ISSN 1725-2555

Official Journal

of the European Union

L 49

English edition

Legislation

Volume 51

22 February 2008

|

ISSN 1725-2555 |

||

|

Official Journal of the European Union |

L 49 |

|

|

|

||

|

English edition |

Legislation |

Volume 51 |

|

Contents |

|

II Acts adopted under the EC Treaty/Euratom Treaty whose publication is not obligatory |

page |

|

|

|

DECISIONS |

|

|

|

|

Commission |

|

|

|

|

2008/136/EC |

|

|

|

* |

Commission Decision of 22 June 2006 on the ad hoc financing of Dutch public service broadcasters C 2/2004 (ex NN 170/2003) (notified under document number C (2006)2084) ( 1 ) |

|

|

|

|

2008/137/EC |

|

|

|

* |

Commission Decision of 7 March 2007 — State aid C 10/06 (ex N555/05) — Cyprus Airways Public Ltd — Restructuring plan (notified under document number C (2007) 300) ( 1 ) |

|

|

|

|

|

(1) Text with EEA relevance |

|

EN |

Acts whose titles are printed in light type are those relating to day-to-day management of agricultural matters, and are generally valid for a limited period. The titles of all other Acts are printed in bold type and preceded by an asterisk. |

II Acts adopted under the EC Treaty/Euratom Treaty whose publication is not obligatory

DECISIONS

Commission

|

22.2.2008 |

EN |

Official Journal of the European Union |

L 49/1 |

COMMISSION DECISION

of 22 June 2006

on the ad hoc financing of Dutch public service broadcasters C 2/2004 (ex NN 170/2003)

(notified under document number C (2006)2084)

(Only the Dutch text is authentic)

(Text with EEA relevance)

(2008/136/EC)

THE COMMISSION OF THE EUROPEAN COMMUNITIES,

Having regard to the Treaty establishing the European Community, and in particular the first subparagraph of Article 88(2) thereof,

Having regard to the Agreement on the European Economic Area, and in particular Article 62(1)(a) thereof,

Having called on interested parties to submit their comments pursuant to the provisions cited above (1),

Having regard to their comments,

Whereas:

I. PROCEDURE AND BACKGROUND

1 PROCEDURE

|

(1) |

In the course of 2002 (2) and 2003 (3) the Commission received several complaints alleging that the public funding system in place for Dutch public broadcasters constitutes unlawful and incompatible state aid within the meaning of Article 87(1) of the EC Treaty. |

|

(2) |

In the course of the preliminary investigation of the complaints, the Commission received additional information from the complainants (4), as well as the Dutch authorities (5). |

|

(3) |

Following the preliminary assessment of the alleged aid measures, the Commission informed the Netherlands, by letter dated 3 February 2004, that it had decided to initiate the procedure laid down in Article 88(2) of the EC Treaty with respect to certain measures which could be qualified as new aid. |

|

(4) |

The Commission decision to initiate the procedure was published in the Official Journal of the European Union (6). The Commission invited interested parties to submit their comments on the aid. |

|

(5) |

The Netherlands responded to the decision to open proceedings by letter dated 30 April 2004. Moreover, the Commission received comments from 11 interested parties (7). By letter of 29 April 2004 the Commission forwarded the comments to the Netherlands. The reaction by the Dutch authorities was received by letter dated 13 August 2004. |

|

(6) |

The Commission asked additional questions to the Dutch authorities by letters of 4 January 2005 and 25 May 2005, to which the Dutch authorities responded by letters of 27 January 2005 and 25 July 2005. Further information was received from one of the complainants (De Telegraaf) on 25 July 2005 and from the Dutch authorities on 2 September. The Commission asked the Dutch authorities for further clarification by e-mails on 22 November 2005, to which the authorities responded on 25 November 2005. The Commission decided after a meeting with the authorities that further clarification was necessary. To this end a request for information was sent to the Dutch authorities on 22 December 2005, to which the Dutch authorities, having been granted a delay, responded on 3 February 2006. Regarding this reply further e-mails were exchanged between the Dutch authorities and the Commission in February 2006 and April 2006. |

|

(7) |

A meeting between the Dutch authorities and the Commission took place on 24 September 2004. A meeting with De Telegraaf took place on 27 October 2004. A meeting with Broadcast Partners took place on 5 January 2005. A meeting between RTL and the Commission took place on 27 July 2005 and between VESTRA and the Commission on 23 September 2005. The Commission had another meeting with the Dutch authorities on 1 February and 14 February 2006. |

|

(8) |

In addition to this procedure on ‘new aid’, the financing of the public service broadcasters through annual state payments and the Stimulation Fund (Stifo, Stichting Stimuleringsfonds Nederlandse Culturele Omroepproducties) (8) is being assessed in a separate ‘existing aid’ procedure (cf. state aid No. E-5/2005). In this Decision the Commission refers to the measures which are the object of the ‘existing aid procedure’ only insofar as necessary to provide an overall picture of the financing of public broadcasting. This Decision does not, however, concern the issue of compatibility with state aid rules of the regular annual payments and of the payments from the Stimulation Fund. |

|

(9) |

This Decision will also be limited to assessing the financing of the public service broadcasters' core activities (the so-called main tasks). Side activities, like the new media services, the provision of SMS and i-mode, are not, therefore, examined. Similarly, this Decision will not deal with the investment by NOS in the network operator Nozema, which according to complaints might not have been done on market terms. These issues will be dealt with separately. |

|

(10) |

Finally, the decision to open the formal investigation procedure covered the procedure as from 1992. Nevertheless, it appears that the first ad hoc payments were made only in 1994. Furthermore, figures up to 2005 are now available and should be taken into account. The period covered by the decision would therefore range from 1994 — when the first ad hoc payment was made — to 2005, the last year for which final figures are available. It should be noted that the Dutch authorities invited the Commission also to take into account 2006. However, the figures for 2006 are only provisional and cannot, therefore, be taken into account. |

2 DETAILED DESCRIPTION OF THE PUBLIC BROADCASTING SYSTEM

|

(11) |

Section 2.1 of this Chapter presents the actors in the (public) broadcasting sector. This is followed in section 2.2 by a description of the different elements of the financing system for the Dutch broadcasting sector in general. In connection with this, the legal provisions entrusting the broadcasters with a public service mission are described, the different financing mechanisms (annual payments and ad hoc payments) are spelled out and, finally, the reserves the public broadcasters have built up and use for the fulfilment of their public service mission are explained. The commercial activities of the Dutch public broadcasters are then discussed in section 2.5. Section 2.6 explains the acquisition of football rights by the NOS and section 2.7 deals with the relation between broadcasters and cable operators. Finally, section 2.8 sets out which measures are the subject of this procedure. |

2.1 Actors in the (public) broadcasting sector

|

(12) |

The public service broadcasting system consists of different organisations, including eight private associations (private broadcasters with members entrusted with a public service mission) and ten private foundations (private broadcasters without members entrusted with a public service mission) (9). |

|

(13) |

Besides the broadcasters mentioned in paragraph 12, the public service broadcasting system includes another actor — the NOS — which performs a dual role. The first role is that of a public service broadcaster, responsible for TV and radio programmes (under the name of ‘NOS RTV’). The second role is that of coordinator of the entire public service broadcasting system and is carried out by the management board of the NOS (the so-called ‘Publieke Omroep’ hereinafter ‘PO’). The PO, whose functions and tasks are enshrined in the Media Act, stimulates cooperation between public broadcasters, coordinates the three public TV channels and reports twice a year on the public broadcasters' activities to the Media Authority. |

|

(14) |

The NOS receives funding from the media budget for both the tasks performed as PO and those performed as NOS RTV. |

|

(15) |

The public service TV-programmes are broadcast by the public service broadcasters over three public channels (10). |

|

(16) |

The Dutch Broadcast Production Organisation (Nederlands Omroepbedrijf, hereinafter ‘NOB’) is also part of the public broadcasting system. The NOB carries out the recording, transmission preparation and actual transmission of sound, moving pictures and data to all possible distribution channels. The NOB provides these services to commercial broadcasters and public service broadcasters. The services provided to the public service broadcasters are considered as public services by the Dutch government and are publicly funded (11). |

|

(17) |

A separate foundation (Stichting Ether Reclame, hereinafter ‘STER’) is exclusively responsible for the sale of advertising space and the broadcasting of advertising on the public channels. The STER is responsible for the broadcasting time which it has been allocated. The revenues generated by the STER are transferred directly to the State. |

|

(18) |

In addition to the national public service broadcasters, there are several commercial broadcasters operating on a national level. Examples of these commercial broadcasters are RTL (RTL 4, 5 and 7, all from the CLT-UFA group), SBS6, NET5 and Veronica (from the SBS Broadcasting group) and Talpa (Talpa Media Holding). They generate their revenues mainly through TV advertising. |

