EUR-Lex Access to European Union law

This document is an excerpt from the EUR-Lex website

Document 52019TA1211(01)

Annual report on EU agencies for the financial year 2018 (2019/C 417/01)

Annual report on EU agencies for the financial year 2018 (2019/C 417/01)

Annual report on EU agencies for the financial year 2018 (2019/C 417/01)

OJ C 417, 11.12.2019, p. 1–214

(BG, ES, CS, DA, DE, ET, EL, EN, FR, HR, IT, LV, LT, HU, MT, NL, PL, PT, RO, SK, SL, FI, SV)

|

11.12.2019 |

EN |

Official Journal of the European Union |

C 417/1 |

Annual report on EU agencies for the financial year 2018

(2019/C 417/01)

CONTENTS

| LIST OF EU AGENCIES AND OTHER UNION BODIES COVERED BY THIS REPORT | 4 |

|

CHAPTER 1 |

The EU agencies and the Court’s audit | 6 |

| INTRODUCTION | 6 |

| THE EU AGENCIES | 6 |

| Different types of agencies help the EU design and implement EU policies | 6 |

| Agencies are financed from various sources and under different MFF headings | 9 |

| Budgetary and discharge arrangements are similar for all agencies, except for EUIPO, CPVO and SRB | 15 |

| The EU Agencies Network facilitates inter-agency cooperation and communication with stakeholders | 16 |

| OUR AUDIT | 16 |

| Our mandate covers annual audits, special audits and opinions | 16 |

| Our audits are designed to address key risks | 17 |

| We report suspected fraud to OLAF | 18 |

| We provide information on audits by the Commission’s internal audit service (IAS) and on external evaluation reports | 18 |

|

CHAPTER 2 |

Overview of audit results | 19 |

| INTRODUCTION | 19 |

| RESULTS FROM THE ANNUAL AGENCY AUDITS FOR THE YEAR 2018 ARE POSITIVE OVERALL | 19 |

| ‘Clean’ opinions on the reliability of all agencies’ accounts | 19 |

| ‘Clean’ opinions on the legality and regularity of the revenue underlying all agencies’ accounts | 20 |

| ‘Clean’ opinions on the legality and regularity of the payments underlying the agencies’ accounts, except for EASO | 20 |

| Our observations address areas for improvement in 36 agencies | 22 |

| AUDIT RESULTS FROM OTHER AGENCY-RELATED PRODUCTS ISSUED BY THE COURT | 31 |

| ECA Special report No 29/2018: EIOPA made an important contribution to supervision and stability in the insurance sector, but significant challenges remain | 31 |

| ECA 2017 specific annual report pursuant to Article 92(4) of Regulation (EU) 806/2014 on any contingent liabilities arising as a result of the performance by the Single Resolution Board, the Council and the Commission of their tasks under this Regulation for financial year 2017 | 32 |

| Other ECA special reports also referring to one or more agencies | 32 |

| THE EU AGENCIES NETWORK’S REPLY | 33 |

|

CHAPTER 3 |

Statements of Assurance and other agency-specific audit results | 34 |

|

3.1. |

Information in support of the Statements of Assurance | 34 |

| AGENCIES FUNDED UNDER MFF HEADING 1A — COMPETITIVENESS FOR GROWTH AND JOBS | 36 |

|

3.2. |

Agency for the Cooperation of Energy Regulators (ACER) | 36 |

|

3.3. |

Agency for Support for Body of European Regulators for Electronic Communications (BEREC Office) | 40 |

|

3.4. |

European Centre for the Development of Vocational Training (Cedefop) | 44 |

|

3.5. |

European Aviation Safety Agency (EASA) | 48 |

|

3.6. |

European Banking Authority (EBA) | 52 |

|

3.7. |

European Chemicals Agency (ECHA) | 57 |

|

3.8. |

European Insurance and Occupational Pensions Authority (EIOPA) | 62 |

|

3.9. |

European Institute of Innovation and Technology (EIT) | 66 |

|

3.10. |

European Maritime Safety Agency (EMSA) | 72 |

|

3.11. |

European Union Agency for Network and Information Security (ENISA) | 76 |

|

3.12. |

European Union Agency for Railways (ERA) | 80 |

|

3.13. |

European Securities and Markets Authority (ESMA) | 85 |

|

3.14. |

European Agency for Safety and Health at Work (EU-OSHA) | 90 |

|

3.15. |

European Foundation for the Improvement of Living and Working Conditions (Eurofound) | 94 |

|

3.16. |

European GNSS (Global Navigation Satellite System) Agency (GSA) | 98 |

| AGENCIES FUNDED UNDER MFF HEADING 2 — SUSTAINABLE GROWTH: NATURAL RESOURCES | 102 |

|

3.17. |

European Environment Agency (EEA) | 102 |

|

3.18. |

European Fisheries Control Agency (EFCA) | 106 |

| AGENCIES FUNDED UNDER MFF HEADING 3 — SECURITY AND CITIZENSHIP | 109 |

|

3.19. |

European Union Agency for Law Enforcement Training (CEPOL) | 109 |

|

3.20. |

European Asylum Support Office (EASO) | 113 |

|

3.21. |

European Centre for Disease Prevention and Control (ECDC) | 121 |

|

3.22. |

European Food Safety Authority (EFSA) | 124 |

|

3.23. |

European Institute for Gender Equality (EIGE) | 128 |

|

3.24. |

European Medicines Agency (EMA) | 132 |

|

3.25. |

European Monitoring Centre for Drugs and Drug Addiction (EMCDDA) | 137 |

|

3.26. |

European Agency for the operational management of large-scale IT systems in the area of freedom, security and justice (eu-LISA) | 141 |

|

3.27. |

The European Union’s Judicial Cooperation Unit (Eurojust) | 146 |

|

3.28. |

European Union Agency for Law Enforcement Cooperation (Europol) | 150 |

|

3.29. |

European Union Fundamental Rights Agency (FRA) | 154 |

|

3.30. |

European Border and Coast Guard Agency (Frontex) | 158 |

| AGENCIES FUNDED UNDER MFF HEADING 4 — GLOBAL EUROPE | 164 |

|

3.31. |

European Training Foundation (ETF) | 164 |

| AGENCIES FUNDED UNDER MFF HEADING 5 — ADMINISTRATION | 167 |

|

3.32. |

Euratom Supply Agency (ESA) | 167 |

| SELF-FINANCED AGENCIES | 170 |

|

3.33. |

Community Plant Variety Office (CPVO) | 170 |

|

3.34. |

European Intellectual Property Office (EUIPO) | 174 |

|

3.35. |

Single Resolution Board (SRB) | 181 |

|

3.36. |

Translation Centre for the Bodies of the European Union (CdT) | 186 |

| COMMISSION EXECUTIVE AGENCIES | 190 |

|

3.37. |

Education, Audiovisual and Culture Executive Agency (EACEA) | 190 |

|

3.38. |

Executive Agency for Small and Medium-sized Enterprises (EASME) | 194 |

|

3.39. |

European Research Council Executive Agency (ERCEA) | 198 |

|

3.40. |

Innovation and Networks Executive Agency (INEA) | 202 |

|

3.41. |

Research Executive Agency (REA) | 206 |

|

3.42. |

Consumers, Health, Agriculture and Food Executive Agency (Chafea) | 210 |

LIST OF EU AGENCIES AND OTHER UNION BODIES COVERED BY THIS REPORT

|

Acronym |

Full name |

Location |

|

ACER |

Agency for the Cooperation of Energy Regulators |

Ljubljana, Slovenia |

|

BEREC Office |

Agency for Support for Body of European Regulators for Electronic Communications |

Riga, Latvia |

|

CdT |

Translation Centre for the Bodies of the European Union |

Luxembourg, Luxembourg |

|

Cedefop |

European Centre for the Development of Vocational Training |

Thessaloniki, Greece |

|

CEPOL |

European Union Agency for Law Enforcement Training |

Budapest, Hungary |

|

Chafea |

The Consumers, Health, Agriculture and Food Executive Agency |

Luxembourg, Luxembourg |

|

CPVO |

Community Plant Variety Office |

Angers, France |

|

EACEA |

Education, Audiovisual and Culture Executive Agency |

Brussels, Belgium |

|

EASA |

European Aviation Safety Agency |

Cologne, Germany |

|

EASME |

Executive Agency for Small and Medium-sized Enterprises |

Brussels, Belgium |

|

EASO |

European Asylum Support Office |

Valletta, Malta |

|

EBA |

European Banking Authority |

Paris, France |

|

ECDC |

European Centre for Disease Prevention and Control |

Stockholm, Sweden |

|

ECHA |

European Chemicals Agency |

Helsinki, Finland |

|

EEA |

European Environment Agency |

Copenhagen, Denmark |

|

EFCA |

European Fisheries Control Agency |

Vigo, Spain |

|

EFSA |

European Food Safety Authority |

Parma, Italy |

|

EIGE |

European Institute for Gender Equality |

Vilnius, Lithuania |

|

EIOPA |

European Insurance and Occupational Pensions Authority |

Frankfurt, Germany |

|

EIT |

European Institute of Innovation and Technology |

Budapest, Hungary |

|

ELA |

European Labour Authority |

Bratislava, Slovakia |

|

EMA |

European Medicines Agency |

Amsterdam, The Netherlands |

|

EMCDDA |

European Monitoring Centre for Drugs and Drug Addiction |

Lisbon, Portugal |

|

EMSA |

European Maritime Safety Agency |

Lisbon, Portugal |

|

ENISA |

European Union Agency for Network and Information Security |

Heraklion, Greece |

|

EPPO |

European Public Prosecutor’s Office |

Luxembourg, Luxembourg |

|

ERA |

European Union Agency for Railways |

Valenciennes, France |

|

ERCEA |

European Research Council Executive Agency |

Brussels, Belgium |

|

ESA |

Euratom Supply Agency |

Luxembourg, Luxembourg |

|

ESMA |

European Securities and Markets Authority |

Paris, France |

|

ETF |

European Training Foundation |

Turin, Italy |

|

EUIPO |

European Union Intellectual Property Office |

Alicante, Spain |

|

eu-LISA |

European Agency for the operational management of large-scale IT systems in the area of freedom, security and justice |

