This document is an excerpt from the EUR-Lex website

Document 01993R2454-20060601

Commission Regulation (EEC) No 2454/93 of 2 July 1993 laying down provisions for the implementation of Council Regulation (EEC) No 2913/92 establishing the Community Customs Code

Consolidated text: Commission Regulation (EEC) No 2454/93 of 2 July 1993 laying down provisions for the implementation of Council Regulation (EEC) No 2913/92 establishing the Community Customs Code

Commission Regulation (EEC) No 2454/93 of 2 July 1993 laying down provisions for the implementation of Council Regulation (EEC) No 2913/92 establishing the Community Customs Code

- Date of document:

- 01/06/2006

- Date of effect:

- 01/06/2006

- Author:

- European Commission

- Form:

- Consolidated text

- Additional information:

- LASTMODIN 32006R0402

- Link

- Link

- Link

- Select all documents mentioning this document

- Consolidation: basic act:

- 31993R2454

1993R2454 — EN — 01.06.2006 — 009.001

This document is meant purely as a documentation tool and the institutions do not assume any liability for its contents

|

COMMISSION REGULATION (EEC) No 2454/93 of 2 July 1993 (OJ L 253, 11.10.1993, p.1) |

Amended by:

|

|

|

Official Journal |

||

|

No |

page |

date |

||

|

L 335 |

1 |

31.12.1993 |

||

|

L 82 |

15 |

25.3.1994 |

||

|

L 162 |

1 |

30.6.1994 |

||

|

L 235 |

6 |

9.9.1994 |

||

|

L 346 |

1 |

31.12.1994 |

||

|

L 171 |

8 |

21.7.1995 |

||

|

L 70 |

4 |

20.3.1996 |

||

|

L 218 |

1 |

28.8.1996 |

||

|

L 289 |

1 |

12.11.1996 |

||

|

L 9 |

1 |

13.1.1997 |

||

|

L 17 |

28 |

21.1.1997 |

||

|

L 196 |

31 |

24.7.1997 |

||

|

L 7 |

3 |

13.1.1998 |

||

|

L 212 |

18 |

30.7.1998 |

||

|

L 10 |

1 |

15.1.1999 |

||

|

L 65 |

1 |

12.3.1999 |

||

|

L 197 |

25 |

29.7.1999 |

||

|

L 188 |

1 |

26.7.2000 |

||

|

L 330 |

1 |

27.12.2000 |

||

|

L 141 |

1 |

28.5.2001 |

||

|

L 68 |

11 |

12.3.2002 |

||

|

L 134 |

1 |

29.5.2003 |

||

|

L 187 |

16 |

26.7.2003 |

||

|

L 343 |

1 |

31.12.2003 |

||

|

L 139 |

1 |

2.6.2005 |

||

|

L 148 |

5 |

11.6.2005 |

||

|

L 38 |

11 |

9.2.2006 |

||

|

L 70 |

35 |

9.3.2006 |

||

Amended by:

|

C 241 |

21 |

29.8.1994 |

||

|

|

(adapted by Council Decision 95/1/EC, Euratom, ECSC) |

L 001 |

1 |

.. |

|

L 236 |

33 |

23.9.2003 |

Corrected by:

|

NB: This consolidated version contains references to the European unit of accout and/or the ecu, which from 1 January 1999 should be understood as references to the euro — Council Regulation (EEC) No 3308/80 (OJ L 345, 20.12.1980, p. 1) and Coundil Regulation (EC) No 1103/97 (OJ L 162, 19.6.1997, p. 1). |

COMMISSION REGULATION (EEC) No 2454/93

of 2 July 1993

laying down provisions for the implementation of Council Regulation (EEC) No 2913/92 establishing the Community Customs Code

THE COMMISSION OF THE EUROPEAN COMMUNITIES,

Having regard to the Treaty establishing the European Economic Community,

Having regard to Council Regulation (EEC) No 2913/92 of 12 October 1992 establishing the Community Customs Code ( 1 ), hereinafter referred to as the ‘Code’, and in particular Article 249 thereof,

Whereas the Code assembled all existing customs legislation in a single legal instrument; whereas at the same time the Code made certain modifications to this legislation to make it more coherent, to simplify it and to plug certain loopholes; whereas it therefore constitutes complete Community legislation in this area;

Whereas the same reasons which led to the adoption of the Code apply equally to the customs implementing legislation; whereas it is therefore desirable to bring together in a single regulation those customs implementing provisions wich (SIC! which) are currently scattered over a large number of Community regulations and directives;

Whereas the implementing code for the Community Customs Code hereby established should set out existing customs implementing rules; whereas it is nevertheless necessary, in the light of experience:

— to make some amendments in order to adapt the said rules to the provisions of the Code,

— to extend the scope of certain provisions which currently apply only to specific customs procedures in order to take account of the Code's comprehensive application,

— to formulate certain rules more precisely in order to achieve greater legal security in their application;

Whereas the changes made relate mainly to the provisions concerning customs debt;

Whereas it is appropriate to limit the application of Article 791 (2) until 1 January 1995 and to review the subject matter in the light of experience gained before that time;

Whereas the measures provided for by this Regulation are in accordance with the opinion of the Customs Code Committee,

HAS ADOPTED THIS REGULATION:

PART I

GENERAL IMPLEMENTING PROVISIONS

TITLE I

GENERAL

CHAPTER 1

Definitions

Article 1

For the purposes of this Regulation:

1. Code means:

Council Regulation (EEC) No 2913/92 of 12 October 1992 establishing a Community Customs Code ( 2 );

2. ATA carnet means:

the international customs document for temporary importation established by virtue of the ATA Convention or the Istanbul Convention;

3. Committee means:

the Customs Code Committee established by Articles 247a and 248a of the Code;

4. Customs Cooperation Council means:

the organization set up by the Convention establishing a Customs Cooperation Council, done at Brussels on 15 December 1950;

5. Particulars required for identification of the goods means:

on the one hand, the particulars used to identify the goods commercially allowing the customs authorities to determine the tariff classification and, on the other hand, the quantity of the goods;

6. Goods of a non-commercial nature means:

goods whose entry for the customs procedure in question is on an occasional basis and whose nature and quantity indicate that they are intended for the private, personal or family use of the consignees or persons carrying them, or which are clearly intended as gifts;

7. Commercial policy measures means:

non-tariff measures established, as part of the common commercial policy, in the form of Community provisions governing the import and export of goods, such as surveillance or safeguard measures, quantitative restrictions or limits and import or export prohibitions;

8. Customs nomenclature means:

one of the nomenclatures referred to in Article 20 (6) of the Code;

9. Harmonized System means:

the Harmonized Commodity Description and Coding System;

10. Treaty means:

the Treaty establishing the European Community;

11. Istanbul Convention means:

the Convention on Temporary Admission agreed at Istanbul on 26 June 1990.

Article 1a

For the purposes of applying Articles 291 to 300, the countries of the Benelux Economic Union shall be considered as a single Member State.

CHAPTER 2

Decisions

Article 2

Where a person making a request for a decision is not in a position to provide all the documents and information necessary to give a ruling, the customs authorities shall provide the documents and information at their disposal.

Article 3

A decision concerning security favourable to a person who has signed an undertaking to pay the sums due at the first written request of the customs authorities, shall be revoked where the said undertaking is not fulfilled.

Article 4

A revocation shall not affect goods which, at the moment of its entry into effect, have already been placed under a procedure by virtue of the revoked authorization.

However, the customs authorities may require that such goods be assigned to a permitted customs-approved treatment or use within the period which they shall set.

CHAPTER 3

Data-processing techniques

Article 4a

1. Under the conditions and in the manner which they shall determine, and with due regard to the principles laid down by customs rules, the customs authorities may provide that formalities shall be carried out by a data-processing technique.

For this purpose:

— ‘a data-processing technique’ means:

—(a) the exchange of EDI standard messages with the customs authorities;

(b) the introduction of information required for completion of the formalities concerned into customs data-processing systems;

— ‘EDI’ (electronic data interchange) means, the transmission of data structured according to agreed message standards, between one computer system and another, by electronic means,

— ‘standard message’ means a predefined structure recognized for the electronic transmission of data.

