EUR-Lex Access to European Union law

This document is an excerpt from the EUR-Lex website

Document 01979L1072-20070101

Eighth Council Directive of 6 December 1979 on the harmonization of the laws of the Member States relating to turnover taxes — Arrangements for the refund of value added tax to taxable persons not established in the territory of the country (79/1072/EEC)

Consolidated text: Eighth Council Directive of 6 December 1979 on the harmonization of the laws of the Member States relating to turnover taxes — Arrangements for the refund of value added tax to taxable persons not established in the territory of the country (79/1072/EEC)

Eighth Council Directive of 6 December 1979 on the harmonization of the laws of the Member States relating to turnover taxes — Arrangements for the refund of value added tax to taxable persons not established in the territory of the country (79/1072/EEC)

No longer in force

No longer in force

1979L1072 — EN — 01.01.2007 — 004.001

This document is meant purely as a documentation tool and the institutions do not assume any liability for its contents

|

EIGHTH COUNCIL DIRECTIVE of 6 December 1979 on the harmonization of the laws of the Member States relating to turnover taxes — Arrangements for the refund of value added tax to taxable persons not established in the territory of the country (OJ L 331, 27.12.1979, p.11) |

Amended by:

|

|

|

Official Journal |

||

|

No |

page |

date |

||

|

L 363 |

129 |

20.12.2006 |

||

Amended by:

|

L 302 |

23 |

15.11.1985 |

||

|

C 241 |

21 |

29.8.1994 |

||

|

|

(adapted by Council Decision 95/1/EC, Euratom, ECSC) |

L 001 |

1 |

.. |

|

L 236 |

33 |

23.9.2003 |

|

NB: This consolidated version contains references to the European unit of accout and/or the ecu, which from 1 January 1999 should be understood as references to the euro — Council Regulation (EEC) No 3308/80 (OJ L 345, 20.12.1980, p. 1) and Coundil Regulation (EC) No 1103/97 (OJ L 162, 19.6.1997, p. 1). |

EIGHTH COUNCIL DIRECTIVE

of 6 December 1979

on the harmonization of the laws of the Member States relating to turnover taxes — Arrangements for the refund of value added tax to taxable persons not established in the territory of the country

(79/1072/EEC)

THE COUNCIL OF THE EUROPEAN COMMUNITIES,

Having regard to the Treaty establishing the European Economic Community,

Having regard to Sixth Council Directive 77/388/EEC of 17 May 1977 on the harmonization of the laws of the Member States relating to turnover taxes — Common system of value added tax (uniform basis of assessment) ( 1 ), and particular Article 17 (4) thereof,

Having regard to the proposal from the Commission ( 2 ),

Having regard to the opinion of the European Parliament ( 3 ),

Having regard to the opinion of the Economic and Social Committee ( 4 ),

Whereas, pursuant to Article 17 (4) of Directive 77/388/EEC, the Council is to adopt Community rules laying down the arrangements governing refunds of value added tax, referred to in paragraph 3 of the said Article, to taxable persons not established in the territory of the country;

Whereas rules are required to ensure that a taxable person established in the territory of one member country can claim for tax which has been invoiced to him in respect of supplies of goods or services in another Member State or which has been paid in respect of imports into that other Member State, thereby avoiding double taxation;

Whereas discrepancies between the arrangements currently in force in Member States, which give rise in some cases to deflection of trade and distortion of competition, should be eliminated;

Whereas the introduction of Community rules in this field will mark progress towards the effective liberalization of the movement of persons, goods and services, thereby helping to complete the process of economic integration;

Whereas such rules must not lead to the treatment of taxable persons differing according to the Member State in the territory of which they are established;

Whereas certain forms of tax evasion or avoidance should be prevented;

Whereas, under Article 17 (4) of Directive 77/388/EEC, Member States may refuse the refund or impose supplementary conditions in the case of taxable persons not established in the territory of the Community; whereas steps should, however, also be taken to ensure that such taxable persons are not eligible for refunds on more favourable terms than those provided for in respect of Community taxable persons;