Tallinn, Estonia |

|

EU-OSHA |

European Agency for Safety and Health at Work |

Bilbao, Spain |

|

Eurofound |

European Foundation for the Improvement of Living and Working Conditions |

Dublin, Ireland |

|

Eurojust |

The European Union’s Judicial Cooperation Unit |

The Hague, The Netherlands |

|

Europol |

European Union Agency for Law Enforcement Cooperation |

The Hague, The Netherlands |

|

FRA |

European Union Agency for Fundamental Rights |

Vienna, Austria |

|

Frontex |

European Border and Coast Guard Agency |

Warsaw, Poland |

|

GSA |

European Global Navigation Satellite Systems Agency |

Prague, Czech Republic |

|

INEA |

Innovation & Networks Executive Agency |

Brussels, Belgium |

|

REA |

Research Executive Agency |

Brussels, Belgium |

|

SRB |

Single Resolution Board |

Brussels, Belgium |

CHAPTER 1

The EU agencies and the Court’s audit

INTRODUCTION

|

1.1. |

The European Court of Auditors (ECA) was established as the external auditor of the EU’s finances by the Treaty on the Functioning of the European Union (1). In this capacity we act as the independent guardian of the financial interests of the citizens of the Union, notably by helping to improve the EU’s financial management. More information on our work can be found in our activity reports, our annual reports on the implementation of the EU budget, our special reports, our landscape reviews and our opinions on new or updated EU laws or other decisions with financial management implications (2). |

|

1.2. |

Within this mandate we carry out an annual examination of the accounts, and the underlying revenue and payments, for EU institutions, agencies and other Union bodies (3). |

|

1.3. |

This report presents the results of our annual audit of the EU agencies and other Union bodies (collectively referred to as ‘the agencies’) for the financial year 2018, as well as additional agency related audit results from other tasks such as special audits or opinions. The report is structured as follows:

|

THE EU AGENCIES

Different types of agencies help the EU design and implement EU policies

|

1.4. |

Agencies are distinct legal entities set up by secondary legislation to carry out specific technical, scientific or managerial tasks that help the EU institutions design and implement policies. Many are highly visible and have significant influence in important areas of European citizens’ daily life, such as health, safety, security, freedom and justice. A short description of the tasks carried out by each agency is given with their statements of assurance in Chapter 3. In this report we refer to specific agencies by their acronyms, a list of which is provided at the beginning of the report. |

|

1.5. |

There are three types of agencies: decentralised agencies, executive agencies and other bodies. The main characteristics of each are described below. The number of agencies has increased over the years and currently stands at 43 (Box 1.1), including two new agencies which are currently being created. These are the European Public Prosecutor’s Office (EPPO), for which the constituent regulation has already been in force since 2017, and the European Labour Authority (ELA), the founding regulation for which entered into force in August 2019. |

Box 1.1

Increase in the number of agencies

|

Source: |

ECA. |

|

1.6. |

Commission executive agencies are located at the seats of the Commission in Brussels and Luxembourg. Decentralised agencies and other bodies are located across the EU in different Member States as shown in the list of acronyms and in Box 1.2. Their locations are decided by the Council or jointly by the Council and the European Parliament.

Following the United Kingdom’s decision to leave the EU, EMA and EBA were relocated to Amsterdam and Paris respectively during the first half of 2019. The EPPO will be located in Luxembourg and ELA in Bratislava, Slovakia. |

Box 1.2

Agencies’ location across the Member States

|

Source: |

ECA. |

Decentralised agencies address specific policy needs

|

1.7. |

The 34 decentralised agencies (4) play an important role in preparing and implementing EU policies, especially for tasks of a technical, scientific, operational and/or regulatory nature. The intention is to address specific policy needs and to reinforce European cooperation by pooling technical and specialist expertise from the EU and national governments. They have been set up for an indefinite period by Regulation of the Council or of the European Parliament and the Council. |

|

1.8. |

The newly established EPPO is the independent and decentralised prosecution office of the European Union, with the competence to investigate, prosecute and bring to judgment crimes against the EU budget, such as fraud, corruption or serious cross-border VAT fraud. The ELA’s mandate will be to strengthen cooperation between labour market authorities at all levels and better manage cross-border situations, as well as develop further initiatives in support of fair mobility. Both agencies will become subject to our audit from the financial year 2019. |

|

1.9. |

All decentralised agencies work under the control of a board consisting of representatives of the Member States, the Commission and, in some agencies other parties. The board (5) establishes the operational framework the agency has to follow, such as the multi-annual and annual work programmes, draft budgets and staff establishment plans, which are implemented under the responsibility of their (executive) directors. |

Commission executive agencies implement EU programmes

|

1.10. |

The six Commission executive agencies (6) are entrusted with executive and operational tasks relating to one or more EU programmes and were set up for a fixed period of time. They were created by a Commission decision and work under the supervision of Steering Committees appointed by the Commission. They work on the basis of multi-annual and annual work programmes established and implemented under the responsibility of (executive) directors. In contrast to decentralised agencies, their budgets cover staff and administrative expenditure only, while all the operational expenditure that they implement stems from the Commission. The executive agencies’ own budgets therefore represent only a very small part of the budget they actually implement. |

Other bodies have specific mandates

|

1.11. |

The three other bodies are the EIT, ESA and the SRB. |

|

1.12. |

The European Institute of Innovation and Technology (EIT) in Budapest is an independent, decentralised EU body, which pools scientific, business and education resources to boost the Union’s innovation capacity by providing grant funding. It was set up for an indefinite period by the European Parliament and the Council. It is headed by a director and supervised by a Governing Board. |

|

1.13. |

The Euratom Supply Agency (ESA) in Luxembourg was created for an indefinite period by the Council to ensure a regular and equitable supply of nuclear fuels to EU users, in line with the Euratom Treaty. To this end, ESA applies a supply policy based on the principle of equal access of all users to ores and nuclear fuel and focuses on improving the security of supply to users located in the EU, thus also contributing to the viability of the EU nuclear industry. An Advisory Committee composed of members from Member States assists the ESA in carrying out its tasks by giving opinions and providing analysis and information. ESA is headed by a director-general who works in close cooperation with the Commission. |

|

1.14. |

The Single Resolution Board (SRB) is the central resolution authority within the Banking Union and has its seat in Brussels. Its mission is to ensure orderly resolution of failing banks with minimum impact on the real economy, the financial system, and the public finances of the participating Member States and beyond. The SRB is represented by its Chair, who also assumes the role of appointing authority. |

Agencies are financed from various sources and under different MFF headings

|

1.15. |

In 2018, the total budget of all agencies (excluding SRB) amounted to 4,2 billion euros (an increase of 20 % compared with the budget of 3,5 billion euros in 2017) which is equivalent to some 2,9 % of the 2018 EU general budget (2017: 2,7 %) as shown in Box 1.3. The agencies with the highest absolute increase in their budgets from 2017 to 2018 were EIT, EMSA and ECHA, which are financed under MFF heading 1a (Competitiveness for growth and jobs) and eu-LISA, Frontex, EMA, EASO and Europol financed under MFF heading 3 (Security and citizenship). |

|

1.16. |

In addition, the 2018 budget of the SRB amounted to 6,9 billion euros (2017: 6,6 billion euros). This consists of contributions from credit institutions to set up the Single Resolution Fund and to finance the SRB’s administrative expenditure. |

|

1.17. |

The budgets of the decentralised agencies and the other bodies cover their staff, administrative and operational expenditure. The executive agencies implement programmes financed by the Commission’s budget, and their own budgets (in 2018 some 249 million euros in total) only cover their staff and administrative expenditure. The Commission operational budget (commitment appropriations) implemented by the six executive agencies in 2018 amounted to some 11,3 billion euros (2017: 11 billion euros). |

Box 1.3

Agencies’ financing sources for 2018

|

Source: |

EU general budget 2018 and agencies’ budgets 2018, compiled by ECA. |

|

1.18. |

Most agencies, including all executive agencies, are financed almost entirely by the EU general budget. The others are fully or partially financed by fees and charges and by direct contributions from countries participating in their activities: Member States, EFTA countries, etc. For the financial year 2018, agencies’ budgets were mainly financed by some 1,8 billion euros from the EU general budget, some 1 billion euros by fees, charges and contributions from national supervisory authorities and some 1,2 billion euros as revenue assigned by the Commission for the execution of specific (delegated) tasks. Box 1.4 shows a breakdown of the agencies’ budgets by source of revenue. |

Box 1.4

Agencies’ 2018 budgets by source of revenue

|

Source: |

Agencies’ budgets 2018, compiled by ECA. |

|

1.19. |

Box 1.5 below presents the agencies’ 2018 budgets as published in the EU Official Journal. They are broken down by type of expenditure (Title I staff cost, Title II administrative expenditure and Title III operational expenditure together with any other titles used), not by activity. |