2.2 Statutory regulation of public service broadcasting

|

(19) |

The broadcasting sector is currently regulated by the Media Act of 21 April 1987 (Stb. 1987, 249) and the Media Decree. Public broadcasters are allowed by law to perform four categories of activities, which are defined in the current Media Act as ‘main task’, ‘side tasks’, ‘side activities’ and ‘association activities’. The public broadcasters are eligible for state funding for the ‘main task’ and ‘side tasks’. |

2.2.1 Legal definitions

|

(20) |

Article 13(c)(1) of the Media Act describes the ‘main task’ of the public service broadcasting as being:

|

|

(21) |

Article 13c(2) of the Media Act lays down the general requirements for the programmes to be broadcast by the public broadcasters. The programmes must ‘give an image of society in a balanced way and of interests and viewpoints on society, culture and philosophy within the population; and

|

|

(22) |

In addition, the total programming time which should be allocated to different categories, such as culture, education, and entertainment, is regulated by means of prescribed percentages (12). |

|

(23) |

Article 16 of the Media Act provides that certain tasks shall be performed by the NOS RTV and lays down the details of these tasks. The provision of sports coverage, including, but not limited to, competition and cup matches and international events is covered. The percentage of total broadcasting time which should be devoted to such sports events is not pre-determined by statute. In practice the NOS RTV aims to devote 9-11 % of total broadcasting time to sports programmes (13). |

|

(24) |

Broadcasting associations are entitled to broadcasting time for the provision of national TV-programmes and have the right, under Article 31(4) of the Media Act, to receive state funding for providing the programme. |

|

(25) |

In accordance with Article 13c(3) of the Media Act, which was introduced in 2000, the public broadcasting system ‘can also fulfil its task, as mentioned in the first paragraph, by providing means of supply and distribution of programme materials, other than those included within paragraph (1)(a)’. In other words, the public service broadcasters can broadcast the public service content, mentioned in paragraph 20 as a main task, on other media platforms, such as the Internet. |

|

(26) |

These so-called ‘side tasks’ must comply with a number of conditions. According to Article 55 of the Media Act, for example, they must not serve to make profits for third parties. Maintaining a website or a theme channel are examples of these side tasks. |

|

(27) |

It should also be mentioned that the exploitation of both the ‘main’ and the ‘side’ tasks generate revenues for the public service broadcasters to be used for public service purposes (14). |

|

(28) |

The Dutch public service broadcasters can also perform activities which are defined as side activities and association activities. Side activities (15) must comply with a number of statutory conditions. Examples of such side activities include the sale of programme guides, sponsoring, sale of programme rights and programme-related material, leasing office space and organising drive-in shows. |

|

(29) |

Other activities are the ‘association activities’, which are activities performed by the broadcasting associations for their members. They include publishing magazines, and organising and selling travel arrangements. |

2.2.2 Entrustment and supervision

|

(30) |

An independent Media Authority (Commissariaat voor de Media) is responsible for ensuring compliance with the programming and financial requirements of the Media Act and the implementing legislation (Article 9 of the Media Act). |

|

(31) |

The Media Authority has a legal duty, laid down in Article 134 of the Media Act, to ensure that the public broadcasters fulfil their obligations, including the quota laid down for different types of programmes. The Media Authority can impose fines if the obligations are not respected. It also checks whether the broadcasters are complying with the legal restrictions on sponsoring and advertising. |

|

(32) |

On the basis of the accountants' reports submitted, the Authority checks every year whether the annual accounts of the public broadcasters comply with the requirements of the Media Act, the Media Decree and the Financial Reporting Manual. If they do, the Authority approves the budgeted amounts for regular programme provision (Articles 100 and 101 of the Media Act). |

2.3 Sources of funding of public service broadcasters

|

(33) |

The public service broadcasters' main sources of funding are the annual payments received by the State. In order to absorb budgetary fluctuations, public service broadcasters are allowed to keep certain reserves. In addition, the public service broadcasters have, since 1994, received ad hoc payments. |

|

(34) |

Since the assessment of the compatibility of the ad hoc funding cannot be carried out without taking into account the other sources of public funding, the following description covers both the annual payments and the ad hoc payments, even though the annual payments and the payments from the Stifo are not subject to this Decision (see paragraph 8). |

2.3.1 Annual payments

|

(35) |

The Dutch public broadcasters receive annual financial contributions from the State's media budget. Over the period 1994-2005, these payments totalled approximately €7,1 billion. From this amount, approximately €819,6 million was transferred to the PO for its management and coordinating role; the remaining €6,3 billion was paid to the individual broadcasters. The media budget is funded from several sources: the State Broadcasting Contribution (collected from taxpayers), advertising revenues from STER and interest revenues from the General Broadcasting Fund (Algemene Omroepreserve, hereinafter ‘AOR’) (16). The level of the media budget sets a ceiling on the amount of annual funding that could be made available to the public broadcasters and the other media organisations. |

2.3.2 Stifo

|

(36) |

In addition to the annual payments, the public broadcasters have received payments from Stifo (Stimulation Fund for Cultural Productions). The funds granted from Stifo qualify as a state aid measure, but the measure was approved by the Commission (NN 32/91). The Stifo aid measure is thus to be considered as existing state aid. The Stifo payments to the individual public service broadcasters (the PO did not receive any payments from Stifo) amounted to €155 million in the period under review. |

2.3.3 Ad hoc

|

(37) |

In addition to the transfers mentioned in paragraphs 34 and 35 — which are considered to be the public service broadcasters' regular sources of funding, the public broadcasters were granted several payments on an ad hoc basis. These were either made directly to the broadcasters or channelled through special funds and reserves. |

2.3.3.1 Matching funds payments

|

(38) |

The matching funds are an earmarked part of the media budget. In the period 1996-1998, an amount of € [...] (17) million was transferred from the matching funds to NOS RTV. The matching funds were introduced in 1996 to co-finance increased programme right prices. The conditions under which the funds can be distributed were adopted by mutual agreement between the State and the public broadcasters. If the public broadcasters are unable to fund the purchase of rights which have increased excessively in price from their regular budget, the State will make a contribution, i.e. co-finance the acquisition of these rights by providing a matching amount. |

