ISSN 1977-0901

Επίσημη Εφημερίδα

της Ευρωπαϊκής Ένωσης

C 40

Έκδοση στην ελληνική γλώσσα

Ανακοινώσεις και Πληροφορίες

63ό έτος

6 Φεβρουαρίου 2020

|

ISSN 1977-0901 |

||

|

Επίσημη Εφημερίδα της Ευρωπαϊκής Ένωσης |

C 40 |

|

|

|

||

|

Έκδοση στην ελληνική γλώσσα |

Ανακοινώσεις και Πληροφορίες |

63ό έτος |

|

Περιεχόμενα |

Σελίδα |

|

|

|

IV Πληροφορίες |

|

|

|

ΠΛΗΡΟΦΟΡΙΕΣ ΠΡΟΕΡΧΟΜΕΝΕΣ ΑΠΟ ΤΑ ΘΕΣΜΙΚΑ ΚΑΙ ΛΟΙΠΑ ΟΡΓΑΝΑ ΚΑΙ ΤΟΥΣ ΟΡΓΑΝΙΣΜΟΥΣ ΤΗΣ ΕΥΡΩΠΑΪΚΗΣ ΕΝΩΣΗΣ |

|

|

|

Ευρωπαϊκή Επιτροπή |

|

|

2020/C 40/01 |

||

|

|

ΠΛΗΡΟΦΟΡΙΕΣ ΣΧΕΤΙΚΑ ΜΕ ΤΟΝ ΕΥΡΩΠΑΪΚΟ ΟΙΚΟΝΟΜΙΚΟ ΧΩΡΟ |

|

|

|

Εποπτεύουσα Αρχή της ΕΖΕΣ |

|

|

2020/C 40/02 |

||

|

2020/C 40/03 |

|

|

V Γνωστοποιήσεις |

|

|

|

ΔΙΚΑΙΟΔΟΤΙΚΕΣ ΔΙΑΔΙΚΑΣΙΕΣ |

|

|

|

Δικαστήριο ΕΖΕΣ |

|

|

2020/C 40/04 |

Δικαστηριο τησ εζεσ Αποφαση του Δικαστηριου της 13ης Νοεμβρίου 2019 στην υπόθεση E-2/19 |

|

|

|

ΔΙΑΔΙΚΑΣΙΕΣ ΠΟΥ ΑΦΟΡΟΥΝ ΤΗΝ ΕΦΑΡΜΟΓΗ ΤΗΣ ΚΟΙΝΗΣ ΕΜΠΟΡΙΚΗΣ ΠΟΛΙΤΙΚΗΣ |

|

|

|

Ευρωπαϊκή Επιτροπή |

|

|

2020/C 40/05 |

Ανακοινωση για την επικείμενη λήξη ορισμένων μέτρων αντιντάμπινγκ |

|

|

|

ΔΙΑΔΙΚΑΣΙΕΣ ΠΟΥ ΑΦΟΡΟΥΝ ΤΗΝ ΕΦΑΡΜΟΓΗ ΤΗΣ ΠΟΛΙΤΙΚΗΣ ΑΝΤΑΓΩΝΙΣΜΟΥ |

|

|

|

Ευρωπαϊκή Επιτροπή |

|

|

2020/C 40/06 |

Προηγούμενη κοινοποίηση συγκέντρωσης (υπόθεση M.9714 — Viacom/beIN/Miramax) Υπόθεση υποψήφια για απλοποιημένη διαδικασία ( 1 ) |

|

|

2020/C 40/07 |

Προηγούμενη κοινοποίηση συγκέντρωσης (Υπόθεση M.9719 — Fairfax Financial Holdings Limited/OMERS Administration Corporation/Riverstone Barbados Limited) Υπόθεση υποψήφια για απλοποιημένη διαδικασία ( 1 ) |

|

|

|

ΛΟΙΠΕΣ ΠΡΑΞΕΙΣ |

|

|

|

Ευρωπαϊκή Επιτροπή |

|

|

2020/C 40/08 |

||

|

2020/C 40/09 |

|

|

|

|

|

(1) Κείμενο που παρουσιάζει ενδιαφέρον για τον ΕΟΧ |

|

EL |

|

IV Πληροφορίες

ΠΛΗΡΟΦΟΡΙΕΣ ΠΡΟΕΡΧΟΜΕΝΕΣ ΑΠΟ ΤΑ ΘΕΣΜΙΚΑ ΚΑΙ ΛΟΙΠΑ ΟΡΓΑΝΑ ΚΑΙ ΤΟΥΣ ΟΡΓΑΝΙΣΜΟΥΣ ΤΗΣ ΕΥΡΩΠΑΪΚΗΣ ΕΝΩΣΗΣ

Ευρωπαϊκή Επιτροπή

|

6.2.2020 |

EL |

Επίσημη Εφημερίδα της Ευρωπαϊκής Ένωσης |

C 40/1 |

Ισοτιμίες του ευρώ (1)

5 Φεβρουαρίου 2020

(2020/C 40/01)

1 ευρώ =

|

|

Νομισματική μονάδα |

Ισοτιμία |

|

USD |

δολάριο ΗΠΑ |

1,1023 |

|

JPY |

ιαπωνικό γιεν |

120,94 |

|

DKK |

δανική κορόνα |

7,4728 |

|

GBP |

λίρα στερλίνα |

0,84444 |

|

SEK |

σουηδική κορόνα |

10,5450 |

|

CHF |

ελβετικό φράγκο |

1,0717 |

|

ISK |

ισλανδική κορόνα |

138,10 |

|

NOK |

νορβηγική κορόνα |

10,1173 |

|

BGN |

βουλγαρικό λεβ |

1,9558 |

|

CZK |

τσεχική κορόνα |

25,055 |

|

HUF |

ουγγρικό φιορίνι |

335,76 |

|

PLN |

πολωνικό ζλότι |

4,2491 |

|

RON |

ρουμανικό λέου |

4,7734 |

|

TRY |

τουρκική λίρα |

6,5975 |

|

AUD |

δολάριο Αυστραλίας |

1,6299 |

|

CAD |

δολάριο Καναδά |

1,4644 |

|

HKD |

δολάριο Χονγκ Κονγκ |

8,5572 |

|

NZD |

δολάριο Νέας Ζηλανδίας |

1,7006 |

|

SGD |

δολάριο Σιγκαπούρης |

1,5202 |

|

KRW |

ουόν Νότιας Κορέας |

1 302,97 |

|

ZAR |

νοτιοαφρικανικό ραντ |

16,2246 |

|

CNY |

κινεζικό ρενμινπί γιουάν |

7,6858 |

|

HRK |

κροατική κούνα |

7,4568 |

|

IDR |

ρουπία Ινδονησίας |

15 036,47 |

|

MYR |

μαλαισιανό ρινγκίτ |

4,5382 |

|

PHP |

πέσο Φιλιππινών |

55,961 |

|

RUB |

ρωσικό ρούβλι |

69,0320 |

|

THB |

ταϊλανδικό μπατ |

34,133 |

|

BRL |

ρεάλ Βραζιλίας |

4,6614 |

|

MXN |

πέσο Μεξικού |

20,4923 |

|

INR |

ινδική ρουπία |

78,4330 |

(1) Πηγή: Ισοτιμίες αναφοράς που δημοσιεύονται από την Ευρωπαϊκή Κεντρική Τράπεζα.

ΠΛΗΡΟΦΟΡΙΕΣ ΣΧΕΤΙΚΑ ΜΕ ΤΟΝ ΕΥΡΩΠΑΪΚΟ ΟΙΚΟΝΟΜΙΚΟ ΧΩΡΟ

Εποπτεύουσα Αρχή της ΕΖΕΣ

|

6.2.2020 |

EL |

Επίσημη Εφημερίδα της Ευρωπαϊκής Ένωσης |

C 40/2 |

Απόφαση αριθ. 085/19/COL της 4ης Δεκεμβρίου 2019 για την κίνηση διαδικασίας σχετικά με ενδεχόμενη χορήγηση κρατικής ενίσχυσης στον όμιλο Remiks σχετικά με υπηρεσίες διαχείρισης αποβλήτων (Υπόθεση 84370)

Πρόσκληση για την υποβολή παρατηρήσεων κατ’ εφαρμογή του άρθρου 1 παράγραφος 2 του μέρους Ι του πρωτοκόλλου 3 της συμφωνίας μεταξύ των κρατών της ΕΖΕΣ για τη σύσταση Εποπτεύουσας Αρχής και Δικαστηρίου σχετικά με θέματα κρατικών ενισχύσεων

(2020/C 40/02)

Με την προαναφερόμενη απόφαση, που αναδημοσιεύεται στην αυθεντική γλώσσα του κειμένου στις σελίδες που ακολουθούν την παρούσα σύνοψη, η Εποπτεύουσα Αρχή της ΕΖΕΣ κοινοποίησε στις νορβηγικές αρχές την απόφασή της να κινήσει τη διαδικασία που προβλέπεται στο άρθρο 1 παράγραφος 2 του μέρους Ι του πρωτοκόλλου 3 της συμφωνίας μεταξύ των κρατών της ΕΖΕΣ για τη σύσταση Εποπτεύουσας Αρχής και Δικαστηρίου, σχετικά με το προαναφερθέν μέτρο ενίσχυσης.

|

EFTA Surveillance Authority |

|

Registry |

|

Rue Belliard 35 |

|

1040 Brussels |

|

BELGIUM |

|

registry@eftasurv.int |

Οι παρατηρήσεις θα κοινοποιηθούν στις νορβηγικές αρχές. Το απόρρητο της ταυτότητας του ενδιαφερόμενου μέρους που υποβάλλει τις παρατηρήσεις μπορεί να ζητηθεί γραπτώς, με μνεία των σχετικών λόγων.

