ISSN 1830-3668

doi:10.3000/18303668.C_2010.095.ron

Jurnalul Oficial

al Uniunii Europene

C 95

Ediţia în limba română

Comunicări şi informări

Anul 53

15 aprilie 2010

|

ISSN 1830-3668 doi:10.3000/18303668.C_2010.095.ron |

||

|

Jurnalul Oficial al Uniunii Europene |

C 95 |

|

|

|

||

|

Ediţia în limba română |

Comunicări şi informări |

Anul 53 |

|

Informarea nr. |

Cuprins |

Pagina |

|

|

I Rezoluții, recomandări și avize |

|

|

|

AVIZE |

|

|

|

Comisia Europeană |

|

|

2010/C 095/01 |

||

|

|

II Comunicări |

|

|

|

COMUNICĂRI PROVENIND DE LA INSTITUȚIILE, ORGANELE ȘI ORGANISMELE UNIUNII EUROPENE |

|

|

|

Comisia Europeană |

|

|

2010/C 095/02 |

||

|

|

IV Informări |

|

|

|

INFORMĂRI PROVENIND DE LA INSTITUȚIILE, ORGANELE ȘI ORGANISMELE UNIUNII EUROPENE |

|

|

|

Comisia Europeană |

|

|

2010/C 095/03 |

||

|

|

INFORMĂRI PROVENIND DE LA STATELE MEMBRE |

|

|

2010/C 095/04 |

||

|

|

V Anunțuri |

|

|

|

PROCEDURI ADMINISTRATIVE |

|

|

|

Comisia Europeană |

|

|

2010/C 095/05 |

Cerere specifică de propuneri – EAC/19/10 – Carta Universitară Erasmus 2011 |

|

|

|

PROCEDURI REFERITOARE LA PUNEREA ÎN APLICARE A POLITICII COMERCIALE COMUNE |

|

|

|

Comisia Europeană |

|

|

2010/C 095/06 |

||

|

|

PROCEDURI REFERITOARE LA PUNEREA ÎN APLICARE A POLITICII ÎN DOMENIUL CONCURENȚEI |

|

|

|

Comisia Europeană |

|

|

2010/C 095/07 |

Ajutor de stat – Țările de Jos – Ajutor de stat C 11/09 [asociat NN 2/10 (ex N 429/09) și N 19/10] – Măsuri de recapitalizare în favoarea FBN și a grupului ABN Amro – Invitație de a prezenta observații în temeiul articolului 108 alineatul (2) din Tratatul privind funcționarea Uniunii Europene ( 1 ) |

|

|

|

ALTE ACTE |

|

|

|

Comisia Europeană |

|

|

2010/C 095/08 |

||

|

2010/C 095/09 |

||

|

|

|

|

|

(1) Text cu relevanță pentru SEE |

|

RO |

|

I Rezoluții, recomandări și avize

AVIZE

Comisia Europeană

|

15.4.2010 |

RO |

Jurnalul Oficial al Uniunii Europene |

C 95/1 |

AVIZUL COMISIEI

din 14 aprilie 2010

privind planul modificat de eliminare a deșeurilor radioactive provenite de la clădirea 443.26, operată de General Electric Healthcare Ltd (fosta Amersham plc), situată în cadrul Harwell International Business Centre din Regatul Unit, în conformitate cu articolul 37 din Tratatul Euratom

(Numai textul în limba engleză este autentic)

2010/C 95/01

La 11 noiembrie 2009, Comisia Europeană a primit de la guvernul britanic, în conformitate cu articolul 37 din Tratatul Euratom, date generale privind planul modificat de eliminare a deșeurilor radioactive provenite de la clădirea 443.26 operată de General Electric Healthcare Ltd (fosta Amersham plc).

Pe baza acestor informații și în urma consultării Grupului de experți, Comisia a formulat următorul aviz:

|

1. |

distanța dintre instalație și cel mai apropiat stat membru, în acest caz, Franța, este de aproximativ 225 km; |

|

2. |

modificarea preconizată vizează o creștere preconizată a limitei autorizate a deversărilor de radon-222 în suspensie în aer; |

|

3. |

în condiții de funcționare normală, modificarea preconizată nu va cauza o expunere susceptibilă să afecteze sănătatea populației din alt stat membru; |

|

4. |

în cazul unor scurgeri neprevăzute de efluenți radioactivi, care ar putea rezulta în urma unui accident de tipul sau de amploarea celor prevăzute în datele generale, dozele pe care populația din alte state membre le-ar putea primi nu ar fi semnificative din punct de vedere al sănătății. |

În concluzie, Comisia consideră că implementarea planului modificat de eliminare a deșeurilor radioactive sub orice formă, provenite de la clădirea 443.26, operată de General Electric Healthcare Ltd (fosta Amersham plc), situată în cadrul Harwell International Business Centre din Regatul Unit, nu poate provoca, nici în timpul funcționării normale și nici în cazul unui accident de tipul și amploarea celor luate în considerare în datele generale, o contaminare radioactivă a apei, a solului sau a spațiului aerian al unui alt stat membru.

Adoptat la Bruxelles, 14 aprilie 2010.

Pentru Comisie

Günther OETTINGER

Membru al Comisiei

II Comunicări

COMUNICĂRI PROVENIND DE LA INSTITUȚIILE, ORGANELE ȘI ORGANISMELE UNIUNII EUROPENE

Comisia Europeană

|

15.4.2010 |

RO |

Jurnalul Oficial al Uniunii Europene |

C 95/2 |

Autorizație pentru ajutoarele de stat acordate în conformitate cu articolele 107 și 108 din Tratatul privind funcționarea Uniunii Europene

Cazuri față de care Comisia nu prezintă obiecții

2010/C 95/02

|

Data adoptării deciziei |

15.1.2010 |

|||||

|

Numărul de referință al ajutorului |

N 178/08 |

|||||

|

Stat membru |

Spania |

|||||

|

Regiune |

Castilla y Léon |

|||||

|

Titlu (și/sau numele beneficiarului) |

Ayuda a la reestructuración de Primayor Elaborados, S.L.U |

|||||

|

Temei legal |

Proyecto de Plan de Reestructuración a favor de la sociedad «Primayor Elaborados, S.L.U.» |

|||||

|

Tipul măsurii |

Ajutor individual |

|||||

|

Obiectiv |

Ajutor pentru restructurarea unei IMM |

|||||

|

Forma de ajutor |

Garanție de stat pentru o operațiune de credit bancar |

|||||

|

Buget |

Buget: 2 324 000 EUR |

|||||

|

Valoare |

100 % |

|||||

|

Durată (perioadă) |

Durata ajutorului este de 5 ani. |

|||||

|

Sectoare economice |

Agricultură |

|||||

|

Numele și adresa autorității de acordare a ajutorului |

|

|||||

|

Alte informații |

Scheme precedente: Ajutorul pentru redresare NN 16/08 (fost N 518/07) |

Textul deciziei în limba (limbile) originală (originale), din care au fost înlăturate toate informațiile confidențiale, poate fi consultat pe site-ul:

http://ec.europa.eu/community_law/state_aids/state_aids_texts_ro.htm

|

Data adoptării deciziei |

19.2.2010 |

||

|

Numărul de referință al ajutorului |

NN 01/09 ex CP 154/08 |

||

|

Stat membru |

Țările de Jos |

||

|

Regiune |

Provincie Overijssel |

||

|

Titlu (și/sau numele beneficiarului) |

Steun voor advisering in verband met het varkensclusterproject, provincie Overijssel |

||

|

Temei legal |

Provinciewet; Begroting van de provincie Overijssel |

||

|

Tipul măsurii |

Ajutoare pentru serviciile de consultanță |

||

|

Obiectiv |

Subvenționarea unui proiect în vederea facilitării și explorării posibilităților de realizare a unei grupări durabile de întreprinderi familiale care își desfășoară activitatea în producția primară de porcine. |

||

|

Forma de ajutor |

Subvenție unică |

||

|

Buget |

214 358 EUR |

||

|

Valoare |

Maximum 50 % |

||

|

Durată (perioadă) |

2005, ajutor unic |

||

|

Sectoare economice |

Producția primară de porcine |

||

|

Numele și adresa autorității de acordare a ajutorului |

|

||

|

Alte informații |

— |

Textul deciziei în limba (limbile) originală (originale), din care au fost înlăturate toate informațiile confidențiale, poate fi consultat pe site-ul:

http://ec.europa.eu/community_law/state_aids/state_aids_texts_ro.htm

|

Data adoptării deciziei |

10.2.2010 |

|||||

|

Numărul de referință al ajutorului |

N 34/10 |

|||||

|

Stat membru |

Belgia |

|||||

|

Regiune |

Flandra |

|||||

|

Titlu (și/sau numele beneficiarului) |

Beperkte steun voor primaire producenten die getroffen zijn door de financiële crisis |

|||||

|

Temei legal |

Besluit van de Vlaamse regering betreffende steun aan de investeringen en aan de installatie in de landbouw (1) |

|||||

|

Tipul măsurii |

Schemă de ajutoare |

|||||

|

Obiectiv |

Ajutor destinat remedierii unor perturbări grave ale economiei |

|||||

|

Forma de ajutor |

Garanții și subvenții la dobânzi |

|||||

|

Buget |

Buget total de 2,73 milioane EUR |

|||||

|

Valoare |

— |

|||||

|

Durată (perioadă) |

31.12.2010 |

|||||

|

Sectoare economice |

Agricultură |

|||||

|

Numele și adresa autorității de acordare a ajutorului |

|

|||||

|

Alte informații |

— |

Textul deciziei în limba (limbile) originală (originale), din care au fost înlăturate toate informațiile confidențiale, poate fi consultat pe site-ul:

http://ec.europa.eu/community_law/state_aids/state_aids_texts_ro.htm

(1) Besluit van de Vlaamse regering van 20 november 2000 betreffende steun aan de investeringen en de installatie in de landbouw, BS, 14.2.2001.