2.3.3.2 Broadcasting Reserve Fund (FOR) payments

|

(39) |

In 1998 the Minister of Education, Culture and Science was given the possibility, under Article 106a of the Media Act, of transferring money on an ad hoc basis from the AOR, which is managed by the Media Authority, to a fund intended to finance specific initiatives of the PO and the public service broadcasters. The fund, referred to as the FOR, was established in 1999 and is controlled by the PO. |

|

(40) |

The principle is that, if the AOR exceeds €90,8 million, there is scope for a transfer to the FOR. This, however, is not an automatic process. Each year the Minister of Education, Culture and Science decides whether a transfer is possible and if so, how much can be transferred. Where such a transfer is approved, the rules are laid down in a protocol. Such protocols were established in 1999 and 2001. On the basis of Article 99 2(d) of the Media Act, the budget must also contain a description of how the Board of Management proposes to spend the money. Based on this proposal, the Minister can then make available to the PO funds from the FOR, which can be used for purposes established by the Minister when making the money available (18). Although the FOR is a fund dedicated to PO initiatives, it is not a reserve that is part of the assets of the PO. |

|

(41) |

The funds available in the FOR make it possible for the PO to give a qualitative impetus, improve programming and invest in the public broadcasters in general. More specifically, the goal of the FOR is to:

|

|

(42) |

By 2005 the public broadcasting system had received €191,2 million from the FOR, of which €157,4 million was transferred to the individual public service broadcasters and €33,8 million to the PO. |

2.3.3.3 Co-Production Fund (CoBo) payments

|

(43) |

The Co-Production Fund (Coproductiefonds Binnenlandse Omroep: hereinafter ‘CoBo Fund’) was created to finance co-productions between Dutch public broadcasters and other programme producers. Its income comes from revenues generated by the copyright payments paid by Belgian and German cable operators for the distribution of the three Dutch channels in Belgium and Germany. The Fund was established by the public broadcasters and is managed through a foundation. The board of the Fund consists of managers from the public broadcasters. |

|

(44) |

In 1994 the Dutch authorities decided to make payments to two sub-funds managed by the CoBo Fund, the ‘Film Fund’, which finances co-productions of films and documentaries, and the ‘Telefilm’ project, which aims to stimulate the production of high-quality television films. |

|

(45) |

The individual public service broadcasters received €31,7 million of public money from the CoBo Fund in the period 1994-2005. The PO did not receive any payments from the CoBo Fund. |

2.4 The reserves held by the individual broadcasters

|

(46) |

Each public service broadcaster maintains certain reserves, which are, typically, a programme reserve and either an association or a foundation reserve, depending on whether the public service broadcaster is a foundation or an association. |

2.4.1 Programme reserves

|

(47) |

Individual public service broadcasters are allowed to increase their reserves when total revenues exceed total costs. These programme reserves can be used to cover programme costs in future years. |

|

(48) |

According to the Dutch authorities, the value of programmes which have been produced but not yet broadcast is added to the programme reserves (19). The programme reserves thus also reflect the value of programmes already produced. In 2005 the total programme reserves held by the individual public broadcasters amounted to €78,6 million. |

|

(49) |

In 2005 the PO also decided that part of the programme reserves should be transferred to the PO itself, but the broadcasters were allowed to maintain reserves of up to 5-10 % of their annual budget. The public broadcasters transferred to the PO an amount of €42,457 million. |

2.4.2 Association reserves

|

(50) |

The public service broadcasting associations originated as private law entities. Over the years they have built up their own association reserves from contributions and legacies received from their members. The association reserves thus originated from private resources. In 1993 the Dutch government decided to ‘freeze’ the association reserves. As of that moment, in principle (20), the profits generated by association activities and other non-public activities had to be used for public service activities and could no longer be transferred to the association reserves. In 2005 the public service broadcasters in the Netherlands had a total association reserve of approximately €131,1 million. |

2.4.3 Foundation reserve NOS RTV and smaller broadcasters

|

(51) |

The NOS RTV, NPS and other smaller broadcasters without members (Article 39f of the Media Act) hold a ‘foundation’ reserve’ (‘stichtingsreserve’). The overall level of the foundation reserves was €42,2 million in 2005 (21). |

2.5 Advertising on public service channels

|

(52) |

As explained in paragraph 17, the STER is responsible for selling advertising time on public service channels. |

|

(53) |

The other main companies selling TV advertising time which are active on the Dutch market are IP and SBS. IP sells advertising time on behalf of the commercial broadcasters RTL4, RTL5 and Yorin. SBS sells advertising time for its commercial broadcasters SBS6, Net 5 and Veronica. In addition to IP and SBS there are a few other commercial broadcasters who also sell advertising time (22). The rates charged by the STER are calculated on the basis of forecasts from advertising agencies, competitors' rates and price history. |

|

(54) |

Table 1 below shows the evolution of the audience share of the public service broadcasters for which STER manages the sale of advertising. The audience share of viewers aged 13+ has declined in recent years from 38,8 in 1997 to 35,4 % in 2005. For the 20-49 category, the audience share is even lower, at 27,2 %. Table 1: Audience share 13+ and 20-49 years old (18.00h - 24.00h), 1997 - 2005

|

|||||||||||||||||||||||||||||||||||||||||||

|

(55) |

Since 1994, the gross revenue (based on list prices) and net revenue (taking into account discounts granted) generated by the commercial broadcasters on the advertising market have exceeded the revenue generated by the public broadcasters. Table 2: Gross revenues from TV advertising 1994 - 2005 (amounts x €1 million)

Table 3: Net revenues from TV advertising, 1994 - 2005 (amounts x €1 million)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

(56) |

As can be inferred from Tables 1, 2 and 3, there is a difference between gross revenues from TV advertising and revenues net of discounts. According to the Dutch authorities, not only are the published tariffs of the public service broadcasters higher, but also the discounts that they grant are lower in comparison with commercial broadcasters (23). |

2.6 Acquisition of football rights by the NOS RTV

|

(57) |

During the period under investigation the NOS RTV obtained broadcasting rights for several important football events (24). The commercial broadcaster Canal+ (pay-TV) obtained the rights for the live matches of the Dutch premier league. The rights for the Champions League were also partly sublicensed to Canal+ by the NOS RTV. The commercial broadcaster SBS obtained the broadcasting rights of two national football cups. It also obtained the rights to the Dutch first division matches and the qualification matches of the Dutch team for the European Championship 2004. The broadcasting rights for various foreign football competitions are held by CLT-UFA, Europe's largest broadcasting group (the parent company of e.g. RTL). |

2.7 Relation between broadcasters and cable operators

|

(58) |

Traditional cable transmission is seen as a separate publication for the purpose of copyright under Dutch law. In principle, the permission of all copyright holders is required, and the copyright holder may claim a payment from the cable operator for the publication. Since 1985 there has been an agreement between the VECAI (representing the cable operators) and the NOS RTV (representing the public broadcasters) under which the cable operators are exempted from making copyright payments to the public broadcasters (the copyright holders) when their programmes are transmitted via cable (25). This agreement was made at the request of the Dutch Government, on the grounds that citizens already paid a contribution for public broadcasting. It was considered that a copyright payment from cable operators, which could result in higher cable subscription fees, would be undesirable. Commercial broadcasters have not asked for copyright payments from the cable operators either. However, this is not related to the aforementioned agreement with the public service broadcasters. |

|

(59) |

It should be noted that cable operators are legally obliged to transmit all the public broadcasters' radio and TV programmes (‘must carry’ obligation) and cannot charge broadcasters for the transmission costs. |

2.8 The measures subject to this Decision

|

(60) |

As set out in the decision to open the formal investigation procedure (26), the following measures are the subject of this Decision:

|

II. GROUNDS FOR INITIATING THE PROCEDURE AND ARGUMENTS OF THE PARTIES

3 SUMMARY OF THE GROUNDS FOR INITIATING THE PROCEDURE

|

(61) |

After its initial investigation, the Commission concluded that certain measures, with the possible exception of the ‘must carry’ obligation, constituted state aid within the meaning of Article 87(1) of the EC Treaty. The Commission also expressed doubts about the compatibility of such state aid under Article 86(2) of the EC Treaty. |

|

(62) |

Regarding the proportionality of the funding, the Commission doubted whether costs and revenues were allocated according to clearly established cost accounting principles. The Commission doubted whether non-public service revenues were fully taken into account when calculating the need for state funding, leading to a risk of funding going beyond the net costs of the public service. |

|

(63) |

Furthermore, the Commission considered that the level of funds in the FOR and the programme reserves was an indication of structural over-compensation. The Commission noted that, of the total ad hoc payments, an amount of €110 million (based on figures of 2001) had not been used. |

|

(64) |

Moreover, the Commission expressed its intention to investigate whether competition in commercial markets had been unlawfully distorted. The Commission stressed that such distortion of competition could occur in the markets for advertising, intellectual property rights for cable transmission and football transmission rights. |

|

(65) |

Finally, the NOB is not allowed to charge the public broadcasters for the services it provides, but receives payments for this task directly from the State. The Commission noted that the provision of technical facilities free of charge could constitute aid to the public broadcasters. |