Συνοπτική παρουσίαση

Διαδικασία

|

(1) |

Η Αρχή έλαβε καταγγελία από τον εμπορικό οργανισμό «Norsk Industri» στις 16 Αυγούστου 2016. |

|

(2) |

Κατόπιν αιτημάτων, η Αρχή έλαβε πληροφορίες από τις νορβηγικές αρχές στις 5 Οκτωβρίου 2016, στις 28 Φεβρουαρίου, στις 20 Μαρτίου, στις 22 Αυγούστου, στις 31 Οκτωβρίου, στις 20 Νοεμβρίου 2017 και στις 5 Μαρτίου 2018. |

Περιγραφή των μέτρων

|

(3) |

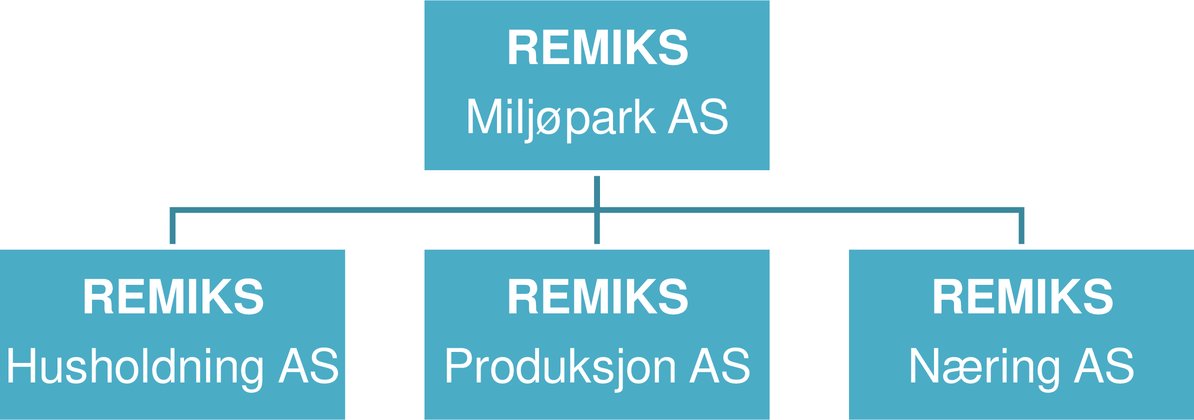

Οι εικαζόμενοι δικαιούχοι ενίσχυσης είναι οι Remiks Miljøpark AS, Remiks Næring AS και Remiks Produksjon AS. |

|

(4) |

Η Remiks Miljøpark AS ανήκει κατά 99,99 % στον Δήμο του Tromsø. Η Remiks Miljøpark AS κατέχει το 100 % των Remiks Næring AS και Remiks Produksjon AS. |

|

(5) |

Η Remiks Miljøpark AS κατέχει επίσης το 100 % της Remiks Huholdning AS. Η εταιρεία αυτή, ωστόσο, παρέχει υπηρεσίες αποκλειστικά στον δήμο του Tromsø και δεν δραστηριοποιείται στην αγορά. Οι αγορές που πραγματοποιεί η Remiks Husholning AS καταλογίζονται στον δήμο. |

|

(6) |

Από τις αρχές του 2010 έως την 1η Φεβρουαρίου του 2017, ο δήμος του Tromsø αγόραζε από τη Remiks Næring AS υπηρεσίες συλλογής αποβλήτων για τα δικά του βιομηχανικά απόβλητα. |

|

(7) |

Ανελλιπώς από τις αρχές του 2010 ο δήμος του Tromsø, στο πλαίσιο του έμμεσου ελέγχου του, αναθέτει στη Remiks Husholning AS να συλλέγει τα οικιακά απόβλητα στον δήμο του Tromsø. Από την 1η Φεβρουαρίου, ο δήμος του Tromsø αναθέτει ανελλιπώς στη Remeks Husholdning AS να συλλέγει επίσης τα βιομηχανικά απόβλητα του δήμου του Tromsø. Η Remiks Husholdning AS παρέχει τις εν λόγω υπηρεσίες για λογαριασμό του δήμου σε τιμή κόστους, πράγμα που σημαίνει ότι αποζημιώνεται με βάση το πλήρες κόστος, χωρίς να συμπεριλαμβάνονται κέρδη. Η Remiks Husholdning AS αναλαμβάνει τη συλλογή των αποβλήτων, αλλά αγοράζει τις απαραίτητες υπηρεσίες επεξεργασίας αποβλήτων από την αδελφή εταιρεία Remiks Produksjon AS. |

|

(8) |

Το 2010 και το 2012, σε συνδυασμό με τη σύσταση του ομίλου Remiks, ο δήμος του Tromsø μεταβίβασε κεφάλαιο, χρέος, κινητά και ακίνητα στη μητρική εταιρεία Remiks Miljøpark AS. |

|

(9) |

Η απόφαση αφορά τα ακόλουθα τρία μέτρα: i) την αγορά από μέρους του δήμου του Tromsø υπηρεσιών συλλογής απορριμμάτων από τη Remiks Næring AS, ii) την αγορά από μέρους της Remiks Husholdning AS υπηρεσιών επεξεργασίας αποβλήτων από τη Remiks Produksjon AS και iii) τις συναλλαγές που πραγματοποίησε ο δήμος του Tromsø υπέρ του ομίλου Remiks το 2010 και το 2012. |

Εκτίμηση των μέτρων

|

(10) |

Για τα μέτρα i) και ii) ανωτέρω, η Αρχή διατηρεί αμφιβολίες κατά πόσον ο δήμος του Tromsø και η Remiks Hushodning AS, αντίστοιχα, κατέβαλαν την τιμή της αγοράς για τις αποκτηθείσες υπηρεσίες. Όσον αφορά το μέτρο iii), η αρχή διατηρεί αμφιβολίες κατά πόσον οι συναλλαγές που πραγματοποίησε ο δήμος του Tromsø υπέρ του ομίλου Remiks πραγματοποιήθηκαν με όρους της αγοράς, σύμφωνα με την αρχή του ιδιώτη επενδυτή σε οικονομία της αγοράς (στο εξής: ΙΕΟΑ). |

|

(11) |

Εάν τα μέτρα συνιστούν κρατική ενίσχυση, δεν έχει τηρηθεί η υποχρέωση κοινοποίησης της ενίσχυσης στην Αρχή πριν από τη θέση της σε ισχύ, σύμφωνα με το άρθρο 1 παράγραφος 3 του μέρους Ι του πρωτοκόλλου 3 της συμφωνίας μεταξύ των κρατών της ΕΖΕΣ για τη σύσταση Εποπτεύουσας Αρχής και Δικαστηρίου. Ως εκ τούτου, η εν λόγω κρατική ενίσχυση θα ήταν παράνομη. |

|

(12) |

Οι νορβηγικές αρχές δεν υπέβαλαν επιχειρήματα που να αποδεικνύουν ότι τα μέτρα, στον βαθμό που συνιστούν κρατική ενίσχυση, θα μπορούσαν να θεωρηθούν συμβατά με τη λειτουργία της συμφωνίας ΕΟΧ. Ως εκ τούτου, η Αρχή διατηρεί αμφιβολίες ως προς τη συμβατότητα και των τριών μέτρων. |

Decision No 085/19/COL of 4 December 2019 to open a formal investigation into potential state aid granted to the Remiks Group related to waste handling services

1. Summary

|

(1) |

The EFTA Surveillance Authority (the «Authority») wishes to inform Norway that, having assessed a complaint relating to (i) Tromsø municipality’s purchase of waste collection services from Remiks Næring AS, (ii) Remiks Husholdning AS’ purchase of waste treatment services from Remiks Produksjon AS, and (iii) transactions from Tromsø municipality to the Remiks Group in 2010 and 2012 (the «measures»), the Authority has doubts as to whether the measures constitute state aid within the meaning of Article 61(1) of the EEA Agreement, and as to the compatibility of the measures with the EEA Agreement. Therefore, the Authority is required to open a formal investigation procedure (1). |

|

(2) |

The complainant has also submitted a separate complaint about alleged violations of the public procurement rules. This decision, however, concerns the state aid complaint only, and remains without prejudice to the ongoing investigation concerning public procurement handled by the Authority’s Internal Market Affairs Directorate (2). |

|

(3) |

The Authority has based its decision on the following considerations. |

2. Procedure

|

(4) |

By letter dated 16 August 2016, Norsk Industri, the Federation of Norwegian Industries, (the «complainant») lodged a complaint against the measures (3). |

|

(5) |

The Norwegian authorities submitted comments to the complaint on 5 October 2016 (4). The Authority requested further information from the Norwegian authorities on 18 January 2017 (5), which was provided by letters dated 28 February (6) and 20 March 2017 (7). |

|

(6) |

The Authority provided the complainant with a preliminary view on the complaint by letter dated 24 May 2017 (8). The Authority received further information from the complainant on 22 June 2017 (9), and from the Norwegian Authorities on 22 August 2017 (10). |

|

(7) |

By letter dated 31 August 2017, the Authority requested further information from the Norwegian authorities (11). By letters dated 31 October and 20 November 2017, the Norwegian authorities replied to the information request (12). |

|

(8) |

By letter dated 16 January 2018, the Authority requested further information from the Norwegian authorities (13), and the Norwegian authorities provided information by letter dated 5 March 2018 (14). |

|

(9) |

The complainant sent additional information by emails of 14 December 2016; 15 September and 13 November 2017; and 12 January, 31 January and 22 May 2018 (15). |

3. Background

3.1 Historical development

|

(10) |

In Norway, waste handling services are regulated by the Pollution Control Act (16). The Act makes a distinction between household waste, which is all waste from the municipalities’ households, and industrial waste, which is the waste from public and private enterprises. |

|

(11) |

Up until 2009, Tromsø municipality organised its waste management services in-house through municipal units and enterprises. In 2009, the municipal council decided to organise the municipality’s waste management in a group of limited liability companies (17). This was done to put an «arm’s length» between the municipality and the activities exposed to competition (18). |

|

(12) |

In June 2009, the municipal council converted the municipal enterprise Tromsø Miljøpark KF (19), which had previously performed waste management services for Tromsø municipality, into Remiks Miljøpark AS (20). In December 2009, three subsidiaries were established under Remiks Miljøpark AS (21): Remiks Husholdning AS («Remiks Husholdning»), Remiks Næring AS («Remiks Næring») and Remiks Produksjon AS («Remiks Produksjon»). Collectively the companies are referred to as the «Remiks Group». |