IV Informări

INFORMĂRI PROVENIND DE LA INSTITUȚIILE, ORGANELE ȘI ORGANISMELE UNIUNII EUROPENE

Comisia Europeană

|

15.4.2010 |

RO |

Jurnalul Oficial al Uniunii Europene |

C 95/5 |

Rata de schimb a monedei euro (1)

14 aprilie 2010

2010/C 95/03

1 euro =

|

|

Moneda |

Rata de schimb |

|

USD |

dolar american |

1,3615 |

|

JPY |

yen japonez |

127,42 |

|

DKK |

coroana daneză |

7,4431 |

|

GBP |

lira sterlină |

0,88140 |

|

SEK |

coroana suedeză |

9,7327 |

|

CHF |

franc elvețian |

1,4368 |

|

ISK |

coroana islandeză |

|

|

NOK |

coroana norvegiană |

7,9955 |

|

BGN |

leva bulgărească |

1,9558 |

|

CZK |

coroana cehă |

25,048 |

|

EEK |

coroana estoniană |

15,6466 |

|

HUF |

forint maghiar |

262,65 |

|

LTL |

litas lituanian |

3,4528 |

|

LVL |

lats leton |

0,7082 |

|

PLN |

zlot polonez |

3,8549 |

|

RON |

leu românesc nou |

4,1440 |

|

TRY |

lira turcească |

2,0162 |

|

AUD |

dolar australian |

1,4583 |

|

CAD |

dolar canadian |

1,3571 |

|

HKD |

dolar Hong Kong |

10,5665 |

|

NZD |

dolar neozeelandez |

1,9089 |

|

SGD |

dolar Singapore |

1,8734 |

|

KRW |

won sud-coreean |

1 514,11 |

|

ZAR |

rand sud-african |

9,9682 |

|

CNY |

yuan renminbi chinezesc |

9,2932 |

|

HRK |

kuna croată |

7,2570 |

|

IDR |

rupia indoneziană |

12 257,63 |

|

MYR |

ringgit Malaiezia |

4,3575 |

|

PHP |

peso Filipine |

60,615 |

|

RUB |

rubla rusească |

39,4845 |

|

THB |

baht thailandez |

43,922 |

|

BRL |

real brazilian |

2,3744 |

|

MXN |

peso mexican |

16,5400 |

|

INR |

rupie indiană |

60,2190 |

(1) Sursă: rata de schimb de referință publicată de către Banca Centrală Europeană.

INFORMĂRI PROVENIND DE LA STATELE MEMBRE

|

15.4.2010 |

RO |

Jurnalul Oficial al Uniunii Europene |

C 95/6 |

Decizie de deschidere a procedurilor de redresare pentru KD Life Asigurări S.A.

(Publicare realizată în conformitate cu articolul 6 din Directiva 2001/17/CE a Parlamentului European și a Consiliului din 19 martie 2001 privind reorganizarea și lichidarea întreprinderilor de asigurare)

2010/C 95/04

|

Întreprinderea de asigurare |

|

||||

|

Data, intrarea în vigoare și natura deciziei |

Decizia nr. 190/3 martie 2010 Data intrarii in vigoare 3 martie 2010 Procedura de redresare financiară prin administrare specială |

||||

|

Autoritățile competente |

Comisia de Supraveghere a Asigurărilor |

||||

|

Autoritatea de supraveghere |

Comisia de Supraveghere a Asigurărilor |

||||

|

Administratorul special desemnat |

|

||||

|

Legea aplicabilă |

Legea nr. 503/2004 privind redresarea financiară și falimentul societăților de asigurare |

V Anunțuri

PROCEDURI ADMINISTRATIVE

Comisia Europeană

|

15.4.2010 |

RO |

Jurnalul Oficial al Uniunii Europene |

C 95/7 |

CERERE SPECIFICĂ DE PROPUNERI – EAC/19/10

Carta Universitară Erasmus 2011

2010/C 95/05

1. OBIECTIVE ȘI DESCRIERE

Carta Universitară Erasmus oferă cadrul general pentru activitățile de cooperare europene pe care le poate desfășura o instituție de învățământ superior în cadrul programului Erasmus ca parte a Programului de învățare de-a lungul vieții (Lifelong Learning Programme – LLP). Carta Universitară Erasmus trebuie să fie acordată ca o condiție preliminară pentru ca instituțiile de învățământ superior să organizeze programe de mobilitate pentru studenți, cadre didactice și alte tipuri de personal, să realizeze cursuri de limbi străine intensive și programe intensive în cadrul programului Erasmus, să prezinte candidaturi pentru proiecte multilaterale, rețele și măsuri adiacente, precum și să organizeze vizite pregătitoare. Carta Universitară Erasmus se bazează pe decizia LLP (1) care acoperă perioada 2007-2013. Obiectivele specifice ale LLP sunt enumerate la articolul 1 alineatul (3) din decizie.

2. CANDIDAȚI ELIGIBILI

Carta Universitară Erasmus se aplică tuturor instituțiilor de învățământ superior definite la articolul 2 alineatul (10) din decizia menționată.

Candidații trebuie să fie stabiliți pe teritoriul uneia dintre următoarele țări:

|

— |

cele 27 de state membre ale Uniunii Europene; |

|

— |

țările AELS-SEE: Islanda, Liechtenstein, Norvegia; |

|

— |

țările candidate: Turcia, Croația, Fosta Republică Iugoslavă a Macedoniei; |

|

— |

Elveția (2). |

3. TERMENUL LIMITĂ DE DEPUNERE A CANDIDATURILOR

Termenul limită de depunere a candidaturilor pentru Carta Universitară Erasmus este 30 iunie 2010.

4. INFORMAȚII COMPLETE

Informațiile referitoare la programul Erasmus și la Carta Universitară Erasmus pot fi consultate la următoarea adresă de internet: http://ec.europa.eu/llp

Candidaturile trebuie prezentate în conformitate cu orientările puse la dispoziție de Agenția Executivă pentru Educație, Audiovizual și Cultură la adresa: http://eacea.ec.europa.eu/llp/index_en.htm

(1) Decizia nr. 1720/2006/CE a Parlamentului European și a Consiliului din 15 noiembrie 2006 de stabilire a unui program de acțiune în domeniul învățării continue. A se vedea http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri= OJ:L:2006:327:0045:0068:EN:PDF

(2) Participarea Elveției se bazează pe Acordul între Uniunea Europeană și Confederația Elvețiană de stabilire a clauzelor și condițiilor de participare a Confederației Elvețiene la programul „Tineretul în acțiune” și la programul de acțiune din domeniul învățării de-a lungul vieții 2007-2013 (semnat la 15 februarie 2010 – nepublicat încă).

PROCEDURI REFERITOARE LA PUNEREA ÎN APLICARE A POLITICII COMERCIALE COMUNE

Comisia Europeană

|

15.4.2010 |

RO |

Jurnalul Oficial al Uniunii Europene |

C 95/9 |

Aviz de expirare iminentă a unor măsuri antidumping

2010/C 95/06

1. În conformitate cu articolul 11 alineatul (2) din Regulamentul (CE) nr. 1225/2009 al Consiliului din 30 noiembrie 2009 privind protecția împotriva importurilor care fac obiectul unui dumping din partea țărilor care nu sunt membre ale Comunității Europene (1), Comisia Europeană face cunoscut faptul că dacă nu se inițiază o reexaminare în conformitate cu procedura următoare, măsurile antidumping menționate în continuare expiră la data menționată în tabelul de mai jos.

2. Procedură

Producătorii din Uniune pot depune o cerere scrisă de reexaminare. Cererea trebuie să conțină probe suficiente care să susțină faptul că expirarea măsurilor ar determina probabil continuarea sau reapariția dumpingului și a prejudiciului.

În cazul în care Comisia decide să reexamineze măsurile în cauză, importatorii, exportatorii, reprezentanții țării exportatoare și producătorii din Uniune vor avea posibilitatea de a dezvolta, de a respinge sau de a comenta chestiunile expuse în cererea de reexaminare.

3. Termen

Pe baza celor de mai sus, producătorii din Uniune pot transmite o cerere scrisă de reexaminare la adresa Comisia Europeană, Direcția Generală Comerț (unitatea H-1), N-105 4/92, 1049 Bruxelles/Brussel, BELGIQUE/BELGIË (2), oricând după data publicării prezentului aviz, dar cel târziu cu trei luni înainte de data menționată în tabelul de mai jos.