4. COMMENTS FROM INTERESTED PART IES

|

(66) |

The following comments relevant for this Decision were provided. |

|

(67) |

The Dutch public broadcasters argued that the measures in question should be considered existing aid because they constitute part of the general financing system for public broadcasting. Moreover, they remarked that the Commission should assess the financing of public broadcasting only in the light of the Protocol on the system of public broadcasting in the Member States, annexed to the EC Treaty (hereinafter ‘Amsterdam Protocol’), and should not apply the criteria of the Altmark judgment (27) or Article 87(1) or 86(2) of the EC Treaty. |

|

(68) |

CLT-UFA noted that it was not until 2002 that the accounts of the public service broadcasting system could be verified and approved by an independent accountant. |

|

(69) |

The public broadcasters commented that there is no over-compensation of €110 million as stated by the Commission. First of all, the public broadcasters and the government work with different accounting systems. The government works on a cash receipts basis of accounting and the public broadcasters work on the basis of costs and revenues which are entered in the accounts at the moment of the transaction. This causes discrepancies. In addition, the revenues of the FOR are, according to the public broadcasters, earmarked for specific future goals. Moreover, they commented that the excess financing cannot lead to distortions in other markets, as this financing can only be used for the public service activities. |

|

(70) |

ACT stated that STER behaves in an anti-competitive manner by undercutting prices in the advertising market. It argues that since the total annual advertising time of public broadcasters is more limited than that of commercial broadcasters, the STER should charge higher prices than commercial operators. |

|

(71) |

SBS Broadcasting confirmed that prices in the Dutch television advertising market are set for GRP (Gross Rating Point) category 20-49. However, as the public broadcasters attract more viewers than commercial broadcasters outside this viewer group, advertisers would be willing to pay a premium on the GRP 20-49. Therefore, a comparison of the GRP 20-49 would not convey the economic reality of the product. Moreover, SBS remarked that for GRP 13+ public broadcasters set lower prices than commercial broadcasters. To support its comments SBS submitted overviews of the average gross GRP 13+ prices for the different channels during prime time in 1995-2004 and per month in 2003 and 2004, which show that those of public broadcasters are lower than those of most commercial operators. |

|

(72) |

According to CLT-UFA the NOS RTV has paid excessive prices for football rights. The prices were far above market prices. CLT-UFA submitted calculation models (28) to show how they calculate the prices for football rights and concluded on this basis that the bid made by the NOS RTV for the rights for the Champions League matches of 2002 was significantly higher than that made by CLT-UFA. ACT and CLT-UFA considered, moreover, that the Commission should not reach the conclusion that there is insufficient evidence of overpayment of football rights on the basis of one example where a commercial operator may have overbid. |

|

(73) |

The association of cable operators, VECAI, raises two issues. First of all, it considers that the cable operators who are subject to the ‘must carry’ obligation should be able to ask for a payment from the relevant broadcasters. Due to the ‘must carry’ obligation, the public broadcasters have not paid a fee for the transmission of the signal over the cable networks. |

|

(74) |

Secondly, VECAI argued that the cable operators actually do pay a fee to the organisations which manage rights on behalf of the NOS RTV, but the NOS RTV and the Dutch Government regard this as a management fee. According to the VECAI it is a fee for intellectual property rights in disguise. |

5. COMMENTS FROM THE DUTCH AUTHORITIES (29)

|

(75) |

The Dutch authorities state that the Commission's assumption that the relevant measures are not part of the regular, annual financing of the public broadcasters as part of the state funding is erroneous. The financing which is the subject of the investigation stems from the regular financing mechanism and was an integral part of the budget planning which led to the payments to the public broadcasters. According to the authorities, the FOR, the matching funds, the CoBo Fund and the payments to the NOB are part of the regular, annual financing mechanism. |

|

(76) |

The Dutch authorities finally remind the Commission that the assessment should take into account the specific context in which the public service broadcasters operate. The authorities request the Commission to take into account the Amsterdam Protocol. If necessary, the subject of the present procedure should be qualified as compatible aid within the meaning of Article 86(2) of the EC Treaty, within the context of the principles laid down in the Amsterdam Protocol. |

|

(77) |

The amount provisionally indicated by the Commission as possible over-compensation is erroneous. This was inferred from the resources of funds which were wrongly qualified as reserves. Since the use of these funds is pre-determined and is subject to control there cannot be over-compensation. Moreover, the authorities argue that if the measures concerned are deemed to be state aid, the aid should be considered to be existing state aid within the meaning of Article 88(1) of the EC Treaty. |

|

(78) |

The Dutch authorities point out that the accounts of the individual public broadcasting associations have always been subject to approval by an independent accountant. |

|

(79) |

The Dutch authorities consider that broadcasts of popular and less popular sports fall within the definition of the main task of the public broadcasters. The Dutch authorities consider that, when determining their bid for transmission rights, public broadcasters did not pay more than was necessary to secure the acquisition of important rights in relation to their public service mission and overall programming. |

|

(80) |

The authorities reiterate that the public service mission of the NOB is part of the public broadcasting system. The fact that NOB does not charge the public broadcasters for the service it provides does not imply that aid is granted to the public service broadcasters. |

|

(81) |

The Dutch authorities state that, given that the commercial operators do not demand copyright payments from cable operators either, the NOS RTV could be said to be acting as a normal market operator in the circumstances of this particular market. |

III. ASSESSMENT OF THE MEASURES UNDER STATE AID RULES

6. EXISTENCE OF AID WITHIN THE MEANING OF ARTICLE 87(1) OF THE EC TREATY

|

(82) |

Article 87(1) of the Treaty lays down the following conditions for the presence of state aid. First, there must be an intervention by the State or through state resources. Second, it must confer an advantage on the recipient. Third, it must distort or threaten to distort competition. Fourth, the intervention must be liable to affect trade between Member States. |

6.1 Presence of state resources

6.1.1 Ad hoc

|

(83) |

The payments referred to in Articles 106a and 170c of the Media Act, which are categorized by the Commission as ad hoc payments, can be divided into matching fund payments, FOR payments and CoBo Fund payments. |

|

(84) |

In the case of the matching funds, money is first set aside within the AOR — which is a fund whose resources are owned by the State and managed by the Media Authority — for the purpose of matching certain types of higher than foreseen expenditure of public service broadcasters. In a second step, the state resources represented by the matching funds of the AOR are transferred to the NOS RTV. |

|

(85) |

The payments made by the FOR fund are considered state resources. Although the FOR is a fund administered and managed by the PO, the money comes from the AOR, which is part of the media budget. |

|

(86) |

More importantly, as described in section 2.3.3.2, the PO distributes the money on the basis of agreements that are made in advance on the use of FOR money. Although it is the PO which proposes how the money should be used, it is the Minister of Education, Science and Culture who ‘adopts the proposal’ and establishes for which purposes the money can be used. The PO can only take the decision to spend the money once the Minister has established the criteria for the distribution of the money. The PO has to take into account the rules laid down by the Minster. It can therefore be considered that the transfer of state resources takes place when the payments are made from the FOR to the individual broadcasters. This is a transfer of state resources, which is moreover imputable to the State (30). |