3.2 Transactions involving the Remiks Group in 2010 and 2012

|

(13) |

On 23 June 2010, Tromsø municipal council made the formal decision to transfer the capital and liabilities that were left in the municipal enterprises Tromsø Miljøpark KF and Remiks Tromsø KF to Remiks Miljøpark AS (22). The transactions involved movables, capital, liabilities, and real estate, including the waste handling facility Remiks Miljøpark (the same name as the parent company) where the Remiks Group companies have their business. The assets were converted into share capital in Remiks Miljøpark AS (23). |

|

(14) |

In 2012, Tromsø municipal council decided to transfer real estate and a loan to Remiks Miljøpark AS, in addition to adjusting the value of the real estate transferred in 2010 (24). In both the preparatory paper (25) and the decision (26), Tromsø municipality specified a requirement for a 9 % return on the investment. |

3.3 The current company structure

|

(15) |

Per November 2019, the Remiks Group is organised as follows (27):

|

|

(16) |

Below is an illustration of the Remiks Group’s structure: |

3.4 Household waste

|

(17) |

The Norwegian Pollution Control Act, section 27a, first paragraph, defines household waste as waste from private households, including large objects such as furniture, etc. |

|

(18) |

Under the Pollution Control Act, sections 29 and 30, the municipalities are obliged to collect and have facilities to treat household waste (29). The costs associated with the waste management are to be covered by a fee, levied on the inhabitants (30). The municipal waste fee are to be calculated based on a self-cost principle; covering the total costs of collecting and handling the waste on behalf of the municipality, without generating a profit for the municipality, in accordance with the Waste Regulation, chapter 15 (31). |

|

(19) |

When Tromsø municipality reorganised its waste handling services and established the Remiks Group in 2010, by way of its control in Remiks Husholdning it instructed Remiks Husholdning to collect the household waste on behalf of the municipality, based on the self-cost principle. Remiks Husholdning collects and sorts the waste. However, it purchases the waste treatment services, consisting of incineration, depositing and recycling, from its sister company Remiks Produksjon. |

3.5 Industrial waste

|

(20) |

The Norwegian Pollution Control Act, section 27a, second paragraph, defines industrial waste as waste from public and private enterprises and institutions. |

|

(21) |

The Norwegian Pollution Control Act does not oblige the municipalities to organise the collection or handling of industrial waste. Any operator can therefore offer these services on the market. However, all producers of industrial waste are obliged to ensure the proper disposal and handling of their waste. Tromsø municipality, as a producer of industrial waste, is therefore obliged to ensure the proper collection and treatment of its own industrial waste, produced by the different municipal units (kindergartens, hospitals, nursing homes, municipal offices, etc.) (32). |

|

(22) |

Before 2010, Tromsø municipality ensured the collection of its own industrial waste through a municipal enterprise (33). When Tromsø municipality reorganised its waste handling services and established the Remiks Group, Remiks Næring took over the collection of the municipality’s own industrial waste (34). Therefore, the agreements for the services were not tendered out or renegotiated. From 2010, Remiks Næring merely continued to provide the same services to the municipality as the municipal enterprise had done before the reorganisation. The only thing that changed was the invoicing system, from internal and centralised to external and decentralised. This meant that each municipal unit (municipal offices, kindergarten, etc.) paid for the service from their budget, and Remiks Næring treated them as individual customers (35). |

|

(23) |

Because of this continuation of the collection services, Remiks Næring and Tromsø municipality never entered into a formal contract for the waste collection services (36). The Norwegian authorities have described the arrangement as an unwritten framework agreement where each municipal unit decided its need for waste collection, and was invoiced separately (37). The Authority will refer to the arrangement between Tromsø municipality and Remiks Næring, regarding the collection of industrial waste, simply as an agreement. |

|

(24) |

In 2016, Tromsø municipality decided to terminate the agreement with Remiks Næring, and concluded a new framework agreement with Remiks Husholdning for the collection of the municipality’s industrial waste, starting 1 February 2017. The agreement was awarded directly, and based on a self-cost principle, meaning that the compensation covers the full costs, but no profits (38). |

|

(25) |

Remiks Husholdning foresaw a total price for the services in 2017 of approximately NOK 8,2 million. This was NOK 3,2 million less than the combined total price all the individual municipal units paid to Remiks Næring in 2016 (39). |

4. Measures covered by the complaint

|

(26) |

The complainant has complained about three separate measures: |

|

(27) |

First, alleged overpayment under the agreement between Tromsø municipality and Remiks Næring for collection of industrial waste for the period running from 2010 until 1 February 2017. |

|

(28) |

Second, alleged overpayment in relation to Remiks Husholdning’s purchase of waste treatment services from its sister company Remiks Produksjon. This agreement has been in force since the establishment of Remiks Husholdning in 2010 and is ongoing. |

|

(29) |

Third, certain transactions from Tromsø municipality to the Remiks Group in 2010 and 2012, which allegedly were not conducted on market terms. |

5. Presence of state aid

5.1 Introduction

|

(30) |

Article 61(1) of the EEA Agreement stipulates that:

«Save as otherwise provided in this Agreement, any aid granted by EC Member States, EFTA States or through State resources in any form whatsoever which distorts or threatens to distort competition by favouring certain undertakings or the production of certain goods shall, in so far as it affects trade between Contracting Parties be incompatible with the functioning of this Agreement.» |

|

(31) |

The qualification of a measure as aid within the meaning of this provision therefore requires the following cumulative conditions to be met: (i) the measure must be granted by the State or through state resources; (ii) it must confer an advantage on an undertaking; (iii) favour certain undertakings (selectivity); and (iv) threaten to distort competition and affect trade. |

5.2 Presence of state resources

5.2.1 Introduction

|

(32) |

For the measure to constitute aid, it must be granted by the State or through state resources. State resources include all resources of the public sector, including resources of intra-state entities (decentralised, federated, regional or other) (40). |

|

(33) |

The transfer of state resources may take many forms, such as direct grants, loans, guarantees, direct investment in the capital of companies and benefits in kind. A positive transfer of funds does not have to occur; waiving revenue that would otherwise have been paid to the state constitutes a transfer of state resources (41). |

5.2.2 Tromsø municipality’s purchase of industrial waste collection services

|

(34) |

The remuneration Tromsø municipality paid to Remiks Næring for the collection of industrial waste came from the budget of Tromsø municipality, as does the remuneration which Remiks Husholdning is currently receiving for the same services. The remuneration therefore constitutes state resources. |

5.2.3 Remiks Husholdning’s purchase of waste treatment services from Remiks Produksjon

|

(35) |

The notion of state aid as expressed in Article 61(1) of the EEA Agreement is to be interpreted widely, therefore it covers not only aid granted directly via the state budget but also compulsory contributions imposed by state legislation. Measures financed through parafiscal charges or compulsory contributions imposed by the State and managed and apportioned in accordance with the provisions of public rules imply a transfer of state resources, even if not administered by the public authorities (42). |

|

(36) |

Remiks Husholdning is financed through the waste fee, which is fixed in accordance with the principles laid down in section 34 of the Pollution Control Act and chapter 15 of the Waste Regulation. The fee is collected by the municipality and disbursed via the municipal budget (43). Thus, the public authorities determine both the size and use of the fee. Further, its legal basis and the way it is collected indicates that it is under the permanent control of public authorities. The fee must therefore be considered to constitute state resources. This Assessment is in line with the Authority’s conclusion in its decision on the financing of municipal waste collectors in Norway in 2013 (44). |

|

(37) |

Further, it must be considered whether Remiks Husholdning’s purchase of waste treatment services from Remiks Produksjon is imputable to Tromsø municipality. That is, whether Tromsø municipality must be regarded as having been involved in the adoption of the measures (45). |

|

(38) |

Remiks Husholdning is indirectly owned by Tromsø municipality and subject to public law, such as the public procurement rules (46). The purchase of waste treatment services from Remiks Produksjon is conducted under the control and instruction of Tromsø municipality, in accordance with the Pollution Control Act. Furthermore, as Remiks Husholdning has been granted an exclusive right to collect the household waste by Tromsø municipality it is not subject to competition on the market, but rather operating under a monopoly (47). |

|

(39) |

Based on this, Remiks Husholdning’s purchase of waste treatment services from Remiks Produksjon appears imputable to Tromsø municipality, so as to constitute state resources for the purposes of Article 61(1) EEA. |

5.2.4 The transactions involving the Remiks Group in 2010 and 2012

|

(40) |

If public authorities or public undertakings provide goods or services at a price below market rates, or invest in an undertaking in a manner that is inconsistent with the market economy operator («MEO») principle, this implies foregoing state resources (as well as the granting of an advantage) (48). |

|

(41) |

Therefore, if the transactions from Tromsø municipality to the Remiks Group in 2010 and 2012 were not conducted on market terms, state resources within the meaning of Article 61(1) of the EEA might have been involved. |

5.3 Undertaking

|

(42) |

Only advantages granted to «undertakings» are subject to state aid law. The concept of an undertaking covers any entity that engages in an economic activity regardless of its status and the way it is financed. Hence, the public or private status of an entity, or the fact a company is partly or wholly publicly owned, has no bearing on whether or not the entity is an «undertaking» (49). |

|

(43) |

An activity is economic in nature where it consists in offering goods and services on a market (50). The assessment of the activity must be based on the factual evidence, and the question is whether there is a market for the services concerned (51). In this regard, it is relevant to consider whether the entities receive compensation for the services, at what level, and whether they face competition from other undertakings (52). |

|

(44) |

Remiks Næring has, since its establishment in 2010, been providing services for collection of industrial waste for remuneration in competition with other undertakings. Based on this, Remiks Næring appears to engage in economic activity so as to constitute an undertaking. |

|

(45) |

Remiks Produksjon offers waste treatment services. The services are offered on the market for remuneration and in competition with other providers. Remiks Produksjon thus appears to engage in economic activity so as to constitute an undertaking. |

|

(46) |

In relation to the transfers from Tromsø municipality to the Remiks Group in 2010 and 2012, the Group must be considered to form one economic unit (53). An entity which, owning controlling shareholdings in a company, actually exercises that control by involving itself directly or indirectly in the management thereof must be regarded as taking part in the economic activity carried on by the controlled undertaking (54). |

|

(47) |

The subsidiaries in the Remiks Group are fully owned by Remiks Miljøpark AS, and the Authority does not have any indications that Remiks Miljøpark AS is not involved in the management of its fully owned subsidiaries. The Authority has preliminarily concluded that both Remiks Næring and Remiks Produksjon undertake economic activity (see immediately above). With this, it is also the Authority’s preliminary conclusion that the Remiks Group, as one economic unit, constitutes an undertaking for the purposes of the application of state aid rules, in so far as it is engaged in the economic activities of Remiks Næring and Remiks Produksjon (55). |