2. The conditions laid down for carrying out formalities by a data-processing technique shall include inter alia measures for checking the source of data and for protecting data against the risk of unauthorized access, loss, alteration or destruction.

Article 4b

Where formalities are carried out by a data-processing technique, the customs authorities shall determine the rules for replacement of the handwritten signature by another technique which may be based on the use of codes.

Article 4c

For test programmes using data-processing techniques designed to evaluate possible simplifications, the customs authorities may, for the period strictly necessary to carry out the programme, waive the requirement to provide the following information:

(a) the declaration provided for in Article 178(1);

(b) by way of derogation from Article 222(1), the particulars relating to certain boxes of the Single Administrative Document which are not necessary for the identification of the goods and which are not the factors on the basis of which import or export duties are applied.

However, the information shall be available on request in the framework of a control operation.

The amount of import duties to be charged in the period covered by a derogation granted pursuant to the first subparagraph shall not be lower than that which would be levied in the absence of a derogation.

Member States wishing to engage in such test programmes shall provide the Commission in advance with full details of the proposed test programme, including its intended duration. They shall also keep the Commission informed of actual implementation and results. The Commission shall inform all the other Member States.

TITLE II

BINDING INFORMATION

CHAPTER 1

Definitions

Article 5

For the purpose of this Title:

1. binding information:

means tariff information or origin information binding on the administrations of all Community Member States when the conditions laid down in Articles 6 and 7 are fulfilled;

2. applicant:

— tariff matters: means a person who has applied to the customs authorities for binding tariff information,

— origin matters: means a person who has applied to the customs authorities for binding origin information and has valid reasons to do so,

3. holder:

means the person in whose name the binding information is issued.

CHAPTER 2

Procedure for obtaining binding information — Notification of information to applicants and transmission to the Commission

Article 6

1. Applications for binding information shall be made in writing, either to the competent customs authorities in the Member State or Member States in which the information is to be used, or to the competent customs authorities in the Member State in which the applicant is established.

Applications for binding tariff information shall be made by means of a form conforming to the specimen shown in Annex 1B.

2. An application for binding tariff information shall relate to only one type of goods. An application for binding origin information shall relate to only one type of goods and one set of circumstances conferring origin.

3.

(A) Applications for binding tariff information shall include the following particulars:

(a) the holder's name and address;

(b) the name and address of the applicant where that person is not the holder;

(c) the customs nomenclature in which the goods are to be classified. Where an applicant wishes to obtain the classification of goods in one of the nomenclatures referred to in Article 20 (3) (b) and (6) (b) of the Code, the application for binding tariff information shall make express mention of the nomenclature in question;

(d) a detailed description of the goods permitting their identification and the determination of their classification in the customs nomenclature;

(e) the composition of the goods and any methods of examination used to determine this, where the classification depends on it;

(f) any samples, photographs, plans, catalogues or other documents available which may assist the customs authorities in determining the correct classification of the goods in the customs nomenclature, to be attached as annexes;

(g) the classification envisaged;

(h) agreement to supply a translation of any attached document into the official language (or one of the official languages) of the Member State concerned if requested by the customs authorities;

(i) any particulars to be treated as confidential;

(j) indication by the applicant whether, to his knowledge, binding tariff information for identical or similar goods has already been applied for, or issued in the Community;

(k) acceptance that the information supplied may be stored on a database of the Commission and that the particulars of the binding tariff information, including any photograph(s), sketch(es), brochure(s) etc., may be disclosed to the public via the Internet, with the exception of the information which the applicant has marked as confidential; the provisions governing the protection of information in force shall apply.

(B) Applications for binding origin information shall include the following particulars:

(a) the holder's name and address;

(b) the name and address of the applicant where that person is not the holder;

(c) the applicable legal basis, for the purposes of Articles 22 and 27 of the Code;

(d) a detailed description of the goods and their tariff classification;

(e) the composition of the goods and any methods of examination used to determine this and their ex-works price, as necessary;

(f) the conditions enabling origin to be determined, the materials used and their origin, tariff classification, corresponding values and a description of the circumstances (rules on change of tariff heading, value added, description of the operation or process, or any other specific rule) enabling the conditions in question to be met; in particular the exact rule of origin applied and the origin envisaged for the goods shall be mentioned;

(g) any samples, photographs, plans, catalogues or other documents available on the composition of the goods and their component materials and which may assist in describing the manufacturing process or the processing undergone by the materials;

(h) agreement to supply a translation of any attached document into the official language (or one of the official languages) of the Member State concerned if requested by the customs authorities;

(i) any particulars to be treated as confidential, whether in relation to the public or the administrations;

(j) indication by the applicant whether, to his knowledge, binding tariff information or binding origin information for goods or materials identical or similar to those referred to under points (d) or (f) have already been applied for or issued in the Community;

(k) acceptance that the information supplied may be stored on a public-access database of the Commission; however, apart from Article 15 of the Code, the provisions governing the protection of information in force in the Member States shall apply.

4. Where, on receipt of the application, the customs authorities consider that it does not contain all the particulars required to give an informed opinion, the customs authorities shall ask the applicant to supply the required information. The time limits of three months and 150 days referred to in Article 7 shall run from the moment when the customs authorities have all the information needed to reach a decision; the customs authorities shall notify the applicant that the application has been received and the date from which the said time limit will run.

5. The list of customs authorities designated by the Member States to receive applications for or to issue binding information shall be published in the ‘C’ series of the Official Journal of the European Communities.

Article 7

1. Binding information shall be notified to the applicant as soon as possible.

(a) Tariff matters: if it has not been possible to notify binding tariff information to the applicant within three months of acceptance of the application, the customs authorities shall contact the applicant to explain the reason for the delay and indicate when they expect to be able to notify the information.

(b) Origin matters: information shall be notified within a time limit of 150 days from the date when the application was accepted.

2. Binding information shall be notified by means of a form conforming to the specimen shown at Annex 1 (binding tariff information) or Annex 1A (binding origin information). The notification shall indicate what particulars will be treated as confidential. The right of appeal referred to in Article 243 of the Code shall be mentioned.

Article 8

1. In the case of binding tariff information, the customs authorities of the Member States shall, without delay, transmit to the Commission the following:

(a) a copy of the application for binding tariff information (set out in Annex 1B);

(b) a copy of the binding tariff information notified (copy No 2 set out in Annex 1);

(c) the data as given on copy No 4 set out in Annex 1.

In the case of binding origin information they shall, without delay, transmit to the Commission the relevant details of the binding origin information notified.

Such transmission shall be effected by electronic means.

2. Where a Member State so requests, the Commission shall send it without delay the particulars obtained in accordance with paragraph 1. Such transmission shall be effected by electronic means.

3. The electronically transmitted data of the application for binding tariff information, the binding tariff information notified and the data as given on copy No 4 of Annex 1 shall be stored in a central database of the Commission. The data of the binding tariff information, including any photograph(s), sketch(es), brochure(s) and so forth, may be disclosed to the public via the Internet, with the exception of the confidential information contained in boxes 3 and 8 of the binding tariff information notified.

CHAPTER 3

Provisions applying in the event of inconsistencies in binding information

Article 9

1. Where different binding information exists:

— the Commission shall, on its own initiative or at the request of the representative of a Member State, place the item on the agenda of the Committee for discussion at the meeting to be held the following month or, failing that, the next meeting,

— in accordance with the Committee procedure, the Commission shall adopt a measure to ensure the uniform application of nomenclature or origin rules, as applicable, as soon as possible and within six months following the meeting referred to in the first indent.

2. For the purpose of applying paragraph 1, binding origin information shall be deemed to be different where it confers different origin on goods which:

— fall under the same tariff heading and whose origin was determined in accordance with the same origin rules and,

— have been obtained using the same manufacturing process.

CHAPTER 4

Legal effect of binding information

Article 10

1. Without prejudice to Articles 5 and 64 of the Code, binding information may be invoked only by the holder.

2.

(a) Tariff matters: the customs authorities may require the holder, when fulfilling customs formalities, to inform the customs authorities that he is in possession of binding tariff information in respect of the goods being cleared through customs.

(b) Origin matters: the authorities responsible for checking the applicability of binding origin information may require the holder, when completing any formalities, to inform the said authorities that he is in possession of binding origin information covering the goods in respect of which the formalities are being completed.