4. Prezentul aviz este publicat în conformitate cu articolul 11 alineatul (2) din Regulamentul (CE) nr. 1225/2009.

|

Produs |

Țara (țările) de origine sau de export |

Măsuri |

Trimitere |

Data de expirare |

|

Produse laminate plate din oțeluri electrice cu siliciu cu grăunți orientați |

Statele Unite ale Americii |

Taxă antidumping |

Regulamentul (CE) nr. 1371/2005 al Consiliului (JO L 223, 27.8.2005, p. 1) |

28.8.2010 |

|

Angajament |

Decizia 2005/622/CE a Comisiei (JO L 223, 27.8.2005, p. 42) |

(1) JO L 343, 22.12.2009, p. 51.

(2) Fax +32 22956505.

PROCEDURI REFERITOARE LA PUNEREA ÎN APLICARE A POLITICII ÎN DOMENIUL CONCURENȚEI

Comisia Europeană

|

15.4.2010 |

RO |

Jurnalul Oficial al Uniunii Europene |

C 95/10 |

AJUTOR DE STAT – ȚĂRILE DE JOS

Ajutor de stat C 11/09 [asociat NN 2/10 (ex N 429/09) și N 19/10] – Măsuri de recapitalizare în favoarea FBN și a grupului ABN Amro

Invitație de a prezenta observații în temeiul articolului 108 alineatul (2) din Tratatul privind funcționarea Uniunii Europene

(Text cu relevanță pentru SEE)

2010/C 95/07

Prin scrisoarea din data de 5 februarie 2010, reprodusă în versiunea lingvistică autentică în paginile care urmează acestui rezumat, Comisia a comunicat Țărilor de Jos decizia sa de a iniția procedura prevăzută la articolul 108 alineatul (2) din TFUE privind măsura menționată anterior.

Părțile interesate își pot prezenta observațiile privind măsura pentru care Comisia inițiază procedura în termen de o lună de la data publicării prezentului rezumat și a scrisorii de mai jos, la adresa:

|

European Commission |

|

Directorate-General for Competition |

|

State aid Greiffe |

|

Building/Office, J-70 03/225 |

|

1049 Bruxelles/Brussel |

|

BELGIQUE/BELGIË |

|

Fax +32 22961242 |

Aceste observații vor fi comunicate Țărilor de Jos. Păstrarea confidențialității privind identitatea părții interesate care prezintă observațiile poate fi solicitată în scris, precizându-se motivele care stau la baza solicitării.

REZUMAT

I. PROCEDURĂ

|

1. |

La 8 aprilie 2009, Comisia a inițiat procedura prevăzută la articolul 108 alineatul (2) din TFUE în ceea ce privește presupusul ajutor pentru Fortis Bank Nederland (FBN) și pentru activitățile din Țările de Jos ale ABN Amro (ABN Amro N). Comisia se îndoiește că statul olandez a acordat împrumuturi pentru FBN în condițiile pieței atunci când a preluat împrumuturile acordate de Fortis Holding pentru FBN, imediat după dezintegrarea suferită de Fortis Holding. De asemenea, Comisia are îndoieli în legătură cu faptul că statul olandez a plătit prețul pieței către FBN, atunci când a achiziționat ABN Amro N de la FBN, în decembrie 2008. |

|

2. |

La 17 iulie 2009, Țările de Jos au notificat Comisiei o recapitalizare în valoare de 2,5 miliarde EUR în favoarea activităților din Țările de Jos ale ABN Amro. Întrucât măsurile incluse în acest plan au fost implementate între timp, fără aprobarea Comisiei, aceasta consideră măsurile respective ca fiind un ajutor nenotificat. La 15 ianuarie 2010, Țările de Jos au notificat măsuri suplimentare în valoare de 4,39 miliarde EUR. |

II. DESCRIERE

|

3. |

Măsurile de recapitalizare notificate la 17 iulie 2009 constau în două măsuri: un swap pe risc de credit și emiterea unor titluri de valoare convertibile în mod obligatoriu. Prin intermediul unui swap pe risc de credit (credit default swap – CDS), guvernul olandez a vândut protecția creditului asupra unui portofoliu ipotecar olandez în valoare de 34,5 miliarde EUR al ABN Amro N, reducând astfel nevoile de capital ale acesteia cu 1,7 miliarde EUR. Pentru instrumentul său de protecție a creditului, statul olandez primește un comision anual de 51,5 puncte de bază (calculat ca un procent din valoarea portofoliului la începutul fiecărei perioade de referință). În plus, statul olandez a subscris un titlu de valoare de rang 1 (Tier 1) convertibil în mod obligatoriu (MCS) cu un cupon de 10 % pentru o valoare nominală de 0,8 miliarde EUR. Aceste două măsuri erau necesare pentru a acoperi deficitul de capital din cadrul ABN Amro Z (care reunește activele ABN Amro Holding care nu fuseseră împărțite între cei trei membri ai consorțiului care dețineau acest grup, și anume Santander, Royal Bank of Scotland și statul olandez) și pentru a acoperi un prim set de costuri de scindare. |

|

4. |

Măsurile suplimentare, care reprezentau o sumă de 4,39 miliarde EUR, vizau ABN Amro și FBN. Pentru a acoperi nevoile de capital ale FBN, statul va realiza un swap de 1,35 miliarde EUR cu FBN, între împrumuturile sale de capital de rang 2 (Tier 2) și capitalul de rang 1 (Tier 1) al FBN. Celelalte măsuri se referă la activitățile ABN Amro deținute de stat. Statul va subscrie emisiuni suplimentare de titluri de valoare convertibile în mod obligatoriu (MCS) pentru a acoperi costurile de scindare suplimentare, deficitul de capital care rezultă din vânzarea sub valoarea contabilă a New HBU și costurile de integrare. De asemenea, statul va plăti 740 de milioane EUR în numerar pentru a-și achita obligațiile față de ceilalți doi membri ai consorțiului. În plus, va fi dezvoltat un mecanism de garantare pentru obligațiile reciproce care rezultă, de asemenea, din vânzarea New HBU, aceasta din urmă fiind o precondiție pentru autorizarea fuziunii dintre FBN și ABN Amro N în temeiul normelor UE privind concentrările economice. Acest mecanism implică constituirea de către stat a unei contragaranții de 950 de milioane EUR pentru ABN Amro. ABN Amro va plăti o remunerație pentru această garanție de stat. |

III. EVALUARE

|

5. |

Comisia prelungește procedura demarată la 8 aprilie 2009 și va lărgi sfera de aplicare a investigării pentru a include noile măsuri. Comisia consideră că unele măsuri sau toate ar putea constitui ajutor de stat în sensul articolului 107 alineatul (1) din TFUE. De asemenea, Comisia are îndoieli în legătură cu faptul că planul de restructurare pe care l-a propus societatea este conform cu Comunicarea privind restructurarea. |

|

6. |

Din considerente de stabilitate financiară, Comisia consideră că toate măsurile sunt compatibile cu articolul 107 alineatul (3) litera (b) din TFUE ca ajutoare pentru salvare, până la 31 iulie 2010. |

IV. OBSERVAȚII FINALE

|

7. |

Pentru a se evita confuzii, vă rugăm să țineți seama de faptul că, datorită reorganizării întreprinderii, denumirile unora dintre entitățile menționate în decizie s-au modificat de la data luării deciziei, la 5 februarie 2010. Denumirea oficială a ABN Amro II este acum ABN Amro Bank NV, ABN Amro Bank NV se numește acum The Royal Bank of Scotland NV, iar ABN Amro Holding NV se numește acum The Royal Bank of Scotland Holding NV. |

TEXTUL SCRISORII

„The Commission wishes to inform the Netherlands that, having examined the information supplied by your authorities on the measures referred to above in favour of its ABN Amro activities and in favour of Fortis Bank Nederland (hereafter “FBN”), it has decided to extend the procedure laid down in Article 108(2) of the Treaty on the Functioning of the European Union (1) (“TFEU”) to these measures. Meanwhile, the Commission has decided to authorise these measures as rescue aid until 31 July 2010 based on Article 107(3)(b) TFEU.

