D) shall be the same. Article 257 Determination of tranche maturity (MT) 1. For the purposes of Subsection 3 and subject to paragraph 2, institutions may measure the maturity of a tranche (MT) as either:

2. For the purposes of paragraph 1, the determination of a tranche maturity (MT) shall be subject in all cases to a floor of 1 year and a cap of 5 years. 3. Where an institution may become exposed to potential losses from the underlying exposures by virtue of contract, the institution shall determine the maturity of the securitisation position by taking into account the maturity of the contract plus the longest maturity of such underlying exposures. For revolving exposures, the longest contractually possible remaining maturity of the exposure that might be added during the revolving period shall apply. 4. The EBA shall monitor the range of practices in this area, with particular regard to the application of point (a) of paragraph 1 of this Article, and shall, in accordance with Article 16 of Regulation (EU) No 1093/2010, issue guidelines by 31 December 2019.

Article 258 Conditions for the use of the Internal Ratings Based Approach (SEC-IRBA) 1. Institutions shall use the SEC-IRBA to calculate risk-weighted exposure amounts in relation to a securitisation position where the following conditions are met:

2. Competent authorities may on a case-by-case basis preclude the use of the SEC-IRBA where securitisations have highly complex or risky features. For these purposes, the following may be regarded as highly complex or risky features:

Article 259 Calculation of risk-weighted exposure amounts under the SEC-IRBA 1. Under the SEC-IRBA, the risk-weighted exposure amount for a securitisation position shall be calculated by multiplying the exposure value of the position calculated in accordance with Article 248 by the applicable risk weight determined as follows, in all cases subject to a floor of 15 %:

where:

where:

where:

where:

The parameters A, B, C, D, and E shall be determined according to the following look-up table:

2. If the underlying IRB pool comprises both retail and non-retail exposures, the pool shall be divided into one retail and one non-retail subpool and, for each subpool, a separate p-parameter (and the corresponding input parameters N, KIRB and LGD) shall be estimated. Subsequently, a weighted average p-parameter for the transaction shall be calculated on the basis of the p-parameters of each subpool and the nominal size of the exposures in each subpool. 3. Where an institution applies the SEC-IRBA to a mixed pool, the calculation of the p-parameter shall be based on the underlying exposures subject to the IRB Approach only. The underlying exposures subject to the Standardised Approach shall be ignored for these purposes. 4. The effective number of exposures (N) shall be calculated as follows:

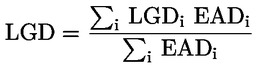

where EADi represents the exposure value associated with the ith exposure in the pool. Multiple exposures to the same obligor shall be consolidated and treated as a single exposure. 5. The exposure-weighted average LGD shall be calculated as follows:

where LGDi represents the average LGD associated with all exposures to the ith obligor. Where credit and dilution risks for purchased receivables are managed in an aggregate manner in a securitisation, the LGD input shall be construed as a weighted average of the LGD for credit risk and 100 % LGD for dilution risk. The weights shall be the stand-alone IRB Approach capital requirements for credit risk and dilution risk, respectively. For these purposes, the presence of a single reserve fund or overcollateralisation available to cover losses from either credit or dilution risk may be regarded as an indication that these risks are managed in an aggregate manner. 6. Where the share of the largest underlying exposure in the pool (C1) is no more than 3 %, institutions may use the following simplified method to calculate N and the exposure-weighted average LGDs:

LGD = 0,50 where

If only C1 is available and this amount is no more than 0,03, then the institution may set LGD as 0,50 and N as 1/C1. 7. Where the position is backed by a mixed pool and the institution is able to calculate KIRB on at least 95 % of the underlying exposure amounts in accordance with point (a) of Article 258(1), the institution shall calculate the capital charge for the pool of underlying exposures as:

where d is the share of the exposure amount of underlying exposures for which the institution can calculate KIRB over the exposure amount of all underlying exposures. 8. Where an institution has a securitisation position in the form of a derivative to hedge market risks, including interest rate or currency risks, the institution may attribute to that derivative an inferred risk weight equivalent to the risk weight of the reference position calculated in accordance with this Article. For the purposes of the first subparagraph, the reference position shall be the position that is pari passu in all respects to the derivative or, in the absence of such pari passu position, the position that is immediately subordinate to the derivative. Article 260 Treatment of STS securitisations under the SEC-IRBA Under the SEC-IRBA, the risk weight for a position in an STS securitisation shall be calculated in accordance with Article 259, subject to the following modifications: risk-weight floor for senior securitisation positions = 10 %

Article 261 Calculation of risk-weighted exposure amounts under the Standardised Approach (SEC-SA) 1. Under the SEC-SA, the risk-weighted exposure amount for a position in a securitisation shall be calculated by multiplying the exposure value of the position as calculated in accordance with Article 248 by the applicable risk weight determined as follows, in all cases subject to a floor of 15 %:

where:

where:

2. For the purposes of paragraph 1, KA shall be calculated as follows:

where: KSA is the capital charge of the underlying pool as defined in Article 255; W = ratio of:

For these purposes, an exposure in default shall mean an underlying exposure which is either: (i) 90 days or more past due; (ii) subject to bankruptcy or insolvency proceedings; (iii) subject to foreclosure or similar proceeding; or (iv) in default in accordance with the securitisation documentation. Where an institution does not know the delinquency status for 5 % or less of underlying exposures in the pool, the institution may use the SEC-SA subject to the following adjustment in the calculation KA:

Where the institution does not know the delinquency status for more than 5 % of underlying exposures in the pool, the position in the securitisation must be risk-weighted at 1 250 %. 3. Where an institution has a securitisation position in the form of a derivative to hedge market risks, including interest rate or currency risks, the institution may attribute to that derivative an inferred risk weight equivalent to the risk weight of the reference position calculated in accordance with this Article. For the purposes of this paragraph, the reference position shall be the position that is pari passu in all respects to the derivative or, in the absence of such pari passu position, the position that is immediately subordinate to the derivative. Article 262 Treatment of STS securitisations under the SEC-SA Under the SEC-SA the risk weight for a position in an STS securitisation shall be calculated in accordance with Article 261, subject to the following modifications:

Article 263 Calculation of risk-weighted exposure amounts under the External Ratings Based Approach (SEC-ERBA) 1. Under the SEC-ERBA, the risk-weighted exposure amount for a securitisation position shall be calculated by multiplying the exposure value of the position as calculated in accordance with Article 248 by the applicable risk weight in accordance with this Article. 2. For exposures with short-term credit assessments or when a rating based on a short-term credit assessment may be inferred in accordance with paragraph 7, the following risk weights shall apply: Table 1

3. For exposures with long-term credit assessments or when a rating based on a long-term credit assessment may be inferred in accordance with paragraph 7 of this Article, the risk weights set out in Table 2 shall apply, adjusted as applicable for tranche maturity (MT) in accordance with Article 257 and paragraph 4 of this Article and for tranche thickness for non-senior tranches in accordance with paragraph 5 of this Article: Table 2

4. In order to determine the risk weight for tranches with a maturity between 1 and 5 years, institutions shall use linear interpolation between the risk weights applicable for 1 and 5 years maturity respectively in accordance with Table 2. 5. In order to account for tranche thickness, institutions shall calculate the risk weight for non-senior tranches as follows:

where T = tranche thickness measured as D – A where

6. The risk weights for non-senior tranches resulting from paragraphs 3, 4 and 5 shall be subject to a floor of 15 %. In addition, the resulting risk weights shall be no lower than the risk weight corresponding to a hypothetical senior tranche of the same securitisation with the same credit assessment and maturity. 7. For the purposes of using inferred ratings, institutions shall attribute to an unrated position an inferred rating equivalent to the credit assessment of a rated reference position which meets all of the following conditions:

8. Where an institution has a securitisation position in the form of a derivative to hedge market risks, including interest rate or currency risks, the institution may attribute to that derivative an inferred risk weight equivalent to the risk weight of the reference position calculated in accordance with this Article. For the purposes of the first subparagraph, the reference position shall be the position that is pari passu in all respects to the derivative or, in the absence of such pari passu position, the position that is immediately subordinate to the derivative. Article 264 Treatment of STS securitisations under the SEC-ERBA 1. Under the SEC-ERBA, the risk weight for a position in an STS securitisation shall be calculated in accordance with Article 263, subject to the modifications laid down in this Article. 2. For exposures with short-term credit assessments or when a rating based on a short-term credit assessment may be inferred in accordance with Article 263(7), the following risk weights shall apply: Table 3

3. For exposures with long-term credit assessments or when a rating based on a long-term credit assessment may be inferred in accordance with Article 263(7), risk weights shall be determined in accordance with Table 4, adjusted for tranche maturity (MT) in accordance with Article 257 and Article 263(4) and for tranche thickness for non-senior tranches in accordance with Article 263(5): Table 4

Article 265 Scope and operational requirements for the Internal Assessment Approach 1. Institutions may calculate the risk-weighted exposure amounts for unrated positions in ABCP programmes or ABCP transactions under the Internal Assessment Approach in accordance with Article 266 where the conditions set out in paragraph 2 of this Article are met. Where an institution has received permission to apply the Internal Assessment Approach in accordance with paragraph 2 of this Article, and a specific position in an ABCP programme or ABCP transaction falls within the scope of application covered by such permission, the institution shall apply that approach to calculate the risk-weighted exposure amount of that position. 2. The competent authorities shall grant institutions permission to apply the Internal Assessment Approach within a clearly defined scope of application where all of the following conditions are met:

3. Where the institution’s internal audit, credit review, or risk management functions perform the review provided for in point (g) of paragraph 2, those functions shall be independent from the institution’s internal functions dealing with ABCP programme business and customer relations. 4. Institutions which have received permission to apply the Internal Assessment Approach shall not revert to the use of other methods for positions that fall within scope of application of the Internal Assessment Approach unless both of the following conditions are met:

Article 266 Calculation of risk-weighted exposure amounts under the Internal Assessment Approach 1. Under the Internal Assessment Approach, the institution shall assign the unrated position in the ABCP programme or ABCP transaction to one of the rating grades laid down in point (e) of Article 265(2) on the basis of its internal assessment. The position shall be attributed a derived rating which shall be the same as the credit assessments corresponding to that rating grade as laid down in point (e) of Article 265(2). 2. The rating derived in accordance with paragraph 1 shall be at least at the level of investment grade or better at the time it was first assigned and shall be regarded as an eligible credit assessment by an ECAI for the purposes of calculating risk-weighted exposure amounts in accordance with Article 263 or Article 264, as applicable.

Article 267 Maximum risk weight for senior securitisation positions: look-through approach 1. An institution which has knowledge at all times of the composition of the underlying exposures may assign the senior securitisation position a maximum risk weight equal to the exposure-weighted-average risk weight that would be applicable to the underlying exposures as if the underlying exposures had not been securitised. 2. In the case of pools of underlying exposures where the institution uses exclusively the Standardised Approach or the IRB Approach, the maximum risk weight of the senior securitisation position shall be equal to the exposure-weighted-average risk weight that would apply to the underlying exposures under Chapter 2 or 3, respectively, as if they had not been securitised. In the case of mixed pools the maximum risk weight shall be calculated as follows:

3. For the purposes of this Article, the risk weight that would be applicable under the IRB Approach in accordance with Chapter 3 shall include the ratio of:

4. Where the maximum risk weight calculated in accordance with paragraph 1 results in a lower risk weight than the risk-weight floors set out in Articles 259 to 264, as applicable, the former shall be used instead. Article 268 Maximum capital requirements 1. An originator institution, a sponsor institution or other institution using the SEC-IRBA or an originator institution or sponsor institution using the SEC-SA or the SEC-ERBA may apply a maximum capital requirement for the securitisation position it holds equal to the capital requirements that would be calculated under Chapter 2 or 3 in respect of the underlying exposures had they not been securitised. For the purposes of this Article, the IRB Approach capital requirement shall include the amount of the expected losses associated with those exposures calculated under Chapter 3 and that of unexpected losses. 2. In the case of mixed pools, the maximum capital requirement shall be determined by calculating the exposure-weighted average of the capital requirements of the IRB Approach and Standardised Approach portions of the underlying exposures in accordance with paragraph 1. 3. The maximum capital requirement shall be the result of multiplying the amount calculated in accordance with paragraphs 1 or 2 by the largest proportion of interest that the institution holds in the relevant tranches (V), expressed as a percentage and calculated as follows:

4. When calculating the maximum capital requirement for a securitisation position in accordance with this Article, the entire amount of any gain on sale and credit-enhancing interest-only strips arising from the securitisation transaction shall be deducted from Common Equity Tier 1 items in accordance with point (k) of Article 36(1).

Article 269 Re-securitisations 1. For a position in a re-securitisation, institutions shall apply the SEC-SA in accordance with Article 261, with the following changes:

2. KSA for the underlying securitisation exposures shall be calculated in accordance with Subsection 2. 3. The maximum capital requirements set out in Subsection 4 shall not be applied to re-securitisation positions. 4. Where the pool of underlying exposures consists of a mix of securitisation tranches and other types of assets, the KA parameter shall be determined as the nominal exposure weighted-average of the KA calculated individually for each subset of exposures. Article 270 Senior positions in SME securitisations An originator institution may calculate the risk-weighted exposure amounts in respect of a securitisation position in accordance with Articles 260, 262 or 264, as applicable, where the following conditions are met:

Article 270a Additional risk weight 1. Where an institution does not meet the requirements in Chapter 2 of Regulation (EU) 2017/2402 in any material respect by reason of negligence or omission by the institution, the competent authorities shall impose a proportionate additional risk weight of no less than 250 % of the risk weight, capped at 1 250 %, which shall apply to the relevant securitisation positions in the manner specified in Article 247(6) or Article 337(3) of this Regulation respectively. The additional risk weight shall progressively increase with each subsequent infringement of the due diligence and risk management provisions. The competent authorities shall take into account the exemptions for certain securitisations provided for in Article 6(5)) of Regulation (EU) 2017/2402 by reducing the risk weight they would otherwise impose under this Article in respect of a securitisation to which Article 6(5) of Regulation (EU) 2017/2402 applies. 2. The EBA shall develop draft implementing technical standards to facilitate the convergence of supervisory practices with regard to the implementation of paragraph 1, including the measures to be taken in the case of breach of the due diligence and risk management obligations. The EBA shall submit those draft implementing technical standards to the Commission by 1 January 2014. Power is conferred on the Commission to adopt the implementing technical standards referred to in the first subparagraph of this paragraph in accordance with Article 15 of Regulation (EU) No 1093/2010.

Article 270b Use of credit assessments by ECAIs Institutions may use only credit assessments to determine the risk weight of a securitisation position in accordance with this Chapter where the credit assessment has been issued or has been endorsed by an ECAI in accordance with Regulation (EC) No 1060/2009. Article 270c Requirements to be met by the credit assessments of ECAIs For the purposes of calculating risk-weighted exposure amounts in accordance with Section 3, institutions shall only use a credit assessment of an ECAI where all of the following conditions are met:

Article 270d Use of credit assessments 1. An institution may decide to nominate one or more ECAIs the credit assessments of which shall be used in the calculation of its risk-weighted exposure amounts under this Chapter (a “nominated ECAI”). 2. An institution shall use the credit assessments of its securitisation positions in a consistent and non-selective manner and, for these purposes, shall comply with the following requirements:

3. Where the exposures underlying a securitisation benefit from full or partial eligible credit protection in accordance with Chapter 4, and the effect of such protection has been reflected in the credit assessment of a securitisation position by a nominated ECAI, the institution shall use the risk weight associated with that credit assessment. Where the credit protection referred to in this paragraph is not eligible under Chapter 4, the credit assessment shall not be recognised and the securitisation position shall be treated as unrated. 4. Where a securitisation position benefits from eligible credit protection in accordance with Chapter 4 and the effect of such protection has been reflected in its credit assessment by a nominated ECAI, the institution shall treat the securitisation position as if it were unrated and calculate the risk-weighted exposure amounts in accordance with Chapter 4. Article 270e Securitisation mapping The EBA shall develop draft implementing technical standards to map in an objective and consistent manner the credit quality steps set out in this Chapter relative to the relevant credit assessments of all ECAIs. For the purposes of this Article, the EBA shall in particular:

The EBA shall submit those draft implementing technical standards to the Commission by 1 July 2014. Power is conferred on the Commission to adopt the implementing technical standards referred to in the first subparagraph of this paragraph in accordance with Article 15 of Regulation (EU) No 1093/2010.’. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

(10) |

Article 337 is replaced by the following: ‘Article 337 Own funds requirement for securitisation instruments 1. For instruments in the trading book that are securitisation positions, the institution shall weight the net positions as calculated in accordance with Article 327(1) with 8 % of the risk weight the institution would apply to the position in its non-trading book according to Section 3 of Chapter 5 of Title II. 2. When determining risk weights for the purposes of paragraph 1, estimates of PD and LGD may be determined based on estimates that are derived from an internal incremental default and migration risk model (IRC model) of an institution that has been granted permission to use an internal model for specific risk of debt instruments. The latter alternative may be used only subject to permission by the competent authorities, which shall be granted if those estimates meet the quantitative requirements for the IRB Approach set out in Chapter 3 of Title II. In accordance with Article 16 of Regulation (EU) No 1093/2010, the EBA shall issue guidelines on the use of estimates of PD and LGD as inputs when those estimates are based on an IRC model. 3. For securitisation positions that are subject to an additional risk weight in accordance with Article 247(6), 8 % of the total risk weight shall be applied. 4. The institution shall sum its weighted positions resulting from the application of paragraphs 1, 2 and 3 regardless of whether they are long or short, in order to calculate its own funds requirement against specific risk, except for securitisation positions subject to Article 338(4). 5. Where an originator institution of a traditional securitisation does not meet the conditions for significant risk transfer set out in Article 244, the originator institution shall include the exposures underlying the securitisation in its calculation of own funds requirement as if those exposures had not been securitised. Where an originator institution of a synthetic securitisation does not meet the conditions for significant risk transfer set out in Article 245, the originator institution shall include the exposures underlying the securitisation in its calculation of own funds requirements as if those exposures had not been securitised and shall ignore the effect of the synthetic securitisation for credit protection purposes.’. |

|

(11) |

Part Five is deleted and all references to Part Five shall be read as references to Chapter 2 of Regulation (EU) 2017/2402. |

|

(12) |

In Article 457, point (c) is replaced by the following:

|

|

(13) |

Article 462 is replaced by the following: ‘Article 462 Exercise of the delegation 1. The power to adopt delegated acts is conferred on the Commission subject to the conditions laid down in this Article. 2. The power to adopt delegated acts referred to in Articles 244(6) and 245(6) and in Articles 456 to 460 shall be conferred on the Commission for an indeterminate period of time from 28 June 2013. 3. The delegation of power referred to in Articles 244(6) and 245(6) and in Articles 456 to 460 may be revoked at any time by the European Parliament or by the Council. A decision to revoke shall put an end to the delegation of the power specified in that decision. It shall take effect the day following the publication of the decision in the Official Journal of the European Union or at a later date specified therein. It shall not affect the validity of the delegated acts already in force. 4. Before adopting a delegated act, the Commission shall consult experts designated by each Member State in accordance with the principles laid down in the Interinstitutional Agreement of 13 April 2016 on Better Law-Making. 5. As soon as it adopts a delegated act, the Commission shall notify it simultaneously to the European Parliament and to the Council. 6. A delegated act adopted pursuant to Articles 244(6) and 245(6) and Articles 456 to 460 shall enter into force only if no objection has been expressed by the European Parliament or the Council within a period of 3 months of notification of that act to the European Parliament and the Council or if, before the expiry of that period, the European Parliament and the Council have both informed the Commission that they will not object. That period shall be extended by 3 months at the initiative of the European Parliament or of the Council.’. |

|

(14) |

The following article is inserted: ‘Article 519a Reporting and review By 1 January 2022, the Commission shall report to the European Parliament and the Council on the application of the provisions in Chapter 5 of Title II of Part Three in the light of developments in securitisation markets, including from a macroprudential and economic perspective. That report shall, if appropriate, be accompanied by a legislative proposal and shall, in particular, assess the following points:

The report shall also take into account regulatory developments in international fora, in particular those relating to international standards on securitisation.’. |

Article 2

Transitional provisions concerning outstanding securitisation positions

In respect of securitisations the securities of which were issued before 1 January 2019, institutions shall continue to apply the provisions set out in Chapter 5 of Title II of Part Three and Article 337 of Regulation (EU) No 575/2013 until 31 December 2019 in the version applicable on 31 December 2018.

For the purposes of this Article, in the case of securitisations which do not involve the issuance of securities, the reference to ‘securitisations the securities of which were issued’ shall be deemed to mean securitisations the initial securitisation positions of which were created.

Article 3

Entry into force and date of application

This Regulation shall enter into force on the twentieth day following that of its publication in the Official Journal of the European Union.

It shall apply from 1 January 2019.

This Regulation shall be binding in its entirety and directly applicable in all Member States.

Done at Strasbourg, 12 December 2017.

For the European Parliament

The President

A. TAJANI

For the Council

The President

M. MAASIKAS

(1) OJ C 219, 17.6.2016, p. 2.

(3) Position of the European Parliament of 26 October 2017 (not yet published in the Official Journal) and decision of the Council of 20 November 2017.

(4) Regulation (EU) 2017/2402 of the European Parliament and of the Council of 12 December 2017 laying down a general framework for securitisation and creating a specific framework for simple, transparent and standardised securitisation, and amending Directives 2009/65/EC, 2009/138/EC, 2011/61/EU and Regulations (EC) No 1060/2009 and (EU) No 648/2012 (OJ L 347, 28.12.2017, p. 35).

(5) Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012 (OJ L 176, 27.6.2013, p. 1).

(6) Regulation (EU) No 1093/2010 of the European Parliament and of the Council of 24 November 2010 establishing a European Supervisory Authority (European Banking Authority), amending Decision No 716/2009/EC and repealing Commission Decision 2009/78/EC (OJ L 331, 15.12.2010, p. 12).

(7) Directive 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment firms and amending Council Directive 82/891/EEC, and Directives 2001/24/EC, 2002/47/EC, 2004/25/EC, 2005/56/EC, 2007/36/EC, 2011/35/EU, 2012/30/EU and 2013/36/EU, and Regulations (EU) No 1093/2010 and (EU) No 648/2012, of the European Parliament and of the Council (OJ L 173, 12.6.2014, p. 190).

(8) OJ L 123, 12.5.2016, p. 1.

|

28.12.2017 |

EN |

Official Journal of the European Union |

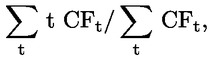

L 347/35 |

REGULATION (EU) 2017/2402 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL

of 12 December 2017