5.4 Advantage

5.4.1 Introduction

|

(48) |

The qualification of a measure as state aid requires that it confers an advantage on the recipient. An advantage, within the meaning of Article 61(1) of the EEA Agreement, is any economic benefit that an undertaking could not have obtained under normal market conditions (56). |

|

(49) |

The measure constitutes an advantage not only if it confers positive economic benefits, but also in situations where it mitigates charges normally borne by the budget of the undertaking. This covers all situations in which economic operators are relieved of the inherent costs of their economic activities (57). |

|

(50) |

Economic transactions carried out by public bodies are considered not to confer an advantage on the counterpart of the agreement, and therefore not to constitute aid, if they are carried out in line with normal market conditions (58). This is assessed pursuant to the MEO principle (59). Therefore, when public authorities purchase a service, it is generally sufficient, to exclude the presence of an advantage, that they pay market price. |

|

(51) |

Whether a transaction is in line with market conditions can be established on the basis of a generally accepted, standard assessment methodology, relying on the available objective, verifiable and reliable data, which should be sufficiently detailed and should reflect the economic situation at the time at which the transaction was decided, taking into account the level of risk and future expectations (60). |

5.4.2 Tromsø municipality’s purchase of waste collection services from Remiks Næring

5.4.2.1

|

(52) |

According to the MEO principle, the decision to carry out a transaction must have been taken on the basis of economic evaluations comparable to those which, in similar circumstances, a rational MEO (with characteristics similar to those of the public body concerned) would have carried out to determine the profitability or economic advantage of the transaction (61). When examining compliance with the principle it is only the information known at the time of the decision which is relevant (62). |

|

(53) |

The purchase of the services through a competitive tender is only one of several methods for ensuring that a transaction does not confer an advantage within the meaning of Article 61(1) of the EEA Agreement. To establish whether a transaction is in line with market conditions, that transaction can be assessed in the light of the terms on which comparable transactions carried out by comparable private operators have taken place in comparable situations (benchmarking) (63) or through a qualified financial assessment (64). |

|

(54) |

Below, the Authority examines the different lines of reasoning that the complainant has brought forward in support of its assertion that Remiks Næring has been overcompensated. |

5.4.2.2

|

(55) |

The complainant alleges that Tromsø municipality has paid disproportionally more than Bodø municipality for similar waste collection services in the same period. |

|

(56) |

The complainant states that Tromsø municipality in 2016 paid to Remiks Næring five times what Bodø municipality paid to Retura Iris AS for collection of industrial waste. Both Tromsø and Bodø are municipalities in the North of Norway, located by the coast, and with a road network interrupted by fjords. The complainant argues that the two municipalities are comparable in size and population density. While there are 5 100 people working in Tromsø municipality at 160 municipal locations, there are 3 100 people working in Bodø municipality, at 100 locations. On that basis, the complainant argues that the price paid in Tromsø should not exceed a price which is proportionally higher (approximately 60–65 % higher) than that paid in Bodø for similar services (65). |

|

(57) |

The Norwegian authorities argue that the agreements in Tromsø and Bodø are different in both size and nature, and that the agreement with Bodø municipality therefore cannot serve as an appropriate benchmark. The municipality of Tromsø has paid a fixed price for waste collection services, based on the size of the bins, regardless of the actual weight. Thus, Remiks Næring carried the risk of the municipality disposing of more waste than budgeted for. The fixed price also covered additional services such as picking up waste that had fallen outside of the bins and additional bags placed next to the bins – in addition to educating the public, raising climate and environmental awareness (66). The municipality of Bodø had an agreement where it paid a price based on the actual weight of waste collected, which means the municipality carried the risk of disposing of more waste than budgeted for. Thus, the scope of and risk allocation under the two agreements are different. |

|

(58) |

Further, the Norwegian authorities argue that the difference in geography, the population density, and municipal locations, including the number of municipal employees, justify different prices for the collection of industrial waste in Tromsø and Bodø. |

|

(59) |

Based on the above, it is the Authority’s preliminary conclusion that benchmarking against Bodø municipality is not an appropriate way to evaluate the market price for the waste collection services (67). |

5.4.2.3

|

(60) |

The complainant argues that the municipality of Tromsø is the largest purchaser of waste collection services in the area concerned, and that it therefore should have been able to negotiate a better price (68). |

|

(61) |

An advantage, within the meaning of Article 61(1) of the EEA Agreement, is any economic benefit, which an undertaking could not have obtained under normal market conditions (69). To establish whether a transaction complies with market conditions, the transaction can be assessed in the light of the terms under which comparable transactions carried out by a comparable private operator would have taken place in a comparable situation (70). |

|

(62) |

The Norwegian authorities have provided documentation indicating that a number of private undertakings have purchased comparable products at the same or a higher price than Tromsø municipality (71). However, it is not clear whether the list includes the majority of Remiks Næring’s other customers, or only a smaller selection. The Authority invites the Norwegian authorities to provide further information on the proportion of other customers that have purchased comparable products to a price equal to or higher that paid by Tromsø municipality. |

5.4.2.4

|

(63) |

The complainant further points out that the total compensation paid to Remiks Næring for the relevant services increased from NOK 7,7 million in 2010 to NOK 11,4 million in 2016, so almost 50 % over six years. |

|

(64) |

The Norwegian authorities have provided documentation showing that the number of inhabitants and municipal employees has increased in the same period, and that the municipality has made several investments in new municipal buildings and units, which has led to an increase in the production of waste. The increase in remuneration to Remiks Næring is also mirrored in a corresponding increase in operating expenditure (72). |

|

(65) |

The Authority, however, has doubts as to whether the information provided can explain a 50 % increase in price over a period of six years. The Authority therefore invites the Norwegian authorities to provide further information on the basis for the increases in the total remuneration paid. |

5.4.2.5

|

(66) |

As of 1 February 2017, Tromsø municipality terminated the agreement with Remiks Næring, and instructed Remiks Husholdning to collect the municipal industrial waste on an in-house basis, at a price not exceeding the costs (self-cost). Remiks Husholdning estimated budget for 2017 was NOK 8,2 million, which is NOK 3,2 million less than the NOK 11,4 million that Remiks Næring received for the services in 2016. |

|

(67) |

The complainant argues that, provided the costs for the waste collection services were the same in 2016 and 2017, Remiks Næring would have had a profit of NOK 3,2 million for the services it provided in 2016. This would entail a margin on these services of 30 %, which is considerably higher than the market standard, which the complainant estimates at 0–8 % (73). |

|

(68) |

The Norwegian authorities argue that the services provided by Remiks Næring under the 2016 agreement and the services provided by Remiks Husholdning under the 2017 agreement are materially different. Under the agreement with Remiks Næring, Tromsø municipality had a fixed price agreement whereby Remiks Næring carried the risk of the municipality disposing of more waste than budgeted for (74). Under the self-cost agreement with Remiks Husholdning, Tromsø municipality entered into an agreement based on the actual weight disposed, which means that the municipality carries the risk of disposing of more waste than budgeted for. The Norwegian authorities argue that the allocation of risk under the two agreements is thus not comparable, and justifies different prices. |

|

(69) |

Further, the Norwegian authorities argue that Remiks Husholdning has been able to take advantage of synergies and efficiency gains when coordinating the collection of industrial waste with the collection of household waste, leading to lower overall costs. It is also argued that Remiks Husholdning is currently at its most efficient, and therefore able to take full advantage of its resources. In the view of the Norwegian authorities, this justifies the difference in price between the remuneration paid to Remiks Næring in 2016 and Remiks Husholdning’s budget for 2017. |

|

(70) |

While the Norwegian authorities have provided explanations seeking to justify the difference in remuneration in 2016 and 2017, the Authority has not been provided with documentation underlying these explanations. The Authority therefore invites the Norwegian authorities to provide documentation evidencing the efficiency gains and synergies said to justify the difference. |

5.4.2.6

|

(71) |

Based on the above, the Norwegian authorities have not at present time provided sufficient evidence showing that the price paid to Remiks Næring for collection of industrial waste, complies with the MEO principle. |

|

(72) |

In light of the above, and in particular in light of the absence of sufficient evidence supporting that the price paid for the collection of industry waste in the period from 2010 to 1 February 2017 was determined in line with normal market conditions, the Authority has formed the preliminary view that Remiks Næring may have received an advantage, within the meaning of Article 61(1) of the EEA Agreement. |

5.4.3 Remiks Husholdning’s purchase of waste treatment services from Remiks Produksjon

|

(73) |

The Norwegian authorities argue that it is impossible for Remiks Husholdning to purchase waste treatment services from any other undertaking than Remiks Produksjon. The reason being that for Remiks Husholdning to purchase waste treatment services from such a third party, the waste that goes through Remiks Husholdning’s optical sorting machine would have to be transported out of Remiks Miljøpark, through Remiks Produksjon’s business area. Remiks Produksjon has not consented to allowing third parties to enter its business area, let alone transport waste through it. This explains why Remiks Husholdning has been purchasing waste treatment services from Remiks Produksjon without tendering out the services (75). |

|

(74) |

The complainant intimates that the purchase of these services, without a tender, has led to Remiks Husholdning paying a price above market price for waste treatment services. |

|

(75) |

The Norwegian authorities argue that the services Remiks Husholdning purchase from Remiks Produksjon are provided on market terms and in accordance with the arm’s length principle in the Limited Liability Companies Act, section 3-9 (76). |

|

(76) |

In determining an appropriate price for Remiks Husholdning’s purchase of waste treatment services from Remiks Produksjon, the two parties looked at the price Remiks Næring paid to Remiks Produksjon for waste treatment services. Remiks Husholdning and Remiks Næring considered that the services Remiks Husholdning purchased were comparable in type and volume to those purchased by Remiks Næring, and that the costs for treating household and industrial waste are similar. |

|

(77) |

The Authority is, however, not convinced that the prices paid by another company in the same group is an appropriate benchmark for establishing market price. |

|

(78) |

In light of the above, and in particular in light of the absence of evidence supporting that the compensation paid to Remiks Produksjon did not lead to overcompensation, the Authority has formed the preliminary view that Remiks Produksjon may have received an advantage within the meaning of Article 61(1) of the EEA Agreement. |

|

(79) |

The Authority invites the Norwegian authorities to provide documentation to substantiate that the compensation paid to Remiks Produksjon in line with normal market conditions (77). |