Box 1.5

Agencies’ 2018 budgets as published in the EU Official Journal

|

Source: |

Agencies, compiled by ECA. |

|

1.20. |

Most of the agencies do not implement big operational spending programmes or other cost intensive operations, but rather deal with tasks of a technical, scientific and/or regulatory nature. Therefore, in most of the cases their budgets consist of staff and administrative expenditure mainly (Box 1.5). Overall, agencies staff and administrative expenditure represent some 14 % of all EU institutions’ and other bodies’ expenditure of this type (Box 1.6). |

Box 1.6

Staff and administrative expenditure (*1) of EU institutions and bodies (billion euros) in 2018

|

Source: |

2018 consolidated accounts of the EU. |

|

1.21. |

The 1,8 billion euros in contributions from the EU general budget are financed under different MFF headings as illustrated in Box 1.7. |

Box 1.7

Agency financing by EU general budgets’ MFF heading

|

Source: |

EU Multiannual financial framework covering the period 2014-2020 and agencies’ budgets 2018, compiled by ECA. |

|

1.22. |

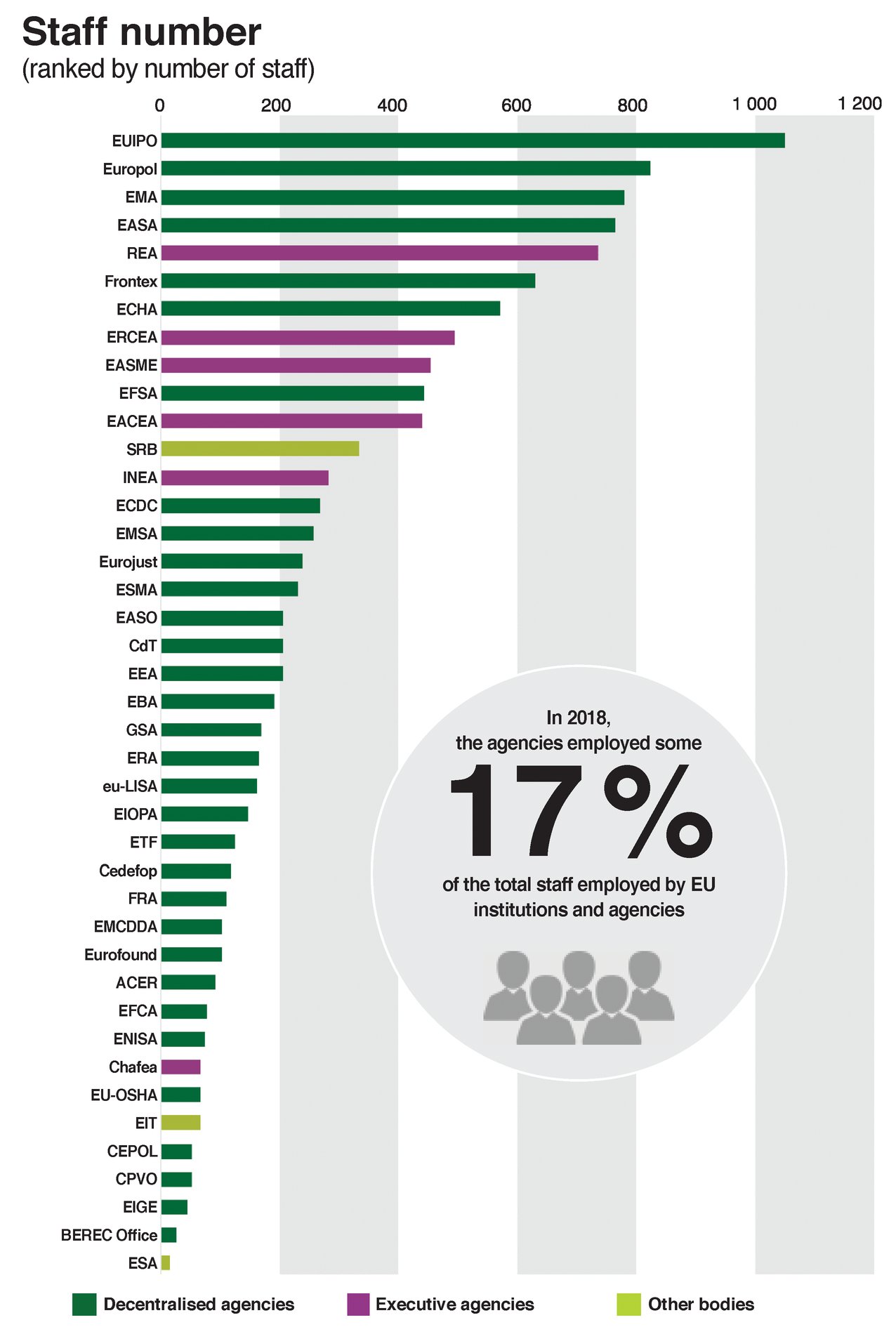

With regard to staff, at the end of 2018 the agencies employed some 11 400 staff (2017: some 11 000), about one fifth of the total staff employed by EU institutions and agencies. These staff figures include officials, temporary and contract staff as well as seconded national experts. The breakdown of the total staff by agency is presented in Box 1.8. In 2018, in addition to their own staff, agencies also used a considerable number of interim staff from temporary work agencies and consultants working in different areas. |

Box 1.8

Numbers of staff per agency at the end of 2018

|

Source: |

Agencies, compiled by ECA. |

Budgetary and discharge arrangements are similar for all agencies, except for EUIPO, CPVO and SRB

|

1.23. |

For most decentralised agencies and other bodies and for all Commission executive agencies, the European Parliament and the Council are responsible for the annual budgetary and discharge procedures. The timeline of the discharge procedure is shown in Box 1.9. |

Box 1.9

Discharge procedure for most agencies

|

Source: |

ECA. |

|

1.24. |

However, one of the three fully self-financed decentralised agencies (EUIPO) is subject to a discharge procedure by its Budget Committee, but not by the European Parliament and the Council. Similarly, the CPVO’s and SRB’s (the other two fully self-financed decentralised agencies) annual budgetary and discharge procedures are the responsibility of their Boards. |

The EU Agencies Network facilitates inter-agency cooperation and communication with stakeholders

|

1.25. |

The EU Agencies Network (EUAN) was set up by the agencies as an inter-agency cooperation platform to enhance the agencies’ visibility, to identify and promote possible efficiency gains and to add value. The EUAN operates on the basis of priorities agreed by the agencies in a 5-year Strategy Agenda (2015-2020) and yearly work programmes specifying activities and deliverables. One important role assigned to EUAN is to ensure efficient communication between the agencies and stakeholders, mainly with the European Institutions. EUAN is chaired by a different agency every year on a rotational basis. |

OUR AUDIT

Our mandate covers annual audits, special audits and opinions

|

1.26. |

As required by Article 287 of the Treaty on the Functioning of the European Union (TFEU), we have audited (7):

|

|

1.27. |

On the basis of the results of our audit, we provide the European Parliament and the Council, or the other discharge authorities referred to in Chapter 3 of this report, with one statement of assurance per agency as to the reliability of the agencies’ accounts and the legality and regularity of the underlying transactions. We complement the statements of assurance with significant audit observations, where appropriate. |

|

1.28. |

Moreover and pursuant to Article 287(4) of the Treaty on the Functioning of the European Union, we also carry out audits and publish special reports on specific topics. We also deliver opinions at the request of one of the other institutions or bodies of the Union, which provide our views on new or updated laws and regulations with a significant impact on EU financial management. See Chapter 2 of this report, section ‘Audit results from other agency-related products issued by the Court’. |

Our audits are designed to address key risks

|

1.29. |

All our audits are designed in such a way that they address the key risks identified. The 2018 annual audit of EU agencies’ accounts and underlying revenue and payments was carried out in response to our risk assessment, which is briefly presented below. |

Risk to the reliability of agencies’ accounts is low in general

|

1.30. |

Overall, we consider the risk to the reliability of the accounts to be low for all agencies. The agencies’ accounts are established by applying the accounting rules adopted by the Commission’s accounting officer. These are based on internationally accepted accounting standards for the public sector. The number of material errors found in the past was small. However, the increasing number of delegation agreements with the Commission assigning specific additional tasks and revenue to agencies represents a challenge in terms of the consistency and transparency of the agencies’ accounting (and budgetary) treatment. |

Risk to the legality and regularity of revenue is low overall, with exceptions

|

1.31. |

The risk to the legality and regularity of revenue underlying the accounts is low for the majority of agencies. These are fully financed by contributions from the EU general budget and, as laid down in their regulations, budgets and resulting revenue are agreed with the budgetary authorities during annual budget procedures. However, risk is medium for the (partly) self-financed agencies (10) where specific regulations are applicable to charging and collecting service fees and contributions from economic operators or cooperating countries. |

Risk to the legality and regularity of payments is medium overall, but varies

|

1.32. |

Risk is generally low. Salaries are administered by the Commission’s PMO service, which the Court audits within the framework of its specific assessments of administrative expenditure. No material errors were found in relation to staff expenditure in recent years. However, where agencies have to recruit a high number of additional staff within a short time, there is a medium to high risk to the legality and regularity of recruitment procedures. |

|

1.33. |

Risk is considered to be medium. Procurements of different kinds of services, with increasing amounts related to IT, involve complex procurement rules and procedures, and agencies’ administrations sometimes do not achieve satisfactory transparency and best value for money. Serious procurement errors affecting the conditions for payments have traditionally been one of the main reasons for qualified audit opinions and observations by the Court. However, office rent is often the main cost category paid on a recurrent basis, and changes usually only occur when agencies move to new premises, so the overall risk is medium. A new risk identified is the increased use of external staff through IT service contracts or from temporary work agencies, for which specific EU and national legal frameworks apply, imposing multiple obligations to user undertakings. |

|

1.34. |

The risk is considered to be low to high. This depends on the specific agencies and the type of operational expenditure they have. In general, procurement-related risks are similar to those in relation to Title II, although the amounts involved can be higher. As far as grants paid under budget Title III are concerned, previous audits found that, while — overall — the agencies’ controls have improved, they are not always fully effective. |