3. The holder of binding information may use it in respect of particular goods only where it is established:

(a) tariff matters: to the satisfaction of the customs authorities that the goods in question conform in all respects to those described in the information presented;

(b) origin matters: to the satisfaction of the authorities referred to in paragraph 2 (b) that the goods in question and the circumstances determining their origin conform in all respect to those described in the information presented.

4. The customs authorities (for binding tariff information) or the authorities referred to in paragraph 2 (b) (for binding origin information) may ask for the information to be translated into the official language or one of the official languages of the Member State concerned.

Article 11

Binding tariff information supplied by the customs authorities of a Member State since 1 January 1991 shall become binding on the competent authorities of all the Member States under the same conditions.

Article 12

1. On adoption of one of the acts or measures referred to in Article 12 (5) of the Code, the customs authorities shall take the necessary steps to ensure that binding information shall thenceforth be issued only in conformity with the act or measure in question.

2.

(a) For binding tariff information, for the purposes of paragraph 1 above, the date to be taken into consideration shall be as follows:

— for the Regulations provided for in Article 12 (5) (a) (i) of the Code concerning amendments to the customs nomenclature, the date of their applicability,

— for the Regulations provided for in Article 12 (5) (a) (i) of the Code and establishing or affecting the classification of goods in the customs nomenclature, the date of their publication in the ‘L’ series of the Official Journal of the European Communities,

— for the Regulations provided for in Article 12 (5) (a) (ii) of the Code concerning amendments to the explanatory notes to the combined nomenclature, the date of their publication in the ‘C’ series of the Official Journal of the European Communities,

— for judgments of the Court of Justice of the European Communities provided for in Article 12 (5) (a) (ii) of the Code, the date of the judgment,

— for the measures provided for in Article 12 (5) (a) (ii) of the Code concerning the adoption of a classification opinion, or amendments to the explanatory notes to the Harmonized System Nomenclature by the World Customs Organization, the date of the Commission communication in the ‘C’ series of the Official Journal of the European Communities.

(b) For binding origin information, for the purposes of paragraph 1, the date to be taken into consideration shall be as follows:

— for the Regulations provided for in Article 12 (5) (b) (i) of the Code concerning the determination of the origin of goods and the rules provided for in Article 12 (5) (b) (ii), the date of their applicability,

— for the measures provided for in Article 12 (5) (b) (ii) of the Code concerning amendments to the explanatory notes and opinions adopted at Community level, the date of their publication in the ‘C’ series of the Official Journal of the European Communities,

— for judgments of the Court of Justice of the European Communities provided for in Article 12 (5) (b) (ii) of the Code, the date of the judgment,

— for the measures provided for in Article 12 (5) (b) (ii) of the Code concerning opinions on origin or explanatory notes adopted by the World Trade Organization, the date given in the Commission communication in the ‘C’ series of the Official Journal of the European Communities,

— for the measures provided for in Article 12 (5) (b) (ii) of the Code concerning the Annex to the World Trade Organization's Agreement on rules of origin and those adopted under international agreements, the date of their applicability.

3. The Commission shall communicate the dates of adoption of the measures and acts referred to in this Article to the customs authorities as soon as possible.

CHAPTER 5

Provisions applying in the event of expiry of binding information

Article 13

Where, pursuant to the second sentence of Article 12 (4) and Article 12 (5) of the Code, binding information is void or ceases to be valid, the customs authority which supplied it shall notify the Commission as soon as possible

Article 14

1. When a holder of binding information which has ceased to be valid for reasons referred to in Article 12 (5) of the Code, wishes to make use of the possibility of invoking such information during a given period pursuant to paragraph 6 of that Article, he shall notify the customs authorities, providing any necessary supporting documents to enable a check to be made that the relevant conditions have been satisfied.

2. In exceptional cases where the Commission, in accordance with the second subparagraph of Article 12 (7) of the Code, adopts a measure derogating from the provisions of paragraph 6 of that Article, or where the conditions referred to in paragraph 1 of this Article concerning the possibility of continuing to invoke binding tariff information or binding origin information have not been fulfilled, the customs authorities shall notify the holder in writing.

▼M18 —————

TITLE IV

ORIGIN OF GOODS

CHAPTER 1

Non-preferential origin

Section 1

Working or processing conferring origin

Article 35

This chapter lays down, for textiles and textile articles falling within Section XI of the combined nomenclature, and for certain products other than textiles and textile articles, the working or processing which shall be regarded as satisfying the criteria laid down in Article 24 of the Code and shall confer on the products concerned the origin of the country in which they were carried out.

‘Country’ means either a third country or the Community as appropriate.

Subsection 1

Textiles and textile articles falling within Section XI of the combined nomenclature

Article 36

For textiles and textile articles falling within Section XI of the combined nomenclature, a complete process, as specified in Article 37, shall be regarded as a working or processing conferring origin in terms of Article 24 of the Code.

Article 37

Working or processing as a result of which the products obtained receive a classification under a heading of the combined nomenclature other than those covering the various non-originating materials used shall be regarded as complete processes.

However, for products listed in Annex 10, only the specific processes referred to in column 3 of that Annex in connection with each product obtained shall be regarded as complete, whether or not they involve a change of heading.

The method of applying the rules in Annex 10 is described in the introductory notes in Annex 9.

Article 38

For the purposes of the preceding Article, the following shall in any event be considered as insufficient working or processing to confer the status of originating products whether or not there is a change of heading:

(a) operations to ensure the preservation of products in good condition during transport and storage (ventilation, spreading out, drying, removal of damaged parts and like operations);

(b) simple operations consisting of removal of dust, sifting or screening, sorting, classifying, matching (including the making-up of sets of articles), washing, cutting up;

(i) changes of packing and breaking-up and assembly of consignments;

(ii) simple placing in bags, cases, boxes, fixing on cards or boards, etc., and all other simple packing operations;

(d) the affixing of marks, labels or other like distinguishing signs on products or their packaging;

(e) simple assembly of parts of products to constitute a complete product;

(f) a combination of two or more operations specified in (a) to (e).

Subsection 2

Products other than textiles and textile articles falling within Section XI of the combined nomenclature

Article 39

In the case of products obtained which are listed in Annex 11, the working or processing referred to in column 3 of the Annex shall be regarded as a process or operation conferring origin under Article 24 of the Code.

The method of applying the rules set out in Annex 11 is described in the introductory notes in Annex 9.

Subsection 3

Common provisions for all products

Article 40

Where the lists in Annexes 10 and 11 provide that origin is conferred if the value of the non-originating materials used does not exceed a given percentage of the ex-works price of the products obtained, such percentage shall be calculated as follows:

— ‘value’ means the customs value at the time of import of the non-originating materials used or, if this is not known and cannot be ascertained, the first ascertainable price paid for such materials in the country of processing,

— ‘ex-works price’ means the ex-works price of the product obtained minus any internal taxes which are, or may be, repaid when such product is exported,

— ‘value acquired as a result of assembly operations’ means the increase in value resulting from the assembly itself, together with any finishing and checking operations, and from the incorporation of any parts originating in the country where the operations in question were carried out, including profit and the general costs borne in that country as a result of the operations.

Section 2

Implementing provisions relating to spare parts

Article 41

1. Accessories, spare parts or tools delivered with any piece of equipment, machine, apparatus or vehicle which form part of its standard equipment shall be deemed to have the same origin as that piece of equipment, machine, apparatus or vehicle.

►M1 2. ◄ Essential spare parts for use with any piece of equipment, machine, apparatus or vehicle put into free circulation or previously exported shall be deemed to have the same origin as that piece of equipment, machine, apparatus or vehicle provided the conditions laid down in this section are fulfilled.

Article 42

The presumption of origin referred to in the preceding Article shall be accepted only:

— if this is necessary for importation into the country of destination,

— if the incorporation of the said essential spare parts in the piece of equipment, machine, apparatus or vehicle concerned at the production stage would not have prevented the piece of equipment, machine, apparatus or vehicle from having Community origin or that of the country of manufacture.