1. PROCEDURE

|

1. |

On 8 April 2009 (2), the Commission initiated the procedure laid down in Article 108(2) TFEU with respect to alleged aid to FBN and the ABN Amro assets owned by the Dutch State. |

|

2. |

On 16 June 2009, the Dutch Ministry of Finance informed the Commission that it was preparing a EUR 2,5 billion recapitalisation plan enabling the separation of ABN Amro Holding into three parts. The Dutch authorities also indicated that at a later stage additional measures might be necessary, without being able to quantify these. |

|

3. |

On 17 July 2009, the Netherlands formally notified a plan with recapitalisation measures worth EUR 2,5 billion: a credit default swap (CDS) (with a capital relief effect of EUR 1,7 billion) and a Mandatory Convertible Security (MCS) of EUR 800 million. The MCS and the CDS were implemented on respectively 30 July 2009 and 31 August 2009. Given that the measures were implemented before the Commission took a decision on them, the case was moved from the register of notified aid into the non-notified aid register under number NN 2/10. |

|

4. |

By letter dated 24 July 2009, the Commission asked for more information, which the Dutch government provided on 19 August 2009 and on 2 September 2009. |

|

5. |

On 8 September 2009, the Commission asked for more information on the outstanding hybrids capital instruments of FBN and ABN Amro, which the Dutch government provided on 24 September 2009. |

|

6. |

On 1 September 2009, the Dutch government sent a non-paper in which it updated its ABN Amro plans. In an addendum to this non-paper sent on 10 November 2009, the Dutch government indicated that its new plan contained State support measures worth in total EUR 6,89 billion (3). Further details were provided in an explanatory note on 13 November 2009. |

|

7. |

On 4 December 2009, the Dutch government submitted a first draft of a business plan for the new entity that will result from the merger between FBN and the State's ABN Amro activities. |

|

8. |

On 15 January 2010, the Dutch government formally notified a complete restructuring plan including additional State aid measures worth EUR 4,39 billion that were not notified in July 2009. This notification was registered under number N 19/10. |

2. DESCRIPTION

2.1. The Beneficiary

|

9. |

In the Spring of 2007, Royal Bank of Scotland (RBS), Banco Santander and Fortis Holding created a new legal entity “RFS Holdings” to acquire ABN Amro Holding (4). The members of the consortium set out the arrangements for dividing up the operations of ABN Amro Holding in a so-called consortium and shareholders’ agreement (hereafter “CSA”). |

|

10. |

The consortium partners intended to split up ABN Amro Holding in three parts. In order to facilitate this break-up, the consortium members created so-called “tracking shares” representing the economic ownership of the businesses of each consortium member. As a result, Royal Bank of Scotland, Banco Santander and Fortis Holding became the economic owner of respectively the R-share, S-share and N-share (hereafter “ABN Amro R”, “ABN Amro S” and “ABN Amro N”). ABN Amro R comprised inter alia the Business Units (BU) Global Business and Markets, Global Transaction Services and the international network, ABN Amro S comprised inter alia BU Latin America and BU Antoveneta (Italy), while ABN Amro N comprised BU Netherlands (including the International Diamond and Jewelry Group) and BU Private Banking. |

|

11. |

Items that were not allocated to the individual consortium members were brought together in the so-called ABN Amro Z-share (hereafter ABN Amro Z), together with e.g. head office functions. Each consortium member holds a pro-rata stake (5) in ABN Amro Z. |

|

12. |

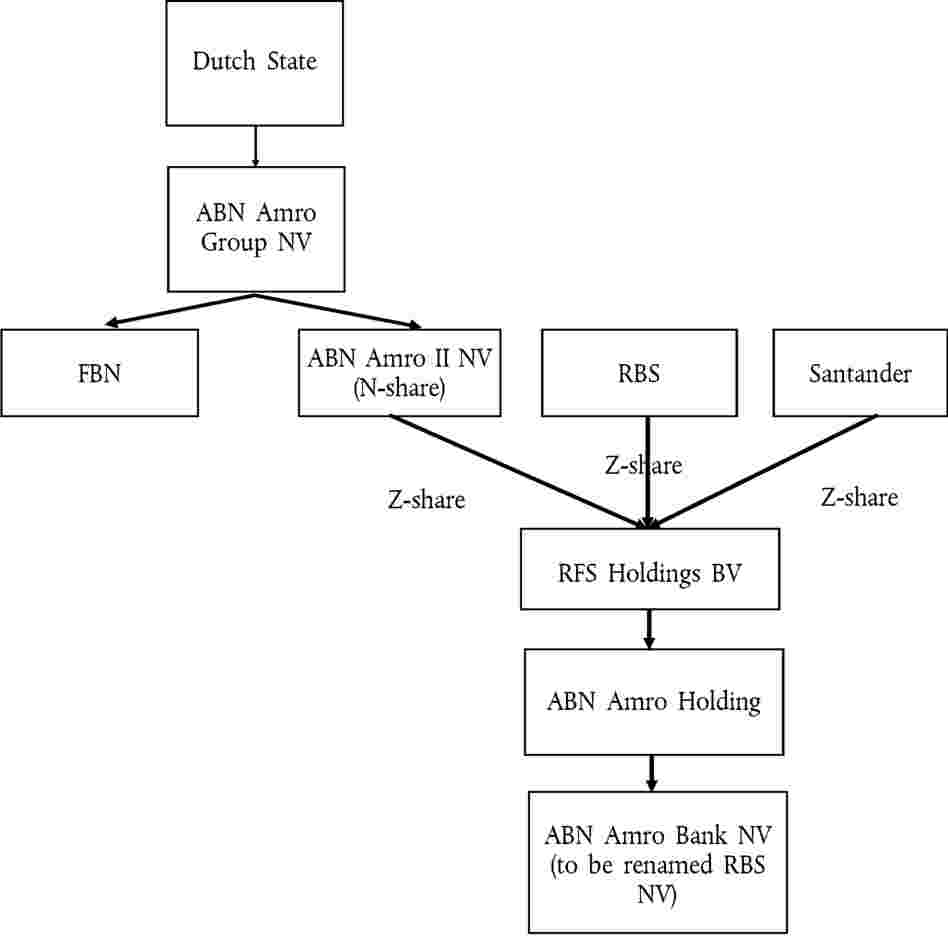

On 3 October 2008, the Dutch State acquired FBN from Fortis Holding, thereby also becoming the indirect owner of ABN Amro N and of 33,81 % of ABN Amro Z, since, within the Fortis Group, FBN was the legal owner of these shares. |

|

13. |

On 17 December 2008, the Dutch State became the direct owner of those shares after acquiring them from FBN. On 24 December 2008, RBS, Santander and the Dutch State signed an amendment to the CSA, by which the Dutch State officially took the place of Fortis Holding in the CSA. After the purchase of FBN by the Dutch State on 3 October 2008, Fortis Holding had remained formally a party to the CSA. However, the Dutch State committed to indemnify Fortis Holding for any charge it would face as a consequence of the continuation of its participation in the CSA. |

|

14. |

In November 2008, the Dutch State announced already that it wished to combine ABN Amro N (which had yet to be hived off) with FBN. Before this can happen, ABN Amro N needs to be split off in accordance with the provisions of the CSA. First a new division will be created (ABN Amro II) which will take place in the beginning of February 2010. The shares in this company (with a banking licence) would then need to be transferred to the Dutch State at the end of March 2010. Then ABN Amro II and FBN can merge and a new entity “ABN Amro Group NV” will be created. The legal merger is currently scheduled for 1 July 2010. |

|

15. |

The Commission decided (6) that a merger between ABN Amro N and FBN would create concentration problems in the Dutch banking market, especially in the segments of commercial banking and factoring. The Dutch government decided to sell a number of activities which were grouped in a new entity “New HBU” (7). On 19 October 2009, the Dutch State and Deutsche Bank concluded a Heads of Agreement document with regard to the sale of new HBU. A Share Purchase Agreement with Deutsche Bank was signed on 23 December 2009. |

|

16. |

The Dutch State will remain the owner of 33,81 % of ABN Amro Z but wants to limit the resources needed to manage this participation. Therefore, the Dutch State will probably transfer its stake in ABN Amro Z to ABN Amro II. The following table (Table I) explains the current structure of ABN Amro Holding and the anticipated de-merger of ABN Amro II.

|

|

17. |

The most likely future structure of ABN Amro according to the Dutch State is represented on the diagram in Table 2 below.

|

|

18. |

As indicated above, ABN Amro N consists of the Business Unit (BU) Netherlands (including the International Diamond and Jewelry Group) and the Business Unit Private Banking. |

|

19. |

BU Netherlands focuses on retail clients and small- to medium-sized enterprises. It offers a broad range of commercial and retail banking products and services. The company has a multi-channel service model, which consists of a network of approximately 600 branches, Internet banking facilities, customer contact centres and ATMs. |

|

20. |

In 2008, BU Netherlands had a balance sheet total of EUR 158,9 billion, risk-weighted assets (RWA) of EUR 83,9 billion and a net operating profit of EUR 306 million. For comparison, in 2007 the corresponding figures were EUR 141,7 billion, EUR 78,7 billion and EUR 882 million. BU Netherlands includes the results of the International Diamond and Jewelry Group, which reported a net operating profit of EUR 28 million in 2008. |

|

21. |

BU Private Banking offers private banking services to individuals with net invested assets of more than EUR 1 million. It has built up a network, through organic growth in the Netherlands and France and through acquisitions in Germany (Delbrück Bethmann Maffei) and Belgium (Bank Corluy). This BU also includes the insurance joint venture Neuflize Vie. |

|

22. |

In 2008, BU Private Banking had total assets of EUR 18,2 billion, RWA of EUR 7,8 billion, assets under management of EUR 102 billion and a net operating profit of EUR 165 million. The corresponding figures over 2007 were EUR 19,6 billion, EUR 8,2 billion, EUR 140 billion and EUR 298 million. |