Risk to Sound Financial Management (SFM) is medium overall

|

1.35. |

Risk to SFM is considered to be medium and has been mainly identified in the areas of IT and public procurement. We previously reported findings on the agencies’ diverse IT systems and weaknesses in IT project management, as well as procurement procedures that did not ensure best value for money. |

|

1.36. |

The need to have separate administrative structures and procedures for all agencies constitutes an inherent risk to administrative efficiency. |

Other risks

|

1.37. |

Following the observations raised in previous years and due to the known EU policy developments in certain areas, the risk identified in relation to the level of cooperation of Member States is high for some agencies: Frontex, EASO, ECHA, SRB. |

We report suspected fraud to OLAF

|

1.38. |

We cooperate closely with the European Anti-Fraud Office (OLAF) in fighting fraud against the EU budget. We forward to OLAF any suspicion of fraud, corruption or other illegal activity affecting the EU’s financial interests that we identify in the course of our audit work. These cases are then followed up by OLAF, which decides on any resulting investigation and cooperates as necessary with Member State authorities. |

|

1.39. |

Although our audits are not designed to specifically search for fraud, we detect cases in which we suspect that irregular or fraudulent activity may have taken place. During 2018, we did not communicate to OLAF any such cases of suspected fraud (2017: 3 cases) that we had identified during our audit work. However, on the request of OLAF, we did provide information on several instances of suspected fraud concerning recruitment procedures in different agencies. |

We provide information on audits by the Commission’s internal audit service (IAS) and on external evaluation reports

|

1.40. |

In the agency specific sections of Chapter 3 of this report we also inform about audit reports prepared by the IAS and external evaluations carried out for the agencies in 2018. We did not verify the related audit or evaluation processes. |

CHAPTER 2

Overview of audit results

INTRODUCTION

|

2.1. |

This Chapter presents an overview of the results from the Court’s annual audits of the agencies for the year 2018 as well as other agency-related audit work carried out by the Court in the course of 2018. |

|

The statements of assurance (audit opinions) on the reliability of the agencies’ accounts and the legality and regularity of the revenue and payments underlying these accounts, as well as all matters and observations not calling into question these opinions, are provided in Chapter 3 of this report. |

RESULTS FROM THE ANNUAL AGENCY AUDITS FOR THE YEAR 2018 ARE POSITIVE OVERALL

|

2.2. |

Overall, our audit of the annual accounts of the agencies for the year ended 31 December 2018 and the revenue and payments underlying them confirmed the positive results reported in previous years. |

‘Clean’ opinions on the reliability of all agencies’ accounts

|

2.3. |

We issued unqualified (‘clean’) audit opinions on the accounts of all agencies. In our opinion, these accounts present fairly, in all material respects, the agencies’ financial positions as of 31 December 2018 and the results of their operations and their cash flows for the year then ended, in accordance with the provisions of the applicable financial regulations and the accounting rules adopted by the Commission’s Accounting Officer (11). |

Emphasis of matter paragraphs are important for the understanding of the accounts (EBA, EMA, Frontex and SRB)

|

2.4. |

Emphasis of matter paragraphs draw the readers’ attention to matters of importance that are fundamental to the users’ understanding of the accounts. For the financial year 2018, we address emphasis of matter paragraphs for four agencies: EBA, EMA, Frontex and SRB. |

|

2.5. |

For EBA and EMA, the previously London-based agencies, we draw attention to the fact that they left the UK in 2019 and that their accounts include provisions for the related removal costs. The accounts of EBA for the financial year ended 31 December 2018 include such provisions amounting to 4,7 million euros and a provision for the remaining future contractual payments for the office in London amounting to 10,4 million euros. The accounts for EMA for the financial year ended 31 December 2018 include provisions for removal related costs amounting to 17,8 million euros. The lease agreement for the Agency’s previous premises in London sets a rental period until 2039 with no exit clause. On 20 February 2019, the High Court of Justice of England and Wales ruled against EMA’s request to cancel the lease. However, the lease agreement allows reassigning or subletting the premises to third parties. When the Agency’s final accounts were signed, negotiations between the Agency and potential subtenants were still ongoing and the future net cost of the uncancellable lease agreement was unknown (12). The notes to the Agency’s accounts for the financial year ended 31 December 2018 disclose the full amount of 468 million euros in rent remaining to be paid until 2039, of which an amount of 465 million euros for the lease period after the Agency’s removal to Amsterdam is disclosed as a contingent liability. Moreover, at the time of our audit of EMA, there was no certainty yet about the total loss of staff following the agency’s relocation. This uncertainty represents a significant business continuity risk to the agency. For both EBA and EMA we also referred to possible decreases in revenue following the UK’s departure from the EU. |

|

2.6. |

Concerning Frontex, the Agency managed financing agreements with cooperating countries for operational activities amounting to 171 million euros (189 million euros in 2017), representing 59 % of the Agency’s 2018 budget. A new simplified financing scheme was introduced covering human resources expenditure declared under such financing agreements. In late 2018, the Agency also introduced a new ex-post control system covering all types of expenditure, and modified its system of ex-ante checks embedded in the financial circuits. The Court will assess the impact of these developments in coming audits. However, the reimbursement of equipment-related expenditure (some 35 % of total expenditure for operational activities or some 60 million euros) is still based on actual cost. A pilot project in 2018 to also move to unit cost-based reimbursements for this type of costs has, so far, been unsuccessful in its current form. The Court has consistently reported since 2014 that proof of equipment-related cost claimed by cooperating countries is often insufficient, which was again confirmed by this year’s audit results. Frontex’s ex ante verifications of these costs are ineffective as long as reimbursements of costs which are not substantiated by supporting documents are continued. In addition, as in the previous year, Frontex did not carry out any ex post verifications, further increasing the risk of unjustified cost reimbursements. |

|

2.7. |

Concerning the accounts of the SRB, we point out that administrative appeals or judicial proceedings related to Fund contributions between some credit institutions and national resolution authorities and the Board as well as legal actions brought before the Court of Justice related to decisions on the adoption of resolution schemes were not subject to our audit. Their possible impact on the Board’s financial statements for the financial year ended 31 December 2018 (in particular on contingent liabilities, provisions and liabilities) is subject to a specific annual audit and audit results will be published by 1 December 2019, as stipulated under Article 92(4) of the SRM Regulation. |

‘Clean’ opinions on the legality and regularity of the revenue underlying all agencies’ accounts

|

2.8. |

For all agencies, we issued unqualified (‘clean’) audit opinions on the legality and regularity of the revenue underlying the annual accounts for the year ended 31 December 2018. In our opinion, revenue was legal and regular in all material respects. |

‘Clean’ opinions on the legality and regularity of the payments underlying the agencies’ accounts, except for EASO

|

2.9. |

For 40 agencies, we issued unqualified (‘clean’) audit opinions on the legality and regularity of the payments underlying the annual accounts for the year ended 31 December 2018. In our opinion, payments were legal and regular in all material respects for these agencies. |

|

2.10. |

For EASO we issued a qualified opinion in relation to our findings reported for the financial years 2016 and 2017, when we had concluded that contracts on the provision of interim workers in Greece, travel services to the Office and rent for the Office’s premises in Lesbos are irregular. Payments made in 2018 under these contracts amounted to 3 405 970 euros (4 % of total 2018 payments). Overall, we conclude that the unsatisfactory situation reported for the year 2017 as regards the Office’s governance and internal control arrangements and the legality and regularity of transactions is only slowly improving and that the corrective actions launched by the Office’s management still need to be completed. This is also reflected by the fact that the major procurement procedure carried out by the Office in 2018 (contract volume of some 50 million euros) was again irregular due to major weaknesses in the procedure. There were no payments made yet under the related contracts in 2018. |

