EUROPEAN COMMISSION

EUROPEAN COMMISSION

Brussels, 30.6.2021

SWD(2021) 170 final

COMMISSION STAFF WORKING DOCUMENT

IMPACT ASSESSMENT REPORT

Accompanying the

Proposal for a DIRECTIVE OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL

on consumer credits

{COM(2021) 347 final} - {SEC(2021) 281 final} - {SWD(2021) 171 final}

DISCLAIMER: This is a working document draft which does not reflect the views of the European Commission. The positions expressed therein do not prejudge the official position of the European Commission

Table of Contents

1.

Introduction: political and legal context

2.

Problem definition

2.1 What are the problem drivers?

2.2 What are the problems?

2.3

What are the consequences of the problems?

2.4

How will the problem evolve?

2.5

Intervention logic

3.

Why should the EU act?

3.1

Legal basis

3.2

Subsidiarity: Necessity of EU action

3.3

Subsidiarity: Added value of EU action

4.

Objectives: What is to be achieved?

4.1

General objectives

4.2

Specific objectives

5.

What are the available policy options?

5.1

What is the baseline from which options are assessed?

5.2

Description of the policy options

5.3

Options discarded at an early stage

6.

What are the impacts of the different policy options and who will be affected?

6.1

Policy option 1: Non-regulatory intervention

6.2

Policy option 2: Targeted amendment of the Directive to increase legal clarity

6.3

Policy option 3a: Extensive amendment of the Directive to include certain new provisions, in line with existing EU acquis

6.4

Policy option 3b: Extensive amendment of the Directive to include provisions going beyond existing EU acquis

7.

How do the options compare?

7.1 Effectiveness: expected achievement of the initiative’s objectives

7.2 Efficiency: impacts on businesses and consumers

7.3 Coherence with other EU legislation (and policy objectives)

7.4 Stakeholder views on the options

7.5 Comparison of options and proportionality

8.

The preferred option

8.1

The overall effectiveness of the preferred option

8.2

Impact on stakeholders

8.3

Synergies with other legislation

8.4

REFIT (simplification and improved efficiency)

9.

How would actual impacts be monitored and evaluated?

Annexes

Annex 1: Procedural information

Annex 2. Stakeholder consultation – Synopsis report

Annex 3. Who is affected by the initiative and how?

Annex 4. Analytical methods used in preparing the impact assessment

Annex 5: Policy options detailed measures

Annex 6: Market developments

Annex 7: Glossary

Annex 8: Mapping of national measures to support borrowers amid the COVID-19 crisis

Annex 9: Approach to monetisation of cost benefits

Annex 10: References and documentation reviewed

Annex 11: List of abbreviations

1.Introduction: political and legal context

Political context

Directive 2008/48/EC on credit agreements for consumers (“the Consumer Credit Directive” or “the Directive”) aims at securing a consistently high level of protection across the EU for consumers taking out loans, thus contributing to consumer confidence. The Directive also seeks to create the best possible conditions for the free movement of credit offers and to establish a level playing field for providers in different Member States.

The Commission evaluated the Directive in 2018-2019, following a

2017 REFIT Platform opinion

on Article 4 of the Directive regarding standard information to be provided when advertising consumer credit agreements. In 2020, the Commission presented the results of the Evaluation in a Staff Working Document and an Implementation Report to co-legislators on the Directive, as well as an externally contracted study.

This full-fledged Evaluation, while establishing that the objectives pursued by the Directive remain relevant, highlighted a number of areas for improvement. The main problems identified include the restricted scope of the Directive, issues about the content and disclosure of information to consumers and insufficient safeguards to ensure responsible lending. The Directive also lacks provisions dealing with events of exceptional and systemic economic disruption (such as the one caused by the COVID-19 crisis).

The consumer credit sector has been profoundly transformed by the digital transition. New actors such as peer-to-peer lending platforms have emerged and traditional providers are increasingly using online sales channels. New products such as short-term high-cost loans, that can lead to significant costs for the borrower, are more and more marketed and sold online. The growing use of digital devices affects the way in which pre-contractual information is provided to consumers. Also, automated decision-making for credit scoring and the use of personal data not directly provided by consumers for assessing their creditworthiness raise questions in terms of consumer and data protection and potential discrimination from decisions based on opaque algorithms. Finally, the COVID-19 crisis has greatly impacted the credit market and consumers, especially vulnerable ones, leading to an increased financial vulnerability of many EU households.

The von der Leyen Commission through its Work Programme 2020

recognised the significant impact of the digital transition in everyday life and included the need for a Europe fit for the digital age among its headline ambitions. The Commission also committed to giving a new push for European democracy, including by aligning consumer protection with contemporary realities - notably cross-border and online transactions - to empower consumers to make informed choices and play an active role in the digital transformation of society.

In this context, the Commission decided to review the Consumer Credit Directive, in line with Better Regulation principles, to ensure enhanced consumer information and understanding of consumer credits, and to better protect consumers from irresponsible lending practices. The Consumer Credit Directive’s review was included in the REFIT annex of the 2020 Commission Work Programme, with a potential new legislative proposal scheduled for the second quarter of 2021.

The Directive’s review is apposite to ensure better consumer empowerment and protection in synergy with other simultaneous initiatives that the Commission is undertaking.

First, the New Consumer Agenda,

which presents a vision for an EU consumer policy from 2020 to 2025, includes the key priority areas accompanying the digital transformation and of taking into account specific needs of consumer groups susceptible of being vulnerable. Therefore the agenda already highlighted the intention to revise the Consumer Credit Directive (action 10) but also to devise actions to enhance debt advice services in Member States (action 15). The Agenda also highlights the synergies of such actions with the ongoing review of other existing legislation, such as the Mortgage Credit Directive, the Payment Account Directive and the Distance Marketing of Financial Services Directive.

Secondly, in September 2020, the Commission adopted a

Digital finance package

, including a Digital finance strategy and legislative proposals on crypto-assets and digital resilience, for a competitive EU financial sector that gives consumers access to innovative financial products while ensuring consumer protection and financial stability. The package supports the EU’s ambition for a recovery that embraces the digital transformation. In 2020, the Commission also published a

White Paper on Artificial Intelligence

presenting options to promote the uptake of Artificial Intelligence but also to address the risks associated with certain uses of this new technology, followed by a

Proposal for a Regulation laying down harmonised rules on artificial intelligence (Artificial Intelligence Act)

published in April 2021.

In addition, the

new Capital Markets Union action plan

, published in September 2020, proposes several actions to support a green, digital, inclusive and resilient post COVID-19 economic recovery, including an action on empowering citizens through financial literacy. The action plan also announces a renewed sustainable finance strategy that the Commission will put forward to increase private investment in sustainable projects and activities.

Finally, the continuous efforts of the Commission towards deepening the Economic and Monetary Union (EMU) by 2025 are to be supported by an increased cross-border integration and risk reduction in the banking system, notably as regard non-performing loans. In 2019 consumer lending non-performing loans (NPLs) represented more than 25% of household NPLs and roughly 10% of total NPLs.

Legal developments

The Directive, which was adopted in 2008, covers consumer credit between EUR 200 and EUR 75 000, such as loans granted for personal consumption, including automotive vehicles, household goods and appliances, travels, as well as some overdrafts and credit cards. Overdraft facilities to be repaid within a month, interest-free credits, leasing agreements without an obligation to purchase are among the main types of credits excluded from its scope.