|

23. |

The most recent audited financials of ABN Amro indicated that ABN Amro N was marginally profitable in the first nine months of 2009 (net profit of EUR 45 million compared with EUR 629 million in the first nine months of 2008). The drop in net profits was mainly attributable to lower net interest income (EUR 2 141 million in the first nine months of 2009 compared with EUR 2 407 million in the first nine months of 2008) and an increase of loan loss provisions (EUR 838 million in 2009 compared with EUR 383 million in 2008). |

|

24. |

ABN Amro Z contains tax assets, a number of participations (amongst others in the Saudi Hollandi Bank) and the remaining private equity portfolio. On the liabilities side there is a provision to settle obligations in respect of the U.S. Department of Justice, other provisions (partly personnel related) and inter-company financing of company assets. As stated above, the stake owned by the Dutch State represents 33,81 % of ABN Amro Z. |

|

25. |

At the end of 2008, FBN had total assets of EUR 184 billion and RWA of EUR 45,9 billion. While the company realised a net loss of EUR 18 billion in 2008 because of the goodwill write-down of its participation in ABN Amro Holding, its net operating profit amounted to EUR 604 million. The net result also suffered because of a credit provision of EUR 922 million (after tax) related to the Madoff fraud. At the end of 2008, FBN's Tier 1 ratio was 11,1 %. |

|

26. |

FBN is active in both the retail market and the wholesale market (commercial banking, corporate and public banking) and a number of specialized niches. |

|

27. |

Fortis Retail (representing roughly 27 % of total RWA of FBN) combines retail and private banking. In retail banking, the company has 156 branches, 2,1 million individual customers and 52 000 SME clients. With a market share of 5 %, Fortis Retail is the fourth largest bank in the Netherlands, after ING, Rabobank and ABN Amro. In private banking, the company (under the “Mees Pierson” brand name) has a leading position especially in the prime segment (customers with assets greater than EUR 1 million). |

|

28. |

Fortis Wholesale (representing roughly 73 % of total RWA of FBN) contains “commercial banking”, which has 23 business centres in the Netherlands to serve companies with a turnover up to EUR 250 million. Companies with a turnover of more than EUR 250 million and the public sector are serviced in another subdivision i.e. “Corporate & Public Banking”. The Wholesale division also includes a number of specialized niches (financial markets, securities financing, M&A advisory, equity capital markets, acquisition finance, private equity, syndications, export and project finance, trade services, transaction banking, factoring, brokerage, clearing and custody, fund administration etc.). |

|

29. |

In the first half of 2009, FBN realised a net profit of EUR 338 million. However, this profit included an exceptional capital gain of EUR 362,5 million. This profit could be broken down as follows: retail banking (+ EUR 62 million), private banking (– EUR 3 million), merchant banking (+ EUR 39 million) and other profit of + EUR 240 million. |

|

30. |

ABN Amro Group NV, the entity which will integrate ABN Amro N and FBN, will mainly focus on the Dutch market. The new group should have assets of around EUR 380 billion and once the merger has been fully completed, its revenues should be around EUR 8 billion. |

|

31. |

The new company will cover both “retail and private banking” and “commercial and merchant banking”. In retail banking, the company is expected to retain market shares of respectively 17,7 % and 18,8 % in “Mass Retail” and “Preferred Banking” (8). In private banking, the new group will have approximately 38 % of the Dutch market and the market share in “commercial and merchant banking” will be around 22,3 % (9). |

|

32. |

In terms of revenues, retail and private banking (with revenues of respectively EUR 3,2 billion and EUR 1,3 billion) should be slightly more important than commercial and merchant banking (with revenues of EUR 3 billion). The main focus will be on the Netherlands (with revenues of EUR 6,4 billion (or 80 % of the total)) versus EUR 1,5 billion abroad. |

|

33. |

ABN Amro Group NV will no longer include “New HBU” which will be divested in the framework of the merger remedy (10). New HBU contains the commercial bank Hollandsche Bank-unie, some ABN Amro sales offices (13 out of 78) and some ABN Amro Corporate Client Units (2 out of 5) and ABN Amro's factoring division IFN Finance. At the end of 2008, New HBU had total assets of EUR 12,5 billion and it employed 1 200 full time equivalents. |

2.2. Description of the State measures

|

34. |

In July 2009, the Dutch State notified several measures. The Dutch State granted a capital relief instrument (measure A with a capital relief effect of EUR 1,7 billion) and a mandatory convertible security (measure B1 of EUR 500 million) in order to fill a capital shortage at the level of ABN Amro Z of EUR 2,2 billion. At the same time, the Dutch State subscribed to another tranche of MCS (measure B2 of EUR 300 million) to cover a first tranche of separation costs. |

|

35. |

In January 2010, the Dutch State notified extra measures worth EUR 4,39 billion. The Dutch State will subscribe to additional MCS-instruments to cover additional separation costs (measure B3), the capital shortfall resulting from the sale of New HBU (measure B4) and integration costs (measure B5). The Dutch State will also swap its Tier 2 instruments in FBN into Tier 1 capital to improve the capital position of FBN (measure C). Finally the Dutch State will also pay consortium partners EUR 740 million in cash (measure D) and provide a guarantee to cover cross liabilities resulting from the sale of New HBU (measure E). |

2.2.1. Credit protection instrument to cover part of the capital shortfall of ABN Amro Z (Measure A, EUR 1,7 billion)

|

36. |

The Dutch mortgage portfolio covered by the CDS granted by the State represents around 39 % of ABN Amro N's total home loan portfolio. Mortgages are only included in the portfolio if they meet well-defined criteria (11). |

|

37. |

The portfolio insured by the State contains loans of 178,569 borrowers with an average net loan balance of EUR 193,478 and an average loan-to-foreclosure-value ratio of 92,4 %. The average maturity of a loan in the portfolio is 338 months. |

|

38. |

For this credit protection instrument, the Dutch State receives an annual fee of 51,5 basis points (calculated as a percentage of the portfolio value in the beginning of each reference period). |

|

39. |

This fee was based on the capital equivalent cost: the Dutch State wanted a 10 % return on the capital released as a result of the CDS (i.e. 10 % on EUR 1,7 billion), which is equivalent to 51,5 basis points of the initial portfolio of EUR 34,5 billion. |

|

40. |

Each year, ABN Amro N keeps a first loss tranche of 20 basis points (calculated as a percentage of the initial portfolio value), but the State has a claw-back clause, which is triggered if years with credit losses of less than 20 basis points were to follow years with credit losses of more than 20 basis points. Since the first loss clause is calculated as a percentage of the initial portfolio value, when clients start to repay their mortgage loan it will represent an increasing percentage of the outstanding portfolio value. |

|

41. |

ABN Amro N also keeps a vertical slice of 5 % of the remaining risk. |

|

42. |

The pricing of the credit protection instrument will not be adjusted once ABN Amro N fully adopts Basel II capital rules (12), even though the capital relief effect of the CDS will be smaller then. |

|

43. |

In principle, the CDS-contract has a maturity of 7 years. ABN Amro N has however call options enabling the early termination of the contract on a number of reference dates (November 2009, January 2010, April 2010, July 2010, October 2010, January 2011 and January 2012). The State also has a call to terminate the transaction on the condition that the termination of the contract does not endanger the capital position of ABN Amro N. |

2.2.2. Mandatory Convertible Security to cover part of the capital shortfall of ABN Amro Z (Measure B1, EUR 500 million)

|

44. |

The Mandatory Convertible Security (MCS) (13) qualifies as hybrid Tier 1 capital, will carry a coupon of 10 % and will automatically convert into shares of ABN Amro II at the time of the separation of ABN Amro N from ABN Amro Holding. At that point in time, it will qualify as core Tier 1 capital. If, at the time of conversion, the Dutch State is still the only shareholder of ABN Amro II, the conversion price for the MCS will be equal to its nominal value. If there are new shareholders involved, the State and ABN Amro II management will ask a third party to determine the fair value of the newly created entity and the conversion will take place at the fair value price. If the regulatory ratios of ABN Amro Holding would fall below certain thresholds before the separation, the MCS would convert into Non-cumulative Modified Securities. The only difference with the original securities is that the coupon payments would no longer be cumulative. Under IFRS rules however, these new securities would qualify as equity. |

2.2.3. Mandatory Convertible Security to cover separation costs (Measures B2 and B3, EUR 1,08 billion)

|

45. |

The Dutch State will subscribe to extra MCS to cover separation costs. A first tranche (measure B2) was already notified in July 2009 (roughly EUR 300 million), with the remainder being notified in January 2010 (measure B3). A description of the instrument is set out in paragraph 44 above. The full amount of EUR 1,08 billion (i.e. measure B2 and measure B3 together) includes well-defined separation costs of EUR 480 million, costs of EUR 90 million related to the set-up of a money market desk and a buffer of EUR 500 million. |

|

46. |

The Dutch State estimates that the separation of ABN Amro II from its former parent company will cost in total EUR 480 million. This includes cross liabilities exposure (EUR 45 million), unwinding of risk allocation letters (EUR 37 million), repurchase of securitization notes (EUR 57 million), the transfer from ABN Amro R of trading-related market risk related to ABN Amro II clients (EUR 47 million), discontinuation of capital relief instruments (EUR 64 million) and general separation and unwinding costs (EUR 230 million). |

|

47. |

After the separation from the parent company, ABN Amro II also needs EUR 90 million of extra capital if it is to set up a money market desk on its own. |

|

48. |

Additionally, the Dutch State will inject an extra EUR 500 million, as a buffer covering unexpected needs in the course of what is a very complex disintegration process. |