5.4.4 Transactions to the Remiks Group in 2010 and 2012

|

(80) |

The complainant argues that Tromsø municipality did not require a sufficient return on the transactions from Tromsø municipality to the Remiks Group in 2010 and 2012. |

|

(81) |

With the establishment of the Remiks Group in 2010, Tromsø municipality transferred (a) capital, (b) debt, (c) movables and (d) real estate to the Remiks Group (78). The assets were converted into share capital. The preparatory paper drafted for the purpose of the transactions (79) underlined the importance of complying with the MEO principle. However, it is not clear how the municipality actually ensured compliance with the principle. |

|

(82) |

In 2012, Tromsø municipality transferred (a) real estate and (b) debt to Remiks Miljøpark AS, in addition to (c) adjusting the value of the real estate transferred in 2010 (80). The Tromsø municipal board decided to require a 9 % return. The preparatory paper prepared for the purpose of the transactions underlined the need to determine an appropriate level of return on the basis of the MEO principle. The preparatory paper included a discussion on whether the fact that only 40 % of the Remiks Group’s activities are conducted in a competitive market, while the remaining 60 % are activities for which the municipality cannot obtain a profit, is relevant for the MEO principle, but does not seem to reach a conclusion on this point (81). The preparatory paper found a 9 % return appropriate (82), but did not set out the economic assessment explaining why. |

|

(83) |

The complainant further argues that the 9 % level of return set in 2012 was determined based on only 40 % of the Remiks Group’s turnover originating from the group’s commercial activities (Remiks Næring and Remiks Produksjon). According to the complainant, the division between commercial and non- commercial activity shifted, and in 2016, 58 % of the turnover was linked to the commercial activities in Remiks Næring and Remiks Produksjon (83). Allegedly, as the conditions for setting the relevant rate of return changed, Tromsø municipality should have adjusted the level of return (84). |

|

(84) |

Whether a transaction complies with the MEO principle must be examined on an ex ante basis, having regard to the information available at the time the transactions were decided. The relevant evidence is the information which was available, and the developments which were foreseeable, at the time when the investment decision was made (85). |

|

(85) |

The question is therefore whether, based on the information available at the time, a rational market economy operator (with characteristics similar to Tromsø municipality) would have carried out similar transactions. |

|

(86) |

In relation to the transactions referred to in paragraph (81) above, the Authority invites the Norwegian authorities to provide further information on the transfers and how these comply with the MEO principle. |

|

(87) |

In relation to the transactions referred to in paragraph (82) above, the Authority invites the Norwegian authorities to provide documentation for, and further elaborate on, the assessments forming the basis for an assessment of compliance with the MEO principle, and the relevant level of return. |

5.5 Selectivity

|

(88) |

To be characterised as state aid within the meaning of Article 61(1) of the EEA Agreement, the measure must also be selective in that it favours «certain undertakings or the production of certain goods». Not all measures which favour economic operators fall under the notion of aid, only those which grant an advantage in a selective way to certain undertakings, categories of undertakings or to certain economic sectors. |

|

(89) |

The purchase of services from Remiks Næring and Remiks Produksjon are specific transactions benefitting the two undertakings respectively. |

|

(90) |

Similarly, the transfers to the Remiks Group are specific transactions benefitting the company group. |

|

(91) |

Accordingly, the alleged measures must be considered selective in the sense of Article 61(1) of the EEA Agreement. |

5.6 Effect on trade and distortion of competition

|

(92) |

In order to constitute state aid within the meaning of Article 61(1) of the EEA Agreement, the measures must be liable to distort competition and affect trade between EEA States. |

|

(93) |

Measures granted by the State are considered liable to distort competition when they are liable to improve the position of the recipient compared to other undertakings with which it competes. A distortion of competition within the meaning of Article 61(1) of the EEA Agreement is generally found to exist when the State grants a financial advantage to an undertaking in a liberalised sector where there is, or could be, competition (86). |

|

(94) |

Public support may be liable to distort competition even if it does not help the recipient undertaking to expand or gain market share. It is enough that the aid allows it to maintain a stronger competitive position than it would have had if the aid had not been provided (87). |

|

(95) |

To the extent that the relevant measures have not been carried out in line with normal market conditions, they have conferred an advantage on the relevant undertakings which may have strengthened the undertakings’ position compared to other undertakings competing with them. |

|

(96) |

The measures must also be liable to affect trade between EEA States. Where state aid strengthens the position of an undertaking compared with other undertakings competing in intra-EEA trade, this is assumed to have effect on trade between EEA States (88). |

|

(97) |

The Authority has previously found that public support to waste collection services in Norway is liable to distort competition and affect trade between EEA States (89). Waste collection and treatment is increasingly an international industry. In 2017, Norway exported 1,7 million tons of waste (90). The practice of tendering out waste services also means that undertakings from other EEA States can compete for waste handling contracts in other municipalities (91). |

|

(98) |

The competitive situation is also highlighted in one of the preparatory papers in relation to the establishment of the Remiks Group in 2010. The paper notes an increasing number of undertakings competing on the markets for collection and handling of industrial waste, and highlights that the competition includes both national companies and companies with international owners (92). |

|

(99) |

Thus the Authority cannot exclude that the measures are liable to distort competition and affect trade within the EEA. |

5.7 Conclusion

|

(100) |

Based on the information provided by the Norwegian authorities and the complainant, the Authority cannot exclude that the measures described above may entail state aid within the meaning of Article 61(1) of the EEA Agreement. |

6. Procedural requirements

|

(101) |

Pursuant to Article 1(3) of Part I of Protocol 3 to the Agreement between the EFTA States on the Establishment of a Surveillance Authority and a Court of Justice («Protocol 3»): «The EFTA Surveillance Authority shall be informed, in sufficient time to enable it to submit its comments, of any plans to grant or alter aid. […] The State concerned shall not put its proposed measures into effect until the procedure has resulted in a final decision.» |

|

(102) |

The Norwegian authorities did not notify the measures before putting them into effect. The Authority therefore concludes that, if the measures constitute state aid, the Norwegian authorities will not have respected their obligations pursuant to Article 1(3) of Part I of Protocol 3. |

7. Compatibility of the aid measure

|

(103) |

The Norwegian authorities have not provided any arguments substantiating why the measures, if they were to constitute state aid, should be considered compatible with the functioning of the EEA Agreement. The Authority has also not identified any clear grounds for compatibility. |

|

(104) |

Thus, if the measures constitute state aid, the Authority has doubts as to their compatibility with the functioning of the EEA Agreement |

8. Conclusion

|

(105) |

As set out above, the Authority has doubts as to whether the measures constitute state aid within the meaning of Article 61(1) of the EEA Agreement, and as to their compatibility with the functioning of the EEA Agreement. |

|

(106) |

Consequently, and in accordance Article 4(4) of Part II of Protocol 3, the Authority hereby opens the formal investigation procedure provided for in Article 1(2) of Part I of Protocol 3. The decision to open a formal investigation procedure is without prejudice to the final decision of the Authority, which may conclude that the measures do not constitute state aid, or are compatible with the functioning of the EEA Agreement. |

|

(107) |

The Authority, acting under the procedure laid down in Article 1(2) of Part I of Protocol 3, invites the Norwegian authorities to submit, by 6 January 2020, their comments and to provide all documents, information and data needed for the assessment of the measures in light of the state aid rules. |

|

(108) |

The Norwegian authorities are requested to immediately forward a copy of this decision to the Remiks Group. |

|

(109) |

If this letter contains confidential information which should not be disclosed to third parties, please inform the Authority by 13 December 2019, identifying the confidential elements and the reasons why the information is considered to be confidential. In doing so, please consult the Authority’s Guidelines on Professional Secrecy in State Aid Decisions (93). If the Authority does not receive a reasoned request by that deadline, you will be deemed to agree to the disclosure to third parties and to the publication of the full text of the letter on the Authority’s website: http://www.eftasurv.int/state-aid/state-aid-register/. |

For the EFTA Surveillance Authority

Bente ANGELL-HANSEN

President

Responsible College Member

Frank J. BÜCHEL

College Member

Högni KRISTJÁNSSON

College Member

Carsten ZATSCHLER

Countersigning as Director,

Legal and Executive Affairs

(1) Reference is made to Article 4(4) of Part II of Protocol 3 to the Agreement between the EFTA States on the Establishment of a Surveillance Authority and a Court of Justice.

(2) Case No 78085.

(3) Document No 814858.

(4) Document No 821154.

(5) Document No 840687.

(6) Document No 844198.

(7) Document No 848555.

(8) Document No 854974.

(9) Document No 862433.

(10) Document No 870978.

(11) Document No 870978.

(12) Documents No 880582 and 884931.

(13) Document No 882703.

(14) Document No 901145.

(15) Documents No 831575, 873959, 882172, 896066, 895954 and 914528.

(16) Forurensningsloven, LOV-1981-03-13-6.

(17) Attachments 2, 3 and 4b to letter dated 3.5.18, Documents No 901215, 901211 and 901203; Tromsø municipality’s letter dated 31 Οκτωβρίου 2017, Document No 880582, and Attachment 7 to the letter, Document No 880592.