The main objectives of the Directive are to ensure that all consumers enjoy a high and equivalent level of protection across the Union as well as to create a genuine internal market for consumer credit (Member States cannot maintain or introduce in their national law provisions diverging from those laid in the Directive for harmonisation purposes). This means that, where no such harmonised provisions exist, for example due to scope limitation, Member States remain free to maintain or introduce national legislation, and most of them did so.

Along the years, a number of relevant pieces of legislation complementing the CCD have been enacted, for instance, the Mortgage Credit Directive (MCD) or the General Data Protection Regulation (GDPR). In fact, there are a number of similarities between the Consumer Credit Directive and the Mortgage Credit Directive: they both share a number of similar definitions and both pieces of legislation are currently struggling with certain similar definitions (example: whether peer-to-peer lenders fall under the definition of ‘creditor’ or ‘creditor intermediaries’). Both pieces of legislation set rules on creditworthiness assessment, with the MCD adopting a more prescriptive approach (ban on negative creditworthiness assessment and more precise text of possible data used for the assessment). The MCD also provides safer and sounder rules with regard to responsible lending, protection of over-indebtedness and regulates practices till now not fully regulated by the Consumer Credit Directive (example: product tying practices, advisory service and knowledge and competence of staff). The GDPR is of particular importance when lenders are carrying out a credit assessment.

The application of the Directive revealed some issues which were not clear, as they rose in subsequent case-law of the Court of Justice. The main issues are the following:

Right of withdrawal: Article 14(1) provides the consumer with a 14 calendar day period in which to withdraw from the credit agreement without giving any reason. The date of commencement of the 14 calendar day start either from the day of the conclusion of the credit agreement, or from the day on which the consumer receives the contractual terms and conditions and information in accordance with Article 10 of the Directive. This latter situation has given rise to a number of pending preliminary rulings for one Member State, namely Germany. The question raised by the national court concern, in particular, whether the right to withdrawal can be invoked forever whenever Article 10 of the Directive is not fully complied with.

Creditworthiness assessment: The Evaluation of the Directive highlighted the Member States’ variant interpretations of the creditworthiness assessment provisions, which created a diverse landscape as regards the requirements for such assessment. The use of new technologies and alternative types of data has led to concerns about personal data protection, particularly about transparency, relevance, proportionality and fairness. There are also concerns, predominantly expressed by consumer organisations in the context of the surveys accompanying the Evaluation and Impact Assessment support studies conducted by external consultants, about granting loans despite a negative creditworthiness assessment. According to the Court of Justice, the obligation to assess the borrower’s creditworthiness is intended to protect consumers against the risks of over-indebtedness and bankruptcy. It has also been ruled that national rules obliging the creditor to refrain from granting credit if there is a lack of the consumer’s creditworthiness, are compliant with the Directive.

In May 2020, the European Banking Authority (EBA) published

Guidelines on loan origination and monitoring

, applying as of 30 June 2021. These guidelines aim to bring together the prudential framework and consumer protection aspects of credit granting.

2.Problem definition

As demonstrated by the Evaluation, the Directive’s objectives, namely ensuring high standards of consumer protection and fostering the development of an internal market for credit, have only been partially achieved. The link between problems identified in this Impact Assessment as well as in the preparatory study, their drivers and their consequences is visualised in the problem tree below.

Figure 1 Problem tree

2.1 What are the problem drivers?

There are five key problem drivers why the Directive’s two main objectives were only partially achieved:

1)Since the entry into force of the Directive, the digitalisation has led to new market developments which are not adequately captured by the current limited scope of the regulatory framework: for instance, short-term high cost loans frequently provided online are often below EUR 200. The digital transformation is radically changing consumers’ lives and its wider implications cut across the other problem drivers.

2)Consumer behaviour and preferences have evolved over the past ten years, and for instance a greater emphasis seems to be put on factors like fast access to credit.

Behavioural biases are not adequately addressed by the current Directive and this has resulted in consumer protection gaps - for instance, against exploitative practices like cross-selling of expensive payment protection insurances not needed by the consumer.

3)Some of the Directive’s definitions have not withstood the test of time, leading to legal uncertainty (e.g. peer-to-peer lending platforms are not explicitly captured in the definition of ‘creditor’ or ‘credit intermediary’).

4)The Directive does not address adequately equity considerations in the sense that, apart from a recital (Recital 26) alluding to the problem, the legal text does not establish measures to support consumers vulnerable to over-indebtedness.

5)Finally what hampered the full achievement of the two objectives is insufficient harmonisation between Member States, allowed by the vague provisions of the Directive, leading to an unlevel playing field.

These five drivers have led to two overarching problems. On the one hand, when consumers take out loans some of them may engage in very costly credit agreements without being fully aware and/or may become unable to pay back their credit, leading to unexpected fees, and possibly to a dramatic deterioration of their financial situation and to over-indebtedness. On the other hand, the competitiveness of the internal market is not yet fully achieved, and the market for consumer credits remains largely fragmented. Each of these problems is divided into sub-problems, described below.

2.2 What are the problems?

Problem 1: consumers taking out loans face detriment that could be avoided

In the light of market, technological and behavioural developments since the Directive’s adoption, some consumers taking out loans are not adequately protected from arrangements that will become unsustainable for them. Ill-suited credits can prompt debt spirals and over-indebtedness, which have become serious social issues in some EU regions. In 2019, 2% of EU households had arrears on hire purchase instalments or other loan payments, and were at risk of over-indebtedness, with big discrepancies among Member States. The number of over-indebted households is expected to increase due to the COVID-19 crisis, which has deeply disrupted the EU economy in the beginning of 2020. Many consumers have already faced important income losses. A recent survey published by the Commission on 12 March 2021 shows that on average 38% of consumers have concerns on how they are going to pay their bills next month and the situation varies greatly among Member States (from 7% to 71%).

As shown by the Market Monitoring Survey 2019, just under three quarters of EU27 consumers trust the loans, credit and credit cards market, and 9% of them experienced problems. Of those who experienced a problem, 4 in 10 experienced financial detriment as a result (around 7 in 10 for consumers who find it very difficult to manage financially), and around three in four experienced other, non-financial impacts. The sources of consumer detriment include: insufficient protection e.g. because of loose creditworthiness assessments allowing consumers to take out credits even when this is not warranted by their financial situation; practices and business conduct of credit providers enticing consumers to take out credits they cannot afford; unclear and non-transparent disclosure of prices and fees limiting consumer understanding of the real costs of the credit; and inappropriate use of personal data.

The underlying problems are presented below.

Sub-problem 1: Emergence of new potentially or actually risky credit products not necessarily covered by the Directive and new actors not (clearly) regulated

The consumer credit market changed considerably since 2010, as a result of the strong impact of digitalisation, and of the growing presence of new products, such as payday loans, often offered by non-bank lenders. The share of non-bank lending to households has seen a dynamic growth over the recent years. Even though the market for consumer credit is still led by traditional operators, new market players, in particular fintech companies, have also appeared on the market.

One of the most important credit products provided by fintech companies is unsecured loans through peer-to-peer (P2P) lending platforms. These platforms seek to match individual borrowers with individual lenders, often tapping onto a segment of consumer lending underserved by banks (e.g. because they received a negative creditworthiness assessment). Some of the most successful in Europe are Auxmoney in Germany, Mintos in Latvia and Bondora in Estonia. P2P lending may be a convenient and quick way to access credit, however, it may involve important risks for consumers. The fast processes may lead to rush decisions. Since this new type of lending is not explicitly mentioned in the Directive, proper creditworthiness assessments may not be carried out, even when platforms act as creditors or intermediaries (i.e. receive a fee for facilitating the transaction) for professional lenders. Furthermore, consumers might be unsure about their rights and possible recourse in case of problems. Evidence from several Member States confirms that consumers are reporting issues.

