ISSN 1977-091X

Official Journal

of the European Union

C 209

English edition

Information and Notices

Volume 62

20 June 2019

|

ISSN 1977-091X |

||

|

Official Journal of the European Union |

C 209 |

|

|

|

||

|

English edition |

Information and Notices |

Volume 62 |

|

Contents |

page |

|

|

|

II Information |

|

|

|

INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES |

|

|

|

European Commission |

|

|

2019/C 209/01 |

||

|

2019/C 209/02 |

Non-opposition to a notified concentration (Case M.9323 — RheinEnergie/SPIE/TankE) ( 1 ) |

|

|

2019/C 209/03 |

Non-opposition to a notified concentration (Case M.9363 — Koito/Elbit/BWV/JV) ( 1 ) |

|

|

IV Notices |

|

|

|

NOTICES FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES |

|

|

|

European Commission |

|

|

2019/C 209/04 |

||

|

|

NOTICES CONCERNING THE EUROPEAN ECONOMIC AREA |

|

|

|

EFTA Surveillance Authority |

|

|

2019/C 209/05 |

No state aid within the meaning of Article 61(1) of the EEA Agreement |

|

|

V Announcements |

|

|

|

PROCEDURES RELATING TO THE IMPLEMENTATION OF THE COMMON COMMERCIAL POLICY |

|

|

|

European Commission |

|

|

2019/C 209/06 |

||

|

2019/C 209/07 |

||

|

|

PROCEDURES RELATING TO THE IMPLEMENTATION OF COMPETITION POLICY |

|

|

|

European Commission |

|

|

2019/C 209/08 |

Prior notification of a concentration (Case M.9314 — Sogeclair/AddUp/PrintSky) — Candidate case for simplified procedure ( 1 ) |

|

|

2019/C 209/09 |

Prior notification of a concentration (Case M.9382 — Toyota Financial Services Corporation/Mazda Motor Corporation/SMM Auto Finance JV) — Candidate case for simplified procedure ( 1 ) |

|

|

|

|

|

(1) Text with EEA relevance. |

|

EN |

|

II Information

INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES

European Commission

|

20.6.2019 |

EN |

Official Journal of the European Union |

C 209/1 |

COMMUNICATION FROM THE COMMISSION

Guidelines on non-financial reporting: Supplement on reporting climate-related information

(2019/C 209/01)

|

Important notice This communication has been prepared pursuant to Article 2 of Directive 2014/95/EU of the European Parliament and of the Council (1) in order to assist companies concerned to disclose non-financial information in a relevant, useful, consistent and more comparable manner. It is a supplement to the Guidelines on Non-Financial Reporting adopted by the Commission in 2017 (C(2017) 4234 final). This communication provides non-binding guidelines, and does not create new legal obligations. To the extent that this communication may interpret Directive 2014/95/EU, the Commission's position is without prejudice to any interpretation of this Directive that may be issued by the Court of Justice of the European Union. Companies using these guidelines may also rely on international, EU-based or national frameworks. This communication does not constitute a technical standard, and neither preparers of non-financial statements nor any party, whether acting on behalf of a preparer or otherwise, may claim that non-financial statements are in conformity with this document. |

Contents

|

1. |

Introduction | 2 |

|

1.1. |

Why provide new guidelines on climate-related disclosures? | 2 |

|

1.2. |

Benefits for reporting companies | 3 |

|

2. |

How to use these guidelines | 3 |

|

2.1. |

General considerations | 3 |

|

2.2. |

Materiality | 4 |

|

2.3. |

Climate-related risks, dependencies, and opportunities | 5 |

|

2.4. |

Structure of the proposed disclosures | 8 |

|

2.5. |

Consistency with recognised reporting frameworks and standards | 8 |

|

3. |

Recommended disclosures and further guidance | 8 |

|

3.1. |

Business Model | 8 |

|

3.2. |

Policies and Due Diligence Processes | 9 |

|

3.3. |

Outcomes | 10 |

|

3.4. |

Principal Risks and their Management | 11 |

|

3.5. |

Key Performance Indicators | 12 |

|

Annex I: |

Further guidance for banks and insurance companies | 21 |

|

Annex II: |

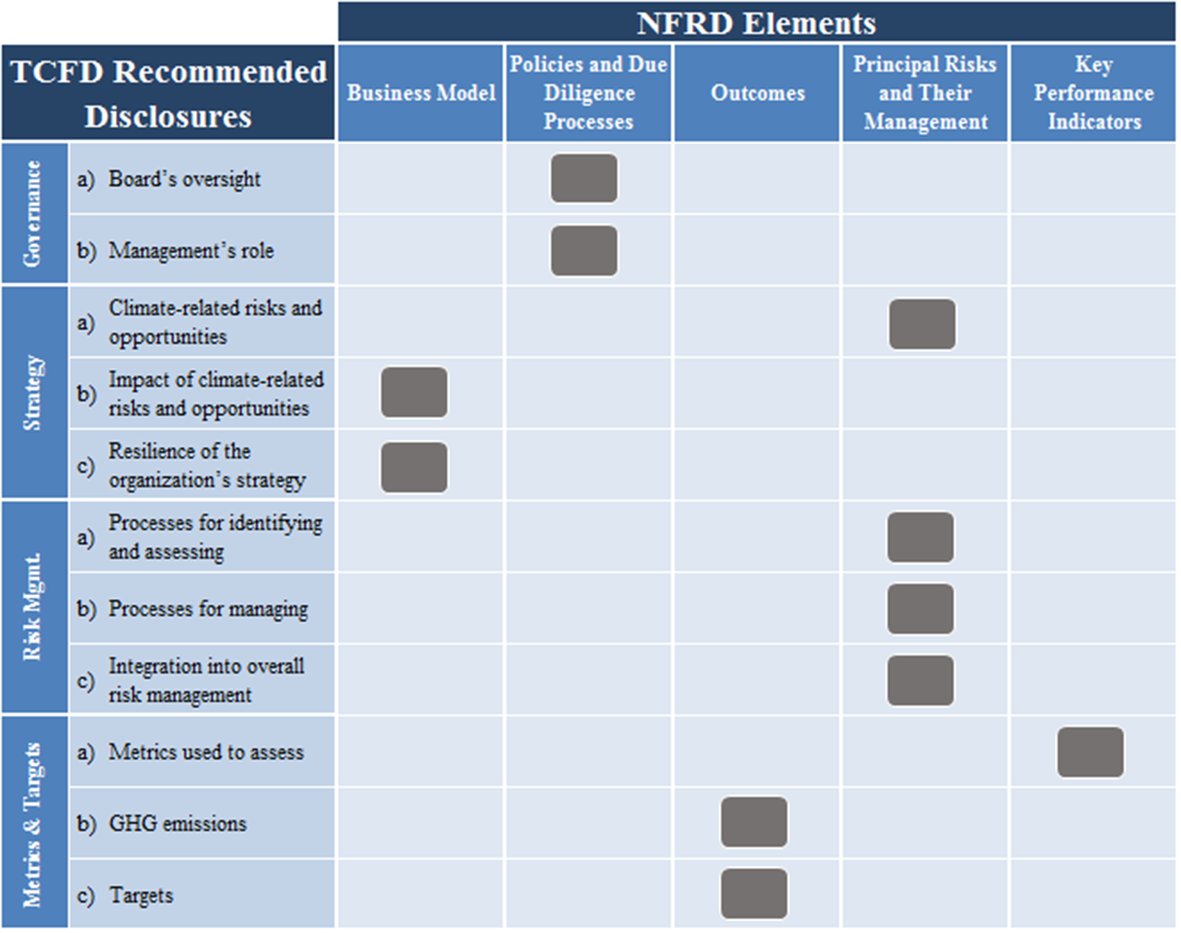

Mapping of Non-Financial Reporting Directive Requirements and TCFD Recommended Disclosures | 29 |

1. INTRODUCTION

1.1. Why provide new guidelines on climate-related disclosures?

The 2015 Paris Agreement on Climate Change, the United Nations’ Sustainable Development Goals and the Special Report of the Intergovernmental Panel on Climate Change (October 2018) all call for accelerated and decisive action to reduce greenhouse gas (GHG) emissions and to create a low-carbon and climate-resilient economy. The EU has agreed ambitious targets for 2030 regarding GHG emission reductions, renewable energy and energy efficiency (2), and has approved rules on GHG emissions from land use as well as emissions targets for cars and vans. In 2018 the Commission published its strategic long-term vision for a prosperous, modern, competitive and climate-neutral economy by 2050 (3).