Whereas, initially, only the Community arrangements contained in this Directive should be adopted; whereas these arrangements provide, in particular, that decisions in respect of applications for refund should be notified within six months of the date on which such applications were lodged; whereas refunds should be made within the same period; whereas, for a period of one year from the final date laid down for the implementation of these arrangements, the Italian Republic should be authorized to notify the decisions taken by its competent services with regard to applications lodged by taxable persons not established within its territory and to make the relevant refunds within nine months, in order to enable the Italian Republic to reorganize the system at present in operation, with a view to applying the Community system;

Whereas further arrangements will have to be adopted by the Council to supplement the Community system; whereas, until the latter arrangements enter into force, Member States will refund the tax on the services and the purchases of goods which are not covered by this Directive, in accordance with the arrangements which they adopt pursuant to Article 17 (4) of Directive 77/388/EEC,

HAS ADOPTED THIS DIRECTIVE:

Article 1

For the purposes of this Directive, ‘a taxable person not established in the territory of the country’ shall mean a person as referred to in Article 4 (1) of Directive 77/388/EEC who, during the period referred to in the first and second sentences of the first subparagraph of Article 7 (1), has had in that country neither the seat of his economic activity, nor a fixed establishment from which business transactions are effected, nor, if no such seat or fixed establishment exists, his domicile or normal place of residence, and who, during the same period, has supplied no goods or services deemed to have been supplied in that country, with the exception of:

(a) transport services and services ancillary thereto, exempted pursuant to Article 14 (1) (i), Article 15 or Article 16 (1), B, C and D of Directive 77/388/EEC;

(b) services provided in cases where tax is payable solely by the person to whom they are supplied, pursuant to Article 21 (1) (b) of Directive 77/388/EEC.

Article 2

Each Member State shall refund to any taxable person who is not established in the territory of the country but who is established in another Member State, subject to the conditions laid down below, any value added tax charged in respect of services or movable property supplied to him by other taxable persons in the territory of the country or charged in respect of the importation of goods into the country, in so far as such goods and services are used for the purposes of the transactions referred to in Article 17 (3) (a) and (b) of Directive 77/388/EEC and of the provision of services referred to in Article 1(b).

Article 3

To qualify for refund, any taxable person as referred to in Article 2 who supplies no goods or services deemed to be supplied in the territory of the country shall:

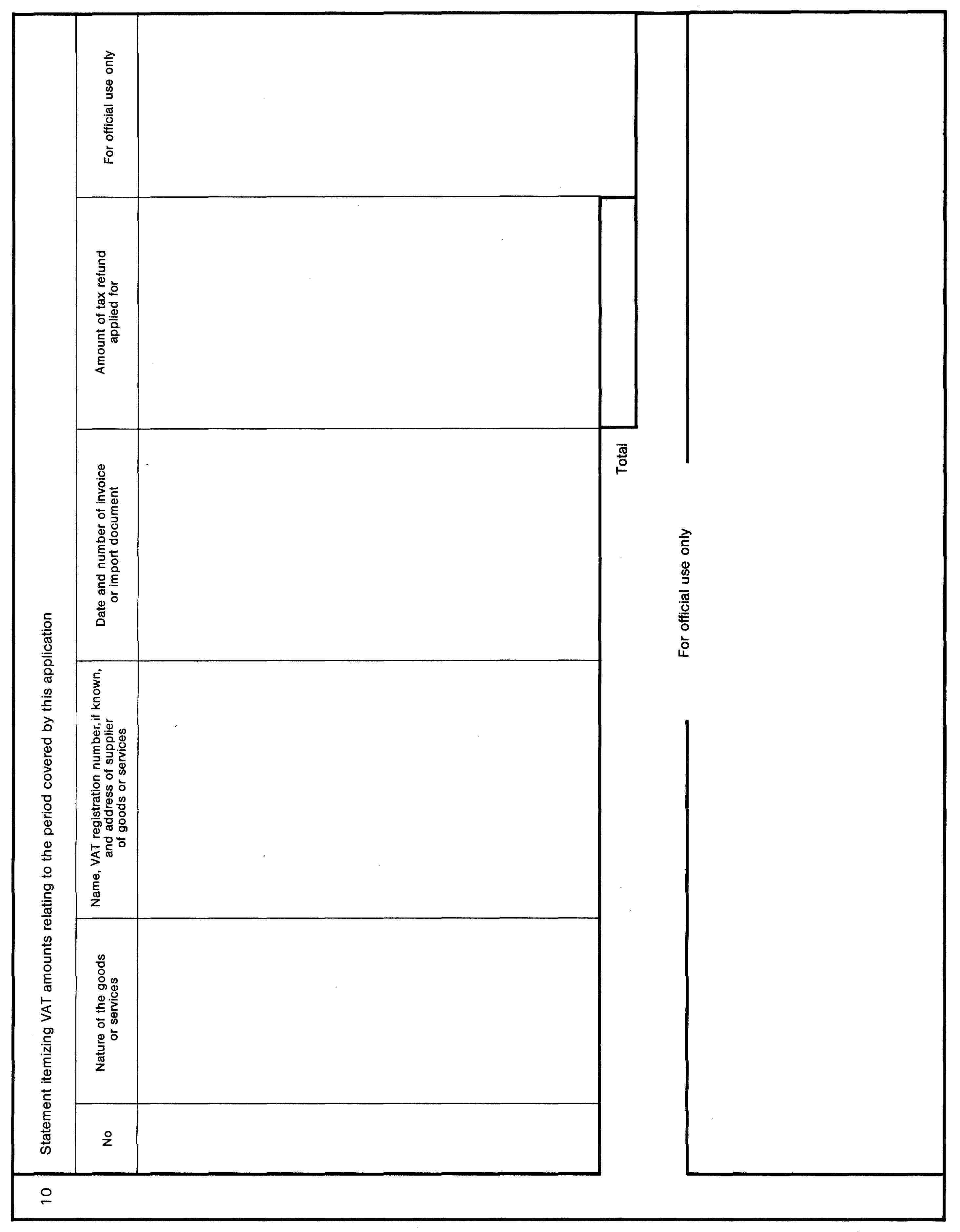

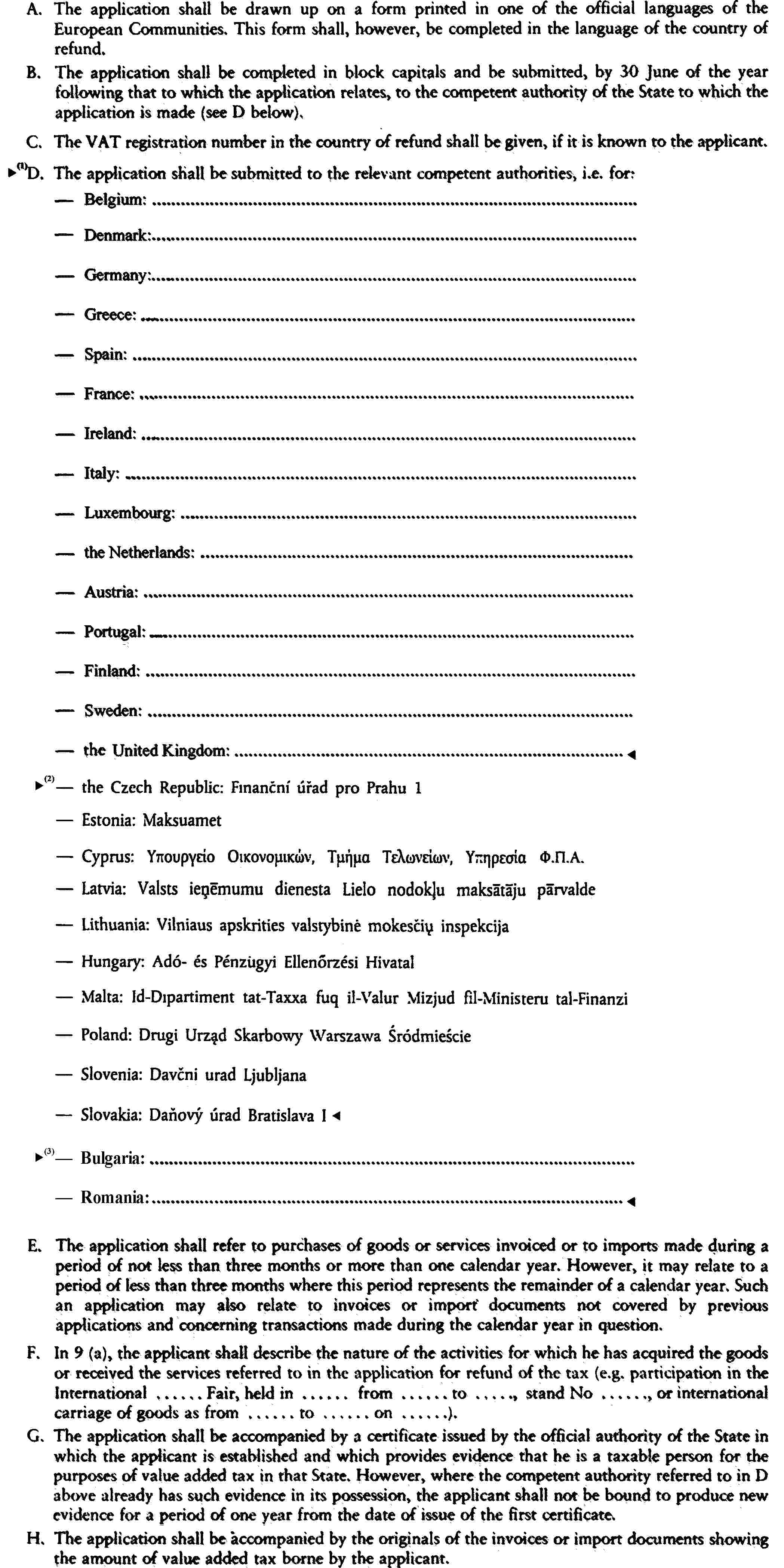

(a) submit to the competent authority referred to in the first paragraph of Article 9 an application modelled on the specimen contained in Annex A, attaching originals of invoices or import documents. Member States shall make available to applicants an explanatory notice which shall in any event contain the minimum information set out in Annex C;

(b) produce evidence, in the form of a certificate issued by the official authority of the State in which he is established, that he is a taxable person for the purposes of value added tax in that State. However, where the competent authority referred to in the first paragraph of Article 9 already has such evidence in its possession, the taxable person shall not be bound to produce new evidence for a period of one year from the date of issue of the first certificate by the official authority of the State in which he is established. Member States shall not issue certificates to any taxable persons who benefit from tax exemption pursuant to Article 24 (2) of Directive 77/388/EEC;

(c) certify by means of a written declaration that he has supplied no goods or services deemed to have been supplied in the territory of the country during the period referred to in the first and second sentences of the first subparagraph of Article 7 (1);

(d) undertake to repay any sum collected in error.

Article 4

To be eligible for the refund, any taxable person as referred to in Article 2 who has supplied in the territory of the country no goods or services deemed to have been supplied in the country other than the services referred to in Article 1 (a) and (b) shall:

(a) satisfy the requirements laid down in Article 3 (a), (b) and (d);

b) certify by means of a written declaration that, during the period referred to in the first and second sentences of the first subparagraph of Article 7 (1), he has supplied no goods or services deemed to have been supplied in the territory of the country other than services referred to in Article 1 (a) and (b).

Article 5

For the purposes of this Directive, goods and services in respect of which tax may be refundable shall satisfy the conditions laid down in Article 17 of Directive 77/388/EEC as applicable in the Member State of refund.

This Directive shall not apply to supplies of goods which are, or may by, exempted under item 2 of Article 15 of Directive 77/388/EEC.

Article 6

Member States may not impose on the taxable persons referred to in Article 2 any obligation, in addition to those referred to in Articles 3 and 4, other than the obligation to provide, in specific cases, the information necessary to determine whether the application for refund is justified.