The available data on the share of households using a particular product falling under the category of consumer credit is quite fragmented.The most common types of consumer credit in the market are predominantly credit cards (owned by 44% of EU citizens), and personal loans (owned by 13% of EU citizens).

The Directive establishes that loans below EUR 200 and above EUR 75 000 are outside its scope of application. Evidence shows that small loan borrowers often have more than one loan. This is particularly dangerous, since their creditworthiness is never assessed. They are therefore likely to experience early payment problems. Concerns raised about the minimum threshold of EUR 200 in the Directive also relate to the fact that in some Member States EUR 200 represent an important share of the monthly income.

In 2019, in Ireland around 300 000 people borrowed from moneylenders.

Short term high-cost (STHC) credit, including payday loans, are quick and easy-access personal loans which may be useful for consumers seeking to obtain a loan in a simple and rapid way. These loans have a clear growth potential in a digitalised market with a stronger cross-border element. They can however rapidly lead to a financial detriment, in particular for consumers with low or unpredictable incomes. STHC loans are often likely to be very expensive, far beyond the rate necessary to integrate the credit risk resulting from the borrower profile and the refinancing costs reflecting the monetary policy stance. In a recent mystery shopping exercise conducted in Ireland, Spain and Romania, the average APR for the small value (below EUR 180) payday loans analysed was found to be 2 543%. Payday loans are popular in some countries (e.g. Lithuania) and have been growing fast in others (e.g. Sweden, Poland and Czech Republic), also thanks to digitalisation that allows for quicker, automated processes.

Since the amount borrowed is typically lower than the minimum threshold of EUR 200, these loans often fall beyond the scope of the Directive.

In the absence of EU rules covering small amount STHC loans, most Member States have adopted rules to address the design of credit products, denoting the perceived importance of the problem at national level. The most common measure is the introduction of interest rate or APR caps, adopted by 23 Member States.

However, the typology of caps and their level vary significantly. Caps have led, in some cases, to lowered default notices and to the disappearance of potentially risky products such as payday loans (e.g. Belgium, Slovakia). STHC loans are growing in Member States with no or high caps and they are the main reason for consumer complaints in some of them (e.g. Bulgaria, Malta).

Revolving credit including credit cards warrant attention too. The term revolving credit encompasses any credit that is automatically renewed as debts are paid off, including thus credit cards. The Directive’s evaluation estimated that up to 20 million EU consumers face problems with their credit card in terms of unrequested extensions of the credit line. Revolving credit and credit cards raise concern among consumer associations because of the potential harm that can stem from the flexibility of these contracts due to behavioural biases. The situation of consumers under the impression of having unlimited credit possibilities from the moment they pay back a part of their debt every month, can suddenly become unsustainable because of high costs non-transparently disclosed. These credits frequently amount to less than EUR 200, and are hence exempted from the Directive’s obligations. In France, revolving credit was identified as a key factor behind over-indebtedness linked to credit. Since the introduction of specific rules in 2010, over-indebtedness related to revolving loans decreased by 47%.

Loans above EUR 75 000 are excluded from the Directive’s scope. However, the Mortgage Credit Directive has widened the scope of the Consumer Credit Directive in the sense that the latter shall apply to credit agreements the purpose of which is the renovation of a residential immovable property involving a total amount of credit above EUR 75 000. However there is no comprehensive data on such big amount loans.

There are also other credit agreements, described below, which fall outside the scope of the Directive and can entail risks for consumers:

Credit agreements where the credit is granted free of interest and without any other charges and credit agreements where the credit has to be repaid within three months and only insignificant charges are payable are not captured within the scope of the Directive (Article 2(2)(f)). These are generally used to finance the purchase of products such as household appliances, in the form of point of sale financing, concluded between the consumer and the retailer selling the good, acting either as a credit provider or intermediary. Moreover, new digital financial tools that let consumers make purchases and pay them off over time, i.e. ‘Buy Now Pay Later’ products, are growing fast in the EU, and raise concerns among consumer organisations. The number of EU citizens who have contracted an interest free loan has been estimated to be around 7 million.Although interest free credits may appear as very convenient and having low or no costs linked to them, since the lender is paid by the merchant (via a fixed or variable fee), they may entail high fees for late or missed payments.

, The risk lies in the fact that consumers are often poorly informed about the conditions of the credit, frequently very strict on delays. Moreover, such financial products promote quick decisions, enticing people to overspend and putting them at risk of taking on financial commitments that they may not be able to honour. Concern at national level is shown by the decision of certain Member States to apply some of the Directive’s provisions to all consumer credits, regardless of the interest rate charged.

Overdraft facilities allow consumers to mobilise amounts for their immediate financial needs, which exceed the balance in their current account. Usually, overdrafts entail high costs if they are not repaid within a certain period, especially for unarranged ones.

If the period does not exceed a month, the credit is not covered by the scope of the Directive (Article 2(2)(e)). Overdraft facilities are an example of loans widely used. The number of EU citizens with an overdraft facility is estimated between 20 and 40 million. National data suggest that they more likely to be needed, and therefore frequently used, by lower income households, resulting in detriment for the more vulnerable consumers.

According to Article 2(2)(d) of the Directive, leasing agreements where an obligation to purchase the object of the agreement is not laid down either by the agreement itself or by any separate agreement, do not fall under the scope of the Directive. Finance Watch estimates that “hire purchase”, a common type of leasing agreement which envisages but does not require the purchase of the good, represents around 12% of the total credit provided to households, although it accounts for 26% in Member States who joined the Union as of 2004. Leasing agreements are being increasingly used to finance automotive purchases. The number of EU citizens with a car leasing agreement is potentially high as 13 million new passenger car registration are done in the EU annually. In France, the number of leasing transactions increased by more than three times between 2008 and 2019. In Ireland, it represented the largest amount of personal financing by value in 2019, at approximately EUR 3.1 billion. Risks for consumers in taking such financing solution are linked to the absence of information enabling them to compare offers (for example a basic consumer credit arrangement could be less costly) as well as to opaque fees structures.

Credit provided by pawnbrokers/pawnshops, offering secured loans using personal property as collateral, is still widely used across the EU, especially by vulnerable consumers who cannot resort to more formal sources of credit (e.g. banks). Consumers are not always clearly informed about the applicable conditions or about the absence of equivalent consumer protections when entering into unregulated agreements. They are often unaware of the high interest rates usually attached to these contracts and they do not always receive the ‘surplus’ money that they are owed in cases where the pawnbroker sells the collateral for a price above the redemption value. It is important to stress that the pawnshop collateralised has no evident cross-border potential.

In the light of the above described problems, in order to ensure effective protection of consumers taking out loans, some Member States opted to extend the Directive’s rules to credit below EUR 200, leasing agreements, or to all overdraft facilities.

Sub-problem 2: Limited consumer awareness of the key elements and costs of the credit product they obtain

Articles 4 and 5 of the Directive indicate the elements of the consumer credit agreement about which consumers must be informed before entering a credit agreement. Article 4 concerning standard information to be included in advertising was the object of a REFIT Platform Opinion in 2017. Article 5 specifies that pre-contractual information must be presented in good time before signing the agreement by means of a standard form (SECCI). The Evaluation found that these articles have succeeded in positively impacting the overall level of consumer protection and ensuring a certain level of harmonisation in how information is provided, notably through the adoption of the SECCI. Nevertheless, there are elements that hamper their effectiveness, especially on digital means.