Companies and financial institutions have a critical role to play in the transition to a low-carbon and climate-resilient economy. Firstly, an additional annual investment of EUR 180 billion is already needed to meet the EU’s energy and climate 2030 targets, and further funds will be needed to achieve climate neutrality by 2050. Many of these investments represent significant business opportunities, and much of the funding will need to come from private capital. Secondly, companies and financial institutions need to better understand and address the risks of a negative impact on the climate resulting from their business activities, as well as the risks that climate change poses to their business. Weather-related disasters caused a record EUR 283 billion in economic damages in 2017 and could affect up to two-thirds of the European population by 2100 compared with 5 % today. Better disclosure of climate-related information by companies can contribute to the implementation of the Sendai Framework for Disaster Risk Reduction 2015-2030, which calls for governments to evaluate, record, share and publically account for disaster losses.

In March 2018 the Commission published the Action Plan on Financing Sustainable Growth, with the aim of reorienting capital towards sustainable investment, managing financial risks that arise from climate change and other environmental and social problems, and fostering transparency and long-termism in financial and economic activity (4). The publication of new guidelines on the disclosure of climate-related information by companies is part of the Action Plan.

A number of other actions in the Action Plan depend to some extent on companies disclosing adequate sustainability-related information. This includes, for example, the proposed regulations on the establishment of a framework (taxonomy) to facilitate sustainable investment (5), on sustainability disclosures by institutional investors and asset managers (6), and on carbon-related benchmarks (7).

Without sufficient, reliable and comparable sustainability-related information from investee companies, the financial sector cannot efficiently direct capital to investments that drive solutions to the sustainability crises we face, and cannot effectively identify and manage the risks to investments that will arise from those crises.

Corporate disclosure of climate-related information has improved in recent years. However, there are still significant gaps, and further improvements in the quantity, quality and comparability of disclosures are urgently required to meet the needs of investors and other stakeholders.

In June 2017, the Task Force on Climate-related Financial Disclosures (TCFD), established by the G20’s Financial Stability Board, published recommendations to encourage financial institutions and non-financial companies to disclose information on climate-related risks and opportunities (8). The TCFD recommendations are widely recognised as authoritative guidance on the reporting of financially material climate-related information, and the Commission encourages companies to implement them. A number of governments and financial regulators around the world have expressed support for the recommendations and are integrating them into their guidance and policy frameworks. Examples include Australia, Canada, Hong Kong, Japan, Singapore and South Africa, as well as some EU Member States.

This supplement integrates the TCFD recommendations, and provides guidance to companies that is consistent with the Non-Financial Reporting Directive and the recommendations of the TCFD.

The Technical Expert Group on Sustainable Finance, appointed by the Commission in June 2018, provided recommendations on climate-related disclosures and these guidelines are built on those recommendations. These guidelines take account of stakeholder feedback on the recommendations of the Technical Expert Group on Sustainable Finance, and of the results of a targeted online consultation carried out by the services of the European Commission in February-March 2019 (9).

1.2. Benefits for reporting companies

Better disclosure of climate-related information can have benefits for the reporting company itself, such as:

|

— |

increased awareness and understanding of climate-related risks and opportunities within the company, better risk management, and more informed decision-making and strategic planning; |

|

— |

a more diverse investor base and a potentially lower cost of capital, resulting for example from inclusion in actively managed investment portfolios and in sustainability-focused indices, and from improved credit ratings for bond issuance and better credit worthiness assessments for bank loans; |

|

— |

more constructive dialogue with stakeholders, in particular investors and shareholders; |

|

— |

better corporate reputation and maintenance of social licence to operate. |

2. HOW TO USE THESE GUIDELINES

2.1. General considerations

Companies should read this supplement together with the relevant national legislation transposing the Non-Financial Reporting Directive (2014/95/EU), and if necessary the text of the Directive itself.

They should also consider the Non-Binding Guidelines on Non-Financial Reporting published by the Commission in June 2017 (10), which contain 6 key principles for good non-financial reporting, namely that disclosed information should be: (1) material; (2) fair, balanced and understandable; (3) comprehensive but concise; (4) strategic and forward-looking (11); (5) stakeholder-oriented; and (6) consistent and coherent. Those principles and the other sections of the Non-Binding Guidelines all apply as appropriate to this supplement.

Companies are also encouraged to read the recommendations of the Task Force on Climate-related Financial Disclosures, and if relevant the supplementary guidance for the financial sector and for companies operating in the sectors of energy, transport, material and buildings, and agriculture, food and forest products (12).

Like the general guidelines published in 2017, this supplement on climate-related reporting is non-binding. Companies may chose alternative approaches to the reporting of climate-related information, provided they meet legal requirements.

These guidelines recognise that the content of climate-related disclosures may vary between companies according to a number of factors, including the sector of activity, geographical location and the nature and scale of climate-related risks and opportunities.

Methodologies and best practice in the field of climate-related reporting are evolving fast. These guidelines therefore recognise that a flexible approach is necessary. Companies and other organisations are strongly encouraged to continue to innovate and further improve climate-related reporting beyond the content of these guidelines. Companies should also ensure that their approach to climate-related reporting is regularly updated in line with the latest scientific evidence.

It is not the intention of these guidelines to encourage stand-alone climate reporting. Companies are encouraged to integrate climate-related information with other financial and non-financial information as appropriate in their reports.

The default location for the non-financial statement according to the Non-Financial Reporting Directive is the company’s management report, although many Member States have taken up the option of allowing companies to publish their non-financial statement in a separate report. The TCFD proposes that its recommended disclosures should be included in the company’s mainstream “annual financial filings” (13).

Companies should in any case seek to ensure that climate-related information is easily accessible for intended users. If companies make cross-references to other reports or documents, this should be done in a simple and user-friendly way, for instance, by applying a practical rule of “maximum one ‘click’ out of the report”.

These guidelines are intended for use by companies that fall under the scope of the Non-Financial Reporting Directive (14). However, they may also be useful for other companies that wish to disclose climate-related information.

2.2. Materiality

According to the Non-Financial Reporting Directive, a company is required to disclose information on environmental, social and employee matters, respect for human rights, and bribery and corruption, to the extent that such information is necessary for an understanding of the company’s development, performance, position and impact of its activities (15). Climate-related information can be considered to fall into the category of environmental matters.

As indicated in the Commission’s 2017 Non-Binding Guidelines on Non-Financial Reporting, the reference to the “impact of [the company’s] activities” introduced a new element to be taken into account when assessing the materiality of non-financial information. In effect, the Non-Financial Reporting Directive has a double materiality perspective:

|

— |

The reference to the company’s “development, performance [and] position” indicates financial materiality, in the broad sense of affecting the value of the company. Climate-related information should be reported if it is necessary for an understanding of the development, performance and position of the company. This perspective is typically of most interest to investors. |

|

— |

The reference to “impact of [the company’s] activities” indicates environmental and social materiality. Climate-related information should be reported if it is necessary for an understanding of the external impacts of the company. This perspective is typically of most interest to citizens, consumers, employees, business partners, communities and civil society organisations. However, an increasing number of investors also need to know about the climate impacts of investee companies in order to better understand and measure the climate impacts of their investment portfolios. |

Companies should consider using the proposed disclosures in these guidelines if they decide that climate is a material issue from either of these two perspectives.