Article 43

For the purposes of Article 41:

(a) ‘piece of equipment, machine, apparatus or vehicle’ means goods listed in Sections XVI, XVII and XVIII of the combined nomenclature;

(b) ‘essential spare parts’ means parts which are:

— components without which the proper operation of the goods referred to in (a) which have been put into free circulation or previously exported cannot be ensured, and

— characteristic of those goods, and

— intended for their normal maintenance and to replace parts of the same kind which are damaged or have become unserviceable.

Article 44

Where an application is presented to the competent authorities or authorized agencies of the Member States for a certificate of origin for essential spare parts within the meaning of Article 41, box 6 (Item number, marks, numbers, number and kind of packages, description of goods) of that certificate and the application relating thereto shall include a declaration by the person concerned that the goods mentioned therein are intended for the normal maintenance of a piece of equipment, machine, apparatus or vehicle previously exported, together with the exact particulars of the said piece of equipment, machine, apparatus or vehicle.

Whenever possible, the person concerned shall also give the particulars of the certificate of origin (issuing authority, number and date of certificate) under cover of which was exported the piece of equipment, machine, apparatus or vehicle for whose maintenance the parts are intended.

Article 45

Where the origin of essential spare parts within the meaning of Article 41 must be proved for their release for free circulation in the Community by the production of a certificate of origin, the certificate shall include the particulars referred to in Article 44.

Article 46

In order to ensure application of the rules laid down in this section, the competent authorities of the Member States may require additional proof, in particular:

— production of the invoice or a copy of the invoice relating to the piece of equipment, machine, apparatus or vehicle put into free circulation or previously exported,

— the contract or a copy of the contract or any other document showing that delivery is being made as part of the normal maintenance service.

Section 3

Implementing provisions relating to certificates of origin

Subsection 1

Provisions relating to universal certificates of origin

Article 47

When the origin of a product is or has to be proved on importation by the production of a certificate of origin, that certificate shall fulfil the following conditions:

(a) it shall be made out by a reliable authority or agency duly authorized for that purpose by the country of issue;

(b) it shall contain all the particulars necessary for identifying the product to which it relates, in particular:

— the number of packages, their nature, and the marks and numbers they bear,

— the type of product,

— the gross and net weight of the product; these particulars may, however, be replaced by others, such as the number or volume, when the product is subject to appreciable changes in weight during carriage or when its weight cannot be ascertained or when it is normally identified by such other particulars,

— the name of the consignor;

(c) it shall certify unambiguously that the product to which it relates originated in a specific country.

Article 48

1. A certificate of origin issued by the competent authorities or authorized agencies of the Member States shall comply with the conditions prescribed by Article 47 (a) and (b).

2. The certificates and the applications relating to them shall be made out on forms corresponding to the specimens in Annex 12.

3. Such certificates of origin shall certify that the goods originated in the Community.

However, when the exigencies of export trade so require, they may certify that the goods originated in a particular Member State.

If the conditions of Article 24 of the Code are fulfilled only as a result of a series of operations or processes carried out in different Member States, the goods may only be certified as being of Community origin.

Article 49

Certificates of origin shall be issued upon written request of the person concerned.

Where the circumstances so warrant, in particular where the applicant maintains a regular flow of exports, the Member States may decide not to require an application for each export operation, on condition that the provisions concerning origin are complied with.

Where the exigencies of trade so require, one or more extra copies of an origin certificate may be issued.

Such copies shall be made out on forms corresponding to the specimen in Annex 12.

Article 50

1. The certificate shall measure 210 × 297 mm. A tolerance of up to minus 5 mm or plus 8 mm in the length shall be allowed. The paper used shall be white, free of mechanical pulp, dressed for writing purposes and weigh at least 64 g/m2 or between 25 and 30 g/m2 where air-mail paper is used. It shall have a printed guilloche pattern background in sepia such as to reveal any falsification by mechanical or chemical means.

2. The application form shall be printed in the official language or in one or more of the official languages of the exporting Member State. The certificate of origin form shall be printed in one or more of the official languages of the Community or, depending on the practice and requirements of trade, in any other language.

3. Member States may reserve the right to print the certificate of origin forms or may have them printed by approved printers. In the latter case, each certificate must bear a reference to such approval. Each certificate of origin form must bear the name and address of the printer or a mark by which the printer can be identified. It shall also bear a serial number, either printed or stamped, by which it can be identified.

Article 51

The application form and the certificate of origin shall be completed in typescript or by hand in block capitals, in an identical manner, in one of the official languages of the Community or, depending on the practice and requirements of trade, in any other languages.

Article 52

Each origin certificate referred to in Article 48 shall bear a serial number by which it can be identified. The application for the certificate and all copies of the certificate itself shall bear the same number.

In addition, the competent authorities or authorized agencies of the Member States may number such documents by order of issue.

Article 53

The competent authorities of the Member States shall determine what additional particulars, if any, are to be given in the application. Such additional particulars shall be kept to a strict minimum.

Each Member State shall inform the Commission of the provisions it adopts in pursuance of the preceding paragraph. The Commission shall immediately communicate this information to the other Member States.

Article 54

The competent authorities or authorized agencies of the Member States which have issued certificates of origin shall retain the applications for a minimum of two years.

However, applications may also be retained in the form of copies thereof, provided that these have the same probative value under the law of the Member State concerned.

Subsection 2

Specific provisions relating to certificates of origin for certain agricultural products subject to special import arrangements

Article 55

Articles 56 to 65 lay down the conditions for use of certificates of origin relating to agricultural products originating in third countries for which special non-preferential import arrangements have been established, in so far as these arrangements refer to the following provisions.

(a)

Certificates of origin

Article 56

1. Certificates of origin relating to agricultural products originating in third countries for which special non-preferential import arrangements are established shall be made out on a form conforming to the specimen in Annex 13.

2. Such certificates shall be issued by the competent governmental authorities of the third countries concerned, hereinafter referred to as the issuing authorities, if the products to which the certificates relate can be considered as products originating in those countries within the meaning of the rules in force in the Community.

3. Such certificates shall also certify all necessary information provided for in the Community legislation governing the special import arrangements referred to in Article 55.

4. Without prejudice to specific provisions under the special import arrangements referred to in Article 55 the period of validity of the certificates of origin shall be ten months from the date of issue by the issuing authorities.

Article 57

1. Certificates of origin drawn up in accordance with the provisions of this subsection shall consist only of a single sheet identified by the word ‘original’ next to the title of the document.

If additional copies are necessary, they shall bear the designation ‘copy’ next to the title of the document.

2. The competent authorities in the Community shall accept as valid only the original of the certificate of origin.

Article 58

1. The certificate of origin shall measure 210 × 297 mm; a tolerance of up to plus 8 mm or minus 5 mm in the length may be allowed. The paper used shall be white, not containing mechanical pulp, and shall weigh not less than 40 g/m2. The face of the original shall have a printed yellow guilloche pattern background making any falsification by mechanical or chemical means apparent.

2. The certificates shall be printed and completed in one of the official languages of the Community.

Article 59

1. The certificate shall be completed in typescript or by means of a mechanical data-processing system, or similar procedure.

2. Entries must not be erased or overwritten. Any changes shall be made by crossing out the wrong entry and if necessary adding the correct particulars. Such changes shall be initialled by the person making them and endorsed by the issuing authorities.

Article 60

1. Box 5 of the certificates of origin issued in accordance with Articles 56 to 59 shall contain any additional particulars which may be required for the implementation of the special import arrangements to which they relate as referred to in Article 56 (3).

2. Unused spaces in boxes 5, 6 and 7 shall be struck through in such a way that nothing can be added at a later stage.

Article 61

Each certificate of origin shall bear a serial number, whether or not printed, by which it can be identified, and shall be stamped by the issuing authority and signed by the person or persons empowered to do so.

The certificate shall be issued when the products to which it relates are exported, and the issuing authority shall keep a copy of each certificate issued.

Article 62

Exceptionally, the certificates of origin referred to above may be issued after the export of the products to which they relate, where the failure to issue them at the time of such export was a result of involuntary error or omission or special circumstances.

The issuing authorities may not issue retrospectively a certificate of origin provided for in Articles 56 to 61 until they have checked that the particulars in the exporter's application correspond to those in the relevant export file.