|

(87) |

In the period under investigation the public broadcasters received an amount of €191,2 million from the FOR and an amount of €[...] million from the matching funds. |

|

(88) |

The payments by the CoBo Fund are considered state resources. As described in paragraph 43, the money in the CoBo Fund comes from direct contributions from the media budget and the revenues generated by the copyright payments paid by Belgian and German cable operators for the distribution of the three Dutch channels in Belgium and Germany. The Commission takes the view that not only the direct contributions from the media budget, but also the copyright payments can be considered state resources. Indeed, the copyright payments should have been used to finance the public service costs of the broadcasters. Setting them aside in the CoBo Fund had the effect of increasing the need for public funding proportionally. The copyright payments are therefore equivalent to resources forgone by the State. |

|

(89) |

Moreover, although the CoBo Fund is owned and managed by a foundation (the board of which is governed by the public service broadcasters), the transfers from the CoBo Fund are only made available to the public service broadcasters under conditions which are determined by the State. |

|

(90) |

The public service broadcasters received an amount of €31,7 million from the CoBo Fund in the period under investigation. This is a transfer of state resources to the individual broadcasters. |

6.1.2 Free access to cable

|

(91) |

The ‘must carry’ obligation imposed on cable operators does not involve any transfer of state resources, nor can the forgone revenues of cable operators be regarded as constituting a transfer of state resources (31). The Commission has no information to suggest otherwise. Accordingly, the preliminary view that the measure does not constitute a state aid within the meaning of Article 87(1) of the EC Treaty can be confirmed. |

6.1.3 Free technical facilities from the NOB

|

(92) |

The public company NOB receives payments from the State for the services it is obliged to deliver to the public broadcasters. These payments involve the direct transfer of state resources. They ultimately benefit the public broadcasters who get the services free of charge (32). Indeed the Dutch authorities themselves have stated that the NOB simply acts as a ‘vehicle’ for transferring state funding to the public service broadcasters who receive the services of the NOB. |

6.2 Economic advantage

|

(93) |

The ad hoc financing (payments to FOR and via the matching funds), the transfers to the CoBo Fund and the provision of free technical facilities provide an economic advantage to the Dutch public service broadcasters, in the sense that these measures relieve them from operating costs that they would otherwise have to bear. |

6.2.1 Applicability of the Altmark judgment

|

(94) |

The Dutch Government and the public broadcasters have argued that the measures under investigation compensate the public broadcasters for the net costs of discharging their public service mission. This would imply that the measures would therefore not provide an advantage to public service broadcasters and not constitute aid, in line with the Altmark judgment (33). |

|

(95) |

State measures compensating for the net additional costs of a SGEI do not qualify as state aid within the meaning of Article 87(1) of the EC Treaty if the compensation is determined in such a way that a real advantage cannot be conferred on the undertaking. In the Altmark judgment the Court of Justice laid down the conditions that have to be satisfied for compensation not to be classified as state aid. These conditions are as follows:

|

|

(96) |

The Commission considers that in the present case the last three conditions set out in paragraph 95 are not fulfilled. First, the transfer of funds from the FOR, the matching funds and the financial contribution from the CoBo Fund to the public service broadcasters is not based on objective and transparent parameters established in advance. |

|

(97) |

Moreover, neither the ad hoc financing measures nor the payments from the CoBo Fund take into account all the relevant receipts of the public service broadcasters. Nor do they include the necessary safeguards to exclude over-compensation. Indeed, as will be assessed in more detail below, the ad hoc funding actually resulted in considerable over-compensation. |

|

(98) |

Finally, the Dutch public broadcasters were not chosen as providers of a SGEI on the basis of a tender, nor was any analysis carried out to ensure that the level of compensation was determined on the basis of an analysis of the costs which a typical undertaking, well run and adequately provided with the means of production so as to be able to meet the necessary public service requirements, would have incurred in discharging those obligations. The same is true of the financing of the technical facilities made available to the public service broadcasters by the NOB. |

|

(99) |

Consequently, the Commission considers that not all conditions set out in the Altmark judgment are fulfilled in this case. |

6.3 Distortion of competition

|

(100) |

The advantage provided by the ad hoc financing, the transfers to the CoBo Fund and the provision of free technical facilities to the Dutch public service broadcasters are not available to any other undertaking in a comparable situation. Given that competition is distorted whenever state aid reinforces the competitive position of the beneficiary undertaking vis-à-vis its competitors, the advantage is capable of distorting competition between the public service broadcasters and other undertakings (34). |

6.4 Affecting trade between Member States

|

(101) |

When state aid strengthens the position of an undertaking compared with other undertakings competing in intra-Community trade, the latter must be regarded as affected by that aid (35) even if the beneficiary undertaking is itself not involved in exporting (36). Similarly, where a Member State grants aid to undertakings operating in the service and distributive industries, the recipient undertakings need not themselves carry on their business outside the Member State for the aid to have an effect on Community trade (37). |

|

(102) |

In line with this case law the 2001 Communication from the Commission on the application of state aid rules to public service broadcasting (hereinafter: ‘the Broadcasting Communication’) (38) explains that: ‘Thus, state financing of public service broadcasters can generally be considered to affect trade between Member States. This is clearly the position as regards the acquisition and sale of programme rights, which often take place at an international level. Advertising, too, in the case of public broadcasters who are allowed to sell advertising space, has a cross-border effect, especially for homogeneous linguistic areas across national boundaries. Moreover, the ownership structure of commercial broadcasters may extend to more than one Member State (39).’ |

|

(103) |

In the present case, the Dutch public broadcasters are themselves active on the international market. Through their membership of the European Broadcasting Union they can exchange television programmes and participate in the Eurovision system. Moreover, their programmes are broadcast in Belgium and Germany. Furthermore, the Dutch public broadcasters are in direct competition with commercial broadcasters that are active on the international broadcasting market and that have an international ownership structure. |

|

(104) |

The Commission concludes on these grounds that the ad hoc financing, the funds provided to the CoBo Fund and the provision of free technical facilities are such as to affect trade between Member States within the meaning of Article 87(1) of the EC Treaty. |

6.5 Conclusion

|

(105) |

Since all conditions laid down in Article 87(1) of the EC Treaty are fulfilled and the conditions set out by the Court of Justice in the Altmark judgment have not been met in their entirety, the Commission concludes that the ad hoc financing (financing from FOR and the matching funds), the funds granted through the CoBo Fund and the provision of free technical services and facilities to the Dutch public broadcasters must be deemed to be state aid within the meaning of Article 87(1) of the EC Treaty. On the other hand, the advantage deriving from free access to the cable network does not involve a transfer of state resources and does not constitute state aid. |

7. CLASSIFICATION MEASURES AS ‘NEW’ AID

|

(106) |

Pursuant to Article 1(b) of the Council Regulation (EC) No 659/99 of 22 March 1999 laying down detailed rules for the application of Article 93 of the EC Treaty (40), ‘existing aid’ means, inter alia:

|

|

(107) |

As stated before, a distinction may be made between the annual payments, which are not the subject of this Decision, and the ad hoc payments. |

7.1 Annual payments

|

(108) |

The annual payment are made on the basis of Article 110 of the Media Act, which states that ‘entities which have been awarded time to broadcast are entitled to funding from the general budget’. The level of funding and the availability are laid down in the same Media Act. This system of funding existed prior to the entry into force of the Treaty and is regarded as existing aid, as acknowledged by the Commission in procedure E-5/2005 (41). |