These two risk perspectives already overlap in some cases and are increasingly likely to do so in the future. As markets and public policies evolve in response to climate change, the positive and/or negative impacts of a company on the climate will increasingly translate into business opportunities and/or risks that are financially material.

The materiality perspective of the Non-Financial Reporting Directive covers both financial materiality and environmental and social materiality, whereas the TCFD has a financial materiality perspective only.

Figure 1

The double materiality perspective of the Non-Financial Reporting Directive in the context of reporting climate-related information

When assessing the materiality of climate-related information, companies should consider a longer-term time horizon than is traditionally the case for financial information. Companies are advised not to prematurely conclude that climate is not a material issue just because some climate-related risks are perceived to be long-term in nature.

When assessing the materiality of climate-related information, companies should consider their whole value chain, both upstream in the supply-chain and downstream.

Given the systemic and pervasive impacts of climate change, most companies under the scope of the Directive are likely to conclude that climate is a material issue. Companies that conclude that climate is not a material issue are advised to consider making a statement to that effect, explaining how that conclusion has been reached.

2.3. Climate-related risks, dependencies, and opportunities

Climate-related risks

Under the Non-Financial Reporting Directive, climate-related information should, to the extent necessary, include both the principal risks to the development, performance and position of the company resulting from climate change, and the principal risks of a negative impact on the climate resulting from the company’s activities. The proposed disclosures in these guidelines reflect both these risk perspectives.

Unless otherwise stated in the text, references to risks should be understood to refer both to risks of negative impacts on the company (transition risks and physical risks — see below) and to risks of negative impacts on the climate.

Both of these kinds of risk — risks of negative impacts on the company and risks of negative impacts on the climate — may arise from the companies own operations and may occur throughout the value chain, both upstream in the supply-chain and downstream.

(1) Risks of negative impacts on the climate

Some examples of risks of negative impacts on the climate are:

|

— |

A company’s industrial production facility might directly emit greenhouse gases (GHGs) into the atmosphere. |

|

— |

The energy that a company buys to run its operations might have been produced from fossil fuels. |

|

— |

The product that a company makes might require the consumption of fossil fuels, for example in the case of cars that run on petrol or diesel. |

|

— |

The production of materials used by the company might result in GHG emissions upstream in their value chain. This may be the case for companies that use materials such as cement or aluminium in their production processes. Similarly, a company producing or processing forest or agricultural commodities, including in sectors such as food, apparel, or wood processing industries, could potentially be causing, directly or indirectly, land-use change including deforestation and forest degradation and related GHG emissions. |

(2) Risk of negative impact on the company

The risks of climate change for the financial performance of the company can be classified as physical risks or transition risks (16).

Transition risks are risks to the company that arise from the transition to a low-carbon and climate-resilient economy. They include:

|

— |

Policy risks, for example as a result of energy efficiency requirements, carbon-pricing mechanisms which increase the price of fossil fuels, or policies to encourage sustainable land use. |

|

— |

Legal risks, for example the risk of litigation for failing to avoid or minimise adverse impacts on the climate, or failing to adapt to climate change. |

|

— |

Technology risks, for example if a technology with a less damaging impact on the climate replaces a technology that is more damaging to the climate. |

|

— |

Market risks, for example if the choices of consumers and business customers shift towards products and services that are less damaging to the climate. |

|

— |

Reputational risks, for example the difficulty of attracting and retaining customers, employees, business partners and investors if a company has reputation for damaging the climate. |

Generally speaking, a company with a higher negative impact on the climate will be more exposed to transition risks.

Physical risks are risks to the company that arise from the physical effects of climate change (17). They include:

|

— |

Acute physical risks, which arise from particular events, especially weather-related events such as storms, floods, fires or heatwaves, that may damage production facilities and disrupt value chains. |

|

— |

Chronic physical risks, which arise from longer-term changes in the climate, such as temperature changes, rising sea levels, reduced water availability, biodiversity loss and changes in land and soil productivity. |

The exposure of a company to physical risks does not directly depend on whether or not that company has a negative impact on the climate.

Dependencies on natural, human and social capitals

Many companies are dependent on natural capital (18). If the natural capital itself is threatened by climate change then the company will be exposed to climate-related risks, especially physical risks. Companies should therefore carefully consider their natural capital dependencies when identifying and reporting on their climate-related risks. For example, an agricultural production company may be dependent on various natural capitals such as water, biodiversity, and land and soil productivity, all of which are vulnerable to climate change. Such a company would be expected to explain these dependencies when reporting on its climate-related risks.

Many companies are also dependent on human and social capital, such as the skills and motivation of employees, and the level of trust the company enjoys amongst external stakeholders. Companies should integrate information on human and social capital as appropriate in their reporting on climate-related issues. For example, employees may be critical to the development of innovative low-carbon products and services.

Climate-related opportunities

Climate-related risks can often be converted into opportunities by companies offering products and services that contribute to climate change mitigation or adaptation.

Climate change adaptation means anticipating the adverse effects of climate change and taking appropriate action to prevent or minimise the damage they can cause. It includes business opportunities such as new technologies to use scarce water resources more efficiently, or the building of new flood defences.

Climate change mitigation refers to efforts to reduce or prevent GHG emissions. Examples of business opportunities associated with mitigation include renewable energy or the development of more energy efficient buildings and transport systems.

The taxonomy of sustainable economic activities, proposed by the Commission as part of the Action Plan on Financing Sustainable Growth, aims to identify and classify climate-related opportunities.

Figure 2 shows the relationship between climate-related risks and opportunities.

Figure 2

Climate-related risks and opportunities

Climate-related risks and opportunities throughout the value chain

When reporting on their climate-related risks, dependencies and opportunities, companies should, where relevant and proportionate, consider their whole value chain, both upstream and downstream. For companies involved in manufacturing activities this means following a product life cycle approach that takes account of climate issues in the supply chain and the sourcing of raw material, as well as during the use of the product and when the product reaches end-of-life. Companies providing services, including financial services, will also need to consider the climate impacts of the activities that they support or facilitate.

When SMEs are part of the value chain, companies are encouraged to support them in providing the required information

2.4. Structure of the proposed disclosures

These guidelines propose climate-related disclosures for each of the five reporting areas listed in the Non-Financial Reporting Directive: (a) business model (b) policies and due diligence (c) outcome of policies (d) principal risks and risk management and (e) key performance indicators.

For each reporting area, the guidelines identify a limited number of recommended disclosures. A company should consider using the recommended disclosures to the extent that they are necessary for an understanding of its development, performance, position and impact of its activities.

Further guidance is provided after the recommended disclosures for each reporting area. The further guidance consists of suggestions for more detailed information that companies may consider including as part of the recommended disclosures. In addition, further guidance is provided for banks and insurance companies in Annex I.

When deciding whether and to what extent they use the recommended disclosures and the more detailed suggestions included under further guidance, including the further guidance for banks and insurance companies in Annex I, companies should take account of the principles of good non-financial reporting contained in the Commission’s 2017 Non-Binding Guidelines on Non-Financial Reporting, including the principles about disclosed information being: material; fair, balanced and understandable; and comprehensive but concise.

The scale of climate-related risks and opportunities that the company identifies will be an important factor in deciding whether and to what extent they use the recommended disclosures and the further guidance.