With regard to Article 4 of the Directive, although it establishes that information in advertising must be presented to consumers in a ‘clear, concise and prominent way’, it does not establish exactly how the information should be provided. Many national authorities, mentioned that even though credit providers are generally complying with their obligation to provide standard information at advertising stage, key information is often not prominently displayed., By presenting certain information in (non) prominent way, the advertising message can become misleading. In a mystery shopping exercise conducted in 2020, in almost 20% of cases, malpractices were experienced in advertising material, and in particular for revolving credits online. It is estimated that around 10 million borrowers may be affected by misleading advertising. Consumers are also concerned about profiling and higher prices linked to targeted advertising based on pervasive tracking and monitoring.

From the perspective of consumers, when credits are advertised through certain communication channels such as radio or TV broadcasts, with important information either shown for a very limited amount of time or spoken very quickly, they do not have the time nor the necessary attention span to process detailed information.

Moreover, the lengthy and complex information disclosed to them at pre-contractual stage appears not to be entirely effective in helping them to properly process the information they need in order to compare offers and reach decisions that are in their best interest. For instance, only 46% of the participants to the Finance Watch mystery shopping reported they could compare consumer credit products before making a decision to take out a loan. Behavioural insights show that various factors play a role in this issue: information overload, the complexity of the information provided to consumers, and practical limits to the full efficiency of the “rational consumer concept” due to the numerous behavioural and cognitive biases affecting consumers. Moreover, Art. 5 aims to ensure that consumers are given enough time to reach an informed decision “in good time before” signing an agreement. However, this open worded text has led to a situation whereby consumers are, sometimes, given very little time, or no time at all, to decide. In fact, quite often pre-contractual information is provided at the same time as the signature of the credit contract. It is estimated that up to 9.8 million consumers find the SECCI unhelpful or very unhelpful, and up to 29 million consumers do not seem to understand credit offers.

As generally agreed by stakeholders, the need to avoid information overload and to adapt the requirements to digital means of communication are key issues to be addressed. With the further use of digital tools to take out credit, (currently 36% of consumers are doing so online) it can be expected that the risks associated to online models will increase.

Sub-problem 3: Existence of practices by credit providers exploiting consumer’s situation and patterns of behaviour

Over the years, consumers’ decision-making processes to take up credit have changed as a result of digitalisation and the transformation of consumption habits. Nowadays, the consumer journey is often multichannel (both offline and online) and quicker. Consumers place greater emphasis on factors such as fast provision done from start to end by a single provider (end-to-end processing of the credit agreement) over the location of the physical branch (e.g. in relation to their home location).

In context of non-physical interaction between traders and consumers, practices exploiting consumer biases and nudging them into sub-optimal choices, including through dark-patterns can be particularly dangerous for the financial sustainability of consumers, in particular the most vulnerable ones.

Such practices include pre-ticked boxes or making credit products available quickly, in a small number of clicks (products advertised as ‘one-click’ credit). Consumers with low digital or financial literacy are particularly vulnerable in this context.

Another practice employed by credit providers, or intermediaries, which may lead to unsuitable choices for consumers, is cross-selling. Cross-selling is where an additional product is sold together with the loan, as either a mandatory (tying) or an optional element (bundling). It represents a highly profitable practice for credit providers or intermediaries, who usually have agreements with insurance companies and receive commissions when they sell these products.,

The sale of tied insurance policies, especially payment protection insurance (PPI) has raised concerns in some Member States as it is linked to a number of mis-selling scandals in the sector. The Directive deals with cross-selling only to a certain extent: it establishes that when a consumer is obliged to purchase another product together with the credit, the cost of that product must be taken into consideration in the calculation of the APR. However, PPIs can entail disguised high costs which do not always appear to be included in the calculation of the APR. Product tying is considered as very problematic and some Member States adopted measures to limit or ban it.

Unsolicited credit offers may entice consumers to take credits which are not suitable for their situation. The current Directive text does not address these practices, instead leaving it to the Member States or other Union instruments, such as the e-Privacy Directive (2002/58/EC) or the Distance Marketing of Financial Services Directive (2002/65/EC) to regulate them to different extents. While some Member States have imposed a ban or heavily regulated unsolicited credit offers (e.g. Belgium, France, Ireland), they are still common practice in many Member States (e.g. Slovenia, Slovakia), in particular for certain types of products such as credit cards, sent to consumers who have not requested them or whose limit is increased without an explicit request.

The Directive does not provide full protection for consumers from making unsuitable choices also because, while under Article 5(6) of the Directive credit providers are obliged to provide ‘adequate explanations’ to consumers before the signature of the contract, it does not impose to advise consumers for example on suitable credit products in the case of ancillary services bundled with a credit agreement. The lack of personalised advice is one of the key problems that consumers face nowadays, according to consumer organisations. The Directive does not include conduct of business obligations when providing credit to consumers either. This is especially relevant given that the performance of staff members of most financial services companies is generally assessed based on their volume of sale.

Without a harmonised approach on the design and marketing of credit products, certain credit providers are expected to continue potentially misleading practices, not in line with responsible lending principles. Further Member States may also adopt measures to limit the incentives for credit providers to make use of them in a non-coordinated manner.

Sub-problem 4: Credits granted without a thorough assessment of the consumer creditworthiness

The Directive, in Article 8, imposes an obligation on the creditor to assess the consumer’s creditworthiness on the basis of sufficient information, where appropriate obtained from the consumer and, where necessary, on the basis of consultation of the relevant database. It also mentions in Recital 26 that creditors should not engage in irresponsible lending or give out credit without prior assessment of the consumer’s creditworthiness. The CJEU has on different occasions highlighted that the article on creditworthiness assessment is fundamental, as it aims at avoiding over-indebtedness, and that the creditors should ensure that this assessment be carried out. There are different reasons hindering the Directive’s creditworthiness assessment provision effectiveness in ensuring the suitability of credit sold to consumers:

·It does not specifically establish whether the assessment should be creditor-focus (i.e. risk assessment) or borrower-focused (i.e. affordability assessment done in the interest of the consumer, as confirmed by the CJEU);

·It does not specify the categories of data that should be considered when conducting a creditworthiness assessment. This has led to the use of personal data by some data controllers (credit lenders, credit bureaus) which may not be necessary and proportionate to the purpose of conducting a creditworthiness assessment. Moreover, a majority of Member States established further requirements, establishing the minimum information to be taken into account or setting out formulas e.g. debt-to-income.

·It does not establish the consequences of a negative creditworthiness assessment, for example some Member States have prohibited the granting of credit following a negative creditworthiness assessment (e.g. Belgium, the Netherlands).

Creditworthiness assessment practices are still seen as a problem area in many Member States, with important issues raised by stakeholders in at least 12 of them. According to the Finance Watch mystery shopping exercise, creditworthiness assessments are worse in the online than in the offline consumer credit market, and worse amongst non-banks than banks. Poor creditworthiness assessment seems to be especially common in certain segments of the consumer credit market, in particular for payday loans and loans provided via peer-to-peer lending platforms.