2.2.4. Mandatory Convertible Security to cover capital shortfall due to sale of New HBU (Measure B4, EUR 300 million)

|

49. |

Under the 2007 merger decision (14), FBN can be integrated with ABN Amro N only if New HBU is sold. The Share Purchase Agreement was signed with Deutsche Bank on 23 December 2009. This sale has a negative capital impact on ABN Amro N of EUR 470 million. Since ABN Amro N does not have sufficient means to compensate for this, the State expects that it will have to contribute EUR 300 million. This contribution will be made by subscribing to additional MCS for this amount. |

2.2.5. Mandatory Convertible Security to cover integration costs (Measure B5, EUR 1,2 billion)

|

50. |

The Dutch authorities claim that the merger between FBN and ABN Amro N will ultimately lead to synergies of EUR 1 billion per year (before tax). In order to reap the full benefit of these synergies, the merger will have to be implemented and this will lead to upfront integration costs of EUR 1,2 billion (after tax). Since these entities do not have sufficient capital to bear these costs, the State will subscribe to additional MCS for this amount. |

2.2.6. Swap of Tier 2 hybrid capital instruments of FBN into core Tier 1 capital (Measure C, EUR 1,3 billion)

|

51. |

In order to comply with the capital requirements of the DNB (15), FBN needs to rebalance its capital structure. This requires an increase of core Tier 1 capital of EUR 1,26 billion. In addition, the separation from Fortis Holding, its former Belgian parent company, leads to extra costs of EUR 90 million, which relate to the set-up of a treasury desk, Basel models, licenses and consultancy services. |

|

52. |

Measure C thus rebalances the capital structure of FBN. FBN needs more Tier 1 capital. The State, which purchased some Tier 2 loans to FBN from Fortis Holding at the time of the acquisition of FBN (16), will provide the Tier 1 capital needed by exchanging some of these Tier 2 loans into Tier 1 capital. According to the Dutch authorities, this is equivalent to a scenario in which FBN repays to the State the Tier 2 capital instruments at par, followed by a Tier 1 capital injection by the State of the EUR 1,35 billion amount. The transaction does not involve any cash. |

2.2.7. Payment obligations towards other consortium members (Measure D, EUR 740 million)

|

53. |

Certain payment obligations have become apparent during the de-merger process of ABN Amro Holding. The CSA contains a number of general principles to resolve such issues but the exact amounts result from a negotiating process in which the Dutch State (and Fortis Holding before it) participated. |

|

54. |

The total amount of EUR 740 million relates to the following:

These cash outflows will partly be compensated by the fact that the Dutch State will receive EUR 31 million from the other consortium partners related to stranded costs. |

|

55. |

The balance of the payment obligations in respect of other consortium shareholders (i.e. EUR 740 million) will be paid in cash, part of it directly to the other consortium members, part of it to ABN Amro Z. |

2.2.8. Cross liabilities (Measure E, EUR 950 million)

|

56. |

Even after the divestment of New HBU, ABN Amro II will remain liable towards creditors of New HBU if New HBU is unable to meet its obligations towards its own creditors (and vice versa for new HBU which will also face cross liabilities). The Dutch State and Deutsche Bank (i.e. the purchaser of New HBU) agreed that new HBU and ABN Amro II would indemnify each other for these cross liabilities and provide to each other collateral, so as to reduce the induced regulatory capital requirements to a desired 20 %. As a result of this agreement, ABN Amro II will have to provide collateral to New HBU for an amount up to EUR 950 million (which will decline over time as liabilities mature) for the liabilities of New HBU towards ABN Amro II and towards ABN Amro Bank NV (to be renamed RBS NV). Since ABN Amro II does not have enough capital to provide the collateral needed in respect of the liability towards ABN Amro Bank NV, the State will provide a counter-indemnity for the entire amount (EUR 950 million). |

|

57. |

The Dutch State has priced this risk as if it was a State guarantee on ABN Amro Bank NV subordinated debt. The pricing methodology of the Dutch State is based on the ECB Recapitalisation Recommendation i.e. 200bp plus the median CDS-spread (17).

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

2.3. Description of presented business plan

|

58. |

In its business plan, the new ABN Amro Group has provided relatively detailed financial projections for the period 2009-2012 in both a base case and a best case scenario. For 2012, the company has also calculated a run-rate (19) profit. The company also presented information on its exit strategy and on the measures it has taken in terms of burden sharing/limits to distortion of competition. |

|

59. |

Both ABN Amro N and FBN are expected to report losses at the end the fiscal year 2009 of respectively of — EUR 1,509 million and — EUR 108 million. This is partly due to extraordinary costs related to the separation from their respective former parent companies. The decline in the net interest income and the increase in the provisions for bad loans contribute also to this negative result. |

|

60. |

In a base case scenario, the new ABN Amro Group expects to return to profitability in 2011 after another negative year in 2010 (net profit of — EUR 838 million, EUR 504 million and EUR 1,391 million in respectively 2010, 2011 and 2012). The company indicates that its run-rate profits in 2012 should amount to EUR 1,627 million. This profitability increase is due to better revenues (21) which improve on the back of higher net interest income and higher other revenues. At the same time, direct costs (22) should decrease on the back of synergies and also loan loss provisions should drop after peaking in 2009/2010. |

|

61. |

Starting from the 2012 run-rate figures, the new ABN Amro Group would have a return on equity (RoE) of 11,4 % and a cost/income ratio of 63 %. |

|

62. |

The best case scenario changes two key assumptions. The interest margin is 10 % higher than in the base case (23), while personnel costs rise by 2 % (rather than by 3,75 %). |

|

63. |

The profits in the best case scenario are somewhat higher than in the base case scenario (EUR 130 million in 2010, EUR 260 million in 2011 and EUR 390 million in 2012). This scenario would lead to a 2012 run-rate return on equity of 13,5 % and a cost/income ratio of 59 %. |

|

64. |

In its business plan, the Dutch State also provides more information on its exit strategy. The Dutch State contends that it does not see itself as a long-term investor in financial institutions, which implies that it will sell its shareholding in new ABN Amro Group at the appropriate time. The Dutch State indicates that the timing of the exit will take place once 1. the new group has been able to show a positive track record (especially in terms of synergies); and 2. market valuations for large financial groups have further normalized. |

|

65. |

The Dutch State already plans a gradual repayment of the support provided to new ABN Amro Group before the full divestment of its shareholding. In the current projections, new ABN Amro Group would call the capital relief instrument in January 2011. The Dutch State also indicates that it will manage closely the capital position of the group encouraging it to pay out any capital above a prudential limit agreed with the DNB. As the only shareholder of new ABN Amro Group, the State can steer the dividend policy (obviously within the limits set by the capital requirements of the financial supervisor). |

|

66. |

The Dutch State underlines that the aided banks have already divested a number of businesses. |

|

67. |

First, to sort out concentration problems resulting from the merger between ABN Amro N and FBN, the Dutch State implemented a merger remedy. It sold New HBU to Deutsche Bank thereby reducing the presence of the new merged entity in “commercial banking” and “factoring”. |

|

68. |

In addition, in September 2009, FBN (and its partner BGL (24)) decided to sell Intertrust to private equity company Waterland. Intertrust is one of the largest players in global trust and corporate management, helping its clients with corporate financial planning, management and operational issues, administration and accounting and asset planning services. Intertrust employs 1 000 experts in 19 countries. Intertrust's income and RWA in 2008 amounted to respectively EUR 170 million and EUR 800 million. |

|

69. |

In 2008, New HBU (including IFN) reported income of EUR 460 million and RWA of EUR 10,3 billion. |

|

70. |

In 2008, New HBU and Intertrust together had revenues of EUR 630 million and RWA of EUR 11,1 billion. This represents respectively 8 % (revenues) and 7 % (RWA) of the new ABN Amro Group. |

|

71. |

In addition, exclusive negotiations have been started with Credit Suisse (25) to sell the FBN division PFS (“Prime Fund Solutions”). PFS provides fund services to the alternative asset management industry allowing clients to focus fully on their investment process. PFS services include: administration, banking, custody and financing and its clients range from boutique asset managers to large scale global institutions such as pension funds and sovereign wealth funds. The EUR 922 million provision related to the Madoff-fraud which FBN registered in 2008 stemmed from this division. |

|

72. |

On 31 July 2009, FBN acquired Fortis Clearing Americas from Fortis Bank Belgium for a price of approximately USD 120 million. This transaction was necessary to correct a misalignment which resulted from the break-up of Fortis Holding. FBN owned the BU Brokerage, Clearing and Custody and all the offices related to this business except the Chicago office (i.e. Fortis Clearing Americas) were within the legal scope of FBN. |