2.5. Consistency with recognised reporting frameworks and standards

Companies are encouraged to disclose information in accordance with widely accepted reporting standards and frameworks to maximise comparability for their stakeholders. To contribute to convergence at EU and global level, these guidelines refer to a number of recognised reporting frameworks and standards.

In particular, they incorporate the recommended disclosures of the Task-Force on Climate-related Financial Disclosures (TCFD), which are themselves aligned with other principal frameworks. The disclosures recommended by the TCFD are separately identified in these guidelines. Annex II shows the disclosure requirements of the Non-Financial Reporting Directive mapped against the recommended disclosures of the TCFD.

In addition to the TCFD, these guidelines also take particular account of the standards and frameworks developed by the Global Reporting Initiative (GRI), the CDP, the Climate Disclosure Standards Board (CDSB), the Sustainability Accounting Standards Board (SASB) and the International Integrated Reporting Council (IIRC) and of the EU Eco-Management and Audit Scheme (EMAS) (19).

3. RECOMMENDED DISCLOSURES AND FURTHER GUIDANCE

3.1. Business Model

It is very important for stakeholders to understand the company’s view of how climate change impacts its business model and strategy, and how its activities can affect the climate, over the short, medium and long term. To adequately report on climate-related matters, companies will need to take a longer term perspective than they normally do for financial reporting.

The climate-related risks and opportunities of a company will depend on the type of its activity, its geographic locations and its positioning in the transition to a low-carbon and climate-resilient economy.

To appropriately incorporate the potential effects of climate change into their planning processes, companies should consider how climate-related risks and opportunities may evolve and their potential business implications under different conditions. One way to assess such implications is through the use of scenario analysis.

Companies that do not appropriately consider their business model and strategy in light of climate change may both cause negative effects on the climate and experience negative impacts on their business such as on the profit and loss statement, financing, future regulatory burden, and “licence to operate”. On the other hand, identifying new climate-related opportunities may strengthen the business model and earnings outlook of a company.

Table 1

Disclosure on Business Model

|

Describe the impact of climate-related risks and opportunities on the company's business model, strategy and financial planning. [Covers TCFD recommendation Strategy b)] |

|

Describe the ways in which the company’s business model can impact the climate, both positively and negatively. |

|

Describe the resilience of the company’s business model and strategy, taking into consideration different climate-related scenarios over different time horizons, including at least a 2 °C or lower scenario and a greater than 2 °C scenario (20). [Covers TCFD recommendation Strategy c)] |

Further guidance:

|

— |

Describe any changes in the company’s business model and strategy to address transition and physical risks and to take advantage of climate-related business opportunities. |

|

— |

Describe the company’s dependencies on natural capitals, such as water, land, ecosystems or biodiversity that are at risk because of climate change. |

|

— |

Describe how any changes in the company’s business model and strategy to address climate change mitigation and/or adaptation will change the company’s human capital needs. |

|

— |

Describe opportunities related to resource efficiency and cost savings, the adoption of low-emission energy sources, the development of new products and services, access to new markets, and building resilience along the value chain. |

|

— |

Disclose how the company has selected scenarios. |

|

— |

Describe how the company’s activities contribute to climate change via GHG emissions, including from deforestation, forest degradation or land-use change. |

3.2. Policies and Due Diligence Processes

Governance and control systems are key to stakeholders’ understanding of the robustness of a company’s approach to climate-related issues. Information on the involvement of the board and management, in particular their respective responsibilities in relation to climate change, informs stakeholders on the level of the company’s awareness of climate-related issues. When describing the role of the board, the company may wish to make a reference to any corporate governance statement that it is required to publish.

Stakeholders may also be interested in the company’s policies and any associated targets that demonstrate its commitment to climate change mitigation and adaptation, and in its due diligence processes. This will help stakeholders to understand the company’s ability to manage its business to minimise climate-related risk, limit negative impacts on the climate and maximise positive impacts throughout the value chain.

Policies and processes addressing climate-related topics may be separate from or integrated into other policies and operational processes. Due diligence processes that take climate into account, for example, might be integrated into the company’s risk management framework. The company may want to explain its approach to managing climate-related issues and the rationale for choosing that approach.

Table 2

Disclosure on Policies and Due Diligence Processes

|

Describe any company policies related to climate, including any climate change mitigation or adaptation policy. |

|

Describe any climate-related targets the company has set as part of its policies, especially any GHG emissions targets, and how company targets relate to national and international targets and to the Paris Agreement in particular. |

|

Describe the board’s oversight of climate-related risks and opportunities. [Covers TCFD recommendation Governance a)] |

|

Describe management’s role in assessing and managing climate-related risks and opportunities and explain the rationale for the approach. [Covers TCFD recommendation Governance b)] |

Further guidance:

|

— |

Describe the company’s engagement with its value chain on climate-related issues, explaining how it engages with upstream and downstream partners to promote climate mitigation and/or adaptation. |

|

— |

Explain how climate-related issues are integrated into the company’s operational decision-making processes. |

|

— |

Describe any public policy engagement on climate-related issues undertaken by the company, including membership of any relevant organisations or interest groups. |

|

— |

Describe whether, how and at what levels (in particular board and management) the company has access to expertise on climate-related issues, either from its own internal capacity and/or from external sources. |

|

— |

Describe any employee policies that are related to the climate, for example investments in skills necessary for the transition to low-carbon technologies, or measures to ensure employees can perform theirs tasks safely in a changing climate. |

|

— |

Describe whether and how the company’s remuneration policy takes account of climate-related performance, including performance against targets set. |

|

— |

Disclose any energy-related targets the company has set as part of its policies (see Section 3.5). |

|

— |

Explain the reasoning behind the selection of any climate-related targets used by the company. |

|

— |

In the case of land sector companies, describe any targets related to GHG “sinks” (GHG absorption). |

3.3. Outcomes

Disclosure of climate-related policy outcomes helps stakeholders monitor and assess a company’s development, position, performance and impact as a result of its policies. In assessing its performance through target setting and reporting against the targets, the company demonstrates the consistency of its strategy, actions, and decisions related to climate change.

Quantitative aspects, such as indicators supporting the analyses, are covered in Section 3.5 Key Performance Indicators of these guidelines.

Table 3

Disclosure on Outcomes

|

Describe the outcomes of the company's policy on climate change, including the performance of the company against the indicators used and targets set to manage climate-related risks and opportunities. [Covers TCFD Metrics and targets c)]. |

|

Describe the development of GHG emissions against the targets set and the related risks over time. [Covers TCFD Metrics and targets b)]. |

Further guidance:

|

— |

Describe how the performance of the company with regard to climate influences its financial performance, where possible with reference to financial KPIs. |

3.4. Principal Risks and their Management

It is very important for investors and other interested stakeholders to know how the company identifies climate-related risks, the principal risks it has identified, and how it manages those risks.

Disclosures on risks should include risks of the company having a negative impact on the climate and risks of climate change having a negative impact on the company (transition and physical risks), and whether and how the two are linked. Companies are advised to take account of the risk definitions given in Section 2.3 when deciding what information to disclose regarding risks.

When disclosing information about climate-related risks, companies should consider longer-term time horizons than they traditionally use for financial risks.

Gaps in data and methodologies may in some cases make it difficult to present quantitative information about climate-related risks, especially regarding longer time horizons. In such cases, companies are encouraged to present qualitative information until these data and methodological issues are adequately addressed.