Other matter paragraphs address issues of specific importance (EASO, EBA, ECHA, EIOPA, ESMA, SRB and GSA)

|

2.11. |

Other matter paragraphs draw the readers’ attention to particular matters of importance not directly linked to the understanding of the accounts. |

|

2.12. |

For EBA, EIOPA and ESMA we draw attention to the fact that their budgets are financed partly from European Union funds and partly through direct contributions from EU Member States’ supervising authorities and/or supervised entities. It is possible that the Authorities’ revenue will decrease in future as a result of the UK’s decision to leave the EU. |

|

2.13. |

Furthermore, as identified by ESMA already fees charged to credit rating agencies are based on their revenue as legal entities, but not as a group or group of related entities. This creates a quasi-legitimate opportunity to reduce or avoid fees by transferring revenues from credit rating agencies under EU jurisdiction to their related entities outside the EU. The likely financial effect of this loophole in the regulations is unknown. The Authority correctly applied the Regulation, identified the risk and addressed it to the Commission. |

|

2.14. |

For EASO, we continue to draw attention to the fact that as from the end of 2017, the human resources situation at the Office had deteriorated exponentially. The majority of vacancies were still not filled at the end of 2018. Of particular concern is the lack of managers in the administration department. Overall, this situation causes a significant risk to the continuation of the Office’s operations at the current scale. |

|

2.15. |

For ECHA, the Court again emphasises that the Agency is partly self-financed and receives a fee from every company applying for the registration of chemicals as required under the REACH Regulation (13). The Agency calculates and invoices the fees on the basis of information provided by the companies on application. Ex-post verifications by the Agency identified the need for considerable fee corrections, with the total amount of corrections being unknown at the end of 2018. This observation demonstrates the limitations of a system that relies excessively on self-declarations made by applicants. |

|

2.16. |

In the case of the SRB we reiterate that the Single Resolution Fund contributions are calculated on the basis of information provided by credit institutions to the Board through the national resolution authorities. Given that the Single Resolution Mechanism Regulation does not provide for a comprehensive and consistent control framework to ensure the reliability of the information, no checks are carried out at the level of the credit institutions. However, the SRB performs consistency and analytical checks of the information. Furthermore, we noted that the methodology for calculating contributions laid down in the legal framework is very complex, resulting in a risk to accuracy. For confidentiality reasons, the Board cannot release the credit institutions’ data used for the calculation of Fund contributions, which reduces transparency. |

|

2.17. |

For the GSA, we again draw attention to the fact that the procurement procedure for a Framework Contract for the exploitation of the Galileo satellite system during the period 2017 to 2027, amounting to 1,5 billion euros has been challenged by one of the tenderers. The ruling of the European Court of Justice will decide on the legality and regularity of the procurement procedure for the framework contract and all related specific contracts and future payments. The Agency disclosed and explained the matter in the 2018 financial statements, together with the information that 121 million euros, representing 10 % of the 2018 budget including amounts received through delegation agreements, have been paid under the framework contract. |

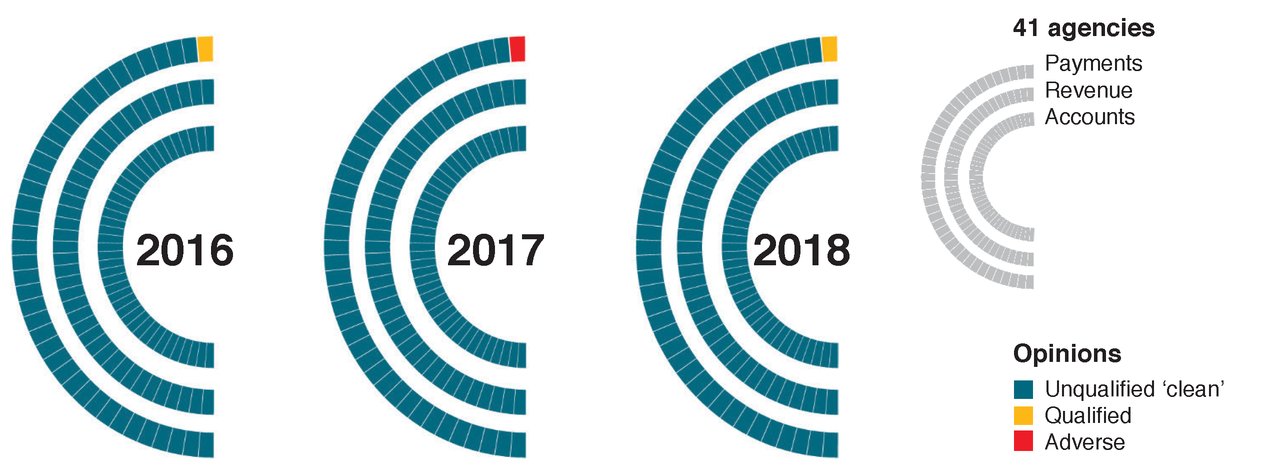

Box 2.1

2016-2018 annual audit opinions on agencies’ accounts, revenue and payments

|

Source: |

ECA. |

Our observations address areas for improvement in 36 agencies

|

2.18. |

In addition to the opinions and accompanying ‘Emphasis of matter’ and ‘Other matter’ paragraphs, we also made around 100 observations concerning 36 agencies to address areas where further improvements are needed. Most of these observations concern shortcomings in public procurement procedures, as was the case in previous years. |

Public procurement management remains the most error-prone area

|

2.19. |

The objective of public procurement rules is to ensure fair competition between economic operators and to achieve the most economically advantageous purchases, thereby respecting the principles of transparency, proportionality, equal treatment and non-discrimination. |

|

2.20. |

Our samples for the 2018 audit included framework, specific and direct contracts covered all agencies. These contracts in 27 agencies worth in total 221 million euros (related 2018 payments of 18 million euros) were affected by public procurement shortcomings of different kinds. However, there is only one agency (EASO) where the irregularities on public procurement procedures and the related payments have led to a qualified audit opinion (see paragraph 2.10). |

|

2.21. |

In relation to the legality aspect (CPVO, EASA, EASO, EIGE, EMCDDA, ERA, EUIPO, eu-LISA, Eurojust, Europol, REA, SRB) recurrent (14) shortcomings refer to the excessive and non-justified use of negotiated procurement procedures without prior publication of contract notice; mistakes in the tender specifications, extensions of contract duration and increases of the initial contract price beyond the legal limit, financial inconsistencies between framework and specific contracts and the conclusion of contracts without evidence on exclusion criteria for tenderers. |

|

Box 2.2 Example of a non-justified use of negotiated procurement procedure without prior publication of contract notice Following a negotiated procurement procedure without prior publication of a contract notice, an agency signed a 3-year IT framework contract (FWC) with a company which had provided the same services under a previous FWC. The FWC was signed for a total amount of 450 000 euros (150 000 euros per year). Under the Financial Regulation, such simplified procedure is only acceptable under specific circumstances which were not substantiated by the agency. |

|

2.22. |

In relation to sound financial management observations (BEREC Office, Cedefop, CEPOL, EBA, ECHA, EEA, EIOPA, EMCDDA, ESMA, ETF, EUIPO, Frontex), recurrent (15) shortcomings refer to the excessive dependency on contractors, external consultancy and interims; to the use of inadequate award criteria and the conclusion of contracts with abnormally low tenderers without reasonable justification. Several EU agencies have outsourced, extensively, regular activities and occasionally core business activities, which weakens the internal expertise and control over contract execution. Some EU agencies have not ensured a sound balance between price and quality award criteria, namely because the price components did not have a sufficient competitive nature. In other cases, contracts were awarded to tenderers whose prices were significantly lower than those of other candidates, without having analysed the reasons for the potentially abnormally low offers and without having obtained the formal and substantial evidence enabling such derogation. Ultimately, these weaknesses may impair fair competition and the achievement of best value for money procurements. |

|

Box 2.3 Example of dependency on contractors Under several framework contracts with the same company, an agency paid 793 000 euros for the purchase of various types of services (clerical and secretarial support, organisation of events, wellbeing and integration of staff, etc.). This amount represents 37 % of its non-salary related 2018 budget, indicating that the agency is dependent on external resources and on one company. This creates a risk to business continuity. |

|

2.23. |

In relation to procurement related internal controls observations (ECDC, EFCA, EIT, EMSA, ERA, Eurofound), we refer to an inter-institutional framework contract for the provision and maintenance of IT equipment put in place by the Commission and used by several agencies. The terms of this contract were weak in so far as they allowed the purchase of items not specifically mentioned therein and not subject to an initial competitive procedure. It also allowed the contractor to charge uplifts on the prices of items purchased from other suppliers. Although agencies have no power to change the basic contractual arrangements, we found that their related ex ante controls did not always check that the contractor offered the most suitable solutions for competitive prices, nor the accuracy of the up-lifts charged by the contractor. The weak contractual arrangements in combination with the partially weak internal controls did not ensure best value for money procurements. The framework contract has expired in the meantime and the succeeding contract is better designed, thereby addressing our finding. |

|

Actions to be taken 1 Public procurement errors remain the most frequent type of errors detected through our audits. The agencies are encouraged to further improve their public procurement procedures, ensuring full compliance with the applicable rules and best value for money procurements. |

|

Actions to be taken 2 When using inter-institutional contracts, agencies remain responsible for the application of public procurement principles for their specific purchases. Agencies’ internal controls must ensure they are respected. |

The use of framework contracts by some of the agencies may limit competition

|

2.24. |

Framework contracts are agreements with suppliers to establish terms governing specific purchases during the life of the agreement. They are used for a precisely defined subject, but where the exact quantities and delivery times cannot be indicated in advance. The main reason for the use of framework contracts is to achieve administrative efficiency and economies of scale. However, we identified cases (EASA and EUIPO) where the use of large framework contracts covering a multitude of different services caused a risk to competition. This is particularly the case when the actual services to be provided during the lifetime of the agreement cannot be clearly specified at the time of the initial procurement procedures, which is typically the case for services like IT and business consulting. |

|

Box 2.4 Example of a FWC lacking specifications For the procurement of data analytics services for a volume of up to 5 million euros, one agency chose to use a framework contract with a single operator resulting from an open procedure. However, the terms used in the framework contract were not specific enough to allow fair competition, because the concrete requirements concerning the services to be provided were not yet known at the time of the procurement procedure. According to the rules of application of the Financial Regulation, in such circumstances, the contracting authority has to award a framework contract to multiple operators and a competitive procedure between the selected contractors must be held for the specific purchases. |

|

2.25. |

Box 2.5 shows values of FWC signed by the agencies between 2015 and 2018. In 2018, the agencies signed multi-annual framework contracts totalling some 1,1 billion euros (16). |