(18) Preparatory papers from Tromsø municipality’s administration to the municipality council, Attachment 2 to letter dated 5.3.18, Document No 901215.

(19) A municipal enterprise (in Norwegian: kommunalt foretak, shortened KF) is an administrative branch of the central municipality, and not a separate legal entity. Municipal enterprises are regulated by the Local Government Act chapter 11.

(20) Tromsø municipality’s letter, dated 31 Οκτωβρίου 2017, Document No 880582, and Attachments 6 and 7 to the letter, Documents No 880590 and 880592.

(21) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145, and Attachment 4 to the letter, Document No 901219, and Tromsø municipality’s letter dated 31 Οκτωβρίου 2017, Document No 880582 and Attachment 7 to the letter, Document No 880592.

(22) Attachment 8a to Tromsø municipality’s letter dated 5 Μαρτίου 2018, Document No 901189. The transfers were decided on in 2010, but backdated to the establishment of Remiks Miljøpark AS in 2009.

(23) Attachments 4, 4c and 8a to Tromsø municipality’s letter dated 5 Μαρτίου 2018, Documents No 901219, 901205 and 901189.

(24) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145, and attachments 8, 8b, 8c, 8d and 9 to the letter, Documents No 901183, 901181, 901177, 901179 and 901175.

(25) In Norwegian: saksfremlegg.

(26) Attachment 9 to the letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901175.

(27) Based on information obtained at www.purehelp.no 21 Νοεμβρίου 2019.

(28) The 0,01 % ownership by Karlsøy municipality seems to be related to intentions that Tromsø and Karlsøy would cooperate on waste handling, but this seems not to have materialised. See letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145.

(29) This means that any private operator needs an explicit permission from the municipality, in order to provide the service.

(30) The Pollution Control Act, section 34. The fees can be secured through a statutory charge pursuant to the Mortgage Act (panteloven, LOV-1980-02-08-2).

(31) The Waste Regulation (avsfallsforskriften, FOR-2004-06-01-930), chapter 15.

(32) The Pollution Control Act, section 32, first paragraph.

(33) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145.

(34) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145.

(35) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145.

(36) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145.

(37) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145, and letter of 31 Οκτωβρίου 2017, Document No 880582.

(38) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145, and attachment 16 to the letter, Document No 901161.

(39) This is based on calculations conducted by the complainant in letter from the complainant dated 22.6.17, Document No 862433.

(40) See the Authority’s Guidelines on the notion of state aid («NoA») (OJ L 342, 21.12.2017, p. 35), and EEA Supplement No 82, 21 Δεκεμβρίου 2017, p. 1, para. 48.

(41) NoA, para. 51.

(42) See NoA, para. 58; Decision No 306/09/COL of 8 Ιουλίου 2009 on the Norwegian Broadcasting Corporation, section 1.2.1, and judgment in Italy v Commission, 173/73, EU:C:1974:71, para. 16.

(43) The fifth paragraph of section 34 of the Pollution Control Act.

(44) Decision No 91/13/COL of 27 Φεβρουαρίου 2013, on the financing of municipal waste collectors, para. 26.

(45) Judgment in France v Commission, C-482/99, EU:C:2002:294, para. 52.

(46) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145.

(47) Letter from Tromsø municipality, dated 5 Μαρτίου 2018, Document No 901145. See also NoA, para. 43.

(48) NoA, para. 52.

(49) Judgment in Congregación de Escuelas Pías Provincia Betania, C-74/16, EU:C:2017:496, para. 42.

(50) NoA, section 2.1.

(51) Judgment in Havenbedrijf Antwerpen and Maatschappij van de Brugse Zeehaven v Commission, T-696/17, EU:T:2019:652, para. 56.

(52) Case E-29/15 Sorpa [2016] EFTA Ct. Rep. 825, paras 51–64.

(53) NoA, para. 11.

(54) Judgment in AceaElectrabel Produzione v Commission, C-480/09 P, EU:C:2010:787, para. 49.

(55) NoA, para. 11.

(56) NoA, para. 66.

(57) NoA, para. 68.

(58) Judgment in SFEI and others, EU:C:1996:285, C-39/94, paras 60–62.

(59) NoA, para. 76.

(60) NoA, para. 101.

(61) NoA, para. 79.

(62) NoA, para. 78.

(63) NoA, paras 98–100.

(64) NoA, paras 101–105.

(65) The Complaint, dated 15 Αυγούστου 2016, Document No 814858, and Annexes IV–VII to the complaint, Documents No 818909–818911.

(66) Letter from Remiks Group, dated 30 Οκτωβρίου 2017, Document No 880602.

(67) See also the Authority’s letter dated 24 Μαΐου 2017, Document No 854974.

(68) Letter from the complainant, dated 15 Δεκεμβρίου 2016, Document No 831575.

(69) NoA, para. 66.

(70) NoA, para. 98.

(71) Letter from Remiks Næring, dated 29 Σεπτεμβρίου 2016, Document No 821156.

(72) Letter from Tromsø Municipality, dated 5 Μαρτίου 2018, Document No 901145.

(73) Letter from the complainant, dated 13 Νοεμβρίου 2017, Document No 882862.

(74) Further explained in section 7.4.2.2.

(75) Letter from Tromsø municipality, dated 5.3.18, Document No 901145.

(76) Lov om aksjeselskaper, LOV-1997-06-13-44.

(77) NoA, para. 74.

(78) Attachment 8a to letter dated 5 Μαρτίου 2018, Document No 901189.

(79) Attachments 4, 4a, 4b and 4c to the letter from Tromsø municipality dated 5 Μαρτίου 2018, Documents No 901219, 901213, 901203 and 901205.

(80) Attachment 9 to letter dated 5 Μαρτίου 2018, Document No 901175.

(81) The same assessment is included in the preparatory paper in relation to the 2010 transfer, Attachment 4 to the letter from Tromsø municipality dated 5 Μαρτίου 2018, Document No 901219.

(82) Attachments 8, 8b, 8c, 8d to letter dated 5.3.18, Documents No 901183, 901181, 901177 and 901197.

(83) Note that some of the revenues in Remiks Produksjon stem from treating household waste from Remiks Husholdning. The complainant has not explained whether or how this affects the calculations.

(84) The complainant’s letter dated 22 Μαΐου 2018, Document No 914528.

(85) Judgment in Commission v EDF, C-124/10 P, EU:C:2012:318, paras 83–85 and 105; judgment in France v Commission, C-482/99, EU:C:2002:294, paras 71–72.

(86) NoA, para. 187.

(87) NoA, para. 189.

(88) Judgment in Eventech, C-518/13, EU:C:2015:9, para. 66.

(89) Decision No 91/13/COL of 27 Φεβρουαρίου 2013, on the financing of municipal waste collectors, para. 41.

(90) Report from the Nordic Competition Authorities, Competition in the waste management sector, section 3.2.4:

https://konkurransetilsynet.no/wp-content/uploads/2018/08/Nordic-Report-2016-Waste-Management-Sector.pdf

(91) Judgment in Altmark, C-280/00, EU:C:2003:415, paras 78–79.

(92) Preparatory paper 29 Απριλίου 2009, attachment 2 to letter dated 5 Μαρτίου 2018, Document 901215. The Authority’s office translation.

(93) OJ L 154, 8.6.2006, p. 27 and EEA Supplement No 29, 8 Ιουνίου 2006, p. 1.

|

6.2.2020 |

EL |

Επίσημη Εφημερίδα της Ευρωπαϊκής Ένωσης |

C 40/16 |

Απόφαση αριθ. 86/19/COL, της 5 Δεκεμβρίου 2019, για την έναρξη επίσημης έρευνας σχετικά με εικαζόμενη κρατική ενίσχυση που χορηγήθηκε στην Gagnaveita Reykjavíkur

Πρόσκληση για την υποβολή παρατηρήσεων κατ’ εφαρμογή του άρθρου 1 παράγραφος 2 του μέρους Ι του πρωτοκόλλου 3 της συμφωνίας μεταξύ των κρατών της ΕΖΕΣ για τη σύσταση Εποπτεύουσας Αρχής και Δικαστηρίου σχετικά με θέματα κρατικών ενισχύσεων

(2020/C 40/03)

Με την προαναφερόμενη απόφαση, που αναδημοσιεύεται στην αυθεντική γλώσσα του κειμένου στις σελίδες που ακολουθούν την παρούσα σύνοψη, η Εποπτεύουσα Αρχή της ΕΖΕΣ κοινοποίησε στις νορβηγικές αρχές την απόφασή της να κινήσει τη διαδικασία που προβλέπεται στο άρθρο 1 παράγραφος 2 του μέρους Ι του πρωτοκόλλου 3 της συμφωνίας μεταξύ των κρατών της ΕΖΕΣ για τη σύσταση Εποπτεύουσας Αρχής και Δικαστηρίου, σχετικά με το προαναφερθέν μέτρο ενίσχυσης.

Τα ενδιαφερόμενα μέρη μπορούν να υποβάλουν τις παρατηρήσεις τους σχετικά με το εν λόγω μέτρο εντός ενός μηνός από την ημερομηνία δημοσίευσης στην ακόλουθη διεύθυνση:

|

EFTA Surveillance Authority |

|

Registry |

|

Rue Belliard 35 |

|

1040 Bruxelles/Brussel |

|

BELGIQUE/BELGIË |

|

registry@eftasurv.int |

Οι παρατηρήσεις θα κοινοποιηθούν στις ισλανδικές αρχές. Το απόρρητο της ταυτότητας του ενδιαφερόμενου μέρους που υποβάλλει τις παρατηρήσεις μπορεί να ζητηθεί γραπτώς, με μνεία των σχετικών λόγων.