Table 4

Disclosure on Principal Risks and Their Management

|

Describe the company’s processes for identifying and assessing climate-related risks over the short, medium, and long term and disclose how the company defines short, medium, and long term (21). [Covers TCFD recommendation Risk management a)] |

|

Describe the principal climate-related risks the company has identified over the short, medium, and long term throughout the value chain, and any assumptions that have been made when identifying these risks. [Covers TCFD recommendation Strategy a)]. This description should include the principal risks resulting from any dependencies on natural capitals threatened by climate change, such as water, land, ecosystems or biodiversity. |

|

Describe processes for managing climate-related risks (if applicable how they make decisions to mitigate, transfer, accept, or control those risks), and how the company is managing the particular climate-related risks that it has identified. [Covers TCFD recommendation Risk management b)] |

|

Describe how processes for identifying, assessing, and managing climate-related risks are integrated into the company’s overall risk management. [Covers TCFD recommendation Risk management c)]. An important aspect of this description is how the company determines the relative significance of climate-related risks in relation to other risks. |

Further guidance:

|

— |

Describe any climate adaptation measures undertaken by the company as part of its risk management process. |

|

— |

Give a detailed breakdown of principal climate-related risks by business activity. |

|

— |

Give a detailed breakdown of principal climate-related risks by geographical location. |

|

— |

Identify the locations that are critical to value chains, including operations, suppliers and markets. |

|

— |

Describe how the company sets and applies limits to climate-related risks, including any triggers used to escalate issues to management attention. |

|

— |

Describe the processes for prioritising climate-related risks, including any thresholds applied and indicate which risks across the value chain are considered most significant. |

|

— |

Categorise the principal risks of climate change on the financial performance of the company according to whether they are transition risks (policy, legal, technological, market and reputational risks) or physical risks (acute and chronic risks). |

|

— |

Disclose any risk mapping that includes climate-related issues. |

|

— |

Provide definitions of risk terminology used or references to existing risk classification frameworks used. |

|

— |

Describe the frequency of reviews and analyses with regard to risk identification and assessment. |

|

— |

Describe the linkages between principal climate-related risks and financial KPIs. |

|

— |

Disclose how scenarios and/or internal carbon pricing are used for risk management actions such as mitigation, transfer or adaptation. |

|

— |

Disclose the financial impacts of extreme weather events, including possible indicators on days of business interruptions and associated costs, cost of repairs, fixed-asset impairment, value chain disruptions and lost revenues. |

|

— |

Describe how the company’s performance is affected by weather variability, in particular for companies sensitive to variability in temperature and precipitation. |

3.5. Key Performance Indicators

According to the Non-Financial Reporting Directive, companies should disclose key performance indicators relevant to their particular business. They should consider using indicators to support their other climate-related disclosures, such as those related to outcomes or principal risks and their management, and to allow for aggregation and comparability across companies and jurisdictions. Indicators should be integrated with other disclosures to support and explain the narrative. However, it is also considered good practice to publish an additional table that presents all indicators in one place.

To meet the expectations of the TCFD, companies should disclose indicators and targets used by the company to assess climate-related risks and opportunities in line with their strategy and risk management processes [Covers TCFD recommendation Metrics and targets a)].

The robustness and reliability of data is key to be able to use the information in decision-making processes. Where not apparent, companies should provide a description of and any changes in the methodologies used to calculate or estimate the indicators.

Recommended indicators (22)

Subject to the company’s materiality assessment and in order to facilitate greater comparability of disclosures of non-financial information by companies, companies should consider disclosing the indicators in this section.

GHG emissions

This section contains four different indicators on GHG emissions: direct GHG emissions; indirect GHG emissions from the generation of acquired and consumed electricity, steam, heat, or cooling; all other indirect GHG emissions that occur in the value chain of the reporting company; and GHG absolute emissions target. Companies that decide to use any or all of these indicators should:

|

— |

calculate their GHG emissions in line with the GHG Protocol methodology or the ISO 14064-1:2018 standard and, where appropriate, with the Commission Recommendation 179/2013 for common methods on measuring GHG performance following a lifecycle approach (Organisation Environmental Footprint and Product Environmental Footprint). This will allow for aggregation and comparability across companies and jurisdictions; |

|

— |

indicate the third-party verification/assurance status that applies to their reported scope 1, scope 2 and scope 3 GHG emissions. |

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||||

|

Direct GHG emissions from sources owned or controlled by the company (Scope 1) |

Metric tons CO2e (23) |

270 900 tCO2e |

This KPI ensures companies are accurately measuring their carbon footprints from direct emissions. |

TCFD Metrics and Targets, CDP Climate Change Questionnaire, GRI 305, CDSB Framework, SASB, EMAS |

EU emissions trading system (ETS) 2030 climate & energy framework |

||||

|

Further guidance:

|

|||||||||

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||||

|

Indirect GHG emissions from the generation of acquired and consumed electricity, steam, heat, or cooling (collectively referred to as “electricity”) (Scope 2) |

Metric tons CO2e |

632 400 tCO2e |

This KPI ensure companies are measuring emissions from purchased or acquired electricity, steam, heat, and cooling. |

TCFD Metrics and Targets, CDP Climate Change Questionnaire, GRI 305, CDSB Framework, EMAS |

2030 climate & energy framework |

||||

|

Further guidance:

|

|||||||||

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||||

|

All indirect GHG emissions (not included in scope 2) that occur in the value chain of the reporting company, including both upstream and downstream emissions (Scope 3) |

Metric tons CO2e |

4 383 000 tCO2e |

For most companies, the majority of emissions occur indirectly from value chain activities. This KPI helps to gauge the thoroughness of companies’ accounting processes and to understand how companies are analysing their emissions footprints. |

TCFD Metrics and Targets, CDP Climate Change Questionnaire, GRI 305, CDSB Framework, EMAS |

2030 climate & energy framework |

||||

|

Further guidance:

|

|||||||||

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||||||||||

|

GHG absolute emissions target |

Metric tons CO2e achieved or % reduction, from base year |

20 % reduction in absolute emissions, equivalent to a 1 500 000 tCO2e reduction by 2025 from 2018 base year |

Target setting provides direction and structure to environmental strategy. This KPI helps to understand companies' commitments to reducing emissions and whether the company has a goal towards which it is harmonising and focusing emissions-related efforts. |

TCFD Metrics and Targets, CDP Climate Change Questionnaire, GRI 103-2 and 305, CDSB Framework, SASB, EMAS |

2030 climate & energy framework |

||||||||||

|

Further guidance:

|

|||||||||||||||

Energy

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||||||

|

Total energy consumption and/or production from renewable and non-renewable sources |

MWh |

292 221 MWh consumed from renewable sources; 1 623 453 MWh consumed from non-renewable sources |

Energy consumption and production accounts for an important proportion of GHG emissions. |

TCFD Metrics and Targets, CDP Climate Change Questionnaire, GRI 302, CDSB Framework, SASB, EMAS |

2030 climate & energy framework; Energy Efficiency Directive |

||||||

|

Further guidance:

|

|||||||||||

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||

|

Energy efficiency target |

Percentage |

6,5 % improvement by 2025 from 2018 base year for product, output or activity. |

This KPI helps data users understand the companies’ ambition to use energy more efficiently, which can reduce its energy costs and lower GHG emissions. It provides further background as to how the company aims to achieve its emissions reduction targets. |

TCFD Metrics and Targets, CDP Climate Change Questionnaire, GRI 103-2 and 302, SASB, EMAS |

2030 climate & energy framework; Energy Efficiency Directive |

||

|

Further guidance:

|

|||||||

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||

|

Renewable energy consumption and/or production target |

% increase of the proportion of renewable energy consumed / produced from base year |

13 % increase of the proportion of renewable energy consumed by 2025 from 2018 base year |

This KPI helps data users understand the companies’ ambition to produce or consume energy with lower GHG emissions. |