Furthermore as already discussed, digitalisation has transformed the process of collection and analysis of consumer’s information. Credit providers make large use of automated decision-making techniques, including machine learning, for credit scoring. In addition, lenders are making use of different data sources found throughout the digital ecosystem. When carrying out creditworthiness assessments, lenders, through big data analytics, are increasingly making use of large numbers of data points, most of which are either not necessarily provided by the consumer or unknown to the consumer. This use is particularly common among certain non-traditional operators such as peer-to-peer lending platforms, but this practice is not restricted to new operators. The 2020 EBA report on big data and advanced analytics shows that 34% of business respondents declared using or planning to use big data for risk scoring. The use of such technology seem to result in a wider access to credit for consumers, but it raises fundamental rights concerns, in terms of potential infringements of the right to the protection to personal data, privacy and issues concerning direct or indirect discrimination. If left unaddressed, the risks associated with the use of machine-learning technology are expected to worsen since the use of innovative digital tools by credit providers is expected to grow.

Sub-problem 5: Certain consumers (because of individual circumstances or systemic economic disruptions) fall easily into over-indebtedness

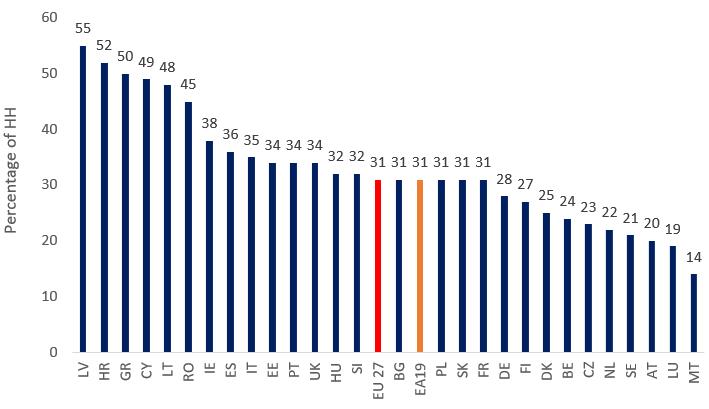

Over-indebtedness refers to a situation in which a household is not able to meet its economic and financial obligations over a sustained period. The latest European Union Statistics on Income and Living Conditions (2018) shows that on average, more than 30% of EU households were unable to meet an unexpected expense, with figures nearing 50% in some countries. According to the latest European Quality of Life Survey (2016) 14% of people (over 18) reported they were unable to make scheduled payments related to rent or mortgages, consumer credit, loans from family or friends, or utility or telephone bills (with differences between Member States). Overall, that proportion rises to 21% for people not in arrears but who have trouble making ends meet. Over-indebtedness often arises from unexpected changes in individual circumstances, usually as a result of a combination of circumstances (e.g. unemployment, personal circumstances such as divorce, illnesses, etc.), but can also be linked to irresponsible lending and borrowing practices. 2% of total EU households, and 3.9% of single parents with dependent children, have arrears on loan payments. However, looking at lower income households with arrears (bottom quartile), 10% of them have arrears on consumer credit.

In France, debts linked to consumer credit count for 37% of the total debt of over-indebted households. 75% of over-indebted households have debt linked to consumer credit, and 62% of them to a revolving credit. In Sweden, around 70% of those taking out a credit below EUR 195 already had a debt with the company that issued the loan. The majority of new small loan borrowers have at least two loans. Over-indebted households are often also in arrears with consumer credit payments, which can lead to debt spirals.

Several tools are available in Member States to assist consumers at risk or already over-indebted, including the provision of independent debt advice services, forbearance measures, or financial education (as a preventive tool). None of those tools are explicitly included among the Directive’s obligations.

Systemic economic disruptions such as the COVID-19 related crisis often have a direct impact on the financial stability of households, by affecting the income at their disposal and the availability of credit for consumers. For instance the widespread retrenchment in credit that followed the 2008 financial crisis, in combination with the job losses and the economic downturn, resulted in increased financial difficulties for European households. At the end of 2020, six in ten consumers had experienced financial problems since the start of the pandemic, and around four in ten reported a difficult financial situation.

However, this crisis is not affecting all population groups equally. Vulnerable groups have less savings, were often already in a precarious situation before the crisis, and may be the most in need to obtain credit to cover their regular expenses, pushing them to obtain higher cost and potentially detrimental credit because they do not have access to alternative, less expensive, products.

When asked about the impact of the COVID-19 crisis, up to 5% of consumers surveyed in 7 EU countries in June 2020 said they had to raise the limit on their credit card, up to 14% had to borrow money from family or friends to make ends meet, and up to 15% had to postpone paying at least one bill. Among low-income consumers surveyed, up to 23% had to postpone bill payments, and up to 20% had to borrow from family and friends. Those who are unemployed or working part-time are most likely to say that COVID-19 has already impacted on their personal income.

Amid the COVID-19 crisis, Member States have adopted a series of relief measures that seek to alleviate the financial burden of citizens and households, such as loan repayment moratoria that were generally extended to consumer credit, next to other credit forms.

Most of them have introduced deferrals of loan repayments, but for different periods and with different conditions, as regards for instance eligibility or responsibility for extra costs. Some of these measures had an effect on consumer protection, while the Directive does not address the impact of systemic economic disruptions on consumers. While Member States initiatives proved to be beneficial, the divergence between national measures taken on consumer credit to alleviate the consequences of such disruption should not lead to an uneven consumer protection level.

The majority of respondents to the New Consumer Agenda public consultation believe that EU-level action is needed to safeguard the interests of lenders and borrowers in exceptional and systemic economic disruptions.

Problem 2: the competitiveness of the internal market is not fully achieved

One of the key objectives of the Directive is to facilitate the emergence of a well-functioning internal market, through a higher degree of legal harmonisation across the EU on certain key elements of consumer credit (Recital 7). Further harmonisation would level the playing field for credit providers regardless of where they are located and facilitate the provision of credit to consumers in other Member States both directly cross- border or via establishment of subsidiaries, allowing them to broaden the number of their customers, and potentially benefit from economies of scale. From the perspective of consumers, effective competition in the internal market would increase their choices and enable them to shop around for the offer that best suits them. Higher harmonisation should also decrease national market segmentation, allowing better competition among the different players and lower interest rates, especially on smaller national markets which are very concentrated, with the top five main financial institutions representing up to 97% of assets at national level (65% on average in the EU).

More harmonisation and legal clarity should facilitate more financial institutions to provide credit across borders, and this would clearly be beneficial to competition.

Despite a high level of harmonisation of the prudential framework under which banks operate and the creation of the Banking Union in the Euro Area, the consumer credit market has remained highly fragmented. Direct cross-border activities in consumer credit, by a legal entity established in another Member State, remain low. ECB data on outstanding positions of cross-border loans to households provided by monetary financial institutions show that these represented less than 1% of total household loans for the period 2008-2019 (0.8-0.9%) and has not evolved. In 2015 fewer than 3% of European consumers purchased banking products such as credit cards in another Member State, and 5% purchased their loans from abroad.

The Directive’s Evaluation confirmed that direct cross-border operations represent 5% or less of credit agreements concluded by the credit providers consulted.

This is due to external factor influencing offer and demand, but also to different consumer protection rules, linked also to the way the Directive has been implemented at national level (regulatory choices, vagueness of some provisions). This increases the burden associated to the consumer credit distribution across borders but also reduces incentives for smaller operators to establish cross-border. Moreover, the Directive’s provisions cover only some areas related to the protection of borrowers (for instance they do not harmonise insolvency procedures).