Συνοπτική παρουσίαση

Διαδικασία

Στις 26 Οκτωβρίου 2016, η Αρχή έλαβε καταγγελία από την ισλανδική εταιρεία τηλεπικοινωνιών Síminn hf. σχετικά με εικαζόμενη κρατική ενίσχυση που χορηγήθηκε από την Orkuveita Reykjavíkur (στο εξής: OR) στη θυγατρική της Gagnaveita Reykjavíkur (στο εξής: GR). Η Αρχή έλαβε συμπληρωματικές πληροφορίες και σχόλια από την καταγγέλλουσα με επιστολές και ηλεκτρονικά μηνύματα της 23ης Νοεμβρίου 2016, της 16ης Ιανουαρίου 2017, της 28ης Μαρτίου 2017, της 1ης Ιανουαρίου 2018, της 20ής Απριλίου 2018, της 21ης Σεπτεμβρίου 2018, της 26ης Μαρτίου 2019 και της 13ης Σεπτεμβρίου 2019.

Η Αρχή, κατόπιν αιτημάτων έλαβε πληροφορίες από τις ισλανδικές αρχές με επιστολές της 7ης Φεβρουαρίου 2017, της 22ας Ιουνίου 2017, της 25ης Μαΐου 2018 και της 4ης Ιουνίου 2019.

Περιγραφή των μέτρων

Η καταγγελία αφορά επενδύσεις της OR στην ευρυζωνικότητα από το 1999, έτος ίδρυσης της προκατόχου της GR Lina.Net, μέχρι σήμερα. Ωστόσο, η καταγγελία αφορά κυρίως την περίοδο από 1ης Ιανουαρίου 2007 και εξής, μετά τη σύσταση της GR. Ειδικότερα, η καταγγελία αφορά εικαζόμενη κρατική ενίσχυση που χορηγήθηκε από την OR στην GR με διάφορα μέσα, όπως οι εισφορές κεφαλαίου και ο δανεισμός, και που δεν πραγματοποιήθηκε με όρους της αγοράς.

Η OR ιδρύθηκε την 1η Ιανουαρίου 1999 ως δημόσια επιχείρηση με την απόφαση του δημοτικού συμβουλίου του Reykjavík να συγχωνεύσει τις δραστηριότητες των επιχειρήσεων ηλεκτρισμού και θέρμανσης που ανήκουν στον δήμο. Η OR ανήκει σε τρεις ισλανδικούς δήμους· i) τον δήμο του Reykjavík (93,5 %), ii) τον δήμο του Akranes (5,5 %) και iii) τον δήμο του Borgarbyggð (1 %). Πέντε μέλη του διοικητικού συμβουλίου της OR διορίζονται από το δημοτικό συμβούλιο του Reykjavík και ένα μέλος από το δημοτικό συμβούλιο του Akranes.

Η GR είναι εταιρεία τηλεπικοινωνιών που ιδρύθηκε το 2007. Η GR συστάθηκε ως ανεξάρτητη νομική οντότητα ώστε να υπάρχει συμμόρφωση προς τις απαιτήσεις της Διοίκησης Ταχυδρομείων και Τηλεπικοινωνιών της Ισλανδίας (στο εξής: PTA) σχετικά με τον διαχωρισμό μεταξύ των ανταγωνιστικών και μη ανταγωνιστικών δραστηριοτήτων της OR. Η GR ανήκει εξ ολοκλήρου στην OR. Σκοπός της GR, σύμφωνα με το καταστατικό της, είναι η λειτουργία ενός δικτύου τηλεπικοινωνιών και μετάδοσης δεδομένων.

Η GR είναι καταχωρισμένη επιχείρηση (μετάδοση δεδομένων και υπηρεσία) βάσει του νόμου αριθ. 81/2003 για τις ηλεκτρονικές επικοινωνίες (στο εξής: νόμος ΗΕ). Σκοπός του άρθρου 36 του νόμου ΗΕ είναι να εξασφαλίσει ότι οι ανταγωνιστικές δραστηριότητες στον τομέα των τηλεπικοινωνιών δεν επιδοτούνται μέσω εσόδων από πράξεις που προστατεύονται από αποκλειστικά δικαιώματα ή από άλλα μέσα.

Σύμφωνα με το άρθρο 36 του νόμου ΗΕ, η PTA διασφαλίζει ότι τα έσοδα που προέρχονται από μη ανταγωνιστικούς τομείς δεν επιδοτούν πράξεις στον ανταγωνιστικό τομέα των τηλεπικοινωνιών. Ως εκ τούτου, η PTA έχει επιφορτιστεί με τον έλεγχο των επενδύσεων της OR στην αγορά των τηλεπικοινωνιών και των επιχειρηματικών σχέσεων μεταξύ GR και OR. Οι έρευνες αυτές μπορούν να ξεκινήσουν με πρωτοβουλία της PTA ή κατόπιν καταγγελιών από τα ενδιαφερόμενα μέρη. Επίσης, η GR υποχρεούται να κοινοποιεί ειδικά μέτρα στην PTA.

Από το 2006 έως το 2019, η PTA εξέδωσε εννέα επίσημες αποφάσεις σχετικά με τον οικονομικό διαχωρισμό της OR και της GR. Οι έρευνες της PTA περιελάμβαναν επανεξέταση του επιχειρηματικού σχεδίου της GR, το οποίο πρέπει να ανανεώνεται ετησίως, σύμφωνα με τα πραγματικά χρηματοοικονομικά δεδομένα. Στο πλαίσιο του ελέγχου της, η PTA ελέγχει, για παράδειγμα, κατά πόσον το ποσοστό απόδοσης για τον επενδυτή (OR) συνάδει εν γένει με την αγορά τηλεπικοινωνιών, εξετάζει δε τη διάρθρωση του κεφαλαίου και εκτιμά αν οι τιμές που συμφωνούνται μεταξύ της OR και της GR υπακούν στους όρους της αγοράς.

Σε τρεις περιπτώσεις, η PTA διαπίστωσε συγκεκριμένες παραβάσεις του άρθρου 36 του νόμου ΗΕ. Σε δύο από τις περιπτώσεις αυτές, η PTA διέταξε την ανάκτηση των μέτρων, ενώ στην τρίτη περίπτωση η PTA δεν διέταξε την ανάκτηση των πλεονεκτημάτων.

Οι ισλανδικές αρχές υποστηρίζουν ότι, σε όλες τις δοσοληψίες της με την GR, η OR ενεργεί σύμφωνα με το κριτήριο του ιδιώτη επενδυτή σε οικονομία της αγοράς στο εξής: ΙΕΟΑ) και ότι δεν έχει χορηγηθεί καμία ενίσχυση στην GR. Στο πλαίσιο αυτό, οι ισλανδικές αρχές επισημαίνουν ότι όλα τα μέτρα που αποτέλεσαν αντικείμενο καταγγελιών όσον αφορά τις οικονομικές σχέσεις μεταξύ της OR και της GR αξιολογήθηκαν από την PTA βάσει του άρθρου 36 του νόμου ΗΕ. Σύμφωνα με τις ισλανδικές αρχές, το κριτήριο που εφαρμόζει η PTA είναι συγκρίσιμο με το κριτήριο που εφαρμόζει η Αρχή, προκειμένου να αποφανθεί αν ένα μέτρο είναι σύμφωνο με τους όρους της αγοράς (δηλαδή το κριτήριο ΙΕΟΑ). Οι ισλανδικές αρχές επισήμαναν επίσης ότι η Αρχή έχει ήδη απορρίψει τους ισχυρισμούς της καταγγέλλουσας όσον αφορά τις επενδύσεις της OR στη Lina.Net στην απόφασή της αριθ. 300/11/COL της 5ης Οκτωβρίου 2011.

Εκτίμηση των μέτρων

Υπό το πρίσμα, μεταξύ άλλων, του νομικού καθεστώτος της OR, της συμφωνίας εταιρικής σχέσης της εταιρείας και της σύνθεσης του διοικητικού συμβουλίου της, η Αρχή δεν είναι σε θέση να αποκλείσει ότι τα μέτρα καταλογίζονται στο κράτος και ότι συνεπάγονται τη μεταφορά κρατικών πόρων εάν και στον βαθμό που παρέχουν πλεονεκτήματα στην GR.

Επιπλέον, παρόλο που η GR δεν πωλεί δικές της υπηρεσίες μέσω του οικείου δικτύου οπτικών ινών, προσφέρει σε όλους τους ενδιαφερόμενους παρόχους υπηρεσιών τηλεπικοινωνιών πρόσβαση σε ουδέτερο και ανοικτό δίκτυο. Η Αρχή θεωρεί ότι η παροχή πρόσβασης σε δίκτυο σε τρίτους παρόχους υπηρεσιών σε καθορισμένη τιμή συνιστά οικονομική δραστηριότητα και ότι, ως εκ τούτου, η GR λειτουργεί, όπως φαίνεται, ως επιχείρηση κατά την έννοια του άρθρου 61 παράγραφος 1 της συμφωνίας ΕΟΧ.

Σύμφωνα με την προκαταρκτική άποψη της Αρχής, λαμβανομένης υπόψη, αφενός, της πρακτικής για λήψη αποφάσεων της PTA δυνάμει του άρθρου 36 του νόμου ΗΕ σχετικά με τη χρηματοδότηση της GR και, αφετέρου, του επιπέδου ελέγχου που απαιτείται για την αξιολόγηση των διαφόρων μέτρων, συνάγεται ότι το κριτήριο που εφαρμόζει η PTA δυνάμει του άρθρου 36 διασφαλίζει εν γένει ότι όλες οι συναλλαγές μεταξύ της GR και της OR, ή άλλων συνδεδεμένων εταιρειών, γίνονται με όρους της αγοράς. Η προσέγγιση της PTA μπορεί να μην είναι πανομοιότυπη με την αξιολόγηση του κριτηρίου του ΙΕΟΑ την οποία θα διενεργούσε η Αρχή βάσει των κανόνων του ΕΟΧ για τις κρατικές ενισχύσεις, αλλά, παρά ταύτα, διασφαλίζει το ίδιο αποτέλεσμα, δηλαδή εμποδίζει τις συναλλαγές που δεν πραγματοποιούνται με όρους αγοράς. Ως εκ τούτου, στο παρόν στάδιο, η προκαταρκτική άποψη της Αρχής είναι ότι η PTA παρέχει αξιολόγηση ισοδύναμη με την αξιολόγηση ΙΕΟΑ από την Αρχή.