TCFD Metrics and Targets, CDP Climate Change Questionnaire, GRI 103-2 and 302, EMAS |

2030 climate & energy framework; Renewable Energy Directive |

||

|

Further guidance:

|

|||||||

Physical risks

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||

|

Assets committed in regions likely to become more exposed to acute or chronic physical climate risks |

Percentage |

15 % of book value of exposed real assets |

Extreme weather events can result in interruptions to or limitations on production capacity or early curtailment of operating facilities. The value of assets in areas exposed to increased weather informs the potential implications for asset valuation. It is important to observe this KPI in conjunction with disclosures regarding the company’s adaptation strategies and policies. |

TCFD Metrics and Targets, all 450a.1 SASB codes within select industries |

EU Adaptation Strategy |

||

|

Further guidance:

|

|||||||

Products and services

|

KPI |

Unit of Measure |

Example |

Rationale |

EU Policy Reference |

||

|

Percent turnover in the reporting year from products or services associated with activities that meet the criteria for substantially contributing to mitigation of or adaptation to climate change as set out in the Regulation on the establishment of a framework to facilitate sustainable investment (EU taxonomy). And / or Percent investment (CapEx) and/or expenditures (OpEx) in the reporting year for assets or processes associated with activities that meet the criteria for substantially contributing to mitigation of or adaptation to climate change as set out in the Regulation on the establishment of a framework to facilitate sustainable investment (EU taxonomy). |

Percentage |

12,5 % (turnover) from products or services associated with activities that substantially contribute to mitigation of or adaptation to climate change 8 % (CapEx) in products associated with activities that substantially contribute to mitigation of or adaptation to climate change |

These KPIs provide useful information to investors who are interested in companies whose products and services substantially contribute to mitigation of or adaptation to climate change whilst not significantly harming any other of the EU’s environmental objectives. |

Proposed Regulation on the establishment of a framework to facilitate sustainable investment Commission action plan on financing sustainable growth |

||

|

Further guidance:

|

||||||

Green Finance

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

||||||

|

Climate-related Green Bond Ratio: Total amount of green bonds outstanding (at year-end) divided by (a 5-year rolling average of) total amount of bonds outstanding and / or, Climate-related Green Debt Ratio: Total amount of all green debt instruments outstanding (at year-end) divided by (a 5-year rolling average of) total amount of all debt outstanding. |

Percentage |

20 % of bonds |

This KPIs helps companies communicate how their low-carbon transition plan is supported by debt financing activities and how capital is raised for existing and new projects with climate benefits. |

ISO/CD 14030-1 Green bonds -- Environmental performance of nominated projects and assets (DRAFT) |

Commission action plan on financing sustainable growth |

||||||

|

Further guidance:

|

|||||||||||

In addition to the above indicators, companies should also consider the following:

|

— |

Sector-specific indicators relevant for the particular industry. Companies from sectors including but not limited to energy, transportation, materials, real estate, and agriculture should refer to the TCFD’s supplemental guidance for non-financial groups and other climate-related reporting frameworks to ensure comparability of reported KPIs across sectors and companies (25). |

|

— |

Indicators on related environmental issues. Companies whose business models are dependent on natural capitals threatened by climate change may need to disclose indicators related to those natural capitals (e.g. water, soil productivity or biodiversity). Companies with adverse impacts on the climate as a result of land-use change including deforestation and forest degradation should consider disclosing indicators on these matters (26). |

|

— |

Indicators on related human capital and social issues, such as training and recruitment of employees. |

|

— |

Indicators related to opportunities. Companies engaging with a transition to a low-carbon and climate-resilient economy, aligned with key EU policies (27), carrying out climate change mitigation / adaptation activities that could translate into opportunities for the company should consider disclosing KPIs that reflect such efforts. Examples of these could be revenues from low-carbon products, revenues from product or services applying to the circular economy model, and R&D expenditures in circular economy production. |

(1) OJ L 330, 15.11.2014, p. 1.

(2) https://ec.europa.eu/clima/policies/strategies/2030_en

(3) https://ec.europa.eu/clima/policies/strategies/2050_en

(4) https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52018DC0097

(5) https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52018PC0353

(6) https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52018PC0354

(7) https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52018PC0355

(8) https://www.fsb-tcfd.org/

(9) https://ec.europa.eu/info/consultations/finance-2019-non-financial-reporting-guidelines_en

(10) OJ C 215, 5.7.2017, p. 1.

(11) This does not prevent appropriate consideration of commercially-sensitive information. Relevant information may be provided in broader terms that still convey useful information to investors and other stakeholders and meets the overall transparency objective.

(12) https://www.fsb-tcfd.org/wp-content/uploads/2017/12/FINAL-TCFD-Annex-Amended-121517.pdf

(13) See Annex II “Mapping of Non-Financial Reporting Directive Requirements and TCFD Recommended Disclosures”.

(14) Large public interest entities according to Directive 2013/34/EU with more than 500 employees.

(15) Article 19a (1) of Directive 2013/34/EU (introduced by Directive 2014/95/EU, the Non-Financial Reporting Directive).

(16) This description of transition and physical risks is to a large extent based on the report of the Task Force on Climate-related Financial Disclosures.

(17) Further guidance on reporting physical risks can be found in Advancing TCFD Guidance on Physical Climate Risks and Opportunities, EBRD and Global Centre of Excellence on Climate Adaptation

https://www.physicalclimaterisk.com/media/EBRD-GCECA_draft_final_report_full.pdf

(18) Further explanation and guidance regarding natural capital is available from the Natural Capital Coalition https://naturalcapitalcoalition.org/

(19) The Corporate Reporting Dialogue is undertaking work to better align the climate-related disclosures of the IIRC, SASB, GRI, CDP and CDSB. Companies are advised to take account of this work when it is complete.

(20) Companies are encouraged to consider a 1,5 °C scenario, in light of the conclusions of the IPCC 2018 Special Report. For further information on how to conduct a scenario analysis to assess the strategic resilience of a company, see TCFD’s Technical Supplement “The Use of Scenario Analysis in Disclosure of Climate-related Risks and Opportunities”

https://www.fsb-tcfd.org/wp-content/uploads/2017/06/FINAL-TCFD-Technical-Supplement-062917.pdf

(21) The definition of short, medium and long term is likely to depend on the company’s business model and the life cycle of its assets and liabilities.

(22) To enhance usability, in this section relevant further guidance is provided immediately after each recommended indicator.

(23) A carbon dioxide equivalent or CO2 equivalent (CO2e) is a metric measure used to compare the emissions from various greenhouse gases on the basis of their global-warming potential, by converting amounts of other gases to the equivalent amount of carbon dioxide with the same global warming potential.

(24) Definition of “renewable energy” from the CDP Climate Change Reporting Guidance 2018.

(25) TCFD (2017): Implementing the Recommendations of the Task-Force on Climate-related Financial Disclosures, https://www.fsb-tcfd.org/wp-content/uploads/2017/06/FINAL-TCFD-Annex-062817.pdf Other reporting standards and frameworks providing industry-specific KPIs on climate-related issues include the CDP Climate Change, Water Security and Forests Questionnaires, the GRI 305: Emissions 2016 and GRI 302: Energy 2016 standards or the SASB industry standards.

(26) Additional guidance can be found in The Natural Capital Protocol Toolkit https://naturalcapitalcoalition.org/protocol-toolkit/ and in the Commission Recommendation 179/2013 for common methods on measuring GHG performance following a lifecycle approach (Organisation Environmental Footprint and Product Environmental Footprint).