Article 7

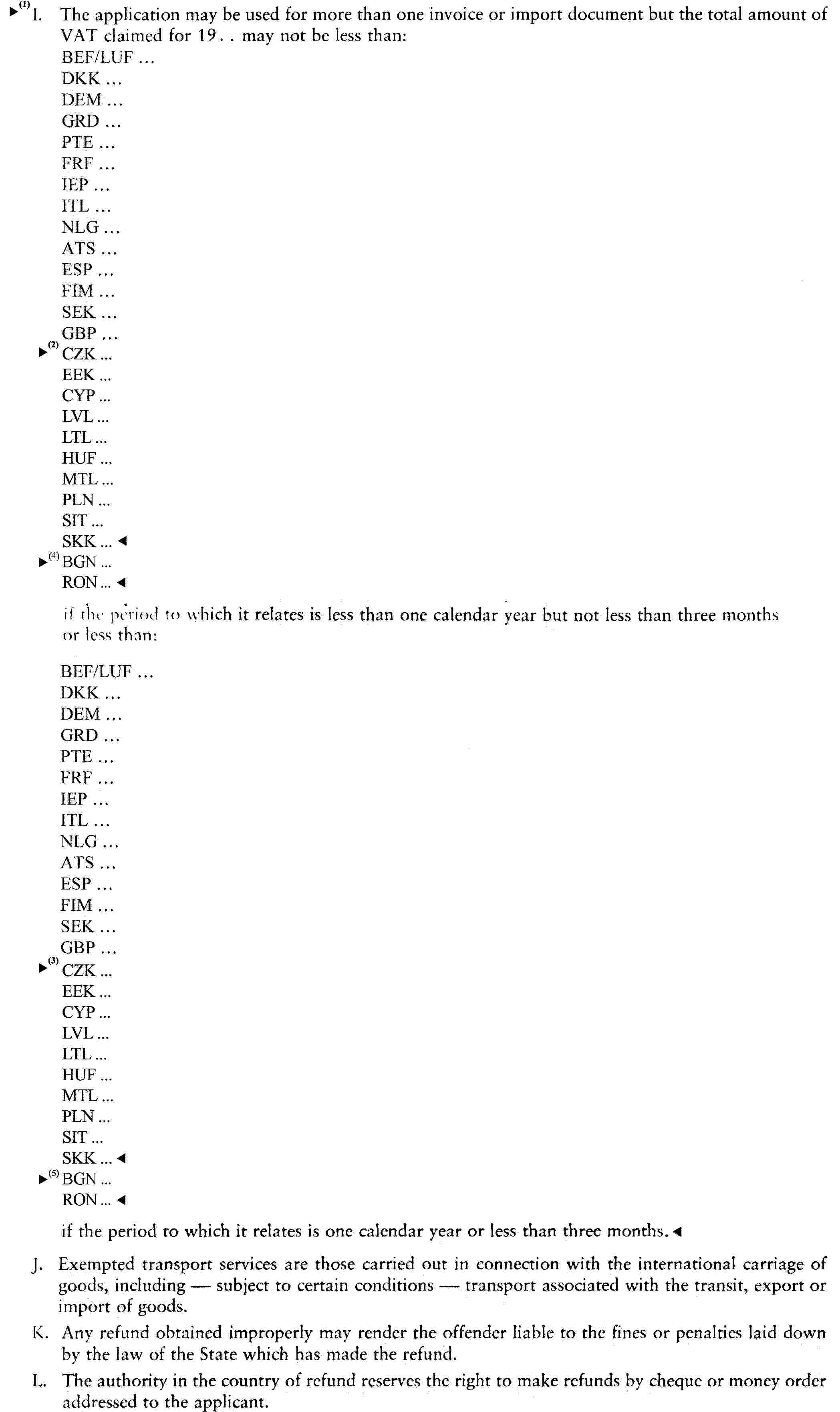

1. The application for refund provided for in Articles 3 and 4 shall relate to invoiced purchases of goods or services or to imports made during a period of not less than three months or not more than one calendar year. Applications may, however, relate to a period of less than three months where the period represents the remainder of a calendar year. Such applications may also relate to invoices or import documents not covered by previous applications and concerning transactions completed during the calendar year in question. Applications shall be submitted to the competent authority referred to in the first paragraph of Article 9 within six months of the end of the calendar year in which the tax became chargeable.