7.2 payments

|

(109) |

The ad hoc payments possess a number of characteristics which distinguish them from the regular annual payments and argue against their classification as existing aid:

|

7.3 Free technical facilities

|

(110) |

The public service broadcasters have received free technical facilities from the NOB since the entry into force of the Media Act 1987. In that year the NOB started providing facilities to the public service broadcasters, whereas originally these facilities had been provided by the NOS. The NOB has been entrusted with a service of general economic interest. It provides the facilities to the individual public service broadcasters free of charge and receives payments from the State directly. This measure can thus also be considered to be a new aid measure. |

7.4 Conclusion on the classification as ‘new aid’

|

(111) |

The ad hoc financing (payments from the FOR to the individual public broadcasters and from the matching funds), the transfers from the CoBo Fund and the provision of free technical facilities should all be deemed to be new aid rather than existing aid. |

8. COMPATIBILITY OF THE AID UNDER ARTICLE 86(2) OF THE EC TREATY

|

(112) |

On the basis of the characteristics of the measures the only possible grounds for compatibility is Article 86(2) of the EC Treaty which states that: ‘undertakings entrusted with the operation of services of general economic interest (…) shall be subject to the rules contained in this Treaty, in particular to the rules on competition, insofar as the application of such rules does not obstruct the performance, in law or in fact, of the particular tasks assigned to them. The development of trade must not be affected to such an extent as would be contrary to the interests of the Community’. |

|

(113) |

The Court of Justice has consistently held that Article 86(2) of the EC Treaty may provide for a derogation from the ban on state aid for undertakings entrusted with a SGEI. The Court's Altmark judgment implicitly confirmed that state aid that compensates for the costs incurred by an undertaking for the provision of a SGEI can be found to be compatible with the common market if it meets the conditions of Article 86(2) of the EC Treaty (43). |

|

(114) |

In line with settled case-law of the Court of Justice (44), Article 86(2) of the EC Treaty constitutes a derogation that should be interpreted restrictively. The Court has made clear that, in order for a measure to qualify for such a derogation, all of the following conditions must be fulfilled:

|

|

(115) |

The Broadcasting Communication sets out the principles and methods which the Commission intends to apply in order to ensure that the conditions referred to above are complied with. It must therefore examine whether in the present case:

|

8.1 Definition

|

(116) |

In this context, it should be mentioned that the ad hoc financing and the free provision of technical facilities were designed to support activities which are part of the general public service remit. An assessment of the overall level of funding of the public service broadcasters is thus necessary, but, with the exception of the specific measures referred to above, this Decision does not intend to assess the mechanism and conditions under which state funding is provided. Nor does this Decision concern the organisation of the public service broadcasting system as a whole. |

|

(117) |

As stated in paragraph 33 of the Broadcasting Communication, it is for the Member States to define the public service remit of a public broadcaster. Given the specific nature of the broadcasting sector, however, the Commission considers ‘a “wide” definition entrusting a given broadcaster with the task of providing balanced and varied programming in accordance with its remit, to be legitimate under Article 86(2) EC, in view of the interpretative provisions of the Protocol. Such a definition would be consistent with the objective of fulfilling the democratic, social and cultural needs of a particular society and guaranteeing pluralism, including cultural and linguistic diversity’. |

|

(118) |

Although the definition may be broad, it should be sufficiently clear and precise to leave no doubt as to whether a given activity performed by the entrusted operator is intended by the Member State to be included in the public service remit or not. As stated in paragraph 36 of the Broadcasting Communication, the role of the Commission is limited to checking whether the public service definition in the broadcasting sector contains any manifest error. |

|

(119) |

The main task of the Dutch public broadcasters is to provide high quality and varied programmes for general broadcast on the public channels, in the general interest, as laid down in Article 13c of the Media Act. Specific programming requirements relating to the categories of content to be covered and the amount of broadcasting time to be devoted to each category are also contained in the legislation. |

|

(120) |

CLT-UFA stated that the Dutch public broadcasters broadcast too much sport in general and too much football in particular. The complainants claimed that the NOS RTV broadcasts the majority of all sports events in the Netherlands. As stated above, the ad hoc financing was intended to finance activities which are part of the general public service remit and were thus also meant for the acquisition of sports rights. |

|

(121) |

The Commission is of the opinion, however, that broadcasting sports programmes, within a limit of around 10 % of total broadcasting time, does not constitute a manifest error. Sports can be part of the broadcasters' public service mission, and devoting 10 % of broadcasting time to sports is not inconsistent with the remit of offering a balanced and varied public service programming mix. |

|

(122) |

The Commission is of the opinion that the main task, as defined in Article 13c(1) of the Media Act, is rather broadly defined, but can be considered to meet — in accordance with the wording of the Amsterdam protocol — the ‘democratic, social and cultural needs’ of Dutch society. Thus, the definition in the legislation is sufficiently clear and precise in relation to the main task, and does not contain any manifest errors. |

8.2 Entrustment

|

(123) |

Paragraph 40 of the Broadcasting Communication states that in order to benefit from the exemption under Article 86(2) of the EC Treaty, the public service remit should be entrusted to the Dutch public broadcasters by means of an official act. The Commission notes that the Media Act formally entrusts the NOS with the task of performing the public service task defined in Article 13c and the supporting legislation. The public broadcasters are given the right to broadcast programmes on the public channels by Article 31 of the Media Act, and the Commission considers that the main task of broadcasting programmes is clearly entrusted to the public broadcasters. |

8.3 Proportionality

|

(124) |

In Chapter 6.3 of the Broadcasting Communication, it is explained that the proportionality test that the Commission must carry out is twofold (45). |

|

(125) |

On the one hand, the Commission has to calculate the net cost of the public service task entrusted to the Dutch public broadcasters and verify whether or not this cost has been over-compensated. When compensating an undertaking, the state aid must not exceed the net costs of the public service mission. To arrive at the net cost, account should also be taken of other direct or indirect revenues derived from the public service mission. Therefore, the net benefit of the exploitation of the public service activities will be taken into account in assessing the proportionality of the aid. |

|

(126) |

On the other hand, the Commission has to investigate any information at its disposal suggesting that public broadcasters have distorted competition in commercial markets more than is necessary for the fulfilment of the public service mission. For example, a public service broadcaster, in so far as lower revenues would be covered by the state aid, might be tempted to depress prices of advertising or of other non-public service activities on the market, so as to reduce the revenue of competitors. Such a practice would require additional state funding to compensate for the revenues forgone from commercial activities and would therefore indicate the presence of over-compensation of public service obligations. |

8.3.1 Transparency and cost-allocation

|

(127) |

The Commission first needs to determine the cost of the SGEI. As the Dutch public broadcasters also carry out non-public service activities, they are required by Commission Directive 80/723/EEC of 25 June 1980 on the transparency of financial relations between Member States and public undertakings (46), as amended by Commission Directive 2000/52/EC (47), to keep separate accounts for the different activities carried out. Costs and revenues must be correctly assigned on the basis of clearly established, objective cost accounting principles. Costs that are entirely attributable to public service activities, while benefiting also commercial activities, need not be apportioned between the two and can be entirely allocated to public service (48). |

|

(128) |

The Transparency Directive has been implemented in the Netherlands through an amendment of the Competition Act (‘Mededingingswet’) (49). Moreover, a special Decree (50) obliges public broadcasters to keep separate accounts for all side activities and association activities. On the basis of this, the Dutch authorities have provided information on the costs and revenues of public broadcasters in the period 1994-2005. |

|

(129) |

Under the Transparency Directive, Member States are required to ensure not only that separate accounts are kept for public service and non-public service activities, but also that all costs and revenues are correctly allocated on the basis of consistently applied and objectively justifiable cost accounting principles and that the cost-allocation principles according to which the separate accounts are maintained are clearly established. |

|

(130) |

However, the Commission notes that the Decree does not determine how the public broadcasters have to allocate costs that are shared by the public service and the non-public service activities. Information from the Dutch authorities confirms, moreover, that the public broadcasters use different methods to allocate costs. The authorities argue that on an individual level the allocation is correct, but that due to the choices individual broadcasters make regarding the allocation, the allocation may differ from one broadcaster to the other. The Commission finds, however, that the fact that there is no consistency between the different broadcasters is an indication that the Decree does not sufficiently prescribe how the cost allocation should take place. |

|

(131) |

Therefore, on the basis of the information submitted by the Dutch authorities, it cannot be concluded that the costs are correctly allocated on the basis of accepted cost-allocation methods. Consequently, the Commission considers that all the net revenues of the commercial activities of the public service broadcasters should be taken into account in determining whether state funding has been proportional to the public service costs. This is also consistent with the Dutch legislative framework that applies to the public service broadcasting system and which obliges broadcasters to use for public service purposes all of their profits, including those from commercial activities (51). |