Box 2.5

Total value of FWCs signed between 2015-2018 (billion euros)

|

Source: |

Agencies’ network, compiled by ECA. |

|

Actions to be taken 3 The use of framework contracts must not hinder a fair and competitive procurement procedure. Competition on price must take into account all major price elements, such as unit prices and the related quantity of units to be charged for the specific services. |

|

2.26. |

The 35 decentralised agencies and other bodies, together with the eight EU joint undertakings (EU bodies), also push for increased administrative efficiency and economies of scale through an increased use of joint procurement procedures where two or more agencies and joint undertakings in need of similar services carry out a procurement procedure jointly and together they become owners of the contract (Box 2.6). The number of joint calls for tenders launched by EU bodies increased from 1 to 17 between 2014 and 2018 and by the end of 2018 30 EU bodies had participated in one or more joint procurements (17). However, despite the promising trend, attempts for joint procurement procedures were not always successful, for instance due to inadequate market analysis. |

Box 2.6

Substantive increase in number of joint calls

|

Source: |

Agencies’ network, compiled by ECA. |

|

Box 2.7 Examples of unsuccessful joint procurements In the absence of appropriate market analysis for two pan-European calls for telecommunication and for banking services, no compliant offers covering the required local markets were received and the procedures failed, causing administrative inefficiency. Also, despite the common location of two agencies, the joint procurement procedure for their new premises was not successful. |

|

Actions to be taken 4 Agencies are encouraged to continue using joint procurement procedures or inter-institutional framework contracts, in order to achieve efficiency gains and economies of scale. For new agencies like EPPO and ELA, participating in joint procurements instead of establishing their own, stand-alone contracts, can be particularly beneficial. However, before launching joint procurement procedures and spending the related administrative efforts, market analysis should proof the feasibility of a joint procedure. |

Temporary agency workers and consultants are not always used in compliance with the legal framework

|

2.27. |

In 2017, the Court issued a rapid case review (18) on how EU institutions and agencies implemented the commitment made to cut 5 % of staff in their establishment plans during the period 2013-2017 (for agencies 2014-2018). For the agencies, we concluded that the 5 % reduction had been implemented, albeit with some delays. |

|

2.28. |

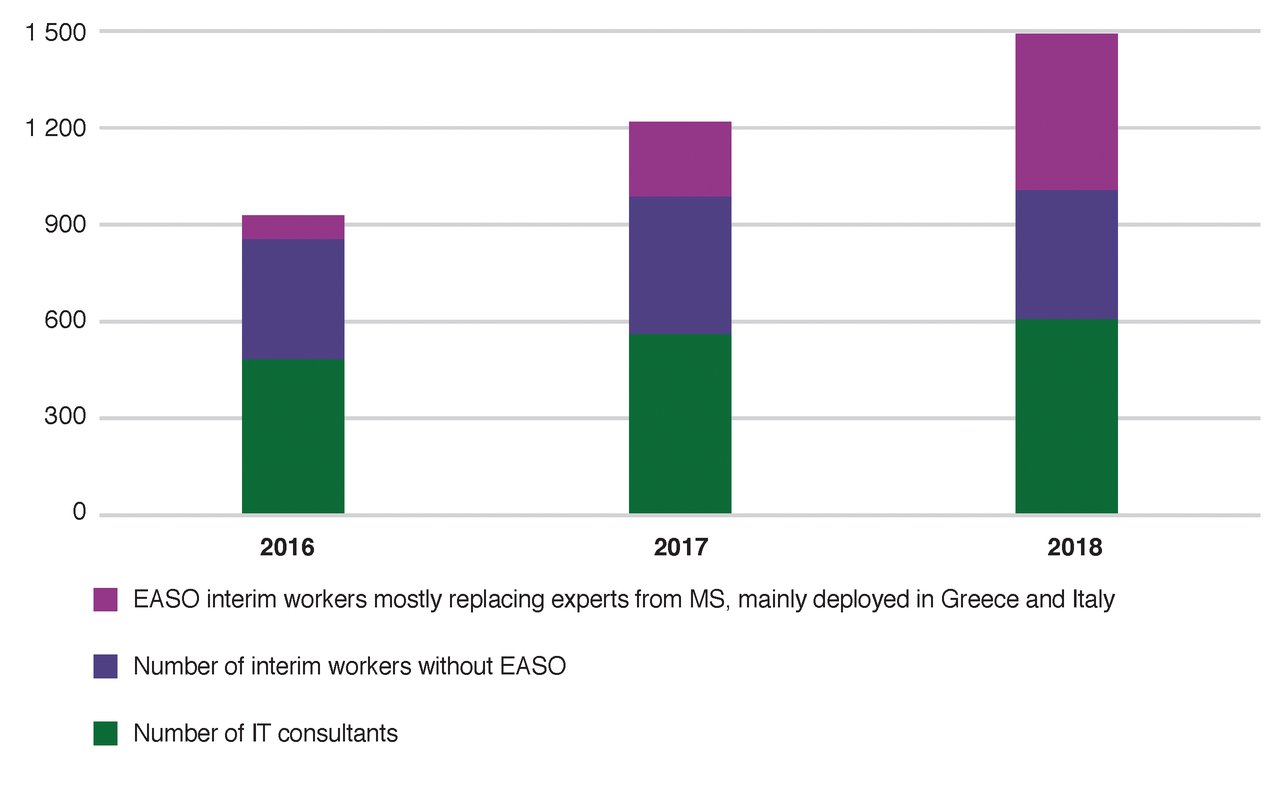

It is in this context that this year’s observations on the use of consultants and interim workers by some of the agencies are of particular importance. While we did not audit the use of external staff horizontally for all agencies, payments in our audit samples indicate a trend to compensate shortages of own statutory staff by external staff. Box 2.8 presents information collected by the Network of EU agencies (EUAN) on the increasing number of IT consultants working in the premises of the agencies and other bodies on times and means contracts and interim staff used by the 33 agencies who replied to a respective survey. |

Box 2.8

Number of IT consultants and interim agents (33 agencies)

|

Source: |

Network of EU agencies (EUAN), figures compiled by ECA. |

|

2.29. |

For eight agencies (BEREC Office, Chafea, CPVO, EASO, ERCEA, ESMA, SRB, EUIPO), we found that they used contracts on the provision of IT and other consultancy services which were formulated and/or implemented in a way that, in practice, might result in the assignment (‘mise à disposition’) of temporary agency workers instead of the provision of clearly specified services or products. The provision of interim workers can only be done through contracts with registered temporary work agencies and in accordance with Directive 2008/104/EC of the European Parliament and of the Council (19), and according to the specific rules adopted by the Member States in the transposition of that Directive. The use of service contracts for the provision of labour is not compliant with the EU Staff Regulations and EU social and employment rules and exposes these agencies to legal and reputational risks. |

|

2.30. |

Furthermore, seven agencies (EASO, EBA, EIOPA, EIGE, EMCDDA, ERCEA, SRB) engaged in the use of interim workers provided by registered temporary work agencies, but did not respect all the rules laid down in both the Directive and in the respective national law, for instance as regards working conditions for interim workers. |

|

Actions to be taken 5 The agencies may analyse, together with the budgetary authorities, whether the use of external staff is cost efficient as compared to the use of own statutory staff. |

|

Actions to be taken 6 Where external staff is used, full compliance with the applicable EU and national legal framework is required as a matter of principle, but also to avoid litigation risks and reputational damage. |

Consultancy and non-consultancy services in EUIPO

|

2.31. |

Given the scale of consulting services used by EUIPO, we carried out an analysis of the Office’s management of consulting services. The main contract for consultancy services has a volume of 80 million euros for four years. The number of external staff provided by service providers under these and similar contracts went up from around 250 in 2011 to a peak of more than 350 in 2014 falling to 215 at the beginning of 2018 (equal to some 20 % of the Office’s statutory staff). |

|

2.32. |

We noted that, while a part of the services delivered under these contracts is indeed consultancy (for example project management support, business process analysis), another part is rather on administrative support (for example secretarial support, administrative clerks preparing reports, support for internal and external communication activities). The latter part represents a purchase of labour or loan of staff, which is strictly regulated by European and national labour law. Only registered temporary work agencies are authorised to make external staff available and such service cannot be provided by consultancy companies. |

The implementation of a new internal control framework is on the way

|

2.33. |

Internal control applies to all financial and non-financial activities and is a process that helps an organisation to achieve its objectives and sustain performance, respecting rules and regulations. It supports sound decision making, taking into account risks to achieve objectives and reduce them to acceptable levels through cost-effective controls. In April 2017, the Commission approved a revised internal control framework (ICF). |

|

2.34. |

The new ICF is designed to provide reasonable assurance regarding the achievement of five objectives set in the Financial Regulations: (1) effectiveness, efficiency and economy of operations; (2) reliability of reporting; (3) safeguarding of assets and information; (4) prevention, detection, correction and follow-up of fraud and irregularities, and (5) adequate management of the risks relating to the legality and regularity of the underlying transactions. It supplements the Financial Regulation with a view to align internal control standards to the highest international standards as set by the Committee of Sponsoring Organisations of the Treadway Commission (COSO) framework. |

|

2.35. |

As was the case for the Commission’s internal control standards which are being replaced by the ICF, entrusted bodies such as agencies are expected to implement the ICF by analogy. By the end of 2018, the boards of 29 agencies had adopted the ICF while 15 agencies also reported its implementation. |

|

Actions to be taken 7 The adoption and implementation of the Commission’s Internal Control Framework (2017) by all agencies is a necessity in order to align internal control standards to the highest international standards and make sure internal controls support decision making effectively and efficiently. |