Σε περίπτωση που η PTA διαπιστώσει εκ των υστέρων παραβάσεις του άρθρου 36 του νόμου ΗΕ, δηλαδή σε περίπτωση που διαπιστώσει ότι μια συγκεκριμένη συναλλαγή δεν πραγματοποιήθηκε με τους όρους της αγοράς, έχει την εξουσία να δώσει εντολή στα μέρη να εξαλείψουν κάθε δυνητικό πλεονέκτημα μέσω της έγκρισης σχετικών μέτρων. Ωστόσο, προκειμένου η PTA να διατάξει την ανάκτηση πλεονεκτήματος, το ασυμβίβαστο μέτρο πρέπει να είναι σαφώς καθορισμένο και αναμφισβήτητο, π.χ. συγκεκριμένο χρηματικό ποσό, όρος σε δανειακή σύμβαση κ.λπ. Επιπλέον, όταν η PTA διατάσσει την ανάκτηση πλεονεκτημάτων που χορηγήθηκαν στην GR, δεν απαιτεί την έντοκη ανάκτησή τους.

Υπάρχουν τρία παραδείγματα κατά τα οποία η ΡΤΑ διαπίστωσε συγκεκριμένες παραβάσεις του άρθρου 36 του νόμου ΗΕ. Σε δύο από τις περιπτώσεις αυτές, η PTA διέταξε την επιστροφή των μέτρων, ενώ στην τρίτη περίπτωση η PTA δεν διέταξε την ανάκτηση των πλεονεκτημάτων. Η Αρχή διαπίστωσε ότι τα μέτρα που αξιολογήθηκαν από την PTA στις περιπτώσεις αυτές είχαν αποφέρει πλεονεκτήματα στην GR τα οποία δεν θα είχε αποκτήσει υπό τις συνήθεις συνθήκες της αγοράς. Επιπλέον, τα εν λόγω πλεονεκτήματα δεν είχαν επιστραφεί πλήρως από την GR.

Ως εκ τούτου, η Αρχή θεωρεί ότι η GR αποκόμισε πλεονέκτημα κατά την έννοια του άρθρου 61 παράγραφος 1 της συμφωνίας ΕΟΧ διότι i) δεν κατέβαλε το επιτόκιο της αγοράς επί πλεονεκτήματος το οποίο έλαβε με προσωρινή αναστολή των πληρωμών τόκων, ii) έλαβε εμμέσως κεφάλαια από την OR για τη διάταξη καλωδιακού δικτύου οπτικών ινών στον δήμο του Ölfus, iii) έλαβε βραχυπρόθεσμα δάνεια από την OR και iv) στις δανειακές συμβάσεις της GR με ιδιώτες δανειστές συμπεριελήφθη όρος για τη διατήρηση της πλειοψηφικής συμμετοχής της OR στην GR.

Σύμφωνα με την προκαταρκτική άποψη της Αρχής, τα εν λόγω μέτρα είναι επιλεκτικά, δεδομένου ότι πρόκειται για μεμονωμένα μέτρα που απευθύνονται μόνο στην GR. Επιπλέον, φαίνεται ότι τα μέτρα είναι ικανά να στρεβλώσουν τον ανταγωνισμό και να επηρεάσουν τις συναλλαγές εντός του ΕΟΧ.

Εάν τα μέτρα συνιστούν κρατική ενίσχυση, δεν έχει τηρηθεί η υποχρέωση κοινοποίησης της ενίσχυσης στην Αρχή πριν από τη θέση της σε ισχύ, η οποία προβλέπεται στο άρθρο 1 παράγραφος 3 του μέρους Ι του πρωτοκόλλου 3 της συμφωνίας μεταξύ των κρατών της ΕΖΕΣ για τη σύσταση Εποπτεύουσας Αρχής και Δικαστηρίου. Μια τέτοιου είδους κρατική ενίσχυση θα ήταν παράνομη.

Οι ισλανδικές αρχές δεν υπέβαλαν επιχειρήματα που να αποδεικνύουν ότι τα μέτρα, στον βαθμό που συνιστούν κρατική ενίσχυση, θα μπορούσαν να θεωρηθούν συμβατά με τη λειτουργία της συμφωνίας ΕΟΧ. Ως εκ τούτου, η Αρχή διατηρεί αμφιβολίες ως προς τη συμβατότητα και των τεσσάρων μέτρων.

Decision No 86/19/COL of 5 December 2019 to open a formal investigation into alleged state aid granted to Gagnaveita Reykjavíkur

1 Summary

|

(1) |

The EFTA Surveillance Authority («the Authority») wishes to inform the Icelandic authorities that some measures covered by the complaint related to Gagnaveita Reykjavíkur («GR») might entail state aid within the meaning of Article 61(1) of the EEA Agreement. Furthermore, the Authority has doubts concerning the compatibility of these measures with the functioning of the EEA Agreement. Therefore, the Authority is required to open a formal investigation procedure into these measures (*) (1). |

|

(2) |

The Authority has based its decision on the following considerations. |

2 Procedure

|

(3) |

By a letter dated 26 October 2016 (2), Síminn hf. («the complainant») made a complaint regarding alleged state aid granted by Orkuveita Reykjavíkur («OR») to its subsidiary GR. By letter dated 7 November 2016, the Authority acknowledged receipt of the complaint (3). By email of 23 November 2016, the complainant submitted further information (4). |

|

(4) |

By letter dated 28 November 2016 (5), the Authority forwarded the complaint and the additional information received to the Icelandic authorities, and invited them to submit information and observations. By email dated 16 January 2017, the Authority received additional information from the complainant (6). By letter dated 7 February 2017, the Icelandic authorities submitted their comments to the Authority (7).The complainant submitted further information by email of 28 March 2017 (8). |

|

(5) |

On 7 June 2017, the Authority discussed the complaint with the Icelandic authorities at the annual package meeting in Reykjavík. On 22 June 2017, the Icelandic authorities provided the Authority with copies of various decisions of the Post and Telecom Administration in Iceland («PTA»), concerning the financing of GR (9). |

|

(6) |

On 25 September 2017, the Authority met with the complainant, at its request, in Reykjavík. On 1 January 2018, the complainant submitted further comments (10). |

|

(7) |

By letter dated 13 March 2018 (11), the Authority informed the complainant about its preliminary assessment that the financing of GR did not raise concerns concerning potential state aid within the meaning of Article 61(1) of the EEA Agreement. By letter dated 20 April 2018 (12), the complainant submitted its response to the Authority’s preliminary assessment. |

|

(8) |

By letter dated 27 April 2018 (13), the Authority forwarded the complainant’s response and additional information received to the Icelandic authorities, and invited them to submit their observations. By letter dated 25 May 2018 (14), the Icelandic authorities submitted their comments. |

|

(9) |

On 6 June 2018, the Authority discussed the complaint with the Icelandic authorities and received a presentation from the PTA at the annual package meeting in Reykjavík (15). By letter dated 21 September 2018 (16), the complainant submitted further information. |

|

(10) |

By letter dated 26 March 2019 (17), the Authority received additional information concerning new developments from the complainant. On 29 April 2019, the Authority requested additional information and clarifications from the Icelandic authorities (18). By letter dated 4 June 2019 (19), the Icelandic authorities replied to the information request and provided the requested information and clarifications. Finally, the complainant submitted additional comments and information by letter dated 13 September 2019 (20).The complaint |

2.1 The complainant - Síminn hf.

|

(11) |

The complainant is a telecommunications company which provides communication solutions to private and corporate clients in Iceland. It offers a range of services, such as: (i) mobile services on its 2G/3G/4G network, (ii) fixed line telephony, (iii) fixed broadband, and (iv) television. The complainant also offers communications and IT solutions for companies of all sizes. The complainant’s subsidiary, Míla ehf., owns and operates a telecommunications network covering the entire country, which builds mostly on fibre optic cables, but also on copper lines and microwave connections. Míla sells its services at a wholesale level to companies with a telecommunications licence in Iceland. |

2.2 Scope of the complaint

|

(12) |

The complaint concerns OR’s investments in fixed broadband from 1999, when GR’s predecessor Lina.Net was established, until today. However, the complaint predominantly concerns the period from 1 January 2007 onwards, following the establishment of GR. In particular, the complaint concerns alleged state aid granted by OR to GR through various means, such as capital injections and lending that was not on market terms. |

|

(13) |

Moreover, the complaint concerns the terms of loans GR has obtained from […]. According to the complainant, the interest rates on GR’s loans are not on market terms that reflect the credit risk inherent in an undertaking such as GR, with a very high debt to EBITDA ratio (21). The complainant maintains that the interest rates offered to GR are directly connected to its ownership, as no market lender would have offered GR such rates without a direct link to its public ownership. |

2.3 Arguments brought forward by the complainant

|

(14) |

The complainant maintains, in general terms, that GR’s activities represent a political rather than a commercial project. It alleges that the company has been operated with a view to enhance competition on the telecommunications market, and that a private investor would not have acted in the same way as OR, when providing loans and capital injections to GR. The complainant moreover alleges that OR has provided GR with several capital injections and loans to finance their operations, which have not been on market terms, as well as more favourable access to OR infrastructure than other market players could receive. |

|

(15) |

According to the complainant, a major part of the alleged unlawful state aid has been in the form of interest rates for loans granted by OR to GR, which have not corresponded to market terms. Furthermore, after the majority of GR’s loans were gradually replaced by loans financed by private lenders (with full replacement at the end of 2017), the interest rates have continued to not correspond to normal market conditions, as OR has provided lenders with a guarantee that it would maintain its majority ownership of GR. The complainant considers that this must be considered as state aid that is incompatible with the functioning of the EEA Agreement. |

|

(16) |

The complainant puts forward that the assessment performed by the PTA under Article 36 of the Electronic Communications Act is substantially different from the assessment conducted by the Authority under the state aid rules. According to the complainant, the application of the said rule by the PTA has consisted in assessing the return on equity. It seems that PTA has not made a detailed comparison with other market investors. The focus has rather been on assessing the financing generally, concentrating on whether the measures provide a direct loss for OR, as opposed to assessing whether the financing would have been provided by an investor operating on the market. |

3 Description of the measures

3.1 Background

3.1.1 OR – Orkuveita Reykjavíkur

|

(17) |