Certificates issued retrospectively shall bear one of the following:

— expedido a posteriori,

— udstedt efterfølgende,

— Nachträglich ausgestellt,

— Εκδοθέν εκ των υστέρων,

— Issued retrospectively,

— Délivré a posteriori,

— rilasciato a posteriori,

— afgegeven a posteriori,

— emitido a posteriori,

— annettu jälkikäteen —utfärdat i efterhand,

— utfärdat i efterhand,

— Vystaveno dodatečně,

— Välja antud tagasiulatuvalt,

— Izsniegts retrospektīvi,

— Retrospektyvusis išdavimas,

— Kiadva visszamenőleges hatállyal,

— Maħruġ retrospettivament,

— Wystawione retrospektywnie,

— Izdano naknadno,

— Vyhotovené dodatočne,

in the ‘Remarks’ box.

(b)

Administrative cooperation

Article 63

1. Where the special import arrangements for certain agricultural products provide for the use of the certificate of origin laid down in Articles 56 to 62, the entitlement to use such arrangements shall be subject to the setting up of an administrative cooperation procedure unless specified otherwise in the arrangements concerned.

To this end the third countries concerned shall send the Commission of the European Communities:

— the names and addresses of the issuing authorities for certificates of origin together with specimens of the stamps used by the said authorities,

— the names and addresses of the government authorities to which requests for the subsequent verification of origin certificates provided for in Article 64 below should be sent.

The Commission shall transmit all the above information to the competent authorities of the Member States.

2. Where the third countries in question fail to send the Commission the information specified in paragraph 1, the competent authorities in the Community shall refuse access entitlement to the special import arrangements.

Article 64

1. Subsequent verification of the certificates of origin referred to in Articles 56 to 62 shall be carried out at random and whenever reasonable doubt has arisen as to the authenticity of the certificate or the accuracy of the information it contains.

For origin matters the verification shall be carried out on the initiative of the customs authorities.

For the purposes of agricultural rules, the verification may be carried out, where appropriate, by other competent authorities.

2. For the purposes of paragraph 1, the competent authorities in the Community shall return the certificate of origin or a copy thereof to the governmental authority designated by the exporting country, giving, where appropriate, the reasons of form or substance for an enquiry. If the invoice has been produced, the original or a copy thereof shall be attached to the returned certificate. The authorities shall also provide any information that has been obtained suggesting that the particulars given on the certificates are inaccurate or that the certificate is not authentic.

Should the customs authorities in the Community decide to suspend the application of the special import arrangements concerned pending the results of the verification they shall grant release of the products subject to such precautions as they consider necessary.

Article 65

1. The results of subsequent verifications shall be communicated to the competent authorities in the Community as soon as possible.

The said results must make it possible to determine whether the origin certificates remitted in the conditions laid down in Article 64 above apply to the goods actually exported and whether the latter may actually give rise to application of the special importation arrangements concerned.

2. If there is no reply within a maximum time limit of six months to requests for subsequent verification, the competent authorities in the Community shall definitively refuse to grant entitlement to the special import arrangements.

CHAPTER 2

Preferential origin

Article 66

For the purposes of this Chapter:

(a) ‘manufacture’ means any kind of working or processing including assembly or specific operations;

(b) ‘material’ means any ingredient, raw material, component or part, etc., used in the manufacture of the product;

(c) ‘product’ means the product being manufactured, even if it is intended for later use in another manufacturing operation;

(d) ‘goods’ means both materials and products;

(e) ‘customs value’ means the value as determined in accordance with the 1994 Agreement on implementation of Article VII of the General Agreement on Tariffs and Trade (WTO Agreement on customs valuation);

(f) ‘ex-works price’ in the list in Annex 15 means the price paid for the product ex-works to the manufacturer in whose undertaking the last working or processing is carried out, provided that the price includes the value of all the materials used, minus any internal taxes which are, or may be, repaid when the product obtained is exported;

(g) ‘value of materials’ in the list in Annex 15 means the customs value at the time of importation of the non-originating materials used, or, if this is not known and cannot be ascertained, the first ascertainable price paid for the materials in the Community or the beneficiary country within the meaning of Article 67(1) or in the beneficiary republic within the meaning of Article 98(1). Where the value of the originating materials used needs to be established, this subparagraph shall be applied mutatis mutandis;

(h) ‘chapters’ and ‘headings’ mean the chapters and the headings (four-digit codes) used in the nomenclature which makes up the Harmonised System;

(i) ‘classified’ refers to the classification of a product or material under a particular heading;

(j) ‘consignment’ means products which are either sent simultaneously from one exporter to one consignee or covered by a single transport document covering their shipment from the exporter to the consignee or, in the absence of such document, by a single invoice.

Section 1

Generalised system of preferences

Subsection 1

Definition of the concept of originating products

Article 67

1. For the purposes of the provisions concerning generalised tariff preferences granted by the Community to products originating in developing countries (hereinafter referred to as ‘beneficiary countries’), the following products shall be considered as originating in a beneficiary country:

(a) products wholly obtained in that country within the meaning of Article 68;

(b) products obtained in that country in the manufacture of which products other than those referred to in (a) are used, provided that the said products have undergone sufficient working or processing within the meaning of Article 69.

2. For the purposes of this section, products originating in the Community, within the meaning of paragraph 3, which are subject in a beneficiary country to working or processing going beyond that described in Article 70 shall be considered as originating in that beneficiary country.

3. Paragraph 1 shall apply mutatis mutandis in order to establish the origin of the products obtained in the Community.

4. In so far as Norway and Switzerland grant generalised tariff preferences to products originating in the beneficiary countries referred to in paragraph 1 and apply a definition of the concept of origin corresponding to that set out in this section, products originating in the Community, Norway or Switzerland which are subject in a beneficiary country to working or processing going beyond that described in Article 70 shall be considered as originating in that beneficiary country.

The provisions of the first subparagraph shall apply only to products originating in the Community, Norway or Switzerland (according to the rules of origin relative to the tariff preferences in question) which are exported direct to the beneficiary country.

The provisions of the first subparagraph shall not apply to products falling within Chapters 1 to 24 of the Harmonised System.

The Commission shall publish in the Official Journal of the European Communities (C series) the date from which the provisions laid down in the first and second subparagraphs shall apply.

5. The provisions of paragraph 4 shall apply on condition that Norway and Switzerland grant, by reciprocity, the same treatment to Community products.

Article 68

1. The following shall be considered as wholly obtained in a beneficiary country or in the Community:

(a) mineral products extracted from its soil or from its seabed;

(b) vegetable products harvested there;

(c) live animals born and raised there;

(d) products from live animals raised there;

(e) products obtained by hunting or fishing conducted there;

(f) products of sea fishing and other products taken from the sea outside its territorial waters by its vessels;

(g) products made on board its factory ships exclusively from the products referred to in (f);

(h) used articles collected there fit only for the recovery of raw materials;

(i) waste and scrap resulting from manufacturing operations conducted there;

(j) products extracted from the seabed or below the seabed which is situated outside its territorial waters but where it has exclusive exploitation rights;

(k) goods produced there exclusively from products specified in (a) to (j).

2. The terms ‘its vessels’ and ‘its factory ships’ in paragraph 1(f) and (g) shall apply only to vessels and factory ships:

— which are registered or recorded in the beneficiary country or in a Member State,

— which sail under the flag of a beneficiary country or of a Member State,

— which are at least 50 % owned by nationals of the beneficiary country or of Member States or by a company having its head office in that country or in one of those Member States, of which the manager or managers, Chairman of the Board of Directors or of the Supervisory Board, and the majority of the members of such boards are nationals of that beneficiary country or of the Member States and of which, in addition, in the case of companies, at least half the capital belongs to that beneficiary country or to the Member States or to public bodies or nationals of that beneficiary country or of the Member States,

— of which the master and officers are nationals of the beneficiary country or of the Member States, and

— of which at least 75 % of the crew are nationals of the beneficiary country or of the Member States.

3. The terms ‘beneficiary country’ and ‘Community’ shall also cover the territorial waters of that country or of the Member States.

4. Vessels operating on the high seas, including factory ships on which the fish caught is worked or processed, shall be considered as part of the territory of the beneficiary country or of the Member State to which they belong, provided that they satisfy the conditions set out in paragraph 2.