It is to be expected that the increasing role of fintech companies as providers of consumer credit will have an impact on the level of cross-border operations. Contrary to traditional providers of credit, these companies tend to target consumers in various Member States. Their market share is currently small, but in the future their contribution to the development of a cross-border market could be potentially significant. As the digital transition makes cross-border credit operations easier, we can already observe an increasing trend of such operations. For instance, the Latvian peer-to-peer consumer lending platform Mintos is operating in several EU countries (e.g. Denmark, Poland, Czech Republic). Similarly, the Estonian platform Bondora allows users to invest in loans granted through the Bondora Group to borrowers in Estonia, Finland and Spain.

Moreover, a fast and radical change could occur, if major actors of the digital economy, such as BigTech companies, start operating in the area of consumer credit. This development can be observed already today outside the EU. In China, the major e-commerce platform Alibaba has widened its portfolio and started offering consumer credit directly on its website to consumers buying products there. In the US, Amazon Lending offers revolving credit for small and medium sellers in the Amazon e-commerce platform. This trend has not yet reached the EU, even though BigTechs are already partnering up with traditional providers to offer financing options.

This possible tendency is recognised by the Commission in the 2020

Digital Financial Strategy

, which says that risks stemming from potential large-scale lending operations by firms outside the banking perimeter should be addressed.

Sub-problem 1: Barriers for credit providers to business expansion across borders

Different regulatory approaches on a number of key Directive’s articles have resulted in different obligations for credit providers depending on the Member State in which they operate. Moreover, it is plausible to assert that legal fragmentation due to the differences in scope of application in the different Member States and different implementation of key terms of the Directive (e.g. ‘sufficient information’ in Art. 8 on creditworthiness assessment) hindered the development of cross-border lending; legal fragmentation can often discourage credit providers from serving consumers in other Member States, either directly or via establishment trade. In fact, credit providers’ lack of knowledge and/or confidence in other Member States’ regulatory framework is singled out as a significant barrier hindering expansion across borders by the business sector.

The issues of enforcement and penalties are another source that leads to high complexity and lack of confidence in the regulatory framework. The choice of sanctions (effective, proportionate and dissuasive) remains at the discretion of Member States (Art. 23). With regard to penalties, Member States have generally established civil and administrative sanctions for infringements of the national provisions transposing the Directive; in addition, some can issue criminal sanctions. As a result, there is considerable disparity in the types and levels of sanctions. With regard to the responsible enforcement authorities, a large number of Member States appointed several bodies to ensure correct implementation of the different aspects of the Directive. Sometimes, the competent authority depends on the type of the credit provider, namely whether it is a bank or a non-bank lender. Having multiple competent authorities with varying sanctioning powers and competent authorities depending on the type of operator has had an impact on the level-playing field between different providers and the consistency of enforcement.

Furthermore the Consumer Protection Cooperation Regulation (N°2017/2394) which is supposed to cover cross border infringement to the consumer legislation included in its annex (including the Consumer Credit Directive), could not be of much assistance in view of the important variations in national implementation of the Directive.

Another aspect to be considered is access to credit databases across borders. Art. 9 of the Directive establishes the obligation on the Member States to ensure access for creditors from other Member States to databases used in that Member State for assessing the creditworthiness of consumers. While the Directive has set up this obligation, it is silent on who is to run the database (publicly run and/or co-exist alongside privately run ones) or what categories of data are to be processed. The result is that the content of such database varies between countries and can include only negative data (e.g. missed payments) or, both positive (e.g. ongoing financial commitments) and negative data, coming from various sources and updated according to different timescales depending on the database. An additional hurdle to the establishment of a well-functioning cross-border database access, is the reciprocity principle. Many credit registers operate on the reciprocity principle, implying that credit providers are to supply the same type of data that they wish to access through the credit database.

However, there are external factors relating to aspects going beyond the Directive elements hampering the cross-border offer of credit. These include legal and technical barriers (know-your-customer requirements as per anti-money laundering requirements, difficulty in checking the identity of consumers, insolvency regimes, contract law relating to the validity of credit agreements) leading to regulatory and market fragmentation, post contractual issues not covered by the Directive, language barriers and questions around applicable law. Some entities may not qualify to obtain existing EU passports and have to ask authorisation in each Member State where they want to offer credit.

Sub-problem 2: Difficulties for consumers to access cross-border credit

The Directive’s Evaluation has shown that there is a growing interest among consumers for cross-border credit offers. Around one third (29%) of the respondents to the consumer survey conducted for the Evaluation said they had looked for a credit from a creditor located in another EU country. This compares to only 2% respondents to a 2011 Eurobarometer who said that they would potentially buy a personal loan in a foreign EU country. This is a marked increase in comparison to the past and demonstrates that consumers are showing a growing interest to take credits in other Member States. However, as mentioned above, very few of them actually go so far as concluding one.

There are several external obstacles and factors that deter consumers from obtaining a credit from a provider established in another Member State:

·Geographical restrictions, imposed by providers to limit access only to domestic consumers, to avoid additional administrative burden related to creditworthiness assessment in another economic environment and credit management, especially in case of default. They include requiring to provide an ID number, address, telephone number or tax declaration from the country where the creditor is based as pre-requisite for the transaction to be accepted, and are often based on geo-blocking techniques.

·General consumer preferences, like finding the offer in the national market sufficient, and preferences for obtaining a credit locally.

·Low trust due to the lack of knowledge among consumers of available redress mechanisms and of applicable legislation in case of cross-border purchase.

·Lack of awareness, since credit providers rarely target consumers in other Member States, many consumers are not aware of the possibility to access credit cross-border.

·Language and cultural barriers.

However, differences in the protection guaranteed by the Directive in different Member States could also play a role in hampering cross-border access.

Moreover, it is important to stress the Directive does not include a specific provision on preventing discrimination on the basis of “nationality or place of residence or by reason of any other ground as referred to in Article 21 of the Charter”, contrary to the Payment Account Directive (Art. 15).

Digitalisation and the change in consumer preferences are expected to lead to an increase in cross-border operations. New digital actors such as fintechs generally target consumers in various Member States more than traditional operators. This strengthen the need to ensure a high and consistent level of consumer protection among Member States.

Sub-problem 3: Information requirements for advertisement on certain channels create unnecessary burden for businesses

The Directive was evaluated following a 2017 REFIT Platform Opinion focusing on the perceived burden caused by standard information that has to be provided when advertising consumer credit agreements in particular on radio. In the Opinion, radio industry stakeholders flagged that current information requirements at advertising stage entail substantial continuous costs for advertisers, which have to pay for additional airtime, and in turn create losses for them because companies choose to advertise on other media channels.

On the other hand, those requirements have seem to have a sub-optimal effects in their main objective of informing consumers. Research carried out by the association of radios in France and in the UK shows that only 3-4% of radio listeners recall the total amount payable immediately after hearing a radio advertisement with a consumer credit offer.

This issue was confirmed by most business representatives consulted during the Evaluation (which however could not clearly ascertain whether the Directive could be simplified), and also more recently for the Impact Assessment. Business associations and credit providers stressed that the reduction of the amount of required information in advertisement and marketing would have a positive impact on the industry. They also indicated that information requirements are among the main issues they face because they are burdensome and not necessarily fit for purpose.

Reducing the information provided at advertising stage on certain channels and streamlining information displayed to consumers at advertising and pre-contractual stage could reduce burden for businesses while helping consumers to better understand the main elements of the credit. The Unfair Commercial Practices Directive already recognises that the limitations of the communication medium have to be taken into account when defining whether a commercial practice has to be regarded as misleading (Art. 7).