(27) Such as the Circular Economy Package, the Renewable Energy Directive, the Energy Efficiency Directive, the EU Emission Trading Scheme or the Clean Transport Package. For more details, see https://ec.europa.eu/clima/policies/strategies/2050_en

ANNEX I

Further guidance for banks and insurance companies

The requirements of the Non-Financial Reporting Directive apply to large listed companies, banks, and insurance companies. The Directive imposes the same requirements on all companies under its scope, regardless of the sector in which they operate. It therefore does not impose additional requirements on banks and insurance companies compared to other companies.

The proposed disclosures in Section 3 are for all companies that fall under the scope of the Non-Financial Reporting Directive, regardless of their sector of activity, including banks and insurance companies. Banks and insurance companies should look at the recommended disclosures under Section 3 from the particular perspective of their business activities, including lending, investing, insurance underwriting, and asset management activities (1). This annex aims to help banks and insurance companies in this exercise, and contains further guidance for them to consider using, where proportionate, when disclosing the information recommended under Section 3.

This annex does not address other financial sector companies, such as asset management companies or pension funds, because they do not fall under the scope of the Non-Financial Reporting Directive. Such companies may nevertheless find some of the proposed disclosures in this annex useful.

The Action Plan on Financing Sustainable Growth places a particular emphasis on the systemic importance of the financial sector in enabling the transition to a low-carbon and climate-resilient economy. Unlike most other companies, banks and insurance companies are both providers and users of climate-related information. Banks and insurance companies may exacerbate climate-related risks if their investments and insurance underwriting policies support economic activities that contribute to climate change via GHG emissions, including from deforestation, forest degradation or land-use change. Conversely, they can promote the transition to a low-carbon and climate resilient economy and increase awareness of the transition by integrating an evaluation of the potential impact on climate change of their prospective investments, loans, and insurance contracts into their policies and procedures.

Where appropriate the further guidance set out below makes a distinction between disclosures that may be relevant to all banks and insurance companies, and disclosures that would only be relevant to a particular business activity (lending, investing, insurance underwriting or asset management).

1. Business Model

Banks and insurance companies should consider including the following information as part of the recommended disclosures on Business Model under Section 3:

|

— |

How climate-related risks and opportunities of the investment, lending and insurance underwriting portfolios might affect the financial institution’s business model. |

|

— |

Whether and how the institution takes into consideration that its counterparties take climate-related risks and opportunities into account. |

|

— |

How the assessment of climate-related risks and opportunities are factored into relevant investment, lending and insurance underwriting strategies and how each strategy might be affected by the transition to a lower-carbon economy. |

|

— |

Insurance underwriting activities: how the potential impacts from climate change could influence policyholder, ceding company, reinsurer and their selection by the insurance company. |

2. Policies and Due Diligence Processes

Banks and insurance companies should consider including the following information as part of the recommended disclosures on Policies and due diligence processes under Section 3:

|

— |

How the financial institution encourages better disclosure and practices related to climate-related risks to improve data availability and any effort to increase the awareness of counterparties, and more generally of customers, of the relevance of climate-related issues as part of their lending, investment, and insurance underwriting processes, including for example by means of specialty climate-related risk advisory services. |

|

— |

Any stewardship activities related to the financial institution’s climate strategy such as engagements with companies, outcomes, and proxy voting (e.g. resolutions filed or supported). |

|

— |

Any investment, lending and insurance underwriting portfolio contributing to climate change mitigation and adaptation and any relevant target in this respect, e.g. in terms of insurance revenues related to energy efficiency and low carbon technology. |

|

— |

Investment activities: how climate-related issues are considered as drivers of value in the financial institution’s investment decision process. |

|

— |

Insurance underwriting activities: whether specific climate-related products are under development, such as the underwriting of risks of green infrastructure and nature-based solutions (2). |

|

— |

Insurance underwriting activities: whether any of the company’s life products incorporate climate considerations in the modelling of biometric risks (Life). |

|

— |

Insurance underwriting activities: whether the insurance company is part of public-private partnerships to promote awareness raising about climate-related risks, disaster risk resilience and/or climate adaptation investments. |

|

— |

Asset management activities: how climate-related considerations are embedded in suitability assessments in order to understand customers’ preferences and awareness regarding climate-related risks and opportunities. |

|

— |

Asset management activities: how the financial institution ensures that its climate-related performance is aligned with the climate strategy of its clients. |

|

— |

Asset management activities: the targets associated with climate-related exposure of assets under management across asset classes (e.g. equity / bonds / infrastructure / real estate / structured products / MBS / derivatives). |

3. Outcomes

Banks and insurance companies should consider including the following information as part of the recommended disclosures on Outcomes under Section 3:

|

— |

The development trend of the amount of carbon-related assets in the different portfolios against any relevant target set and the related risks over time. |

|

— |

The development trend of the weighted average carbon intensity for the different portfolios against any relevant target set and the related risks over time. Financial institutions should disclose the changes in the sector and geographic allocation of their investments compared to the previous reporting year and explain the impact of these changes on the average weighted carbon intensity of their portfolios. |

4. Risks and Risk management

Banks and insurance companies should consider including the following information as part of the recommended disclosures on Risks and risk management under Section 3:

|

— |

Whether risk management processes, including internal stress testing, consider climate-related risks. |

|

— |

Any exposures in the different lending, investment and underwriting activities to sectors perceived as contributing to climate change, which might create reputational risks for the financial institution. |

|

— |

The climate-related risks identified in the different lending, investment or underwriting activities and how the financial institution assesses and manages those risks. |

|

— |

The exposure of financial assets, non-financial assets and assets under management to principal climate-related risks and provide with a breakdown of those risks in physical and transition risks. |

|

— |

How the financial institution has assessed the exposure of financial assets and non-financial assets to climate-related risks under different climate-related scenarios. |

|

— |

Characterisation of their climate-related risks in the context of traditional industry risk categories such as credit risk, market risk and operational risk (3). |

|

— |

How climate-related risks could affect overall solvency needs of insurance companies and banks’ present and future regulatory capital requirements. For that purpose, banks may use the outcomes of their own internal capital adequacy assessment process (see Article 73 of Directive 2013/36/EU), and insurance companies may use the results of the calculations carried-out in their Own Risk and Solvency Assessments (see Article 45 of Directive 2009/138/EC and Article 262 of Commission Delegated Regulation (EU) 2015/35), and the outcome of stress testing and sensitivity analysis (see Article 295.6 of Commission Delegated Regulation (EU) 2015/35), in particular when those techniques make use of climate-related data (4). |

|

— |

Lending activities: volume of the collateral highly exposed to climate-related risks and the impact of the selected scenarios on its value. |

|

— |

Lending activities: volume of real estate collateral by energy efficiency rating according to energy performance certificates. In particular, volume of real estate collaterals highly exposed to transition risk, including collateral with the lowest energy efficiency ratings in comparison to total collaterals. |

|

— |

Lending activities: volume of real estate collaterals highly exposed to physical risk in comparison to total collaterals. |

|

— |

Insurance underwriting activities: processes for identifying and assessing climate-related risks on re-/insurance by geography, business division, or product segments. |

|

— |

Insurance underwriting activities: mitigating actions, such as reinsurance treaties or hedging strategies put in place by the institution to reduce climate-related risks and the effect of any change in such techniques. |

|

— |

Insurance underwriting activities: the amount of carbon-related underwriting exposures in terms of insurance revenues. |

5. KPIs

In disclosing indicators related to GHG emissions, banks and insurance companies should focus on their Scope 3 GHG emissions, despite the well-known challenges. Scope 1 and Scope 2 GHG emissions (direct emissions and indirect emissions from the generation of purchased energy) are likely to be small when compared to other indirect emissions (Scope 3).

Where relevant and proportionate, the reported Scope 3 GHG emissions of banks and insurance companies should include not only their counterparties’ Scope 1 and 2 emissions, but also their counterparties’ Scope 3 emissions. When SMEs are part of the value chain, banks and insurance companies are encouraged to support them in providing the required information.