Article 69

For the purposes of Article 67, products which are not wholly obtained in a beneficiary country or in the Community are considered to be sufficiently worked or processed when the conditions set out in the list in Annex 15 are fulfilled.

Those conditions indicate, for all products covered by this section, the working or processing which must be carried out on non-originating materials used in manufacturing, and apply only in relation to such materials.

If a product which has acquired originating status by fulfilling the conditions set out in the list is used in the manufacture of another product, the conditions applicable to the product in which it is incorporated shall not apply to it, and no account shall be taken of the non-originating materials which may have been used in its manufacture.

Article 70

1. Without prejudice to paragraph 2, the following operations shall be considered as insufficient working or processing to confer the status of originating products, whether or not the requirements of Article 69 are satisfied:

(a) preserving operations to ensure that the products remain in good condition during transport and storage;

(b) breaking-up and assembly of packages;

(c) washing, cleaning; removal of dust, oxide, oil, paint or other coverings;

(d) ironing or pressing of textiles;

(e) simple painting and polishing operations;

(f) husking, partial or total milling, polishing and glazing of cereals and rice;

(g) operations to colour sugar or form sugar lumps; partial or total milling of sugar;

(h) peeling, stoning and shelling, of fruits, nuts and vegetables;

(i) sharpening, simple grinding or simple cutting;

(j) sifting, screening, sorting, classifying, grading, matching; (including the making-up of sets of articles);

(k) simple placing in bottles, cans, flasks, bags, cases, boxes, fixing on cards or boards and all other simple packaging operations;

(l) affixing or printing marks, labels, logos and other like distinguishing signs on products or their packaging;

(m) simple mixing of products, whether or not of different kinds, where one or more components of the mixtures do not meet the conditions laid down in this section to enable them to be considered as originating in a beneficiary country or in the Community;

(n) simple assembly of parts of articles to constitute a complete article or disassembly of products into parts;

(o) a combination of two or more of the operations specified in points (a) to (n);

(p) slaughter of animals.

2. All the operations carried out in either a beneficiary country or the Community on a given product shall be considered together when determining whether the working or processing undergone by that product is to be regarded as insufficient within the meaning of paragraph 1.

Article 70a

1. The unit of qualification for the application of the provisions of this section shall be the particular product which is considered as the basic unit when determining classification using the nomenclature of the Harmonised System.

Accordingly, it follows that:

(a) when a product composed of a group or assembly of articles is classified under the terms of the Harmonised System in a single heading, the whole constitutes the unit of qualification;

(b) when a consignment consists of a number of identical products classified under the same heading of the Harmonised System, each product must be taken individually when applying the provisions of this section.

2. Where, under general rule 5 of the Harmonised System, packaging is included with the product for classification purposes, it shall be included for the purposes of determining origin.

Article 71

1. By way of derogation from the provisions of Article 69, non-originating materials may be used in the manufacture of a given product, provided that their total value does not exceed 10 % of the ex-works price of the product.

Where, in the list, one or several percentage are given for the maximum value of non-originating materials, such percentages must not be exceeded through the application of the first subparagraph.

2. Paragraph 1 shall not apply to products falling within Chapters 50 to 63 of the Harmonised System.

Article 72

1. By way of derogation from Article 67, for the purposes of determining whether a product manufactured in a beneficiary country which is a member of a regional group originates therein with the meaning of that Article, products originating in any of the countries of that regional group and used in further manufacture in another country of the group shall be treated as if they originated in the country of further manufacture (regional cumulation).

2. The country of origin of the final product shall be determined in accordance with Article 72a.

3. Regional cumulation shall apply to three separate regional groups of beneficiary countries benefiting from the generalised system of preferences:

(a) Group I: Brunei-Darussalam, Cambodia, Indonesia, Laos, Malaysia, Philippines, Singapore, Thailand, Vietnam;

(b) Group II: Bolivia, Colombia, Costa Rica, Ecuador, El Salvador, Guatemala, Honduras, Nicaragua, Panama, Peru, Venezuela;

(c) Group III: Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan, Sri Lanka.

4. The expression ‘regional group’ shall be taken to mean Group I, Group II or Group III, as the case may be.

Article 72a

1. When goods originating in a country which is a member of a regional group are worked or processed in another country of the same regional group, they shall have the origin of the country of the regional group where the last working or processing was carried out, provided that:

(a) the value added there, as defined in paragraph 3, is greater than the highest customs value of the products used originating in any one of the other countries of the regional group, and

(b) the working or processing carried out there exceeds that set out in Article 70 and, in the case of textile products, also those operations referred to at Annex 16.

2. When the conditions of original in paragraph 1(a) and (b) are not satisfied, the products shall have the origin of the country of the regional group which accounts for the highest customs value of the originating products coming from other countries of the regional group.

3. ‘Value added’ means the ex-works price minus the customs value of each of the products incorporated which originated in another country of the regional group.

4. Proof of the originating status of goods exported from a country of a regional group to another country of the same group to be used in further working or processing, or to be re-exported where no further working or processing takes place, shall be established by a certificate of origin Form A issued in the first country.

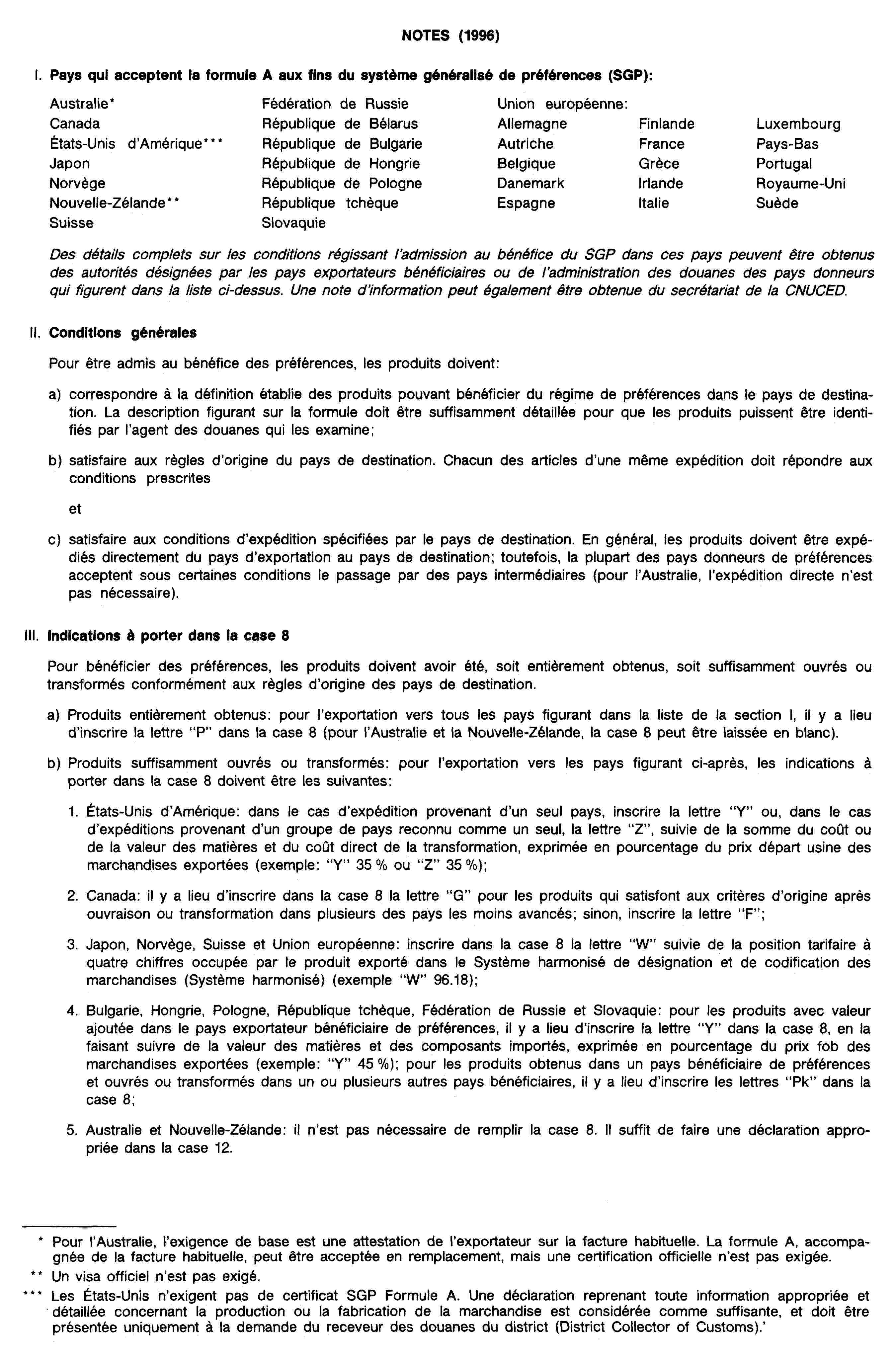

5. Proof of the originating status, acquired or retained under the terms of Article 72, this Article and Article 72b, of goods exported from a country of a regional group to the Community, shall be established by a certificate of origin Form A issued or an invoice declaration made out in that country on the basis of a certificate of origin Form A issued according to the provisions of paragraph 4.