Not all agencies have a sensitive posts policy in place

|

2.36. |

Management of sensitive functions is a standard element of internal control, which aims to reduce the risk of the misuse of powers delegated to staff to an acceptable level. Sensitive functions are those where a member of staff executing an activity has a degree of autonomy and/or decisional power sufficient to permit them, should they so wish, to misuse these powers for personal gain (20). In an effective internal control framework, risks associated with sensitive functions are managed through mitigating controls and ultimately staff mobility. We found that seven agencies (EASO, EASME, ECHA, EEA, ENISA, Frontex, SRB) do not have policies in place defining their sensitive functions and related mitigating controls. |

|

2.37. |

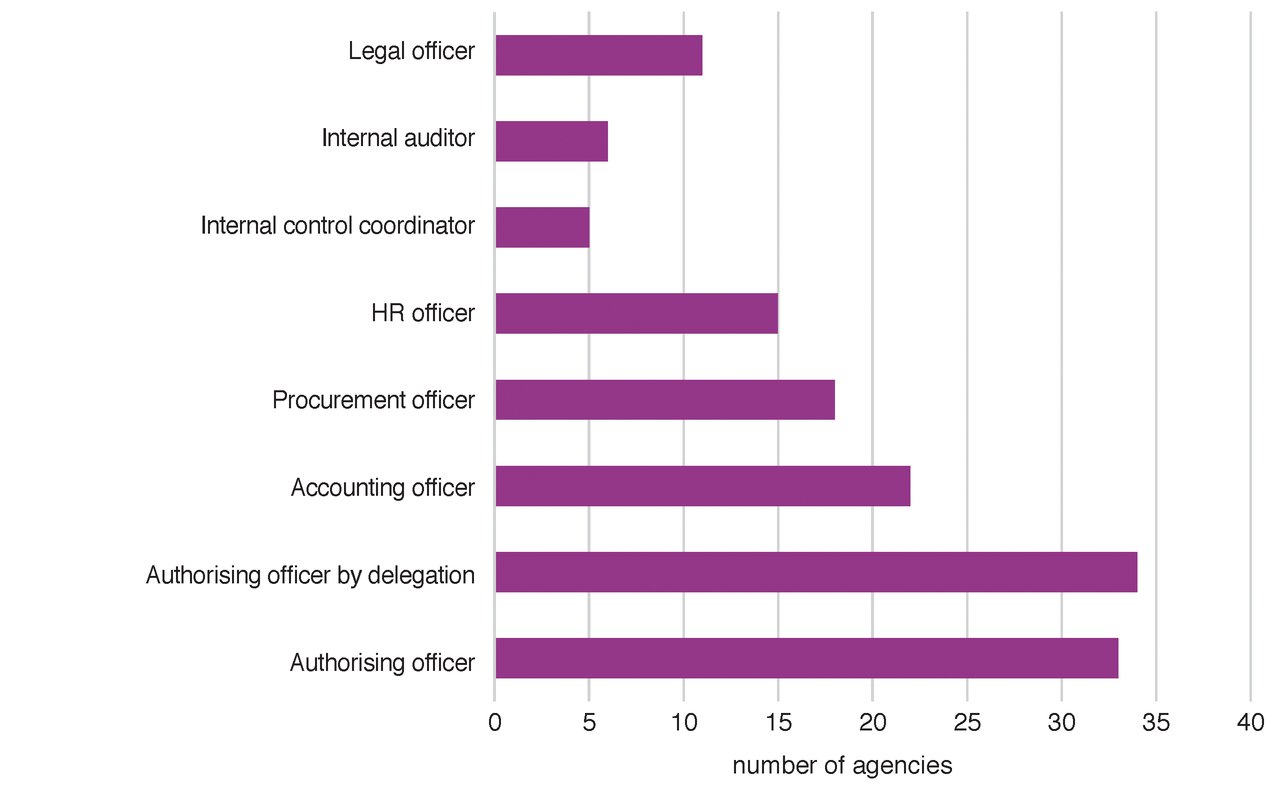

Even though agencies have a similar administrative structure and the roles of the financial actors are governed by similar financial regulations, they apply different interpretations of what posts should be considered potentially sensitive. Box 2.9 below shows the number of agencies that consider a specific post potentially sensitive. |

Box 2.9

Potentially sensitive posts

|

Source: |

ECA. |

|

2.38. |

The main controls put in place by agencies in order to mitigate sensitive posts related risks are the segregation of duties and application of the 4-eyes-principle for the initiation and authorisation of transactions. However, a policy of mandatory mobility for staff holding sensitive posts exists in one third of the agencies only. |

|

Actions to be taken 8 The agencies are invited to agree on which posts are to be considered sensitive and to introduce or align their sensitive posts policies in order to mitigate the risk of misuse of powers for personal gain. |

There is scope for more meaningful budget structure and reporting

|

2.39. |

As in previous years, the number and volume of delegation and grant agreements concluded between the Commission and a number of agencies has further increased in 2018. Under these agreements, agencies receive funds from the Commission assigned for the execution of specific tasks on behalf of the Commission. |

|

2.40. |

Although these funds become part of the budget revenue (assigned revenue) of the agencies concerned, they can be used only for the purposes defined in the delegation agreements. If tasks last for more than one year, agencies are supposed to keep the part of the funds not spent at the end of the year in order to use them for the remaining tasks to be delivered until the end of the agreement. Only then, remaining funds have to be returned to the Commission. As a consequence, these funds have to be eliminated from the calculation of the agencies’ ‘own’ annual budgetary result, which forms part of their financial statements. Most of the agencies include a correction figure to this effect in their calculations of the budget result. However, with the increasing number and volume of these agreements, we see the need for a more comprehensive and standardised reporting on assigned revenue and related expenditure for the calculation of agencies’ budgetary results. |

|

Actions to be taken 9 In order to increase the transparency of budgetary reporting, agencies implementing assigned revenue are encouraged to include in their financial statements a standardised overview disclosing the assigned revenue and related expenditure per Commission delegation agreement. |

|

2.41. |

Furthermore, the planning procedures implemented by all agencies and resulting in annual and multi-annual work programmes (or single programming documents) are based on activities. For each of these activities, specific work programmes have to contain information on the resources planned (human and financial). However, we noted that the published budgets of all agencies are presented by type of expenditure (staff expenditure, administrative expenditure and operational expenditure, see Box 1.5 in Chapter 1), but not by activity. As a consequence, resources spent for the different activities are not visible. |

|

Actions to be taken 10 A publication of agency budgets by activity would allow linking resources to the activities they are used for. |

There are risks to the correct calculation of registration and service fees

|

2.42. |

A number of agencies (CdT, CPVO, EASA, EBA, ECHA, EIOPA, EMA, ESMA, EUIPO, SRB) collect revenue from service or registration fees charged to economic operators (see Chapter 1, boxes 1.3 and 1.4). We noted risks concerning the correct calculation of such fees. |

|

2.43. |

ECHA receives a fee from every company requesting the registration of chemicals (21) which depends on the size of the companies (micro, small, medium, large) and the volume of chemicals (different thresholds) registered. Based on ECHA’s own verifications carried out since 2011 and completed so far, some 52 % of the companies checked, which claimed to be of a micro, small or medium size (11 % of all companies) had categorised their size incorrectly resulting in lower fees (22). While the Agency has made considerable progress in recovering undue fee reductions and collecting overdue administrative charges, the verification work is still causing a significant workload in terms of identifying and correcting these cases. Furthermore, the quantities of chemicals to be registered form an important element for the calculation of the registration fees. However, ECHA has no verification rights as to the accuracy of these quantities, which are with the Member States. |

|

2.44. |

The fees charged by ESMA to credit rating agencies are based on their revenue as legal entities, but not as a group or group of related entities. A gap in the related fees regulation creates a quasi-legitimate opportunity to reduce or avoid fees by transferring revenues from credit rating agencies under the EU jurisdiction to their related entities outside the EU. The Authority correctly applied the regulation, identified the risk and addressed it to the Commission. |

|

2.45. |

Credit institutions’ contributions to the Single Resolution Fund managed by the SRB are calculated on the basis of information provided by the credit institutions to the Board through the national resolution authorities. Given that the Single Resolution Mechanism Regulation does not provide for a comprehensive and consistent control framework to ensure the reliability of the information, no checks are carried out at the level of the credit institutions. However, the SRB performs consistency and analytical checks of the information. Furthermore, the methodology for calculating contributions laid down in the legal framework is very complex, resulting in a risk to accuracy. For confidentiality reasons, the Board cannot release the credit institutions’ data used for the calculation of Fund contributions, which reduces transparency. |

|

Actions to be taken 11 The agencies concerned are invited to consult the Commission concerning any need to adjust the legal framework in order to ensure fee calculations on the basis of accurate information reflecting economic reality. |

Agencies are following-up on previous years’ audit findings

|

2.46. |

We provided a status on follow-up actions taken by the agencies in response to observations from previous years. Box 2.10 shows that for the 223 observations that had not been addressed at the end of 2017, corrective action was completed or ongoing in most cases in 2018. Out of the 107 outstanding and ongoing observations, the necessary corrective action to address 13 observations was not under the agency’s (sole) control. |

Box 2.10

Agencies’ efforts to follow-up previous years’ observations

|

Source: |

ECA. |

|

2.47. |

In the course of last year’s annual audit, we reviewed agencies’ accounting environments, which are an important element for the preparation of reliable accounts. We raised observations on the independence of accounting officers in the execution of their duties for 13 agencies. Following the Court’s observations, the majority of agencies addressed the issue in 2018, except for two (EACEA, EFSA). A similar trend was observed concerning outstanding (re) validations of accounting systems. All seven agencies for which we reported such a need in 2018 had completed corrective action in 2018. |

|

2.48. |

Good progress was also made in relation to the introduction of e-procurement. As reported last year, the Commission launched tools for electronic invoicing in 2010 (e-invoicing), for the electronic publication of documents related to contract notices in the EU Official Journal in 2011 (e-tendering) and for the electronic submission of tenders in 2015 (e-submission). Box 2.11 below shows the progress made in introduction of the tools by the end of 2018. |