8.3.2 Proportionality of public funding

|

(132) |

According to paragraph 57 of the Broadcasting Communication, state aid must not exceed the net costs of the public service incurred by the broadcaster. Thus, after having determined the net costs of the public service it has to be established whether the total amount of state funding does not exceed this figure. |

|

(133) |

If a complete or meaningful cost allocation has not taken place, the net revenues of all the activities that have benefited directly or indirectly from public funding have to be taken into account for the calculation of the net public service costs (52). Only the revenues of the commercial ‘stand-alone’ activities do not have to be taken into account in establishing the net costs of the public service mission. These are activities which have not benefited directly or indirectly — for example by way of cheaper production inputs — from state funding or which have paid the full value of inputs which they share with or result from the public service activity. |

|

(134) |

In the Dutch public service broadcasting system, there is neither the concept of ‘stand-alone’ activities nor a meaningful and complete allocation of resources between different activities of broadcasters. Moreover, the Media Act stipulates that all the net revenues of main and side tasks (53), side activities and association activities (54) have to be used for the fulfilment of the public service mission (55). |

|

(135) |

Consequently, the net costs of the public service activities are determined by taking into account the revenues from all activities of the public service broadcasters. The calculation is therefore as follows:

|

|

(136) |

The sum of all the above items determines whether or not the total state funding exceeds the total net public service costs or, in other words, whether or not there has been over-compensation of the public service tasks. |

|

(137) |

As regards the free provision of technical services and facilities by the NOB, the measure should, in principle, be taken into account in the assessment of the over-compensation. However, it is not necessary to explicitly include the measure in the calculations, since the benefits from the free technical service can be considered to be compensating costs that would otherwise have had to be financed. Thus, having to pay the costs in question would have increased by the same amount the costs of the public service entrusted to the Dutch public broadcasters. The inclusion of these costs would therefore not alter the final net result (57). |

8.4 Decision to initiate the procedure and period under investigation

|

(138) |

In the decision to initiate the procedure, the Commission quantified over-compensation, on a preliminary basis, as €110 million. The calculation was based on incomplete figures on the actual amount of transfers to the reserves and of the level of reserves held by the public service broadcasting system as a whole during the years 1992-2002. The authorities had not at the time provided complete data on individual broadcasters. |

|

(139) |

After initiating the procedure the Commission received the cost and revenue figures of the individual broadcasters, which are more detailed than the overall figures provided at the time of the opening of the procedure. Moreover, the new information provides actual data up to 2005 and also includes an estimate for 2006. |

|

(140) |

This Decision concerns the ad hoc payments which were paid as of 1994 and covers the period up to 2005. As regards the end date, the Dutch authorities invited the Commission to take into account the figures from 2006 too. However, the Commission does not consider this to be appropriate, since figures from 2006 are only estimates for the ongoing budget year. |

8.4.1 Assessment of the compensation of the individual public service broadcasters

|

(141) |

It appears that 14 out of the 19 public service broadcasters were over-compensated in the period 1994-2005. The over-compensation generated €32 million profits, which were generally transferred to their programme reserves. |

|

(142) |

However, in some cases part of the over-compensation was used to balance under-compensation in the period before 1994. At the beginning of 1994 some broadcasters had a negative programme reserve (58). Broadcasters were only allowed to register negative programme reserves when the public service costs exceeded the various sources of public service funding. In other words, negative programme reserves could only result from under-compensation of public service costs. |

|

(143) |

On the other hand, any possible loss from commercial activities had to be financed through the association reserves and could not be reflected in the programme reserves. According to the Dutch authorities, the association reserves were built up with private funds. |

|

(144) |

There are also cases in which the under-compensation of public service costs was temporarily financed with association reserves. In 1993, the association reserves were ‘frozen’ by the Dutch authorities; as of that moment, revenues from public service and commercial activities could no longer be added to these association reserves. However, an exception was made for the reimbursement of payments made out of association reserves before 1994 to cover for unfunded public service costs. According to the Dutch authorities, this is the only circumstance in which funds were still added to these reserves after 1994 (59). |

|

(145) |

The Commission considers that the negative amounts recorded in the programme reserves and the positive variations of association reserves after 1994 only occurred as a result of previous ‘under-compensation’ of public service costs. The consequent balancing of these sums is therefore considered to constitute eligible costs of the public service task. The corresponding amounts therefore do not have to be taken into account for the establishment of the over-compensation. |

|

(146) |

As stated in paragraph 141, the over-compensation generally flowed into the programme reserves. In 2005 the PO decided for the first time, on the basis of Article 19a(1)h and Article 109a of the Media Act, that reserves held by the individual broadcasters in excess of 5-10 % of their annual budget should be transferred to the PO (60). This transfer is also considered part of the ad hoc measures and is taken into account in determining the proportionality of the compensation. As a result, this transfer has reduced the overall compensation of the individual public service broadcasters, while increasing the over-compensation of the PO. |

|

(147) |

By subtracting — for each year from 1994 to 2005 — the net cost of the public service from the overall funding received from the State, in the way described in section 8.3.2, the Commission comes to the conclusion that none of the individual broadcasters has received public funding in excess of 10 % of its annual budget. Since the costs of public broadcasting may vary every year, the State may indeed wish for budgetary reasons to keep the fluctuations in state financing to a minimum and permit a certain percentage of the annual over-compensation to be carried forward to the next year. The Commission recognised this principle in the Danish public broadcasting case (61). |

|

(148) |

In the Danish state aid case the Commission stated that these reserves must be established for a specific purpose and that they must be regularised on a fixed date, i.e. being deducted from the next year's compensation if over-compensation has been found. Thus, if the over-compensation does not exceed 10 % of the amount of the annual compensation, such over-compensation is compatible with the EC Treaty and may be carried forward to the next annual period and deducted from the amount of compensation payable in respect of that period. |

|

(149) |

The Dutch authorities have decided that each individual public service broadcaster can only maintain a dedicated reserve of a maximum of 5-10 % of its annual budget (62). In view of this constraint, the PO ordered the transfer of €42,457 million of reserves from the individual broadcasters to the PO in 2005. The authorities have also committed themselves to carrying out regular monitoring of the reserves and ordering the reimbursement of the excess amounts above 10 % of the annual compensation as of 2006 (63). The Commission therefore considers that the conditions are fulfilled for accepting as compatible an amount of over-compensation provided that this does not exceed 10 % of the annual budget of the public service broadcasters (64). |

|

(150) |

Since the over-compensation does not exceed the 10 % margin of the annual budget, it can therefore be considered justified for the fulfilment of the public service mission and the aid is thus considered compatible with Article 86(2) of the EC Treaty. |