When disclosing key performance indicators relevant to their particular business and in supporting their other qualitative climate-related disclosures, as recommended under Section 3, banks and insurance companies should consider disclosing the following indicators:

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

|

Amount or percentage of carbon-related assets in each portfolio in MEUR or as a percentage of the current portfolio value (5). |

M in reporting currency / percentage |

EUR 20 m or 20 % carbon-related assets of bank’s equity portfolio |

Show awareness of the exposure of portfolio to sectors affected to varying degrees by climate-related risks and opportunities. |

TCFD Common Carbon Footprinting and Exposure Metrics |

2030 climate & energy framework |

|

Weighted average carbon intensity of each portfolio, where data are available or can be reasonably estimated (6). |

tCO2e/M revenues in reporting currency |

A bank reports the carbon intensity of its equity portfolio in terms of tCO2e per EUR m using third-party carbon data. |

Show awareness of the exposure of portfolio to sectors affected to varying degrees by climate-related risks and opportunities. |

TCFD Common Carbon Footprinting and Exposure Metrics |

2030 climate & energy framework |

|

Volume of exposures by sector of counterparty. |

Reporting currency % of the total risk exposure |

EUR 1 250 m in energy sector accounting for 17 % of total investments |

Show the concentration of exposures towards high-carbon and low-carbon sectors. |

|

EU Low Carbon Economy Roadmap |

Lending and Investment Activities

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

|

Credit risk exposures and volumes of collateral by geography/country of location of the activity or collateral, with an indication of those countries/geographies highly exposed to physical risk. |

Reporting currency |

EUR 750 m |

Show the concentration of exposures and collateral in countries and geographies highly exposed to physical risks. |

|

EU Low Carbon Economy Roadmap |

|

Volume of collaterals related to assets or activities in climate change mitigating sectors. |

% of the total volume of collaterals |

12 % of collaterals |

Show the volume of green collaterals, e.g. with lower carbon exposure. |

|

2030 climate & energy framework |

|

Volume of financial assets funding sustainable economic activities contributing substantially to climate mitigation and/or adaptation (absolute figures and compared to total exposures) according to the EU taxonomy. |

Reporting currency % of the total risk exposure |

EUR 650 m accounting for 12 % of lending portfolio |

Show the concentrations of green investments and their resilience to climate change. |

|

EU Low Carbon Economy Roadmap |

|

Total amount of the fixed income portfolios invested in green bond certified according to a potential EU Green Bond Standard if and when such a standard is approved, or according to any other broadly recognised green bond framework (at year-end) divided by (a 5-year rolling average of) total amount of holdings in fixed income portfolios. |

Percentage and total amount in -Reporting currency |

Green bonds compared to vanilla bonds underwritten or emitted |

This indicator demonstrates commitment to green finance and the investor’s strategy and transition path towards alignment with a well below 2 °C scenario. It helps demonstrate track-record and forward-looking data can underpin the investor’s transition strategy with a robust key-performance indicator. |

The proposed draft version of ISO 14030 (October 2018) on green bonds already requires reporting on this indicator. |

Upcoming EU eco-label on green financial products (7). |

Insurance underwriting activities

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

|

Breakdown of underwriting exposure by lines of business to economic sectors (life / non-life / reinsurance). |

Reporting currency |

Amount and % of net premiums written and of technical provisions as in Directive 2009/138/EC deriving from infrastructure insurance from policyholders in the energy sector. |

Demonstrate awareness of current economic exposure and concentration (if any) in industries that are impacted by climate change in varying degrees. |

EU Taxonomy SASB Directive 2009/138/EC (Solvency II) |

2030 climate & energy framework |

|

Percentage of products incorporating climate-related risks into the underwriting process for individual contracts (life / non-life / reinsurance). |

0-100 % |

Products could be related to a specific type of risk or to a segment of the clientele with particular exposure to climate risks. |

Demonstrate product portfolio resilience to climate change. |

SASB |

2030 climate & energy framework |

|

Number and value of climate-related underwriting products offered (Non-life / reinsurance). The company has developed a specific offering for geographic areas particularly exposed to extreme weather events, and discloses quantitative information around the uptake of the product. |

Reporting currency Number |

The company has developed a specific offering for geographic areas particularly exposed to extreme weather events, and discloses quantitative information around the uptake of the product. |

Demonstrate ability to capture opportunities deriving from climate change mitigation and adaptation. |

N/A |

2030 climate & energy framework EU Adaptation Strategy |

|

Maximum Expected Loss from natural catastrophes caused by climate change (life / non-life / reinsurance). |

Reporting currency |

A company discloses its Net Maximum Expected Loss by peril and region Based on Occurrence Exceedance Probability (OEP) in billion EUR. Perils include hurricanes, floods, wildfires and droughts. |

Demonstrate risk management maturity and business resilience to adverse conditions. |

SASB FN-IN-450a.1, AODP ASTM |

2030 climate & energy framework EU Adaptation Strategy |

|

Total losses attributable to insurance payouts from (1) expected natural catastrophes and (2) non-expected natural catastrophes, by type of event and geographic segment (net and gross of reinsurance). |

Reporting currency |

A company discloses the key results of its natural catastrophe risk management. |

Demonstrate risk management maturity and business resilience to adverse conditions. |

SASB FN-IN-450a.2, GRI 201-2 |

2030 climate & energy framework |

Asset Management activities

|

KPI |

Unit of Measure |

Example |

Rationale |

Alignment with Other Reporting Frameworks |

EU Policy Reference |

|

Breakdown of assets under management by business sector across asset classes (equity / bonds / infrastructure / real estate / structured products / MBS / derivatives) (8). |

Reporting currency |

Report the net asset value in equity broken down by industry. |

Demonstrate awareness of current economic exposure and concentration (if any) in industries that are impacted by climate change in varying degrees. |

EU Taxonomy EIOPA SASB FN-IN-410a. GRI 201-2 |

2030 climate & energy framework |

(1) Financial institutions should read and use these proposed disclosures with due regard for any legal requirements regarding confidentiality.

(2) http://ec.europa.eu/research/environment/index.cfm?pg=nbs

(3) Examples of Climate Risks across Insurance Operations and Activities: International Association of Insurance Supervisors 2018 https://www.iaisweb.org/page/supervisory-material/issues-papers/file/76026/sif-iais-issues-paper-on-climate-changes-risk

(4) In light of regulatory developments in the prudential area, banks and insurance companies should ensure consistency between the disclosed information required by prudential rules and any other information disclosed in general purpose reports.

(5) The TCFD recognises that the term carbon-related assets is not well defined. Entities need to use a consistent definition to support comparability. The TCFD suggests defining carbon-related assets as those assets tied to the energy and utilities sectors under the Global Industry Classification Standard, excluding water utilities and independent power and renewable electricity producer industries.

(6) Financial institutions should disclose the changes in the sector and geographic allocation of their investments compared to the previous reporting year and explain the impact of these changes on the average weighted carbon intensity of their portfolios. Financial institutions are advised to review the relevance and utility of this indicator on an annual basis, in light of rapid advances in the development of scenario analysis methodologies and decision-useful, climate-related risk indicators.

The TCFD acknowledges the challenges and limitations of current carbon footprinting indicators, including that such indicators should not necessarily be interpreted as risk indicators. The TCFD recognises that some asset managers may be able to report weighted average carbon intensity for only portion of the assets they manage given data availability and methodological issues. Reporting entities may provide other carbon footprinting and exposure indicators included in the TCFD supplemental guidance for the financial sector along with a description of the methodology used (TCFD annex p. 43).