6. The country of origin shall be marked in box 12 of the certificate of origin Form A or on the invoice declaration, that country being:

— in the case of products exported without further working or processing according to paragraph 4, the country of manufacture;

— in the case of products exported after further working or processing, the country of origin as determined in accordance with paragraph 1.

Article 72b

1. Articles 72 and 72a shall apply only where:

(a) the rules regulating trade in the context of regional cumulation, as between the countries of the regional group, are identical to those laid down in this section:

(b) each country of the regional group has undertaken to comply or ensure compliance with the terms of this section and to provide the administrative cooperation necessary both to the Community and to the other countries of the regional group in order to ensure the correct issue of certificates of origin Form A and the verification of certificates of origin Form A and invoice declarations.

This undertaking shall be transmitted to the Commission through the following Secretariats, as the case may be:

(i) Group I: the General Secretariat of the Association of South-East Asian Nations (ASEAN);

(ii) Group II: the Andean Community — Central American Common Market and Panama Permanent Joint Committee on Origin (Comité Conjunto Permanente de Origen Comunidad Andina - Mercado Común Centroamericano y Panamá);

(iii) Group III: the Secretariat of the South Asian Association for Regional Cooperation (SAARC).

2. The Commission shall inform the Member States when the conditions set out in paragraph 1 have been satisfied, in the case of each regional group.

3. Article 78(1)(b) shall not apply to products originating in any of the countries of the regional group when they pass through the territory of any of the other countries of the regional group, whether or not further working or processing take place there.

Article 73

Accessories, spare parts and tools dispatched with a piece of equipment, machine, apparatus or vehicle which are part of the normal equipment and included in the price thereof or which are not separately invoiced, shall be regarded as one with the piece of equipment, machine, apparatus or vehicle in question.

Article 74

Sets, as defined in general rule 3 of the Harmonised System, shall be regarded as originating when all the component products are originating products. Nevertheless, when a set is composed of originating and non-originating products, the set as a whole shall be regarded as originating, provided that the value of the non-originating products does not exceed 15 % of the ex-works price of the set.

Article 75

In order to determine whether a product is an originating product, it shall not be necessary to determine the origin of the following which might be used in its manufacture:

(a) energy and fuel;

(b) plant and equipment;

(c) machines and tools;

(d) goods which do not enter, and which are not intended to enter, into the final composition of the product.

Article 76

1. Derogations from the provisions of this section may be made in favour of the least-developed beneficiary countries benefiting from the generalised system of preferences when the development of existing industries or the creation of new industries justifies them. The least-developed beneficiary countries are listed in the Council Regulations and the ECSC Decision concerning the application of generalised tariff preferences. For this purpose, the country concerned shall submit to the Community a request for a derogation together with the reasons for the request in accordance with paragraph 3.

2. The examination of requests shall, in particular, take into account:

(a) cases where the application of existing rules of origin would affect significantly the ability of an existing industry in the country concerned to continue its exports to the Community, with particular reference to cases where this could lead to business closures;

(b) specific cases where it can be clearly demonstrated that significant investment in an industry could be deterred by the rules of origin and where a derogation encouraging implementation of the investment programme would enable the rules to be satisfied by stages;

(c) the economic and social impact of the decision to be taken especially in respect of employment in the beneficiary countries and the Community.

3. In order to facilitate the examination of requests for derogation, the country making the request shall furnish in support of its request the fullest possible information, covering in particular the points listed below:

— description of the finished product,

— nature and quantity of materials originating in a third country,

— manufacturing process,

— value added,

— the number of employees in the enterprise concerned,

— the anticipated volume of the exports to the Community,

— other possible sources of supply for raw materials,

— reasons for the duration requested,

— other observations.

4. The Commission shall present the derogation-request to the Committee. ►M22 It shall be decided on in accordance with the committee procedure. ◄

5. Where use is made of a derogation, the following phrase must appear in box 4 of the certificate of origin Form A, or on the invoice declaration laid down in Article 89:

‘Derogation - Regulation (EC) No …/…’.

6. The provisions of paragraphs 1 to 5 shall apply to any prolongations.

Article 77

The conditions set out in this section for acquiring originating status must continue to be fulfilled at all times in the beneficiary country or in the Community.

If originating products exported from the beneficiary country or from the Community to another country are returned, they must be considered as non-originating unless it can be demonstrated to the satisfaction of the competent authorities that:

— the products returned are the same as those which were exported, and

— they have not undergone any operations beyond that necessary to preserve them in good condition while in that country or while being exported.

Article 78

1. The following shall be considered as transported direct from the beneficiary country to the Community or from the Community to the beneficiary country:

(a) products transported without passing through the territory of any other country, except in the case of the territory of another country of the same regional group where Article 72 is applied;

(b) products constituting one single consignment transported through the territory of countries other than the beneficiary country or the Community, with, should the occasion arise, trans-shipment or temporary warehousing in those countries, provided that the products remain under the surveillance of the customs authorities in the country of transit or of warehousing and do not undergo operations other than unloading, reloading or any operation designed to preserve them in good condition;

(c) products transported through the territory of Norway or Switzerland and subsequently re-exported in full or in part to the Community or to the beneficiary country, provided that the products remain under the surveillance of the customs authorities of the country of transit or of warehousing and do not undergo operations other than unloading, reloading or any operation designed to preserve them in good condition;

(d) products which are transported by pipeline without interruption across a territory other than that of the exporting beneficiary country or of the Community.

2. Evidence that the conditions specified in paragraph 1(b) and (c) have been fulfilled shall be supplied to the competent customs authorities by the production of:

(a) a single transport document covering the passage from the exporting country through the country of transit; or

(b) a certificate issued by the customs authorities of the country of transit:

— giving an exact description of the products,

— stating the dates of unloading and reloading of the products and, where applicable, the names of the ships, or the other means of transport used, and

— certifying the conditions under which the products remained in the country of transit;

(c) or, failing these, any substantiating documents.

Article 79

1. Originating products sent from a beneficiary country for exhibition in another country and sold after the exhibition for importation into the Community shall benefit, on importation, from the tariff preferences referred to in Article 67, provided that the products meet the requirements of this section entitling them to be recognised as originating in the beneficiary country and provided that it is shown to the satisfaction of the competent Community customs authorities that:

(a) an exporter has consigned these products from the beneficiary country directly to the country in which the exhibition is held and has exhibited them there;

(b) the products have been sold or otherwise disposed of by that exporter to a person in the Community;

(c) the products have been consigned during the exhibition or immediately thereafter to the Community in the state in which they were sent for exhibition;

(d) the products have not, since they were consigned for exhibition, been used for any purpose other than demonstration at the exhibition.

2. A certificate of origin Form A shall be submitted to the Community customs authorities in the normal manner. The name and address of the exhibition must be indicated thereon. Where necessary, additional documentary evidence of the nature of the products and the conditions under which they have been exhibited may be required.

3. Paragraph 1 shall apply to any trade, industrial, agricultural or crafts exhibition, fair or similar public show or display which is not organized for private purposes in shops or business premises with a view to the sale of foreign products, and during which the products remain under customs control.