3. POSITION OF THE NETHERLANDS

|

73. |

The Dutch State argues that the Commission should take into account that the Dutch State was obliged to buy FBN in very special circumstances. When Fortis Holding encountered important problems in September 2008, the Dutch State had no choice but to step in, to preserve financial stability. By acquiring FBN (including ABN Amro N and 33,8 % of ABN Amro Z), the Dutch State became de facto a partner in the CSA, so that it took over a number of contractual obligations. This obliged the Dutch State to implement the de-merger process as described in the CSA and is for instance at the basis of the obligation to fill the regulatory capital shortfall in ABN Amro Z (measure A) and the obligation to settle remaining issues with other consortium shareholders (measure D). |

|

74. |

The Dutch State claims to have based the ABN Amro recapitalisation plan on the principles set forward in the Banking Communication (26) and the Recapitalisation Communication (27) of the Commission. In general, the Dutch State argues that the measures it has implemented were well-targeted, proportionate to the challenges faced and designed in such a way to minimize negative spill-over effects to competitors. |

|

75. |

The Dutch State argues that the financial means granted to ABN Amro N (measure A and measure B1) to cover the capital shortage of the Z-share is not State aid. The Dutch State indicates that the CSA implied that it had no choice but to fill the capital shortage of ABN Amro Z. It argues that the available capital position of ABN Amro N did not change as a result of the intervention, which implies that its relative position versus competitors has not changed because of these measures. According to the Dutch State, it has merely used ABN Amro N as an intermediate vehicle to sort out the ABN Amro Z capital shortfall, which was actually the responsibility of the Dutch State as a shareholder of ABN Amro Z. |

|

76. |

If the Commission were to consider measures related to the capital shortage of ABN Amro Z as State aid, the Dutch State argues that the Impaired Asset Communication (28) does not apply to the credit protection instrument of ABN Amro N. According to the Dutch State, the protected assets cannot be considered “impaired” as that term is used in the Communication, while there is also no uncertainty as to their valuation. Should the Commission not share this point of view, the Dutch government contends that ABN Amro N's CDS still complies with the general principles put forward in that Communication. Besides, it argues that the credit protection instrument is necessary and proportional, while it keeps competition distortions to the minimum. |

|

77. |

Practical and legal obstacles explain why the Dutch State favours the current solutions (with inter alia a CDS in combination with a mandatory convertible security) over, for instance, a classic cash capital injection. Any cash injected in ABN Amro Holding cannot be ring-fenced and might potentially become available to businesses that are not owned by the Dutch State. In this regard, the Dutch government points out that ABN Amro R is also not sufficiently capitalised and that the unwinding of ABN Amro Holding can only go ahead once also this problem has been addressed by RBS. |

|

78. |

On the Credit Protection Instrument, the Dutch State underlines that the first loss tranche of 20 basis points exceeds the provisions made by ABN Amro N on the covered portfolio, which reflect the credit losses expected by ABN Amro N. |

|

79. |

The Dutch State also points out that the Credit Protection Instrument becomes relatively unattractive after the full implementation on Basel II. |

|

80. |

The Dutch State considers the remuneration of the MCS to be higher than is required in paragraph 27 of the Recapitalisation Communication, underlining that the coupon is 10 %. |

|

81. |

The Dutch State claims that the separation costs and the capital shortfall related to the HBU-divestment (measures B2, B3 and B4) are obligations of the State as a shareholder of ABN Amro N and that ABN Amro N in the end will not have more financial means. The Dutch State argues that it is merely complying with a number of obligations it inherited from Fortis Holding. It argues that Fortis Holding took the decision to de-merge ABN Amro N and to merge the two entities and that the Dutch State now has to bear the costs of these decisions of Fortis Holding. |

|

82. |

The Dutch State indicates that the State money granted to finance integration costs (measure B5) should be seen as a rational investment, leading to healthy returns in the form of synergies. The Dutch government estimates these synergies at around EUR 1 billion a year (pre-tax). |

|

83. |

The Dutch State acknowledges that FBN will benefit from the injection of Tier 1 capital (measure C). At the same time however, the Dutch State underlines that the Commission should also take into account that FBN will repay the existing Tier 2 instruments at par, while the market now typically prices this type of instruments at a discount. The Dutch State claims, based on market data, that the repayment at par implied a benefit of EUR 200 million for the State, i.e. that the market value of these instruments was EUR 200 million below their nominal value. This would imply that the State aid component in this measure amounted to EUR 1,15 billion (rather than EUR 1,35 billion). |

|

84. |

The Dutch State indicates that the payment of EUR 740 million (measure D) is not a payment to ABN Amro N. It underlines that the payment stems from its contractual obligations under the CSA. |

|

85. |

Also with respect to the State counter guarantee on the cross liabilities linked to the divestment of New HBU, the Dutch State claims that these resulted from the merger decision which was already taken by Fortis Holding in 2007. It contends that the underlying business of ABN Amro N will not benefit from the support provided to cover these costs (measure E). |

|

86. |

The Dutch State considers the cross liabilities solution to be in line with the Commission Communications and it underlines that is has based its pricing on the ECB Recapitalisation Recommendations. |

|

87. |

The Dutch State also attracts the attention of the Commission to the fact that the sale of New HBU has been very burdensome for the Dutch State and for ABN Amro N. New HBU was sold below book value and ABN Amro N also accepted a credit umbrella in which it took a 75 % of the credit losses of the existing loan portfolio up to a maximum of EUR 1,6 billion. The Dutch State underlines that the HBU transaction led to an economic loss of EUR 1,2 billion, while it also had a negative capital impact of EUR 470 million. |

4. ASSESSMENT

4.1. Existence of aid

|

88. |

According to Article 107(1) TFEU, a State measure can be classified as State aid when 1. it gives a selective economic advantage; 2. it is financed by State resources; 3. it distorts or threatens to distort competition; and 4. it affects the trade between Member States. |

|

89. |

The Commission observes that all the measures which are the object of this decision clearly involve State resources since they are directly financed by the State (condition 2). As regards condition 4, the Commission observes that all the measures threaten to affect trade between Member States since both ABN Amro N and FBN are active on foreign markets, while subsidiaries of companies from other Member States compete with ABN Amro N and FBN on the Dutch market. The reinforcement of these two banks also threatens to discourage entry by foreign banks on the Dutch market. Because of the aid allowing the separation from the respective mother company and then the merger, ABN Amro N and FBN are stronger companies on the market, which distorts competition (condition 3). The following paragraphs will discuss more in detail whether the State measures described above represent a selective advantage to ABN Amro N and FBN (condition 1). |

|

90. |

As regards measures A and B1 they seem to convey an advantage to ABN Amro N since they provide it with a guarantee and capital that it could not have found on the market. The Dutch State claims that these measures were granted to cover the capital shortage of ABN Amro Z, which has only limited economic activities. The Dutch State argues that this was an obligation of the State as a shareholder of the Z-share and as partner under the CSA. The Dutch State indicates that this obligation was not linked to ABN Amro N and therefore does not provide any advantage to ABN Amro N, i.e. the lines of business which will be transferred to ABN Amro II. According to the Dutch State, ABN Amro N is only used as an intermediate vehicle to settle the obligation of the State with respect to ABN Amro Z. At separation, ABN Amro N will have to leave EUR 2,2 billion to fill the shortage of ABN Amro Z and will therefore not receive any advantage. The Commission observes however that ABN Amro N and Z do not have separate legal status and that the Dutch State manages its ABN Amro activities (both ABN Amro N and Z) as a single economic entity. The Dutch authorities have provided no proof that ABN Amro N and Z are clearly ring-fenced from one other. On the contrary, there are indications that the profits and cash flows of the two units have not been clearly separated, especially in the past. In 2008, the consortium shareholders decided for instance to transfer EUR 1 billion in Unicredito shares from ABN Amro Z to the other entities (ABN Amro R, S and N), without any compensation. The Commission also notes that ABN Amro Z incurs the costs of head office functions, thereby providing a clear advantage to ABN Amro N apparently without any compensation. In other words, it seems that the capital shortage of ABN Amro Z partially stems from the transfer of net assets to ABN Amro N and from the provision of head office functions to ABN Amro N. By filling the capital shortage of ABN Amro Z, the Dutch State seems therefore to pay the remuneration for an advantage granted to ABN Amro N. It seems therefore that ABN Amro N should be seen as a beneficiary of the measures, since, if the Dutch State did not fill the capital shortage of ABN Amro Z, the two other consortium members would try to repatriate assets obtained by ABN Amro N to ABN Amro Z or directly to ABN Amro R and S. At this stage, the Commission can therefore not take a final view on the existence of an advantage to ABN Amro N financed by State resources. The Dutch government is invited to provide more evidence of its claim that the capital shortage at the level of ABN Amro Z existed already when it acquired FBN and its ABN Amro assets on 3 October 2008 and to precisely quantify the different causes of this capital shortage. |