8.4.2 Over-compensation of the PO

|

(151) |

The PO has also received compensation for its role in managing and coordinating the broadcasting system. The PO performs this role as a separate organisation, which, internally, keeps separate accounts. The Dutch authorities have stated that although the NOS RTV and the PO are parts of a single legal entity and also present consolidated accounts, under no circumstances could they have access to each other's funds. |

|

(152) |

On the basis of the separate accounts for the PO and according to the accounting method described above, the Commission concludes that the PO has received a total over-compensation of €55,908 million, not including the reserves which were transferred in 2005 from individual broadcasters. The transfer of the reserves amounted to €42,457 million. When this transfer is taken into account, the total over-compensation of the PO amounts to €98,365 (€55,908 + €42,457) million. Table 4: Overview of annual funding of PO (1994-2005) amounts x €1 million (65)

|

|

(153) |

In the Commission's view, the over-compensation of €98,365 million is not necessary for the functioning of the public service and it cannot, therefore, benefit from the Article 86(2) derogation from the prohibition on state aid. The over-compensation is consequently not considered compatible aid and should in principle be recovered from the PO. |

|

(154) |

Nevertheless, it appears that the over-compensation exceeds the total ad hoc payments accrued to the PO. The PO has received €33,870 million as ad hoc payments from the State's media budget, plus the ad hoc transfer of €42,457 million from the other broadcasters. This gives a total of €76,327 million of payments received from ad hoc measures. In addition, the ad hoc payments have also generated interest, which should be taken into account in determining the amount of funds which were not received in the context of the ‘existing aid measures’. The recovery would, therefore, have to be capped at €76,327 million plus interest, because the ‘remaining’ over-compensation was granted through existing aid and cannot be recovered. |

8.5 Anti-competitive behaviour on commercial markets

|

(155) |

As explained in the Broadcasting Communication, the Commission is of the opinion that anti-competitive conduct by public service broadcasters cannot be considered necessary for the fulfilment of the public service mission. In the decision to initiate the formal investigation procedure the Commission mentioned the following possible market distortions: |

8.5.1 Cable transmission

|

(156) |

The model contract concluded between broadcasters and cable operators in 1985 stipulates, at the request of the Dutch government, that cable operators do not pay any intellectual property rights for transmission of Dutch public television programmes. It is legitimate to question whether, by forgoing intellectual property rights payments from cable operators, the PO acted as a normal market operator, since it waived commercial income. |

|

(157) |

The Dutch authorities argue, however, that the fact that the PO does not claim a fee for intellectual property rights is not necessarily contrary to market behaviour. After all, commercial broadcasters do not require a fee from the cable operators for the transmission of their programmes either (66). |

|

(158) |

Indeed, the commercial agreements between the broadcasters and the cable operators can take various forms, particularly in view of the fact that the transaction involves an exchange of transmission services for availability of content, which is valuable to both parties. The Commission finds accordingly that there are no clear indications that the PO acted contrary to market behaviour and that by renouncing commercial revenues it increased the need for state funding. |

8.5.2 Advertising market

8.5.2.1 Alleged undercutting of prices for GRP 20-49

|

(159) |

At the opening of the formal investigation procedure, the Commission did not have sufficient evidence that the STER had actually undercut prices. Nevertheless, the information which was submitted after the opening of the investigation by the complainants and the Dutch authorities has to be assessed. |

|

(160) |

Paragraph 58 of the Broadcasting Communication indicates that public service broadcasters might be tempted to depress the prices of advertising so as to reduce the revenue of competitors. However, one should keep in mind that the public broadcasters in the Netherlands do not directly carry out advertising activities, but the advertising activities are carried out by a separate organisation, the STER. According to its mission statement, the STER must exploit the time available for advertising in such a way as to deliver an optimal contribution to the central financing of the public service broadcasters. It functions as an intermediary, with the job of maximising profits from the sale of the advertising space of the public broadcasters. As already mentioned in paragraph 17, the STER transfers the advertising revenues directly to the media budget. |

|

(161) |

Any undercutting behaviour by the STER might be inferred from some or all of the following circumstances: STER's prices being lower than its competitors', an increase in market share and loss of revenues for the STER. |

|

(162) |

First, as the Commission also indicated in the decision to open the formal investigation procedure, a comparison between the prices of the public and private advertising sales companies could be regarded as a meaningful measure of the criteria set out in paragraph 58 of the Broadcasting Communication. |

|

(163) |

In order to compare prices, the target group of 20-49 year-olds is the most relevant one. As can be inferred from Table 5, there are different sub-groups, many of which target viewers in the 20-49 age range: Table 5: Percentage of target GRP's (gross rating points) acquired by the STER in 2004

|

|||||||||||||||||||||||||||||||||

|

(164) |

Table 5 indicates that the STER predominantly sells advertising for viewers. Since 1999, the STER's market share in advertising and the audience reached by the public service broadcasters for the target group aged 20-49 has decreased. The gross prices charged to the advertisers for the 20-49 target group were as follows: Table 6: Gross prices per GRP for the target group of 20-49 year-olds (18.00h - 24.00h), 1995 - 2005 in €

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

(165) |

On the basis of the data provided above, the STER's list prices for GRP for the 20-49 target group have been only slightly lower than the commercial broadcaster's list prices. According to the Dutch authorities the broadcasters and the STER grant quite substantial discounts. The commercial broadcasters seem to have granted much higher discounts, especially since 1998. These discounts are listed below: Table 7: Actual discounts granted in 1994-2005 in %

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

(166) |

Even though the STER has a less attractive audience than the commercial broadcasters — it has a low selectivity and is thus less able to offer a very specific target group — and has a lower audience and advertising market share (see Table 9 below), its net prices are higher than those charged by the commercial broadcasters. Table 8: Net prices per GRP for the target group of 20-49 year-olds (18.00h - 24.00h), 1995 - 2005 in €

|

|

(167) |

From Table 9 it can, moreover, be inferred that there is a clear correlation between the decrease in audience share and advertising share for the public broadcasting service. There is no evidence that the STER is increasing its market share by possible price dumping, or even maintaining its market share despite the decrease in the audience share of its client broadcasters. On the contrary, the STER is losing advertising market share at a similar pace as the public service broadcasters are losing audience. Table 9: Audience and advertising market shares

|

|||||||||||||||||||||||||||||||||||||||||||||

|

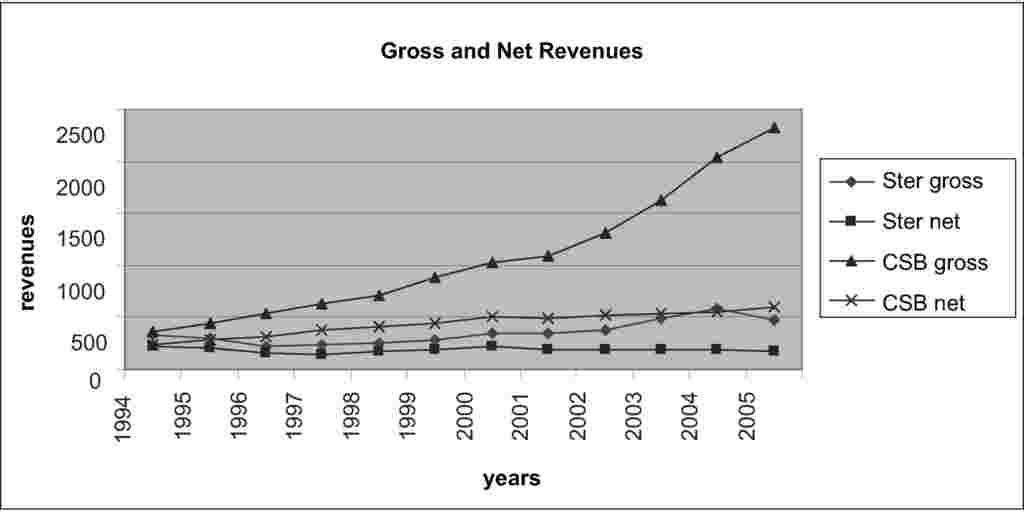

(168) |

Finally, there is no evidence of the STER losing advertising revenues in order to increase its market share. Figure 1: Development of gross and net revenues

|

|

(169) |