2.3What are the consequences of the problems?

The problems identified lead to a variety of consequences for different stakeholders.

·Consumers are harmed when they take a credit not corresponding to their needs, financial situation and repayment possibilities. The detriment concerns higher interest rates paid, or interest rates paid when they should not have been granted the credit (but the assessment of their creditworthiness was not performed thoroughly) and the possible unexpected degradation of their debt situation. In addition a worsening of their situation can have a lot of moral damage on the consumers and on their facilities. Because of ineffective information provision and processing (due to information overload), and practices nudging them, consumers end up making sub-optimal choices, which lead to additional costs incurred and lower level of trust. The lack of provisions to assist consumers when necessary, enhance their financial literacy or address the impact on consumers of systemic economic disruptions, can lead to an increase in over-indebtedness. Insufficient harmonisation between Member States, also reduces the competition and increases the concentration of markets which leads to price increase and lower choices for consumers. Vulnerable consumers, such as low-income or over-indebted consumers, are particularly affected by the identified problems.

·Businesses can easily exploit the gaps in the system to develop irresponsible lending practices. With competition being strong on certain less regulated segments of the market, there is an incentive for the less responsible lenders to set (bad) market standards. Different sets of rules for different kinds of credits and unclear obligations also prevent both the expansion of direct cross border lending and establishment trade by smaller credit institutions, and lead to an unlevel playing field. Moreover, unclear obligations and information related obligations that do not benefit consumers create unnecessary burden for businesses. Uncompliant providers or providers offering products not in the scope have a competitive advantage because they do not bear compliance costs than other operators do bear.

·The burden on national authorities enforcing the Directive increases as a result of consumers being exposed to irresponsible practices that lead to more consumer difficulties that in turn lead to more complaints to be processed. EU public authorities face many requests for preliminary rulings submitted to the CJEU, because of the vagueness of the Directive, an increased number of consumer and stakeholders’ complaints and need to provide more assistance to enforcers.

·Consequences for society are the negative externalities of increased level of over-indebtedness, risks for social inclusion, but also risks for financial stability.

2.4How will the problem evolve?

In case of no EU intervention (baseline scenario), the current market trends can be used as benchmark.

Even though the consumer credit market is at the moment still led by traditional operators

, digitalisation is already changing its landscape considerably. Fintech companies have expanded significantly in the last decade and are expected to develop further in the future. In 2018, the total value of the peer-to-peer consumer lending market in Europe remained limited (around EUR 2.4 billion), but grew by 89% year-on-year from 2017. Looking at global developments, peer-to-peer lending to consumers is expected to grow, however the impact of the COVID-19 crisis both on creditors and consumers is unclear. Since peer-to-peer consumer lending is excluded from the scope of the recently adopted EU Crowdfunding Regulation ((EU) 2020/1503) and it is not explicitly under the Directive scope, this development could increase the presence of unregulated risky products. Big Techs such as Google, Facebook, Alibaba or Amazon, who are already offering their own version of mobile wallets, as well as loans and credit lines through store cards in third countries, might enter the EU consumer lending market too.

Growing use of digital tools would also exacerbate the problem of limited consumer awareness of the key elements and costs of the credit product they obtain, because the Directive information requirements are not adapted to digital tools. Online practices from credit providers nudging consumers into making unsuitable choices, not regulated by the Directive at present, would be likely to continue and grow. The use of automated decision-making , including machine learning, for credit scoring is expected to increase too, as well as the use of alternative categories of data (such as social media data), since digitalisation makes the process of collecting and analysing consumer’s information faster and easier. This raises questions as to what data will be used in the future for assessing consumers’ creditworthiness and highlights the risks of discrimination from decisions based on algorithms. Moreover, this could worsen the problem of credits granted without thorough assessment of the consumer creditworthiness

Another aspect to be taken into account for the future market developments is the medium- to long-term societal and economic impact of COVID-19, which will take time to emerge. In the course of 2020, EU economies were supported by an unprecedented level of economic support packages.

When this support phases out, the wider cost of COVID-19 will appear. Consumers are concerned about the worsening of their financial situation. Initial data shows that low-paid workers have been particularly affected by the crisis. There were 6.1 million fewer people in employment in Q2 2020 than in Q4 2019, with temporary employees affected the hardest. Challenges in repaying the credit or accessing new credit, may appear in this subset of consumer’s segment first.

This is expected to aggravate the problem of consumers falling into over-indebtedness.

As regards the impact of COVID-19 on the consumer credit market specifically, banks expect a continued net tightening of credit standards. The weaker the contraction in output and faster and more robust the recovery is, the more contained the impact of COVID-19 would be (‘V-shaped recovery’). Conversely, deep recession and prolonged recovery spread over longer period of time (‘L-shape recovery’) would be more detrimental for consumer credit markets. The data from the 2008 crisis shows that originations were noticeably lower soon after the crisis and recovered only in recent years to 2008-levels. However, many consumers in financial difficulties due to the crisis are expected to seek consumer credit, and irresponsible lending practices from certain credit providers in the COVID-19 context can put them at risk.

Insufficient harmonisation between legislative frameworks of the Member States leading to unlevel playing field would continue to create barriers for credit providers to business expansion across borders and difficulties for consumers to access cross-border credit offers.

The negative effect of concentration of national markets will continue to negatively affect competition conditions and in particular interest rates levels.

Finally, green loans for energy efficient renovation of houses are expected to rise, especially in some Member States, as well as available public funding directed towards green investment in the coming years.

2.5Intervention logic

The problems presented above have key regulatory drivers leading to the problems and their effects on consumers, credit providers, public authorities and the society. Those are presented in the problem tree (Section 2). An objective tree is also included in Section 4. The intervention logic diagram, links the policy options with the objectives and the identified problems.

Table 1 Intervention logic diagram

3.Why should the EU act?

3.1Legal basis

The Treaty on the Functioning of the European Union (TFEU) confers upon the EU institutions the competence to lay down appropriate provisions that have as their object the establishment and functioning of the internal market (Article 114 TFEU).

Article 169 TFEU, related to consumer protection, also states that to promote the interests of consumers and ensure a high level of consumer protection, the Union shall contribute to protecting the health, safety and economic interests of consumers, as well as to promoting their right to information, education and to organise themselves in order to safeguard their interests. Article 169(2) TFEU specifies that these objectives can be reached through measures adopted pursuant to Article 114 in the context of internal market completion. Thus, a thorough examination of the possible legal basis was conducted and the one concerning consumer protection (Article 169 TFEU) points towards Article 114 TFEU.

This is in fact the approach adopted in this initiative. The objectives set out in Article 169 TFEU are attained through Article 114 TFEU, which serves as the legal basis for this Proposal, thus following the same approach as Directive 2008/48/EC. Article 114 TFEU remains the most appropriate legal basis also in light of the objective and necessity to strengthen the cross-border element. In fact, as digitalisation makes cross-border credit operations easier and the possible entry into the credit market of BigTechs companies in the EU market becomes a reality, the cross-border element is expected to increase. Thus, anchoring the revision of the Directive on Article 114 TFEU will ensure the continuity of ensuring a high level of consumer protection and at the same time allowing for the strengthening of the cross-border element.