|

91. |

The recapitalisation granted to finance the separation costs of EUR 1,08 billion (measure B2 and B3) seems to constitute State aid to ABN Amro N. By supporting these costs for ABN Amro N, the State provides an advantage to ABN Amro N. It is the Commission's understanding that the Dutch State had to inject capital because ABN Amro N could not self-finance these costs. The Commission also observes that the use of a significant fraction of the total amount (i.e. the extra precautionary buffer of EUR 500 million) is not specified and remains rather unclear. |

|

92. |

The sale of New HBU (measure B4) leads to a capital shortage at the level of ABN Amro N. ABN Amro N is able to cover only part of this. The fact that the State has to make up the balance (i.e. approximately EUR 300 million) represents therefore an advantage to ABN Amro N. The Dutch authorities claim that the sale of New HBU was an obligation of the State as a successor of Fortis Holding, following from the Commission's merger decision of 2007 (29); the support granted to ABN Amro N only covers the costs caused by this sale without granting any net advantage to ABN Amro N. The Commission cannot accept this claim at this stage. It observes that the aid finances the consequences of the sale of New HBU, a condition sine qua non for the merger between ABN Amro N and FBN. In other words, this aid allows a merger which will make ABN Amro N a stronger bank on the Dutch market. Moreover, the Commission notes that it was the decision of the Dutch State to merge FBN and ABN Amro N. When the Dutch State acquired FBN (including ABN Amro N and 33,8 % of ABN Amro Z), there was no legal obligation to pursue a merger. The Dutch State could for instance also have chosen to manage the two companies as separate entities. The Dutch State has chosen to pursue the merger and therefore the claim that it inherited the obligation to sell New HBU from Fortis Holding is only partially correct. The same reasoning holds for the guarantee given for cross liabilities stemming from the sale of New HBU (measure E): there was no legal obligation to merge FBN and ABM Amro N and the cross liabilities are a cost stemming from the sale of New HBU, a sale had to be implemented following the decision to merge both banks in order to make them a stronger competitor on the Dutch market. |

|

93. |

The Commission considers that the capital injection of EUR 1,2 billion capital (measure B5) to finance integration costs provides an advantage to ABN Amro N. Indeed, it provides additional resources to the company and without this capital injection the merger could not be financed. |

|

94. |

As regards the swap of EUR 1,35 billion of Tier 2 hybrid loans to FBN for Tier 1 capital (measure C), it seems to be an advantage to FBN. FBN needs more Tier 1 capital to meet the capital requirements of the DNB and it is not able to finance these by its own means (including retained earnings). The Dutch authorities claim that the amount of State aid implied in this measure is not 100 % since it should take into account the fact that this exchange of an existing subordinated claim is equivalent to FBN repaying the State's Tier 2 instruments at par, which seems to be above current market price of similar hybrid instruments. The Commission observes in this respect that several banks have indeed been able to repurchase their subordinated debt instruments at a significant discount in the last quarters. Based on a preliminary assessment, the claim of the Dutch government that the State aid implied in this measure amounts to EUR 1,15 billion seems a reasonable estimation. |

|

95. |

As for the settlement of payment obligations as regards other consortium members (measure D), the Commission can only accept that it is not State aid if it does not imply a transfer of net assets or another advantage to ABN Amro N. At first sight, it seems that the EUR 740 million payment to the other consortium members based on CSA provisions mainly relates to adjusted purchase prices for existing assets and does not stem from the transfer of new assets to ABN Amro N, in which case there would be an advantage to the latter. This payment of EUR 740 million does not seem to convey an advantage to the consortium members either, since the State is contractually obliged to pay this amount under the CSA and if it does not pay it, consortium members could sue the State to make these payments or prevent the transfer of the BU Nederland and BU Private Banking to the Dutch State. At this stage, it seems that measure D does not convey any advantage. The Commission can however not exclude that a more in-depth analysis of the case will reveal that there is nevertheless an advantage. It can therefore not take a final position on the absence of advantage at this stage. The Dutch State is invited to provide more information ensuring that there is no transfer of net assets in favour of ABN Amro N involved in measure D. |

|

96. |

The Commission observes that the Dutch authorities claim that certain of the measures constitute rational business decisions, increasing the value of the banks owned by the Dutch State. In particular, these measures are necessary to allow the merger between ABN Amro N and FBN, which will generate annual synergies larger than EUR 1 billion. Based on a preliminary assessment, the Commission considers that the private investor test cannot be applied to the present case. The State became the owner of FBN and ABN Amro N and Z on 3 October 2008 in the framework of a transaction aiming at rescuing these banks and which would not have been acceptable to a private investor, as concluded in paragraph 50. of the decision of 3 December 2008 on the aid to Fortis Bank S.A. (30). In other words, all the State measures which are assessed in the present decision that aim at preserving or increasing the value of ABN Amro N and FBN are the consequence of an aid measure, i.e. the rescue of these banks on 3 October 2008. Since these State measures are the direct consequence of an aid measure and since they are taken in framework of the restructuring of these two entities which directly follows from this purchase, the behaviour of the State cannot be compared to that of a private investor. A private investor would not have found itself in the situation of the State, i.e. without the State aid of 3 October 2008 Fortis Holding including its subsidiary FBN would have disappeared. |

|

97. |

In conclusion, based on a preliminary assessment, the Commission cannot exclude that the measures A, B1, B2, B3, B4, B5, C, D and E constitute State aid. Measure C benefits FBN, while the other measures provide an advantage to ABN Amro N. Any aid contained in these measures would come on top of any aid contained in the measures covered by the opening decision of 8 April 2009. |

|

98. |

The Commission invites the Dutch authorities and the parties concerned to submit their comments on these preliminary conclusions concerning the existence of aid. |

4.2. Compatibility of the alleged aid measures as restructuring aid

4.2.1. Legal basis for the assessment of compatibility

|

99. |

Article 107(3)(b) TFEU allows aid to remedy a serious disturbance in the economy of a Member State. In this regard, it is however important to underline that the Court of First Instance has emphasized that this provision should be applied restrictively (31), which implies that the economic disturbance should have nation-wide implications and not just regional. |

|

100. |

The Commission notes that ABN Amro N and FBN are leading Dutch banks with a nation-wide branch network and top market positions in a wide range of segments on the Dutch retail and SME banking market. In the context of the various uncertainties surrounding the current recovery from the global financial and economic crisis, the discontinuity of these banks would create a serious disturbance for the Dutch economy and therefore State aid from the Dutch government can be assessed under Article 107(3)(b) TFEU. |

|

101. |

The Commission has explained in the Restructuring Communication how it will assess restructuring aid to banks in the current crisis: (i) the Member State should commit to implement a restructuring plan restoring the long-term viability of a bank without reliance on State support; (ii) the bank and its capital providers should contribute to the financing of the restructuring costs as much as possible with their own resources thereby limiting the total amount of State aid necessary; and (iii) the plan should contain sufficient measures to limit distortions of competition, which is most relevant in business segments where the bank's relative position remains strong (32). |

|

102. |

In addition to complying with the Restructuring Communication, the form of the aid measure has to comply with the corresponding Communication: the State guarantee measures (measure E) have to comply with the Banking Communication and the recapitalisation measures (measures A, B1, B2, B3, B4, B5, C and D) have to comply with the Recapitalisation Communication. |

|

103. |

As regards measure A, the guaranteed portfolio is not made of impaired assets. However, the Commission considers that it should be assessed by analogy on the basis of the principles laid down in the Impaired Assets Communication. The principles developed in that Communication aim at ensuring that State guarantees on bank assets are done under conditions which ensure that these aid measures are well-targeted, that the aid is limited to the minimum and that distortions of competitions are limited. Since measure A is a State guarantee on a portfolio of loans held by ABN, the same principles should be applied to it. |

4.2.2. Assessment of measure A under the principle laid down in the Impaired Assets Communication

|

104. |

Based on a preliminary assessment, the Commission acknowledges that the credit protection instrument has been developed to sort out a very particular problem, namely the need to address the shortage of regulatory capital identified by the Dutch supervisor. The latter will not authorise the separation of ABN Amro N before this shortage is solved. As such, the credit protection measure is intrinsically linked to the spin-off schedule. Within this specific framework, the Commission notes that the choice of the Dutch State to grant a credit protection instrument instead of a standard recapitalisation has been only dictated by the fact that the N-share represents per se only economic rights but not a separate legal entity; in case of a standard capital injection in ABN Amro, the Dutch State runs the risk that the money injected would benefit other parts of the group, i.e. the other consortium members. The credit protection instrument provides a capital relief and therefore covers the capital shortage without implementing a standard capital increase. |

|

105. |

Moreover, at this stage, the Commission has no reason to believe that the protected portfolio contains “impaired” assets. Indeed, it seems that expected losses of the guaranteed portfolio are very low and that all the underlying assets are currently performing without any exception. They are also considered as safe by the market. In conclusion, the Commission acknowledges that the situation is different to that of other cases with impaired assets. In spite of this, as explained in paragraph 103. above, the Commission thinks that the measure should comply with the general principles underlying the Impaired Asset Communication. In addition, when assessing measure A as a restructuring measure lasting longer than six months, the guiding principles of the Impaired Asset Communication should be complied with. |

|

106. |