Box 2.11

E-procurement is on its way

|

Source: |

ECA. |

|

2.49. |

Some progress was also made in 2018 in relation to the introduction of SYSPER II, the HR management tool on human resources developed by the Commission. Box 2.12 below shows that in 2018 five additional agencies signed up for the tool. The Commission reported good cooperation with the agencies in general. However, the project being complex and each agency having its own specificities, the progress in the implementation of the SYSPER II varies. Some agencies struggle to assign the necessary resources to the project and thus are facing some delays. |

Box 2.12

Introduction of SYSPER II HR tool

|

Source: |

ECA. |

Not all agencies are subject to the same budgetary and discharge procedure

|

2.50. |

Unlike other agencies, the fully self-financed decentralised agency EUIPO is subject to discharge procedure by its Budget Committee, rather than by the European Parliament and the Council (see Chapter 1, paragraphs 1.23 and 1.24). Similarly, for the other two fully self-financed agencies SRB and CPVO, the annual budgetary and discharge procedures are the responsibility of their Boards. These different procedures are provided by their founding regulations. |

|

2.51. |

These are self-financed agencies and bodies, whose budgets do not form part of the general budget of the Union, however their revenue stems from the exercise of a public authority on the basis of EU law. Thus, the ECA has consistently stated that the same principles of accountability and transparency should be applied to all EU-related bodies. For EUIPO, the ECA expressed concerns about the Office’s budgetary discharge procedure in its opinions issued in 2015 (23) and 2019 (24). For SRB (25) and CPVO (26), the Court equally addressed its concerns in opinions published in 2015. |

AUDIT RESULTS FROM OTHER AGENCY-RELATED PRODUCTS ISSUED BY THE COURT

ECA Special report No 29/2018: EIOPA made an important contribution to supervision and stability in the insurance sector, but significant challenges remain

|

2.52. |

EIOPA was established in 2011, following the reform of EU financial sector supervision after the financial crisis of 2007-2008. EIOPA acts as an independent advisory body to the European Commission, the Parliament and the Council. |

|

2.53. |

In a special audit carried out in addition to our annual financial and compliance audit of EIOPA, we examined whether the authority makes an effective contribution to supervision and financial stability in the insurance sector. In particular, we analysed EIOPA’s actions in the field of supervision and supervisory convergence (co-operation with National Competent Authorities (NCAs), their work on internal models and cross-border business), the 2016 insurance stress test as well as the adequacy of EIOPA’s resources and governance. |

|

2.54. |

Our overall conclusion is that EIOPA has made good use of a wide range of tools to support supervisory convergence and financial stability. However, there are still significant challenges to be addressed by EIOPA itself, by national supervisors and by legislators, for example in the context of the European Supervisory Authorities’ (ESAs) and Solvency II reviews. Moreover, we recommended that for improving the efficiency and effectiveness of EIOPA’s actions, the Authority should strengthen human resources assigned to supervision. |

|

2.55. |

The full audit conclusions, together with the related recommendations and the authority’s replies, are addressed in our Special report No 29/2018 which is available on our website eca.europa.eu |

ECA 2017 specific annual report pursuant to Article 92(4) of Regulation (EU) 806/2014 on any contingent liabilities arising as a result of the performance by the Single Resolution Board, the Council and the Commission of their tasks under this Regulation for financial year 2017

|

2.56. |

Pursuant to Article 92(4) of the SRM Regulation we audit annually the existence of any contingent liabilities arising as a result of the performance by the Single Resolution Board, the Council and the Commission of their tasks under this Regulation. |

|

2.57. |

The audit conclusions for the financial year 2017, together with the related recommendations and the SRB’s replies, are addressed in our specific report, which is available on our website eca.europa.eu |

Other ECA special reports also referring to one or more agencies

|

2.58. |

Apart from audit reports specifically dedicated to the agencies, in the course of 2018 we also issued a number of special audit reports on EU policy implementation which referred to a number of agencies (Box 2.13). |

Box 2.13

Other ECA special audit reports referring to agencies

|

Source: |

ECA. |

THE EU AGENCIES NETWORK’S REPLY

The Agencies appreciate the Court’s positive conclusions on the reliability of their accounts and the transactions underlying them.

|

2.21, 2.22 and 2.28. |

The Network would like to highlight that the observations in the area of financial management, procurement related internal controls and the procurement of interim services consist of highly diverse cases and differ from Agency to Agency, therefore the Network would like to make reference to Agency’s individual responses in Chapter 3. |

|

2.29. |

Indeed EU Agencies have to conclude the contracts for interim/temporary workers in accordance with the applicable EU Financial Rules and the relevant national legislation transposing Directive 2008/104/EC on temporary agency work. The temporary-work companies contracted by the EU Agencies are obliged to comply with the conditions laid down by national legislation (transposing the relevant EU legislation) for the contract of employment for temporary work concluded with each interim worker and subject to possible litigation regarding its execution. The (standard) service contract concluded between the EU Agency and the temporary-work company usually refers to this obligation. |

|

2.31. |

The Office has a strict separation between the concept of staff and external resources; hence the concept of external staff does not exist at the EUIPO. Besides, the Office mainly contracts external services through the fixed price modality. Therefore, the number of resources is not a good indicator. Moreover, the budget allocated to consultancy has been steadily decreasing over recent years. |

|

2.32. |

Regarding the use of the FWC, for requesting services which could appear to be of an administrative nature, the Office does not consider it can be associated with ‘a loan of staff’. As a general policy such contracted administrative support is provided in the context of projects and not core business. In general, the use of non-statutory staff for the provision of administrative support outside projects is limited to agency workers (interim). |

|

2.37. |

The Network wishes to stress its commitment to aligning policies. In case of the matter at stake (‘potentially sensitive post’), a possible alignment should be carefully considered in relation to the identification of possible sensitive positions and the nature and level of the risks inherent to the latter. The mitigating measures that may be considered necessary/proportional to address these risks, depend, quite substantially, on factors such as the size of the Agency and/or the nature and scope of its mandate/core business. Any non-proportionate ‘harmonisation’, or ‘one-size-fits-all’ solution, should be avoided, in particular the possible use/application of ‘mandatory mobility’ for certain pre-defined positions. Such a measure should always rely on the actual assessment of its proportionality and effectiveness in relation to each Agency, by considering the actual risks at stake, as well as its potential disruptive effect on the regular functioning of the Agency. |

|

2.50 and 2.51. |

EUIPO would like to highlight the decision of the legislators which was confirmed during the last legislative reform. According to Article 176(2) of the Regulation (EU) 2017/1001 of the European Parliament and of the Council of 14 June 2017 on the European Union trade mark (EUTMR), ‘the Budget Committee shall give a discharge to the Executive Director in respect of the implementation of the budget’. Such discharge is strongly based on the annual reports issued by the ECA. |

CHAPTER 3

Statements of Assurance and other agency-specific audit results

3.1. INFORMATION IN SUPPORT OF THE STATEMENTS OF ASSURANCE

Basis for opinions

|

3.1.1. |

We conducted our audit in accordance with the IFAC International Standards on Auditing (ISAs) and Codes of Ethics and the INTOSAI International Standards of Supreme Audit Institutions (ISSAIs). Our responsibilities under those standards are further described in the ‘Auditor’s responsibilities’ section of our report. We are independent, in accordance with the Code of Ethics for Professional Accountants issued by the International Ethics Standards Board for Accountants (IESBA Code) and with the ethical requirements that are relevant to our audit, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the IESBA Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. |

Responsibilities of management and those charged with governance

|

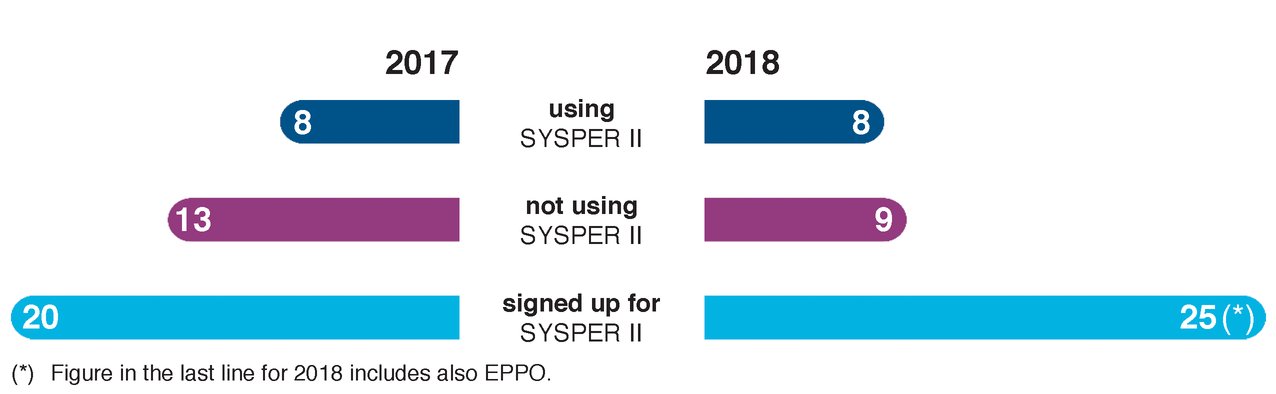

3.1.2. |