Subsection 2

Proof of origin

Article 80

Products originating in the beneficiary country shall benefit from the ►C6 tariff preferences ◄ referred to in Article 67, on submission of either:

(a) a certificate of origin Form A, a specimen of which appears in Annex 17; or

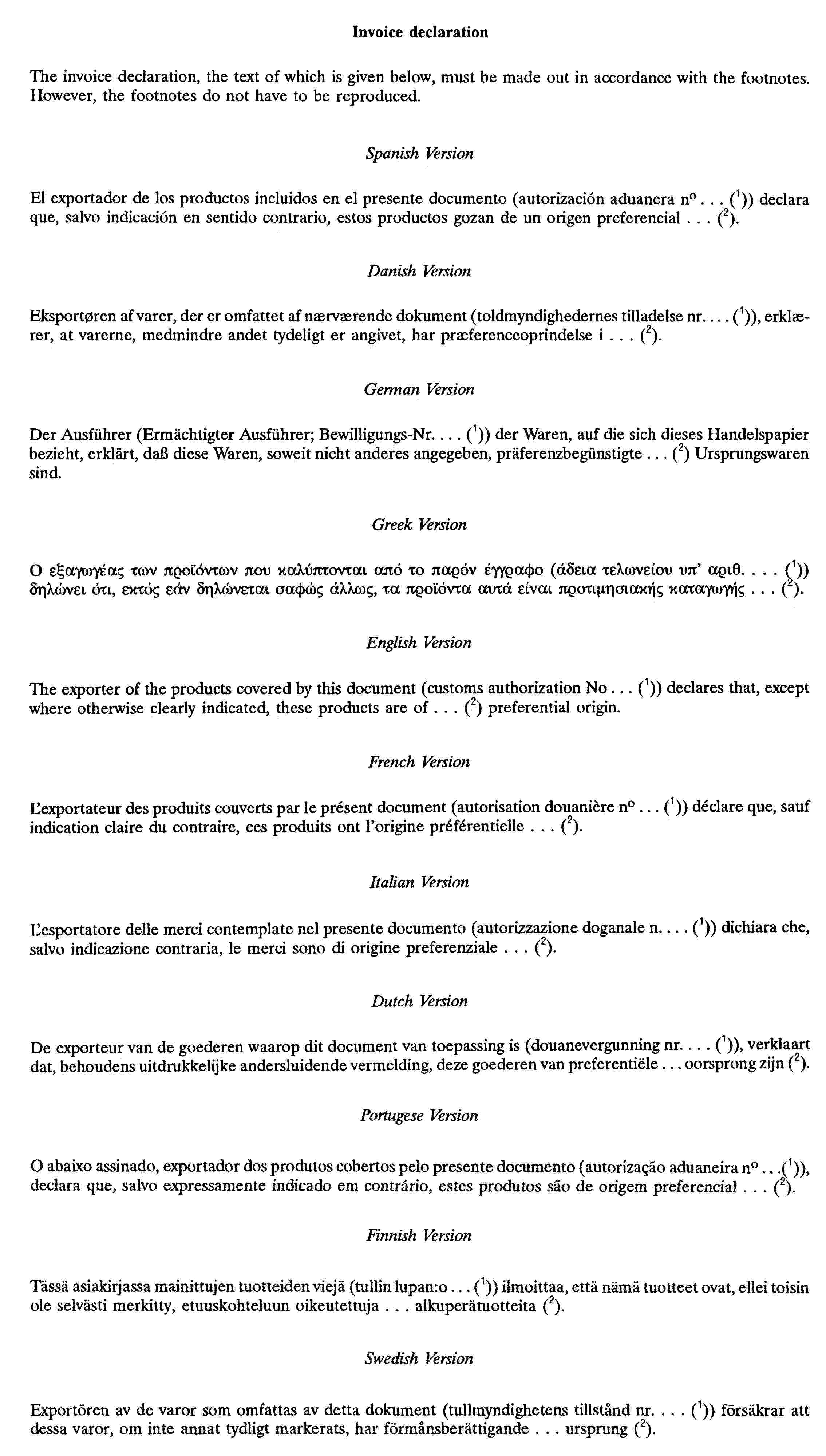

(b) in the cases specified in Article 89(1), a declaration, the text of which appears in Annex 18, given by the exporter on an invoice, a delivery note or any other commercial document which describes the products concerned in sufficient detail to enable them to be identified (hereinafter referred to as the ‘invoice declaration’).

(a)

CERTIFICATE OF ORIGIN FORM A

Article 81

1. Originating products within the meaning of this section shall be eligible, on importation into the Community, to benefit from the tariff preferences referred to in Article 67, provided that they have been transported directly within the meaning of Article 78, on submission of a certificate of origin Form A, issued by the customs authorities or by other competent governmental authorities of the beneficiary country, provided that the latter country:

— has communicated to the Commission the information required by Article 93, and

— assists the Community by allowing the customs authorities of Member States to verify the authenticity of the document or the accuracy of the information regarding the true origin of the products in question.

2. A certificate of origin Form A may be issued only where it can serve as the documentary evidence required for the purposes of the tariff preferences referred to in Article 67.

3. A certificate of origin Form A shall be issued only on written application from the exporter or his authorised representative.

4. The exporter or his authorised representative shall submit with his application any appropriate supporting documents proving that the products to be exported qualify for the issue of a certificate of origin Form A.

5. The certificate shall be issued by the competent governmental authorities of the beneficiary country if the products to be exported can be considered as products originating in that country within the meaning of Subsection 1. The certificate shall be made available to the exporter as soon as the export has taken place or is ensured.

6. For the purposes of verifying whether the conditions set out in paragraph 5 have been met, the competent governmental authorities shall have the right to call for any documentary evidence or to carry out any check which they consider appropriate.

7. It shall be the responsibility of the competent governmental authorities of the beneficiary country to ensure that certificates and applications are duly completed.

8. The completion of box 2 of the certificate of origin Form A shall be optional. Box 12 shall be duly completed by indicating ‘European Community’ or one of the Member States.

9. The date of issue of the certificate of origin Form A shall be indicated in box 11. The signature to be entered in that box, which is reserved for the competent governmental authorities issuing the certificate, shall be handwritten.

Article 82

Where, at the request of the importer and on the conditions laid down by the customs authorities of the importing country, dismantled or non-assembled products within the meaning of general rule 2(a) of the Harmonised System and falling within Section XVI or XVII or heading No 7308 or 9406 of the Harmonised System are imported by instalments, a single proof of origin for such products shall be submitted to the customs authorities on importation of the first instalment.

Article 83

Since the certificate of origin Form A constitutes the documentary evidence for the application of provisions concerning the tariff preferences referred to in Article 67, it shall be the responsibility of the competent governmental authorities of the exporting country to take any steps necessary to verify the origin of the products and to check the other statements on the certificate.

Article 84

Proofs of origin shall be submitted to the customs authorities of the Member States of importation in accordance with the procedures laid down in Article 62 of the Code. The said authorities may require a translation of a proof of origin and may also require the import declaration to be accompanied by a statement from the importer to the effect that the products meet the conditions required for the application of this section.

Article 85

1. By way of derogation from Article 81(5), a certificate of origin Form A may exceptionally be issued after exportation of the products to which it relates, if:

(a) it was not issued at the time of exportation because of errors or involuntary omissions or special circumstances; or

(b) it is demonstrated to the satisfaction of the competent governmental authorities that a certificate of origin Form A was issued but was not accepted at importation for technical reasons.

2. The competent governmental authorities may issue a certificate retrospectively only after verifying that the information supplied in the exporter's application agrees with that in the corresponding export file and that a certificate of origin Form A satisfying the provisions of this section was not issued when the products in question were exported.

3. Box 4 of certificates of origin Form A issued retrospectively must contain the endorsement ‘Issued retrospectively’ or ‘Délivré a posteriori’.

Article 86

1. In the event of the theft, loss or destruction of a certificate of origin Form A, the exporter may apply, to the competent governmental authorities which issued it, for a duplicate to be made out on the basis of the export documents in their possession. Box 4 of a duplicate Form A issued in this way must be endorsed with the word ‘Duplicate’ or ‘Duplicata’, together with the date of issue and the serial number of the original certificate.

2. For the purposes of Article 90b, the duplicate shall take effect from the date of the original.

Article 87