If the application relates to a period of less than one calendar year but not less than three months, the amount for which application is made may not be less than the equivalent in national currency of 200 European units of account; if the application relates to a period of a calendar year or the remainder of a calendar year, the amount may not be less than the equivalent in national currency of 25 European units of account.

2. The European unit of account used shall be that defined in the Financial Regulation of 21 December 1977 ( 5 ), as determined on 1 January of the year of the period referred to in the first and second sentences of the first subparagraph of paragraph 1. Member States may round up or down, by up to 10 %, the figures resulting from this conversion into national currency.

3. The competent authority referred to in the first paragraph of Article 9 shall stamp each invoice and/or import document to prevent their use for further application and shall return them within one month.

4. Decisions concerning applications for refund shall be announced within six months of the date when the applications, accompanied by all the necessary documents required under this Directive for examination of the application, are submitted to the competent authority referred to in paragraph 3. Refunds shall be made before the end of the abovementioned period, at the applicant's request, in either the Member State of refund or the State in which he is established. In the latter case, the bank charges for the transfer shall be payable by the applicant.

The grounds for refusal of an application shall be stated. Appeals against such refusals may be made to the competent authorities in the Member State concerned, subject to the same conditions as to form and time limits as those governing claims for refunds made by taxable persons established in the same State.

5. Where a refund has been obtained in a fraudulent or in any other irregular manner, the competent authority referred to in paragraph 3 shall proceed directly to recover the amounts wrongly paid and any penalties imposed, in accordance with the procedure applicable in the Member State concerned, without prejudice to the provisions relating to mutual assistance in the recovery of value added tax.

In the case of fraudulent applications which cannot be made the subject of an administrative penalty, in accordance with national legislation, the Member State concerned may refuse for a maximum period of two years from the date on which the fraudulent application was submitted any further refund to the taxable person concerned. Where an administrative penalty has been imposed but has not been paid, the Member State concerned may suspend any further refund to the taxable person concerned until it has been paid.

Article 8

In the case of taxable persons not established in the territory of the Community, Member States may refuse refunds or impose special conditions.

Refunds may not be granted on terms more favourable than those applied in respect of taxable persons established in the territory of the Community.

Article 9

Member States shall make known, in an appropriate manner, the competent authority to which the application referred to in Article 3 (a) and in Article 4 (a) are to be submitted.

The certificates referred to in Article 3 (b) and in Article 4 (a), establishing that the person concerned is a taxable person, shall be modelled on the specimens contained in Annex B.

Article 10

Member States shall bring into force the provisions necessary to comply with this Directive no later than 1 January 1981. This Directive shall apply only to applications for refunds concerning value added tax charged on invoiced purchases of goods or services or in imports made as from that date.

Member States shall communicate to the Commission the texts of the main provisions of national law which they adopt in the field covered by this Directive. The Commission shall inform the other Member States thereof.

Article 11

By away of derogation from Article 7 (4), the Italian Republic may, until 1 January 1982, extend the period referred to in this paragraph from six to nine months.

Article 12

Three years after the date referred to in Article 10, the Commission shall, after consulting the Member States, submit a report to the Council on the application of this Directive, and in particular Articles 3, 4 and 7 thereof.

Article 13

This Directive is addressed to the Member States.

ANNEX A

SPECIMEN

ANNEX B

SPECIMEN

CERTIFICATE OF STATUS OF TAXABLE PERSON

ANNEX C

Minimum information to be given in explanatory notes

( 1 ) OJ No L 145, 13. 6. 1977, p. 1.

( 2 ) OJ No C 26, 1. 2. 1978, p. 5.

( 3 ) OJ No C 39, 12. 2. 1979, p. 14.

( 4 ) OJ No C 269, 13. 11. 1978, p. 51.

( 5 ) OJ No L 356, 31. 12. 1977, p. 1.