3.2Subsidiarity: Necessity of EU action

The revision of the Directive aims to modernise the current regulatory framework and fix the areas that the Evaluation has flagged as inefficient. The two overarching objectives of the current Directive, namely to ensure that all consumers in the EU enjoy a high and equivalent level of protection and to create a genuine internal market, remain relevant.

So as to remedy this partial achievement of two overarching objectives of the Directive, legislative amendments to the current framework at EU level are required to attain further harmonisation which could lead to a higher and more uniform level of consumer protection, whilst facilitating the development of cross-border activities. These legislative amendments, including improving certain definitions, such as ‘creditor’ and/or ‘credit intermediary’ laid down in Article 3, widening the provision concerning the scope of the Directive and ensuring that key articles, such as on creditworthiness assessment, will be drafted in a clear and unambiguous manner. Thus amending current provisions of Directive 2008/48/EC by ensuring added clarity and legal certainty, the objectives laid down in the Directive will be rendered more effective.

EU action is also needed to introduce new provisions to cater for situations not envisaged in 2008. Provisions, rather than a recital, on responsible lending and provisions on ways to combat exploitative behaviour will ensure that the Directive keeps ensuring a high level of consumer protection whilst improving EU cross-border uptake of credit agreements.

While the figures concerning the conclusion of cross-border credit agreements has remained constantly low, the aim of the revision of the Directive is to propose a forward-looking legislation which facilitates its two principal objectives. What is more, it is important to stress that most Member States have enhanced the level of consumer protection by adopting measures that go beyond the Directive’s current requirements. This indicates that more efficient EU action is ever more important and necessary to intervene, where national legislation cannot sufficiently protect consumers. The dynamic market developments of recent years, especially in the light of digitalisation, show an increasing or likely to increase number and type of cross-border providers of consumer credit. As explained earlier, with new market players (e.g. peer-to-peer lenders) and possible market developments (BigTechs’ entry in the consumer lending market), the figures concerning the conclusion of cross-border credit agreement are expected to increase. Since digitalisation crosses across the different Member States and in an effort to ensure a revised Directive that is dynamic, EU action becomes necessary.

3.3Subsidiarity: Added value of EU action

Directive 2008/48/EC is a full harmonisation instrument in the areas it covers; thus, Member States could not maintain or introduce national provisions other than those laid down in the Directive in said areas. However, where no such harmonised provisions exist, Member States are free to maintain or introduce national legislation.

With regard to scope, all Member States, except Greece and Cyprus, have adopted transposing measure that extend the scope of the Directive in this sense. Indeed, 15 Member States removed the minimum and/or the maximum threshold (fully or partially) when transposing the Directive in their national legislation. Similarly, most Member States (15) extended the scope of application of the Directive (or certain of its provisions) to consumer credit not covered by the Directive, so as to include leasing agreement and/or overdraft facilities, revolving credit, mortgages, zero-interest rate and pawnshop agreements. However, in respecting the principle of subsidiarity, the proposal does not extend the scope of the Directive in instances when either cross-border potential is low (e.g. pawnshops) or when no comprehensive data and evidence of major consumers issues have been detected (e.g. loans above EUR 75 000). Thus, the principle of subsidiarity points to the option of not including pawnshops and loans above EUR 75 000 in the scope – it has not been obvious that EU action would have an added value in that regard, nor has it been proved that such extension would be beneficial for consumers.

Regarding creditworthiness assessment, most Member State (15) have already laid down further provisions about the creditworthiness assessment, defining how the assessment is to be conducted and imposing other obligations on creditors. These two examples (on the issues of scope and on the creditworthiness assessment) show that most Member States have felt the need to go beyond the current regulatory framework provided by the Directive in order to enhance the level of consumer protection. However, in so doing, their actions have impacted the objective of ensuring a level playing field for creditors, also leading to different levels of protection for consumers. Therefore, action by Member States alone will not solve the problems identified above, particularly as regards scope and creditworthiness assessment. In addition, widening the scope by removing thresholds and improving the article regulating creditworthiness assessment will increase effectiveness in attaining the objective of facilitating cross-border provision of credit agreements, as a harmonised approach will improve the credit providers’ knowledge of the regulatory system in other Member States.

In light of the situation as developed over the past 12 years, improving the current regulatory framework can only be achieved at EU level, as different Member States took different approaches (e.g. when regulating creditworthiness assessment, extending the scope of application of the Directive in differing ways and for different consumer credit products). The EU added value of doing so would be to bring a clearer legislative framework that ensures legal certainty, achieved through more harmonization.

Regulatory fragmentation among Member States was highlighted as a key issue by all stakeholder groups. Stakeholders tend to agree that the fragmentation negatively impacts both consumers and the development of a cross-border credit market. Consumer organisations mainly raised the need to adopt more prescriptive measures, which was echoed by national authorities, to protect consumers against over-indebtedness.

The recent COVID-19 pandemic has also illustrated that while Member States might be better placed to take specific measures in the area of consumer credit agreements, it is of fundamental importance not to lower the consumer’s level of protection. To cater for any possible situation leading to exceptional or systematic economic disruptions, the revised Directive is an opportunity to clarify and ensure that the rights provided to consumers (such as the right to information) are not lost or mitigated, even in exceptional circumstances which the EU might have to face. Such goal of ensuring that all citizens across the EU enjoy the rights provided by the Directive, even in case of national measures responding to a pandemic, cannot be achieved solely by Member State action.

Further to the above reasons why Member States alone would not achieve the objectives, is the impact of digitalisation. The use of digital tools is not limited to a single Member State. Rules fit for the digital age are needed to foster cross-border activity and competition. Hence, action on provisions of the Directive that are digitally relevant, such as improving how pre-contractual information is displayed online, can be achieved better at EU level: unilateral actions from Member States on this cannot deliver the same fruits as EU action.

4.Objectives: What is to be achieved?

Table 2 Objective tree

|

General objectives

|

Specific objectives

|

|

Reduce the detriment of consumers taking out loans in a changing market

|

1) Reduce the detriment arising from unregulated credit products (problem 1.1)

|

|

|

2) Ensure consumers taking out a credit are empowered by effective and timely information on the risks, costs and impact of credit on their finances, also via digital means (problem 1.2)

|

|

|

3) Ensure that credit granting is based on thorough assessment (both from credit providers and consumers) of the consumer best interest (problem 1.3, 1.4)

|

|

|

4) Prevent that specific individual or systemic situations exacerbate consumer detriment and increase over-indebtedness (problem 1.5)

|

|

Facilitate cross-border provision of consumer credit and the competitiveness of the internal market

|

5) Reduce barriers for providers offering credit across borders while enabling more choice for consumers (problem 2.1, 2.2)

6) Simplify the existing legal framework and reduce unnecessary burdens (problem 2.3)

|

4.1General objectives

The general goals of the Directive’s review are to reduce the detriment of consumers taking out loans in a changing market and to facilitate cross-border provision of consumer credit and the competitiveness of the internal market. This is in line with the original objectives of the Directive, namely securing a consistently high level of consumer protection across the EU, thus contributing to consumer confidence, and facilitate the emergence of a well-functioning internal market in consumer credit, creating the best possible conditions for the free movement of credit offers. The Evaluation showed that the Directive is only partially effective in meeting its objectives and pointed to scope for improvement.

4.2Specific objectives

The specific objectives (SOs) of the review are detailed below.

·SO1: Reduce the detriment arising from unregulated credit products by ensuring better regulatory coverage of the consumer credit products raising problems for consumer protection (addressing sub-problem 1.1).